The stock market remains on edge as the war in Iran enters its 4th week. As we have seen since the start, war is messy and difficult to predict. We will continue to see fluctuations based on "news" from various sources. The fact of the matter is the longer there is unrest in the middle east, the more structural damage we will see. At at time where economic growth was weakening, inflation was rising, and the stability of the AI/Data Center buildout was being questioned, market participants are justifiably concerned.

This week once again, I'm going to keep my commentary brief. There's no sense adding to the endless parade of people pontificating about the end of the war and the impact it will have. NOBODY knows how this will end and what the short and long-term damage will end up being. Instead we will again focus on the data. Most people are focusing on the stock market as the S&P 500 approaches "correction" territory (down 10%). I understand the need for simple terms and definitions such as a correction being down 10% and a bear market at 20%, but in reality, there is a lot more to it.

A "correction" implies stocks just got a little ahead of themselves and the prices came back down to a more reasonable level. Is a decline of 10% the "reasonable" level? If the war is over quickly and the concerns over AI/Data Center financing/growth goes away, then maybe down 10% is what we needed to see. However, if we see a prolonged conflict along with some other structural issues impacting the economy, a decline of 10% is just the beginning. Again, nobody knows the duration or impact of the war in Iran, so it's too early to determine whether this correction is a good buying opportunity.

