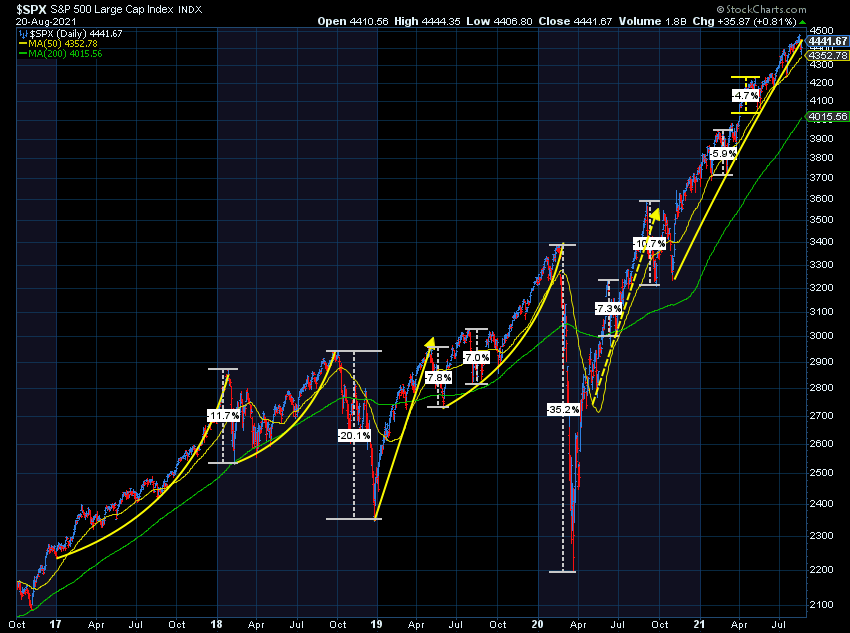

A lot of bad news this week. Mostly between the continued spread of the Delta Variant around America and the grim scenes and stories out of Afghanistan – it is easy to look at the sky falling around us. While personally both of those things are horrific, and I pray that the pain caused can be ceded soon, the effect on the markets have not shown major sell-offs due to these events. The S&P did lose about ¾ of a percent last week. This sell-off seems like it could be about any number of bad news we received this past week, but the Fed minutes are the most likely factor. The news of the Fed slowing down debt purchases will have a negative impact on the market, but it was inevitable that these decisions would eventually have to be made. You can’t just keep buying debt with blank checks indefinitely. While this news isn’t really that shocking when you think about it, SEM waits to see how the market takes the news and doesn’t do any of our own personal speculation to make moves in our programs. Overall, at the moment, the US markets have only shown minor corrections.

What we have seen instead is larger selloffs in Asia, caused by the ever-changing landscape in China. This time, it’s thanks to a new strict privacy law. While this hasn’t shown any sell signals in SEM systems, we will continue to monitor the situations we see and more importantly, analyze how those situations are impacting the stock market.

Jeff's Musings

I’ve been spending the month of August away from the day-to-day market movements and focusing on more big picture items. Part of this is brushing up on the CFA curriculum. Each August the CFA Institute releases “refresher readings” for CFA Charterholders. The purpose of these readings is to provide updates about the latest research now included in the curriculum. I thoroughly enjoy going back through the materials, which is probably why I’m called a ‘nerd’ so often by friends and family. With all that’s been happening in the markets the past 3 years I haven’t been able to spend as much time on this as I would have liked.

This week one of the new readings was on “Technical Analysis”. This was a Level I reading, but rather than being a single chapter like it was 6 years ago when I studied for Level 1, an entire unit was dedicated to this subject. There wasn’t a lot I learned, but it did generate a few trading system ideas I’ll have Steve, Rick, and Dustin start to work on.

