Regulators in our industry frown upon the use of the word ‘guarantee’ for obvious reasons. If you live long enough (or study economic history) the only guarantee in life is we will all eventually die. The exception to the use of the “G” word seems to be in the use of annuity contracts. These contracts are all full of the word, making them easy to sell to clients by advisors who are confident the insurance company will be able to stand behind their guarantee.

Before you send me hate mail or stop reading, let me say I have no issues with advisors using annuities or other insurance products in the financial planning process. In pretty much any speaking engagement, whether in front of clients or advisors I have said as much. That said, I would not be fulfilling my role as the OCIO (Outsourced Chief Investment Officer) for so many advisors around the country if I didn’t educate these advisors on the risks behind these “guaranteed” contracts.

I’ve spent quite a bit of time digging through offering documents, speaking to advisors about the various contracts they use, asking anybody in our industry if they understand the mechanics behind the contracts, and conducting my own research on how they work internally. I’ve had a few motivations:

-

We’ve had advisors asking SEM if they could become investment advisor representatives directly with us, breaking away from their Broker-Dealer [the answer is ‘yes’ — ask me for the details]

-

We work with friends and family offering financial planning and would like to pursue all possible planning options.

-

If an insurance company can do something that is a source of “low risk”, is there a way SEM could offer something similar [the answer is ‘probably yes’ after E*TRADE Advisory Services works out some legal/compliance/technical tie-ins with the retail side of E*TRADE’s business.]

-

Educate our advisors on the risks they are taking so they can both explain it to their clients and protect their businesses going forward. [Problems with a few annuity company could literally put an advisor out of the business and even possibly bring down a Broker/Dealer if they had too many of those products, this of course would create chaos for SEM and our mutual clients.]

There are a few things I have found I think everyone offering an annuity needs to understand.

-

Advisors need to do a better job of educating clients on the downside of locking their money away in a contract as well as the fees involved. Not only is a new fiduciary standard coming from the SEC (and possibly FINRA), the other side of the debt bubble could be a period where locking in guarantees at today’s rates could do serious harm to the overall financial planning picture.

-

Even if you don’t sell products with specific risky riders, insurance companies run as a pool, so a blow-up in one product line hurts all clients inside the insurance company.

-

Insurance companies are state regulated, which means different rules and also different pools of protection for the insurance holders. If a state does offer protection, keep in mind the protection is only as strong as the finances of that state. If some of the things listed below cause an annuity to blow-up, chances are quite high state-run pensions will have problems as well (because they rely on the same underlying investment vehicles.) Remember, a state cannot print money to prop-up their state funded guaranteed pools of money.

-

Insurance issuers may be monitored by the Fed (if they are ‘systematically important’ or have an arm that is a Federal Reserve branch). However, there are so many layers and divisions inside the Wall Street banks the Fed may not know who is watching what or even be able to monitor what the other divisions inside the bank are doing. In addition, it is literally impossible for them to map who has double cross-party exposure to other banks (or their divisions). If you want to understand some of the inner-workings of the banks and their various divisions watch “The Big Short” (or better yet, read the book as it is much more detailed). NOTHING inside the financial reform bill (Dodd-Frank) included ways for regulators to watch what is happening in the various divisions more closely. Worse, the few restrictions in Dodd-Frank regarding cross-division exposures have mostly been pulled back because “we’re 10 years removed from the crisis, nothing bad has happened, and the regulations hurt the competitiveness of the banks.” Keep in mind, Glass-Stegall was repealed in 1999 after “nothing bad had happened and the regulations hurt the competitiveness of the banks”. Glass-Stegall went into place in the 1933. It took 10 years for the financial system to blow-up.

-

There is no guarantee the Federal Reserve or Congress will step in to bail-out the insurance or banking industry this time around. This is one thing I’ve heard most advisors tell me they are resting their guarantees on. Please remember we are in a completely different social environment than we were 10 years ago. Could you imagine the uproar if Congress or the Federal Reserve once again stepped in and saved the Wall Street banks who needed saved just 10 or 15 years earlier?

Understanding all of the above, I saw a presentation from the head of risk strategy at AXA. It was an eye opening look at the risks insurance companies are facing when they offer any sort of annuity. Here is his list of “what keeps insurance risk managers up at night”:

-

Stocks falling: All insurance companies hedge against this risk; The real problem comes only if the counter-party providing the “hedge” is unable to remain liquid. The derivatives used by insurance companies are nearly all “off-exchange” (SOURCE) meaning there is nobody ensuring the ability of both parties to fulfill their obligation.