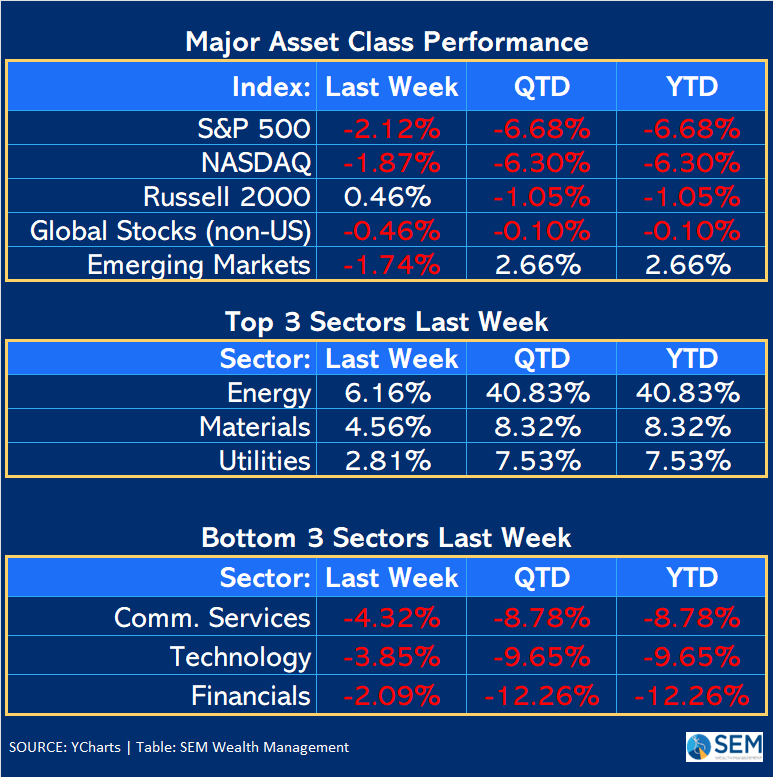

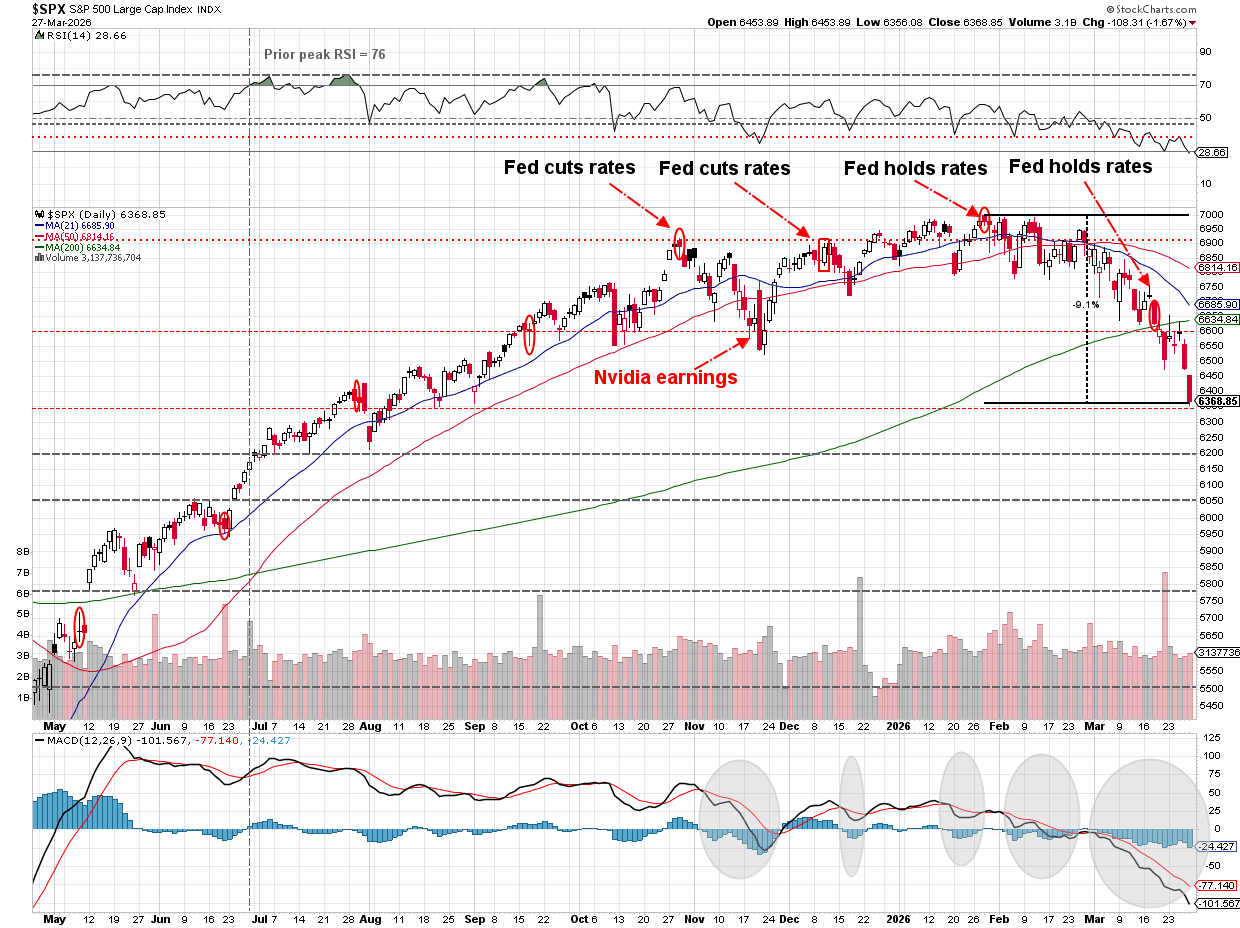

Market Charts

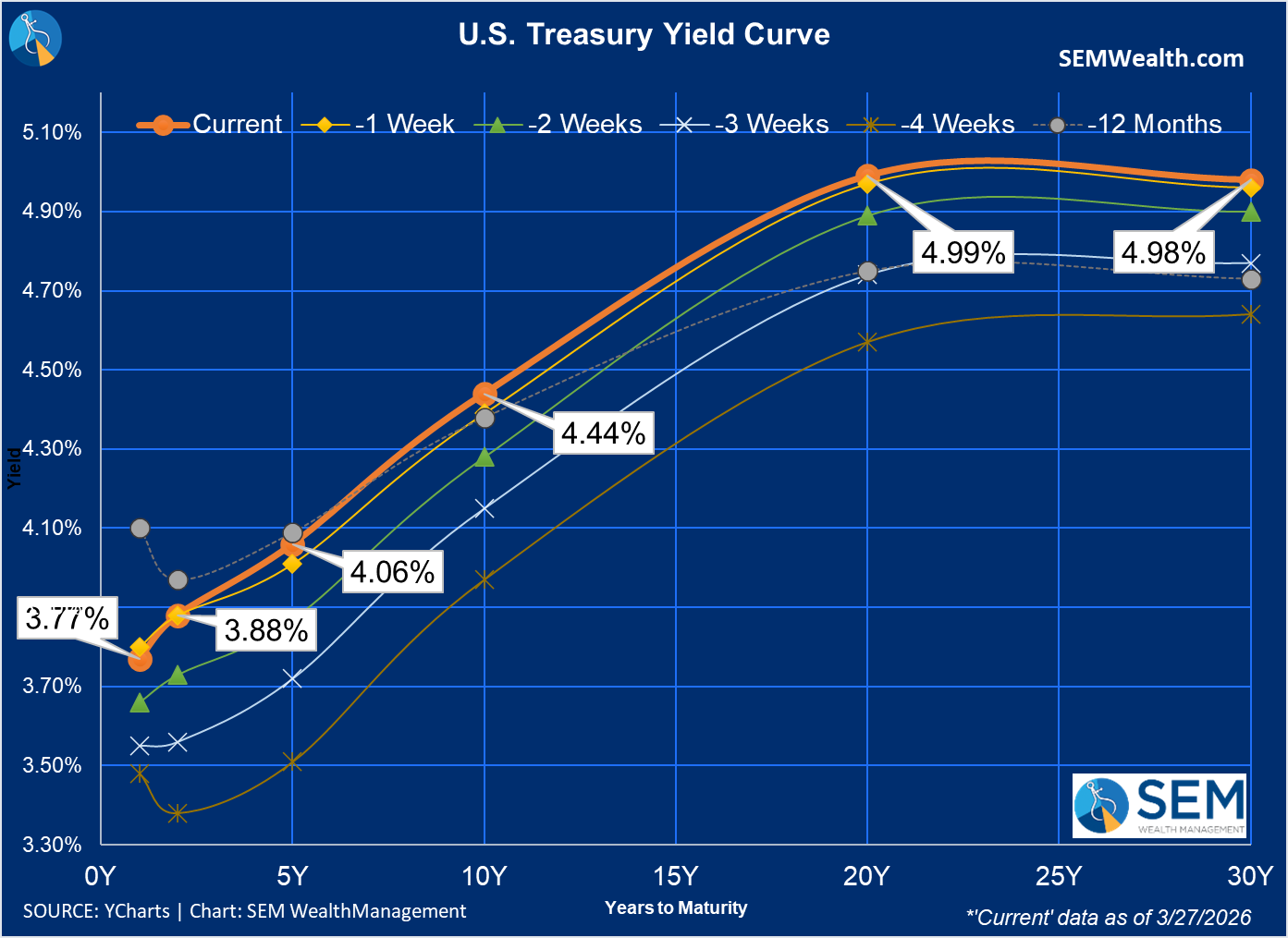

This week I'd like to start with the bond market as it can have a much bigger impact on the economy. The yield curve has seen a significant shift higher over the past 4 weeks and nearly all durations of interest rates are higher than they were 12 months ago.

