When we were young parents with 4 kids age 6 and under, we had to implement some rules that might seem odd to anyone who didn't have multiple young children. Some of those rules were for words we shouldn't say......words that sometimes mommy and daddy might be heard saying.

We'll never forget during the first week of kindergarten, Tyler coming home very upset that a kid at school said the "s-word".

We both were a little shocked as well. He said he said it to him multiple times. We finally said, "wait, what word did he say?"

Tyler replied, "the sh-word you said we can't say."

Finally his mom said, tell us what it was. He looked incredulously at us and said, "I can say it?".

"Yes", we both responded.

Tyler looked around and quietly said, "shut-up".

Yes, that was one of the s-words we were trying to teach our kids to not use. "Stupid" was another one. A few weeks later he came home saying that another kid had used the really bad "sh" word.

In economics there is another "s-word" you shouldn't say. That word was on a lot of our minds after a bad week of economic data. That word is "stagflation".

Stagflation is the worst possible economic scenario — inflation during an economic slowdown. In a world where we are conditioned to believe the Fed and Congress will step in to stop any economic slowdown, a slowdown that also includes or is caused by inflation, is nearly impossible for them to fight. The Fed can either fight the slowdown and make inflation even worse, or fight inflation and make the slowdown even worse. The last prolonged period of stagflation was in the 1970s.

Why is everyone looking around and whispering "stagflation"? Let's take a look at some of the data from last week.

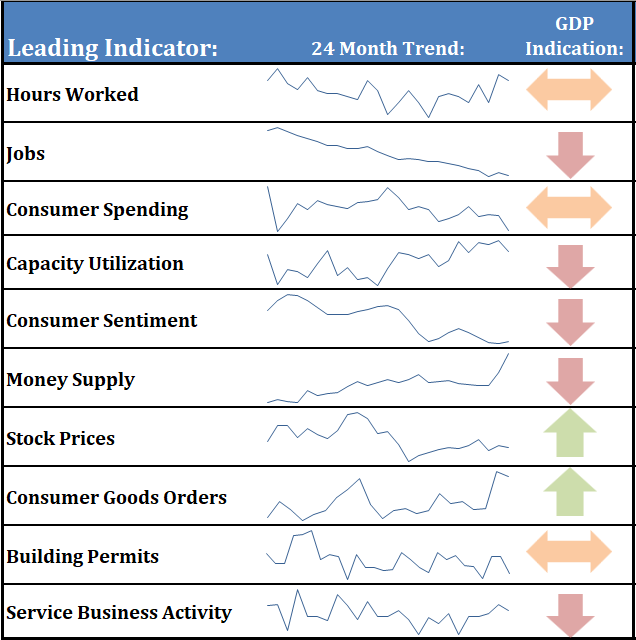

Economic Slowdown?

