Everyone is back from their Thanksgiving holiday so we are now seeing market participants turning their focus to the rest of 2016 and beyond. The overwhelming consensus seems to be a Trump Presidency will lead to years of strong growth and we are seeing market participants adjusting their portfolios accordingly. We have to keep in mind these same “experts” told us the market would collapse if Donald Trump were elected president.

As I’ve said from the beginning, if you ignore Mr. Trump’s brash statements on immigration and trade, on paper his policies are extremely bullish for the economy and something we haven’t seen from the White House since Ronald Reagan. However, it appears Mr. Trump is not willing to completely back away from some of those protectionist ideals, which means we cannot discount the prospects of some sort of trade war breaking out. This would hurt growth and also dampen the prospects of many of his other policies being implemented.

In addition, we have to remember only about 35% of Republicans voted for Mr. Trump in the primaries, and most Republicans were reluctant supporters in the weeks leading up to the election. There are wings of the Republican party that will not stand behind some of his policies, which could lead to infighting and compromises that only create larger divides inside a party that was already deeply divided.

The other issue we have to keep in mind is the ongoing push from the Democrats to destroy any chance of seeing both parties working together. The latest effort from Green Party candidate Jill Stein, which is now fully supported by Hillary Clinton to push for a recount in Wisconsin, Michigan, & Pennsylvania could throw the entire transition process into chaos. I’ve seen several posts saying the main goals of this effort is to further reduce the legitimacy of a Trump Presidency by forcing Congress to decide the outcome (since the recount may not be completed before the Electoral College vote on December 19).

Adjusting portfolios based on assumptions of what might happen in Washington is never a good idea. Given all the upheaval in our country and the character of the man elected president, I continue to recommend caution in making subjective calls on which investments will thrive under his presidency.

Tuesday, November 29

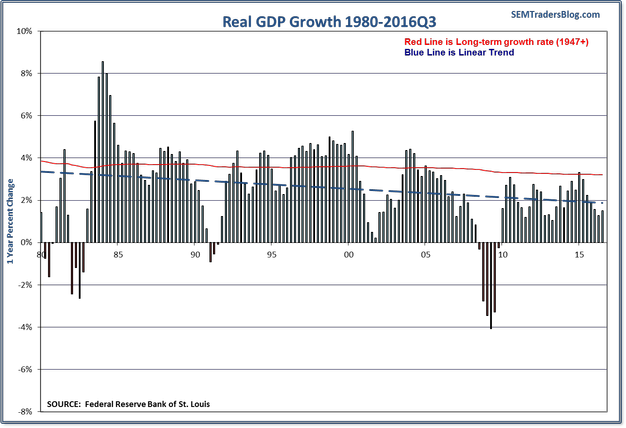

Stocks paused a bit on Monday, possibly due to the push for a recount in some key states that threatens to throw the transition process into chaos ahead of the electoral college vote on December 19. Other than that there was no major news to drive prices in either direction. This morning the focus will turn to GDP growth when we get the 2nd revision of 3rd quarter GDP. Estimates are for the annualized growth rate for the quarter to be revised from 2.9% up to 3.0%.

Following the initial release, the “experts” predicted this “strong” growth would be enough to ensure Hillary Clinton of victory. Donald Trump had been running on a platform that was highly critical of the Democrats’ economic policy and the headline number was supposed to be a reminder that growth was decent and getting stronger. Unfortunately for Mrs. Clinton and all those “experts” the voters were not that naive. The majority of middle class Americans have not felt much growth the past 7 years and this chart of GDP growth shows us why that is the case. Remember the government’s “official” number is essentially the last quarter’s growth compared to the prior quarter compounded four times, whereas this chart shows the percentage change over the past year.

For more on the 3rd Quarter GDP estimate, click here.

Wednesday, November 30

GDP growth was revised even higher than expected to 3.2% (seasonally adjusted annualized rate of the growth from the 2nd quarter to the 3rd). On a year over year basis (the number that really matters) growth was adjusted from 1.5% to 1.57%. This is still well below the long-term average as well as the downtrend in growth we’ve witnessed the past 40 years.

Wall Street is betting President Trump and the Republican led Congress will be able to accelerate that growth rate………at least that is the narrative. This morning I clicked on a headline on Yahoo about the “bullish” forecasts from Wall Street strategists for 2017. Browsing the predictions for where the market will finish NEXT YEAR and the justifications the forecasts seem bullish, but digging into the numbers you have to wonder what in the world the strategists are thinking.

According to S&P the forecast level of operating (adjusted or not-GAAP compliant) earnings is for growth of 20%, which is the average growth of the strategists in the Yahoo article. With 20% earnings growth you would think their market forecasts would be for a robust year for stocks. That is simply not the case as the average prediction (throwing out Goldman’s “bearish” forecast of a slight decline in stocks) is a 6% return for the S&P 500 next year. They are actually predicting a decline in the P/E ratio from the current 19 down to 17 (the post 2003 average P/E).