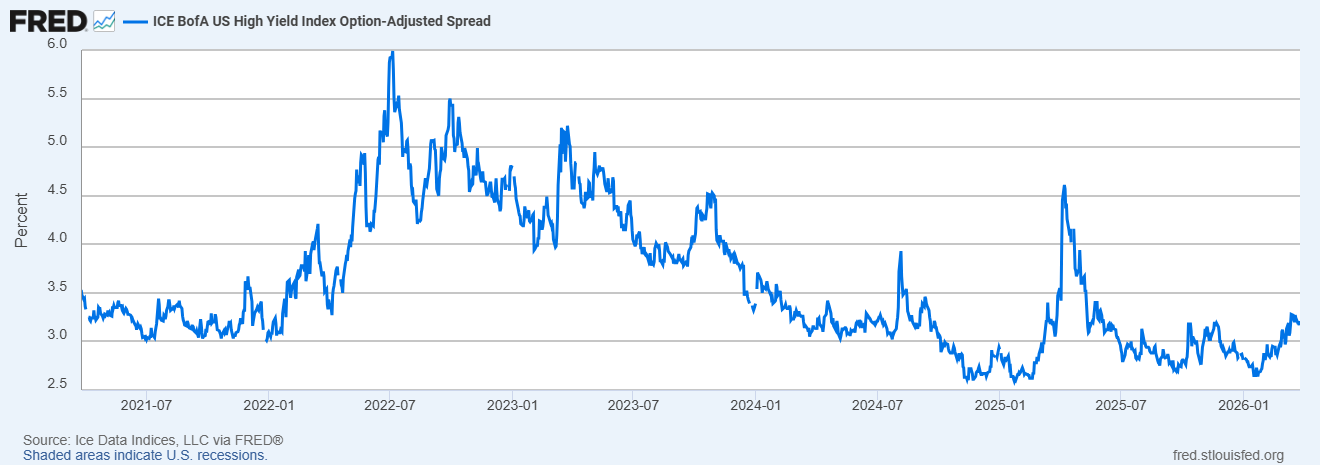

My favorite measure of risk, the difference between High Yield Bond Yields and Treasury Yields is rising, but not like it has during recent sell-offs in the stock market. One thing keeping spreads down is the fact Treasury yields are rising faster than Junk Bond yields.