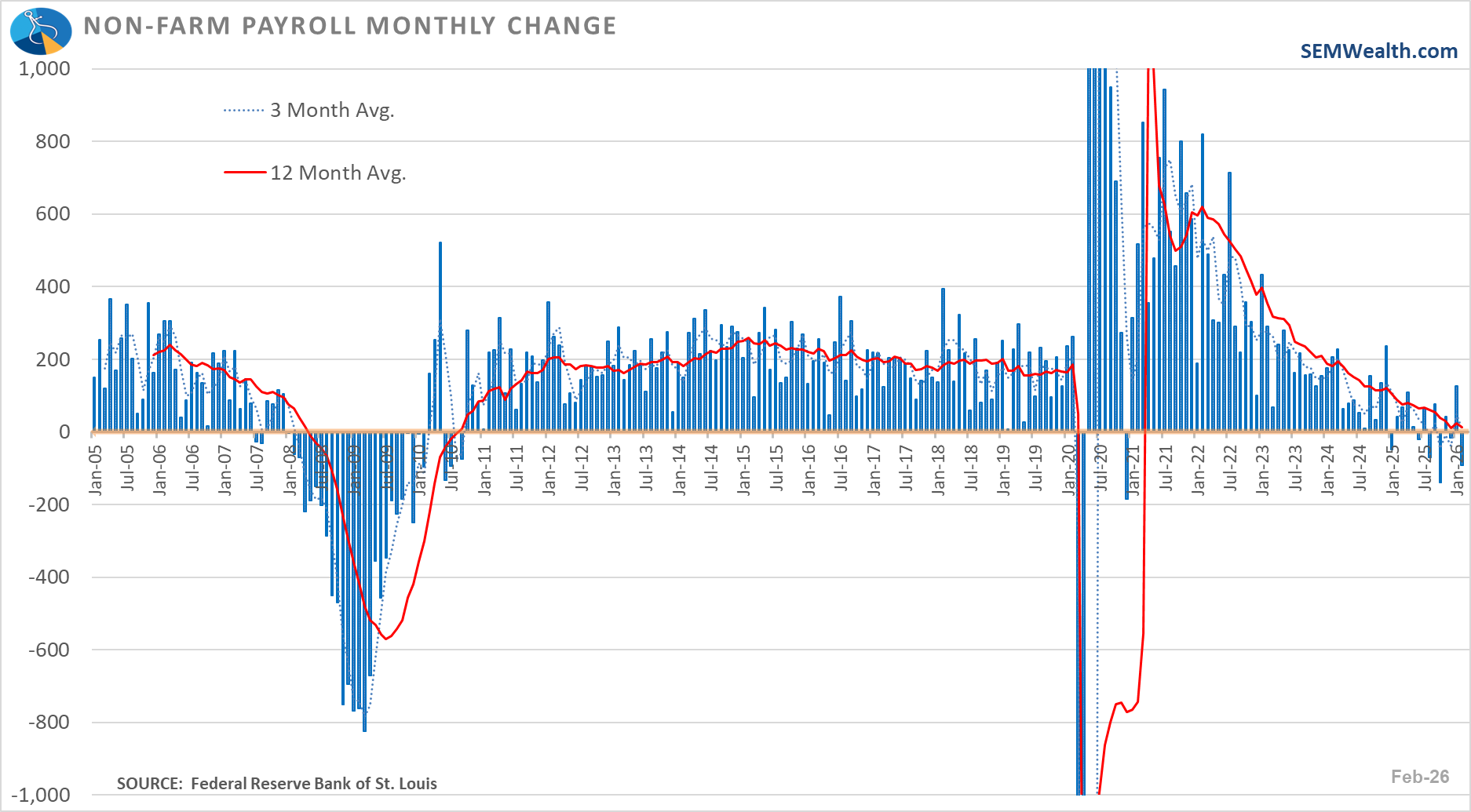

Friday's payrolls report dashed the hopes the economy was stabilizing. Payrolls declined by 92,000 in February, bringing the 1-year change to +0.10%. This is the worse 12-months since the early days of the pandemic. Prior to that the last time payrolls were flat for the past year was in April 2008, just before the financial crisis reared its ugly head.