What stood out to me in the reading was this sentence as it sums up exactly why SEM has always followed a technical (quantitative) approach:

“Human behavior is often erratic and driven by emotion in many aspects of one’s life, so technicians conclude that it is unreasonable to believe that investing is the one exception where humans always behave rationally.” – 2021 CFA Program Refresher Readings, Level 1, Reading 55

I think this is critical. The Level III materials were game changing to me back in 2016 as the unit on Behavioral Finance explained something I’d been witnessing for 20+ years in the industry. Nobel Prize winning economist Richard Thaler in his book, Misbehaving identified the same thing. In sociology it is assumed humans will behave irrationally. These are people whose field is studying human behavior. You would think they would be considered the experts. Yet in economics/finance, the assumption is humans will always behave rationally and it all circumstances.

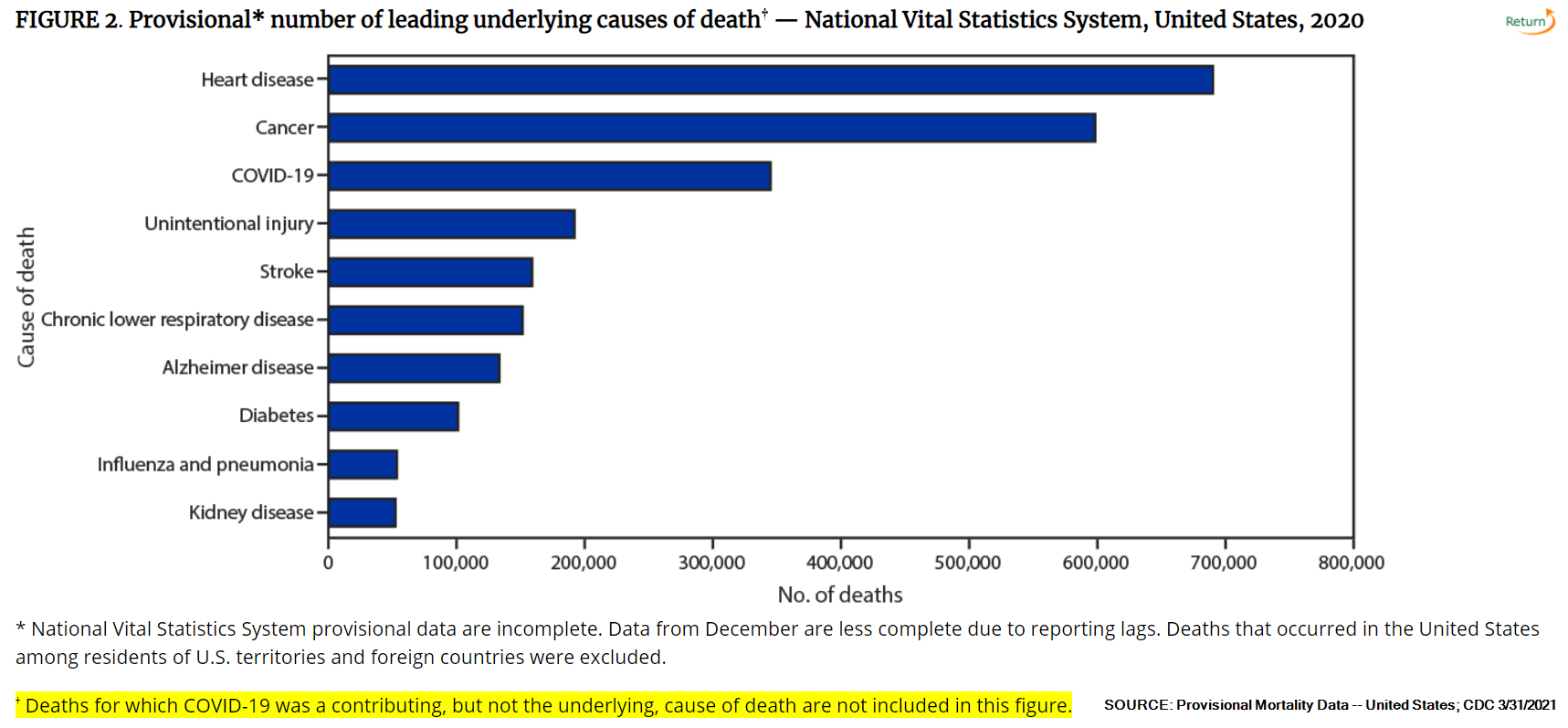

Dr. Thaler went on to create a list of times where humans did not behave the way economists assumed they would. The list grew so long Dr. Thaler became a ‘black sheep’ in the economics community in the 1980s. I don’t want to get political, but COVID has proven again our inability to think rationally. For decades science has shown us that reducing calories, cutting sugary foods, avoiding processed foods as much as possible, and exercising at least 30 minutes a day not only increases our quality of life (by helping us avoid debilitating diseases, injuries, etc), but also can add 5-10 years to your life expectancy. During 2020, we learned COVID was most devastating in those who were obese. 42% of America is considered obese according to the CDC. If you include anybody with a BMI over 30 (as my doctor does when she put in my chart last year that I was mildly ‘obese’), that number jumps to 73%.

73% of our country is in danger of dying from the number one killer of Americans – heart disease, yet the obesity numbers go up every single year. The fact that we KNOW all of this, but won’t change our behavior to combat it is yet another example of the lack of “rationality” in most Americans. Even more striking is the fact so many Americans were concerned about COVID, but still did nothing to change their overall health. By the way, the same can be said about those who fear the side effects of vaccines --- you are far more likely to have long-term issues or early death from obesity than any sort of side effect from a vaccine.