-

Stocks Soaring: The risk here is rising account values mean higher benefit levels that may not have been planned for. Some insurance companies hedge this risk, but not all. Another risk is a drop in demand for annuities following a few positive years in the market. Insurance companies rely on the “pools” of money, which includes new money going into new contracts with more favorable terms to the insurance company.

-

Declining Interest Rates: Declining interest rates make it difficult for insurers to match the maturity of their promised benefits. This becomes difficult to hedge if the yield curve becomes too flat (or worse inverts). If you have declining Treasury yields at the same time you see increasing investment grade bond yields it gets even worse. The speaker listed this as a MODERATE RISK for annuities. You also run the risk of counter-parties having their own problems hedging all of their exposure (derivative contracts are highly sensitive to changes in interest rates).

-

Rising Interest Rates: If rates rise too much, the value of the guarantees are greatly diminished. This could lead to annuity holders letting their annuities lapse and/or choosing to pay the penalty to get out. This creates a cash flow issue for the insurance company and could leave them in a situation where the high risk clients in the pool remain and the low risk clients fleeing. This was also listed as a MODERATE RISK for annuity issuers. Like falling rates, this again creates issues with the counter-party as well due to the pricing of the derivative contracts. From a client perspective, I think this risk is ignored. Locking in “guarantees” at today’s still low rates is a significant risk. There are products that have inflation protection, but the benefits are often lower and the costs higher, making them less attractive today. There is a good chance interest rates will be much higher 3-10 years from now, which puts the client in position to miss out on other opportunities (or see their buying power eroded due to inflation). Most annuities have some sort of inflation protection options, but those are often more expensive and offer lower immediate payouts.

-

Bond Downgrades & Defaults: This was listed as a SEVERE RISK for annuity issuers. It was this specific risk that led me to write this article. This risk is something EVERY investor should be aware of. I’m currently working on a more detailed explanation of the risks in the bond market that could cause some annuity issuers to fail. I’ll post the link here when it is finished, but the Cliff Notes (Spark Notes for those younger than 40) version is this — half the investment grade bond market is rated one step above junk (BBB), with 85% of new issues falling in that category. Insurance companies and pension funds are restricted from owning bonds rated below investment grade. Companies have used the easy money created by the Fed to issue debt at record levels, but have used it to buy back stock and issue dividends. This increased their stock prices, but now they have no assets to cover their debt which is coming due. A few downgrades due to an economic slowdown or issuers being unable to re-finance could cause a death spiral for the BBB bond market.

Looking at the list above, besides the major risks in the BBB bond market (article coming soon), counter-party risk is screaming at me as the primary risk annuity holders are facing. Again, NOBODY can guarantee all of their counter-parties are not doing something stupid inside another division that the other divisions are not aware of. When you add in the potential for tens if not hundreds of billions of dollars of investment grade bond downgrades, things can get ugly rather quickly. Maybe the Fed will bail them out, maybe Congress will, or maybe the social mood will not allow either of them to step in and save an industry that has done nothing to help the American economy (in the eyes of the electorate). I don’t want to take that gamble.

Digging into the Counter-Party Risk

Parents know if you don’t punish your child for breaking a rule, they will break it again (and probably become more brazen). I said the same thing following the ‘solution’ to the financial crisis — giving the biggest banks who were failing Trillions of dollars while letting smaller banks fail. Looking at the most recent report from the National Association of Insurance Commissioners it appears my prediction is closer to coming true. The report posted in November 2018 only had data through the end of 2017, but it does give us a slightly better feel of the potential counter party exposure in the insurance industry.

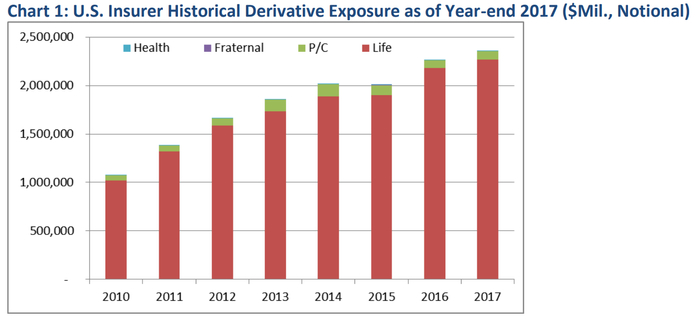

First off, 13% of insurance company holdings (or $331B) are in the financial services sector. Of those bonds, 55% mature in the next 5 years (which will be at rates significantly higher than they had in the previous 5 years.) [Source] Worse is their derivatives exposure. At the end of 2017 it had climbed to $2.4 Trillion. This is up from $1 Trillion at the end of 2010. These “financial weapons of mass destruction” (as described by Warren Buffett) nearly brought down the entire global financial system. Again, when you do not punish somebody making a mistake they will make the same mistake again (but often in a bigger way).