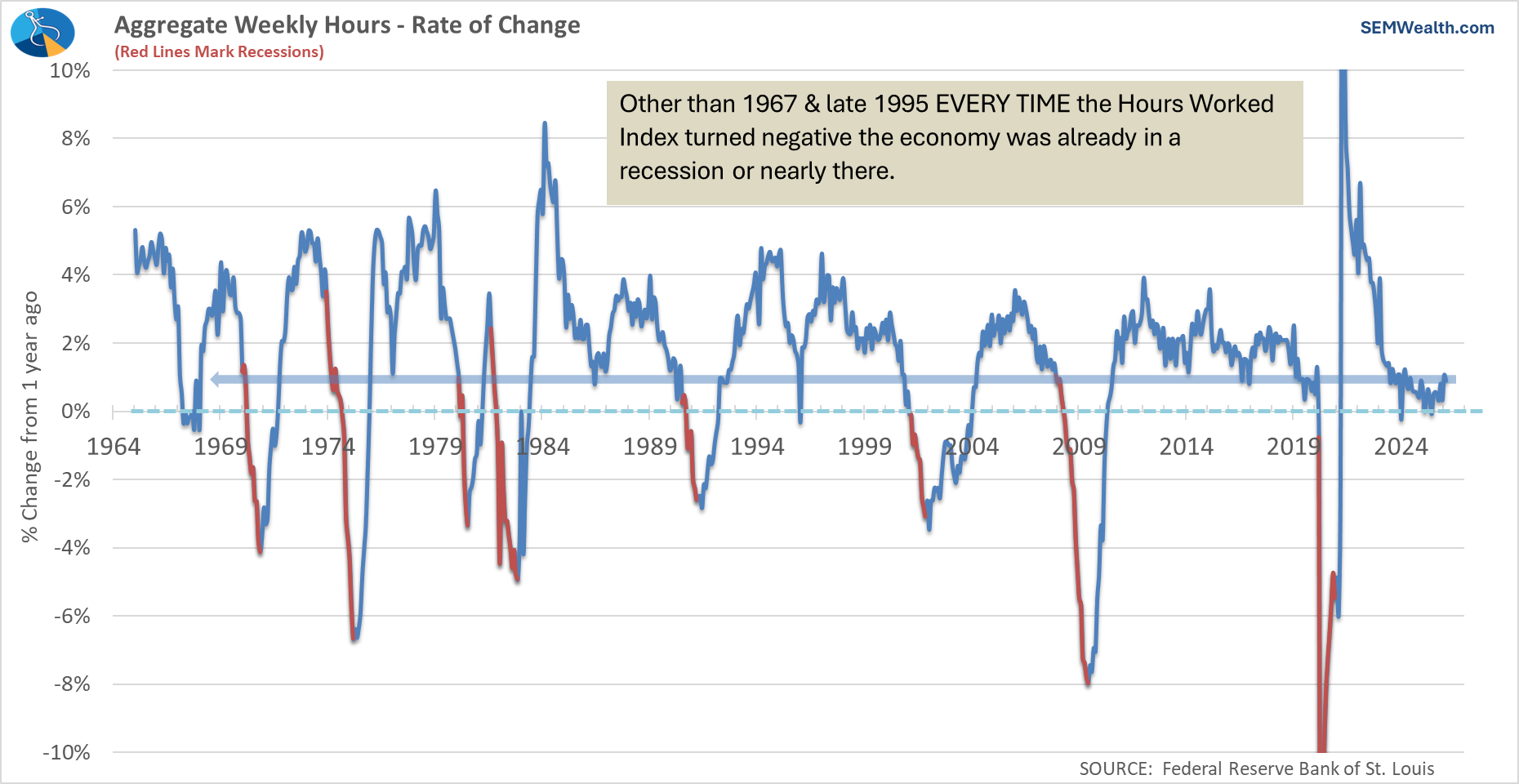

Hours worked are still up 0.90% for the past 12-months, so things aren't yet as dire as the market was acting on Friday.