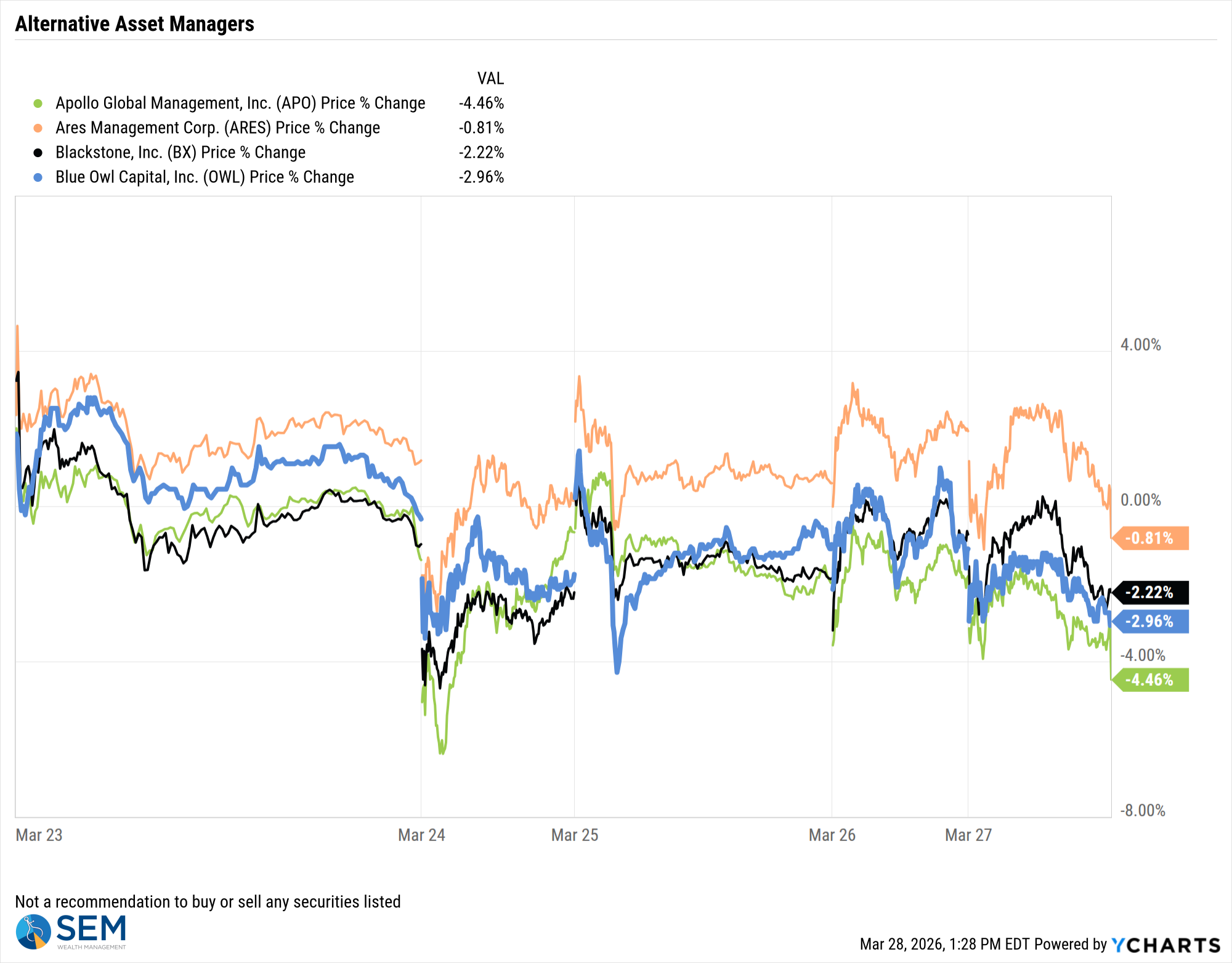

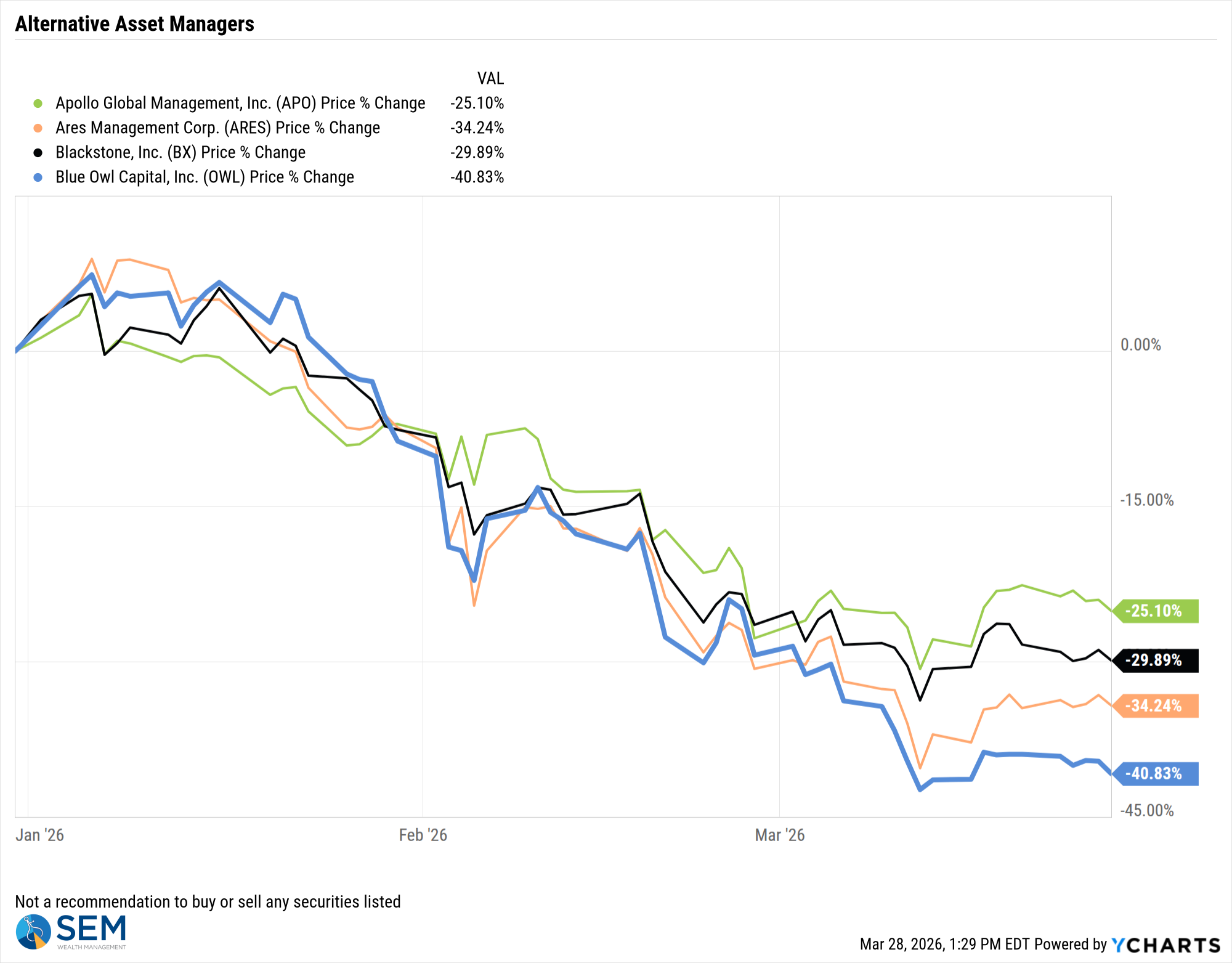

Private Credit continues to weigh on the risk appetite. The latest firm to cap redemptions on a fund was Apollo, which saw its stock hit the hardest last week.