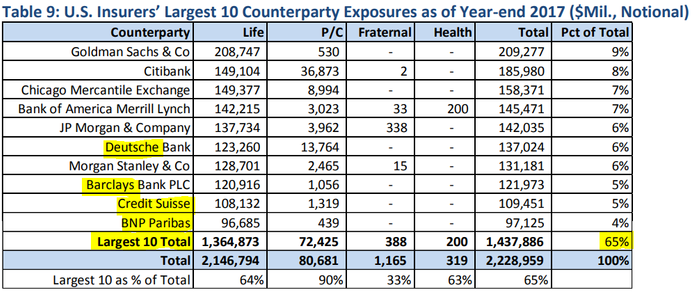

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

65% of this counter-party exposure is with just 10 entities. This leaves 35% exposure to who knows which entities. In 2016, AIG was in the top 10, but was surpassed by BNP Paribas in 2017. The question is what other insurers besides AIG are also providing “hedges” for other insurers? I also highlighted the foreign banks that are on the other side of the hedge for the insurance companies. Even if the Fed decides to bailout the Wall Street banks despite what is likely to be a major populist backlash, will they also bailout the foreign owned banks?

Problems in the BBB bond market WILL cause problems with the counter-parties. They are all linked.

What can you do for your clients?

I truly hope I am wrong. If I’m not, some people I consider good friends could be hurt badly if not pushed out of the business. I saw it happen the last two times the financial bubble burst. I think this time could be even worse because the thing that saved us last time (massive debt-fueled stimulus) is the very thing that will cause the next crisis. Even with proper preparation a mass downgrade in the BBB bond market combined with a social mood that doesn’t allow any bailouts could cause serious collateral damage. There aren’t a lot of things that keep me up at night, but this is at the top of the list.

One thing I have done is renew my premium subscription to Weiss Ratings. For those of you not aware, unlike the popular ratings services such as A.M Best, S&P, Moody’s, or Fitch, Weiss only receives compensation from their customers (those wanting an unbiased opinion on whether a company has specific financial risk.) Weiss was invaluable during the financial crisis for us as we helped our clients and advisors figure out which insurance companies, banks, credit unions, and other financial companies were at risk of going under.

As the Outsourced Chief Investment Officer (OCIO) for a group of advisors we call our Platinum Advisors, I am offering to begin tracking the annuity issuers they are using. If you are in that group, please send me a list of which insurance companies you are using and which products you use. I will not only prepare a report on the issuer, but I will add them to a watch list so we can see if they are downgraded (or upgraded) as we progress through the next recession. There are some stronger ones out there based on the first screen I ran with one of our Platinum Advisors.

If you’re not yet an SEM Platinum Advisor, but would like to learn more, drop me a quick note and we can schedule a time to talk.

As part of my research process, I used this template to dig into the details of the various annuity contracts. If you are utilizing any fixed annuities, index or otherwise, I’d encourage you to use it.

I understand this will upset a lot of people. With back-to-back record sales years for index annuity products, I know many of our readers have begun making annuities a major part of their business. I truly hope I am wrong. At a minimum, I’m probably early — I usually am. Please do not take this as a “all annuities are bad” message. My job is to look at risks our clients and advisors are taking and this one is overwhelmingly at the top of the list. Do what you must with this information.

If you’re an insurance wholesaler, I would love to talk about your products with the risk manager at your firm. With our network of advisors knowing which firms have excessive risk and which ones do not could give your firm an advantage over the others.

Jeff is a CFA charterholder and received his Bachelor of Science degree in Business Administration (Finance & Accounting emphasis) from the University of Northern Colorado, where he was a member of the Financial Management Association National Honor Society. He has worked in the field of accounting and finance since 1992. Jeff was one of the minority of advisors warning about the looming financial crisis. SEM first warned about the upcoming recession in December 2006. In addition to helping his clients successfully navigate the dot-com bubble bursting, his piece, The Pending Forest Fire was widely criticized as ‘doom & gloom’ marketing by advisors throughout 2007 and early 2008. Instead it correctly predicted how easily the crisis could spread due to the bubble cycles created by the Federal Reserve. Prior to joining SEM, Jeff served as a Fund Manager/Analyst for the UNC Alumni Foundation Fund, a balanced portfolio consisting of equity, fixed income, and cash securities. He joined SEM in October 1998.