Personally I would be jumping up and down if we were going to see 20% growth in earnings next year. This type of growth should lead to HIGHER P/E ratios and on paper would mean our Dynamic Aggressive Growth program was set for a spectacular year. I guess after 7 years where stock returns far out paced earnings growth I should not be surprised we are seeing earnings growth exceeding stock growth.

Reading between the lines, it seems the strategists are pricing in either a lot of uncertainty and volatility and/or a recession on the horizon in 2018. Time will tell.

Thursday, December 1

The markets started November fearful of a Donald Trump victory. Stocks sold off hard & bonds rallied. As we enter the final month of the year the markets are pricing in a major overhaul to the US economy behind the president they feared the most. The bond market is not as excited. November saw the global bond market lose $1.7 TRILLION in value, the worst month on record.

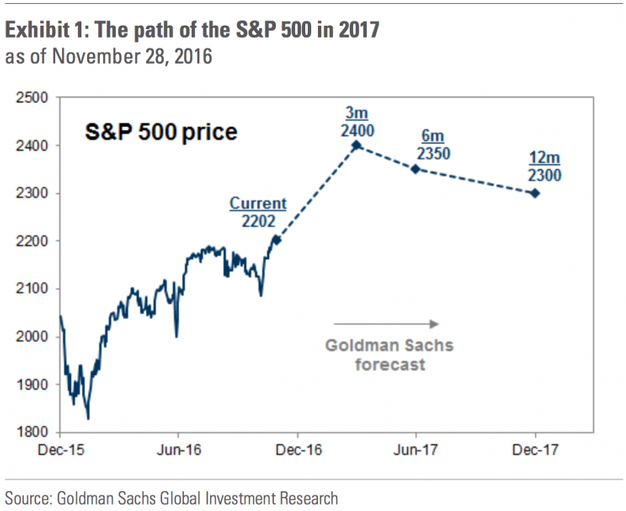

Yesterday I looked at the forecasts of many top Wall Street strategists. I mentioned excluding Goldman’s “bearish” forecast for a flat year. No sooner had I posted the article did I see an email from Goldman regarding an increase in their S&P 500 2017 target. They are predicting “hope” to prevail in the early months of 2017, leading to a 9% rally up to 2400. From there they see reality setting in as market participants realize how difficult it is to turn campaign ideas into actual actions. Goldman than sees a 4% slide the rest of the year back to the 2300 range that is the year end target for most Wall Street firms.

Making these types of predictions seems silly to me as nobody knows how things might shake out. About the only prediction I can make is 2017 will not be as smooth as the Goldman scenario pictured above.

Friday, December 2

Is the euphoria wearing off or is the market just taking a break before moving higher? That will be the question on market participants’ minds today and into the weekend. From a seasonal perspective the few weeks after Thanksgiving are typically weaker before the “Santa Claus” rally emerges about a week before Christmas. This morning the focus will be on the November Payrolls Report (our Chart of the Week will provide my take on that report.)

Last night I saw an interesting take on The Reformed Broker blog. It is written by Josh Brown of CNBC’s Halftime Report fame. Josh was discussing WHY the market has been so strong when so many predicted a Trump victory would be a disaster for stocks. The reason? Animal Spirits. Here’s Josh:

When outrageous things happen, all of a sudden there can be a sense that many other outrageous things are also possible. This ignites imaginations and gets the creative juices flowing. If this sort of thing extends beyond the speculators in the stock market into the actual C-Suites where spending and investment decisions are made, then it becomes self-fulfilling and it could actually work. If it doesn’t, well then at least we’ll have some fun in the meantime.

Over the last five months, small cap stocks are up 15%. The stocks of oil and gas producers are up 23%. The stocks of regional banks are up 40%. Do we believe that the fundamentals of thousands of small cap companies or hundreds of energy companies and banks have improved by 15, 23 or 40%? Of course we don’t. This is the role that sentiment plays in the stock market. There’s no equation. No formula.

Animal spirits cannot be modeled.

They can’t be foreseen or managed either. We cannot know for how long they’ll run on for or what might dissipate them. We can only accept that they are a part of the game, coming and going at uneven intervals, spreading joy and pain in their path.

When animal spirits take control strange things do seem to happen, but they also tend to lead to dangerous situations for investors. Doubleline’s Jeffrey Gundlach is warning of just that. The “bond king” predicted in January the Donald Trump’s victory (due to growing unrest from the middle class), called the bottom in bond yields in July, and is now calling the top in stocks. Here’s his take according to Reuters (and ZeroHedge):

“The bar was so low on Trump to the point people were expecting markets will go down 80 percent and global depression – and now this guy is the Wizard of Oz and so expectations are high. There’s no magic here.”

Gundlach had warned last month that federal programs take time to implement, rising mortgage rates and monthly payments are not positive for the “psyche of the middle class and broadly,” and supporters of defeated White House candidate Hillary Clinton are not in a mood to spend money.

“There is going to be a buyer’s remorse period.”

“People want something real. No more on this ‘man behind the curtain’ stuff. Industrials, materials … people are tired of tweets. They want cement.”

He concluded: “It is so late to be buying the Trump Trade.”

As I’ve said since the election……..tread carefully. We are in dangerous territory.