Overall, it's been a tough 2026 so far for these firms. Since we don't have data or pricing on their underlying funds, we only have their stock prices to follow as we look for signs of additional stress or stabilization in this key space.

Overall, it's been an ugly month for stocks, especially technology stocks. It's not just the war in Iran causing this. Stocks peaked the first week of February, a month before the start of the war.

It was another week that started promising, but ended again on a negative note.

The S&P 500 fell below its 200 Day Moving Average last week, a sign the intermediate-term trend may have shifted. Friday saw the market hit the lows from last August.

Our indicators are close to issuing more "sells" should the market be unable to stabilize this week. Stay tuned.

Toby's Take

A look at our intern's top WSJ stories from last week

3/23/2026 - ‘Stop, Stop, Stop’: LaGuardia Airport Closed After Runway Collision Kills Two Pilots - WSJ

LaGuardia Airport closed after tragic incident involving a passenger plane and an emergency vehicle. The Firefighter team in Truck 1 was called after a crew member on a United flight reported feeling ill from an odor in the cabin. Air-traffic control signaled the truck to cross and roughly seven seconds after came on the radio saying to stop. Jazz Aviation flight AC8646, who was operating on behalf of Air Canada, struck the firefighting truck. The 2 pilots were killed and 41 people were taken to the hospital. This tragic incident is going to cause more fear surrounding air travel potentially causing the air travel market to drop.

3/24/2026 - Gulf States Edge Toward Joining Fight Against Iran - WSJ

What was meant to be a simple and short conflict with Iran has grown rapidly to a larger war. At the beginning U.S. allies turned down joining the fight, but now as their own economies are being hit and at further risk we are likely to receive help in the fight. If we get more support we will be able to give harder more frequent attacks hopefully overturning the rule over the energy-rich region. Hopefully the conflict ends soon and our oil markets can level out.

3/25/2026 - The Oil Supply Crunch Is Spreading From the Gulf to the Rest of the World - WSJ

The price of oil has gone up so much since the war in Iran started and it is seeming to reach other parts of the world now. The reason for the price going so high is because our usual oil producers in the middle east can't get oil tankers to sail safely through the Strait of Hormuz because it is under threats from Iran. So companies are paying $160 a barrel for the Emirati oil that is able to get around the strait. That price is absolutely absurd and governments around the world are trying to figure out how to fix this issue. The prices even if the war to end right away would take some time to level out at home. This can cause disruption in many households having to readjust their budget for these high gas prices.

3/26/2026 - Trump Says the Energy Shock Will Be Short-Lived. CEOs Paint a Scarier Picture. - WSJ

President Trump and his administration have been setting the conflict in Iran to be not nearly as dire as it truly is. Major oil CEOs have spoken at conferences and private meetings and have said that the financial markets aren't accurately reflecting the gravity of the crisis. The war is causing major damage to the world's fuel supplies by putting the oil industry's Middle East operations at risk. When will this conflict be over and how will we recover? This is an important matter that President Trump needs to be addressing.

3/27/2026 - U.S. and Israel Have Pounded—but Not Eliminated—Iran’s Missile Threat - WSJ

The United States' main goal going into this war with Iran was to prevent Tehran from continuing to threaten the Middle East with their missiles and drones. At the beginning of the war lots of their launch sites were destroyed greatly limiting them, however they continue to strike Israel and Gulf Arab States every day keeping themselves in the fight. Their goal is to continuously prolong this conflict to cause great economic issues pressuring the United States. The issue with the United States backing out now is that they will just go and recover all of the missiles they can from the destroyed launch sites making this all for nothing. President Trump is looking for a swift end to the war in the upcoming weeks. We can expect this to continue in that time causing more and more economic discomfort.