I guess this highlights a key bias we all have – Availability (or recency). We see people dying from COVID in a matter of a month or two, but heart disease, diabetes, and cancer are long-term, slow killers. We hear about some side effects from the vaccine, but we don’t see articles about every person who has gone on disability because of their obesity.

I don’t want to offend anybody. Being irrational means you’re human. I struggle mightily with my weight and especially my love for chocolate. I hate exercising unless it’s part of a sport. I know I need to do better and have been working towards this for the past year. Heart disease, diabetes, or cancer are far more likely to kill me than COVID or the COVID vaccine.

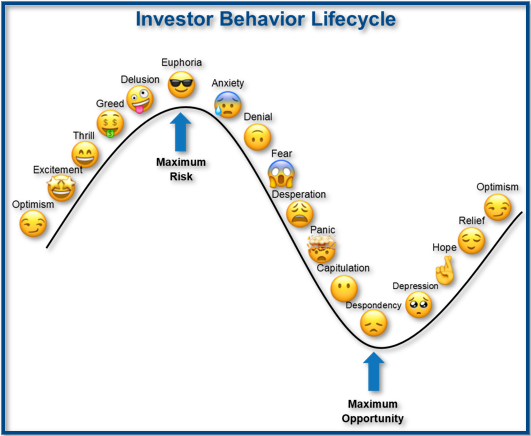

Bringing this back to investing --- if in all other aspects of our lives irrational behavior is the norm, why should we expect to behave rationally when it comes to our money? Money drives more emotion than anything other than our relationships with others. The more emotions, the higher chances of irrational behavior.

At SEM everything we’ve done has been purposeful in allowing our clients and advisor to be HUMAN. From the Risk Questionnaire we designed, to each of our individual investment models, to the trading systems inside each model our goal is to remove as much human emotion from the decision making as possible. We know we cannot trust our brains.

Last week I wrote about “Recency” (Availability) bias and how it causes us to believe major risks have been removed from the investment equation. It is normal to think that, but also extremely dangerous. When we are at this part of the investment cycle, the risks of seemingly minor events causing a large market sell-off are quite high.

Now would be a great time for a financial check-up. The best place to start is our Risk Questionnaire. It gives you the opportunity to have your portfolio reviewed to see whether or not we should make adjustments. It’s always better to do this when the market is up rather than after the inevitable bear market has started.