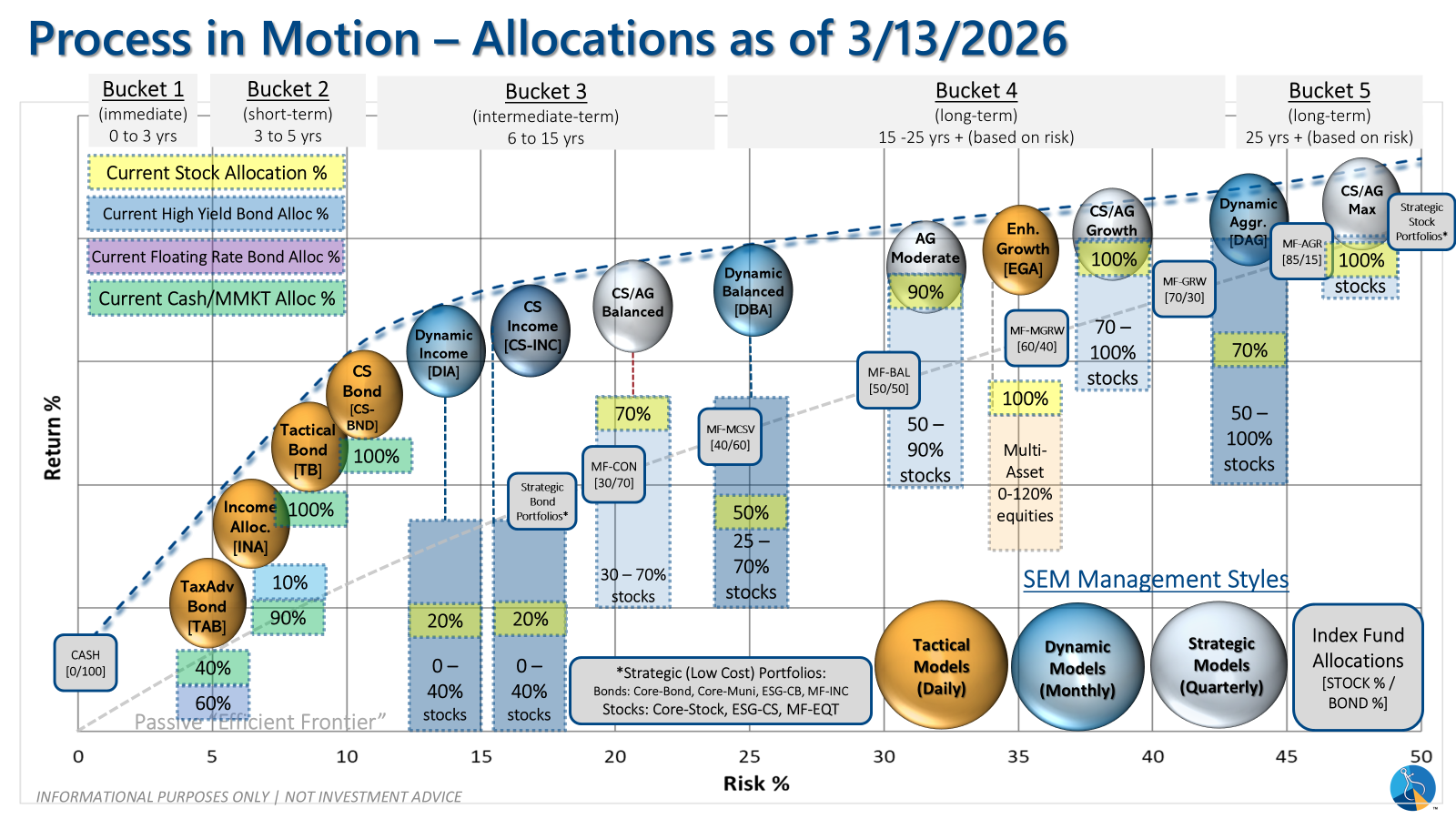

SEM Market Positioning

| Model Style | Current Stance | Notes |

|---|---|---|

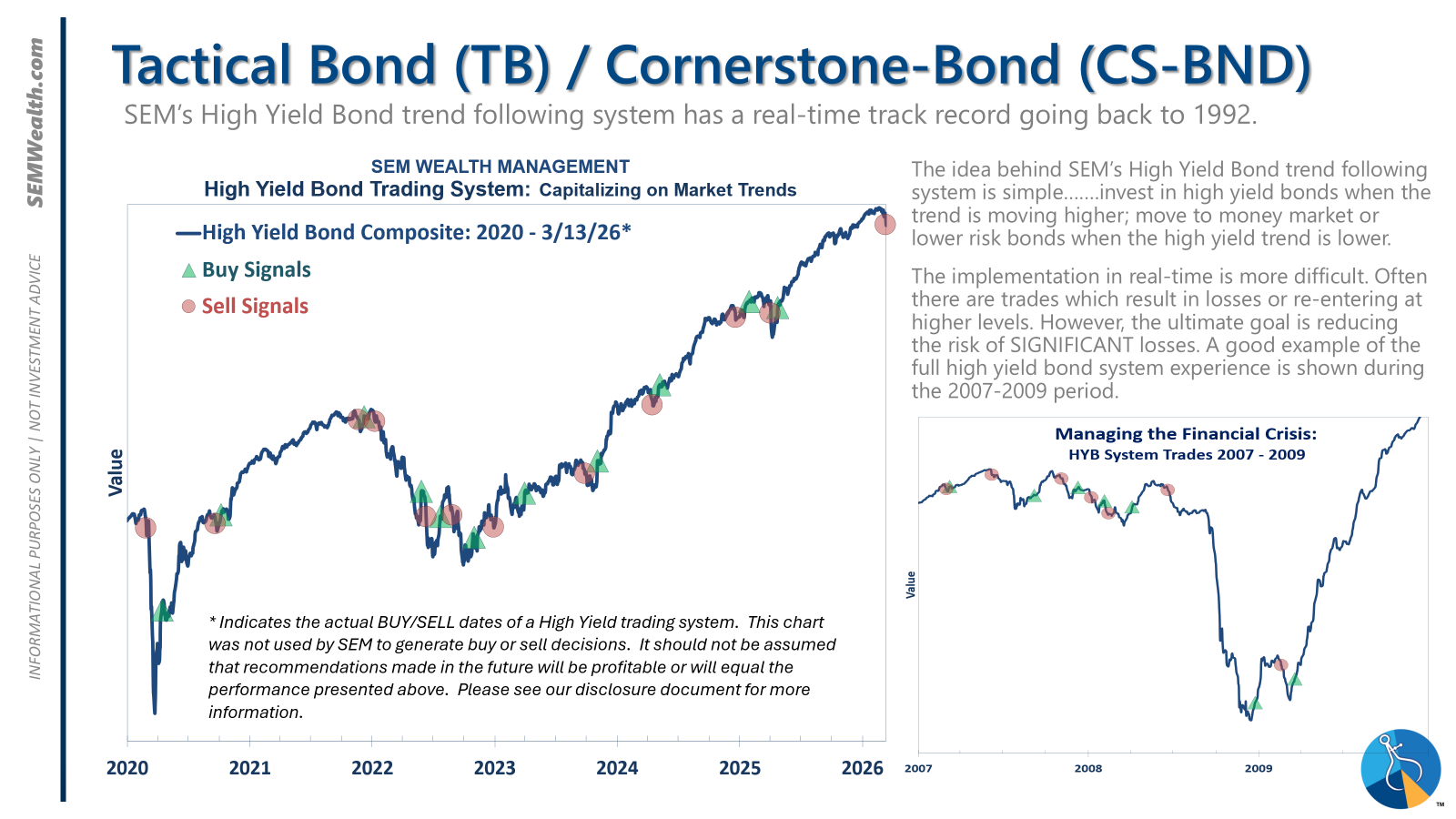

| Tactical | 100% MMKT | High-yield spreads narrow and trend has reversed lower |

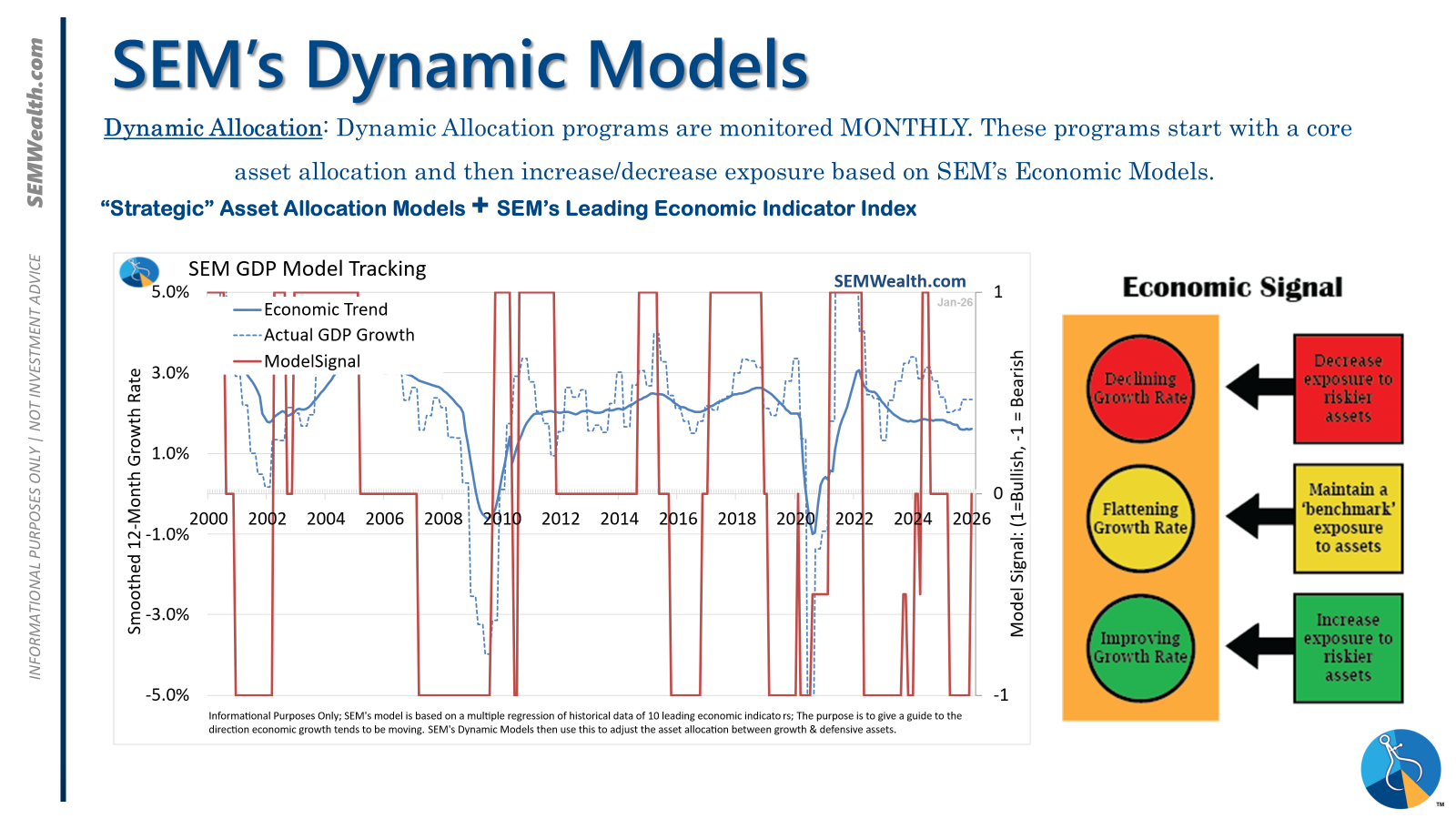

| Dynamic | Neutral | Economic model turned neutral Feb 15 '26' – benchmark weightings |

| Strategic | Fully invested | Trend overlay shaved 10 % equity in April -- added back early July |

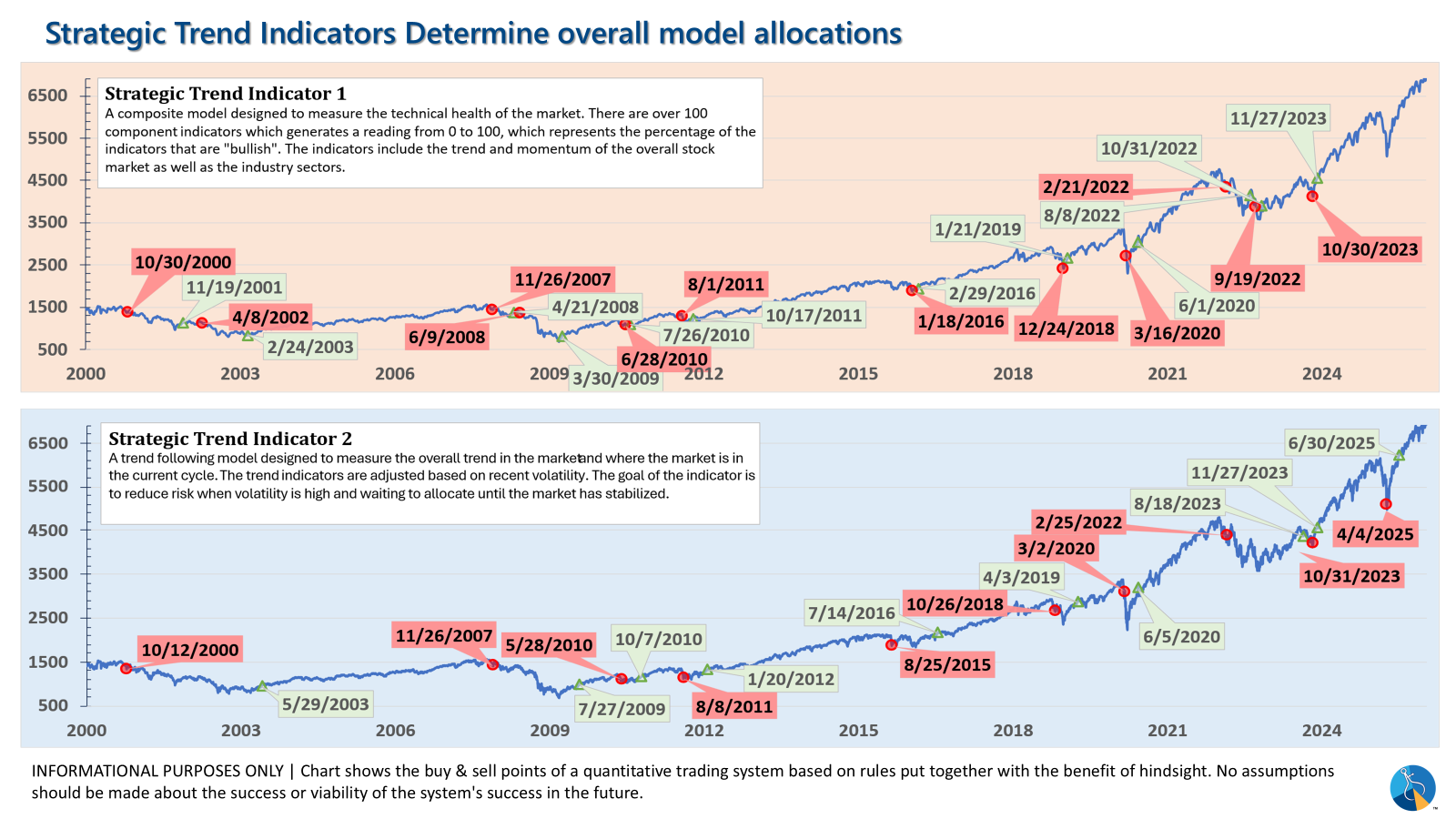

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

Tactical (daily): The high yield system sold on 3/13/2026 after the buy signal from 4/25/2025.

Dynamic (monthly): The economic model went 'bearish' in June 2025 after being 'neutral' for 11 months. This means eliminating risky assets – sell the 20% dividend stocks in Dynamic Income and the 20% small cap stocks in Dynamic Aggressive Growth. The interest rate model is 'bullish' meaning higher duration (Treasury Bond) investments for the bulk of the bonds.

Strategic (quarterly)*: One Trend System sold on 4/4/2025; Re-entered on 6/30/2025

The core rotation is adjusted quarterly. This quarter we saw half of our international positions reduced (we sold developed markets and kept our emerging markets exposure). We also saw the remaining share of mid-cap reduced in favor of more small cap exposure. We remain with a "barbell" core portfolio – about half in large cap and half in small cap as the models expect the market to "broaden".

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

Overall, this is how our various models stack up based on the last allocation change:

Curious if your current investment allocation aligns with your overall objectives and risk tolerance?