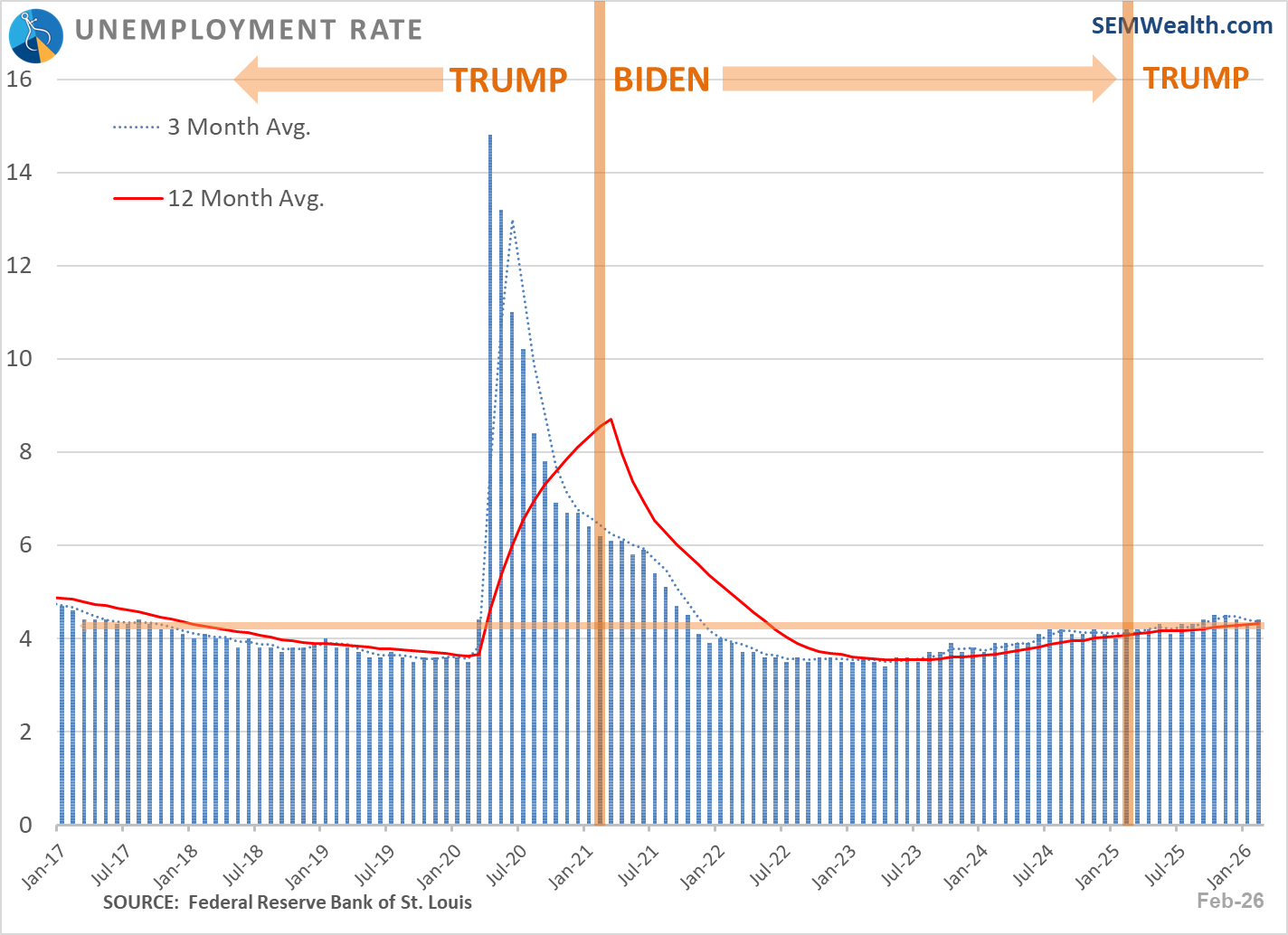

The unemployment rate also hasn't spiked. It's gradually moving hire, but not at a rate to be concerned about.

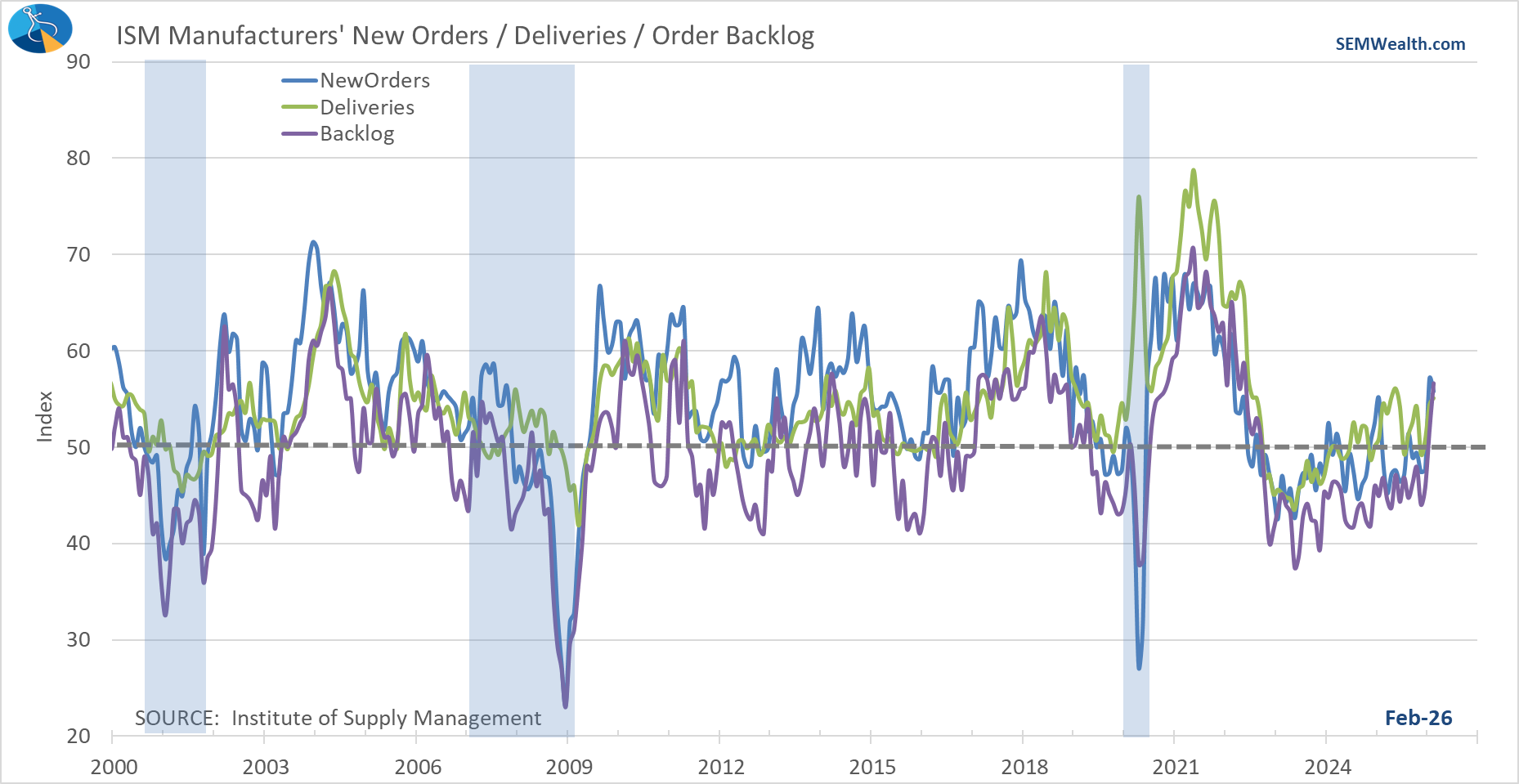

The February Manufacturing Index also showed the leading indicators all moving higher.

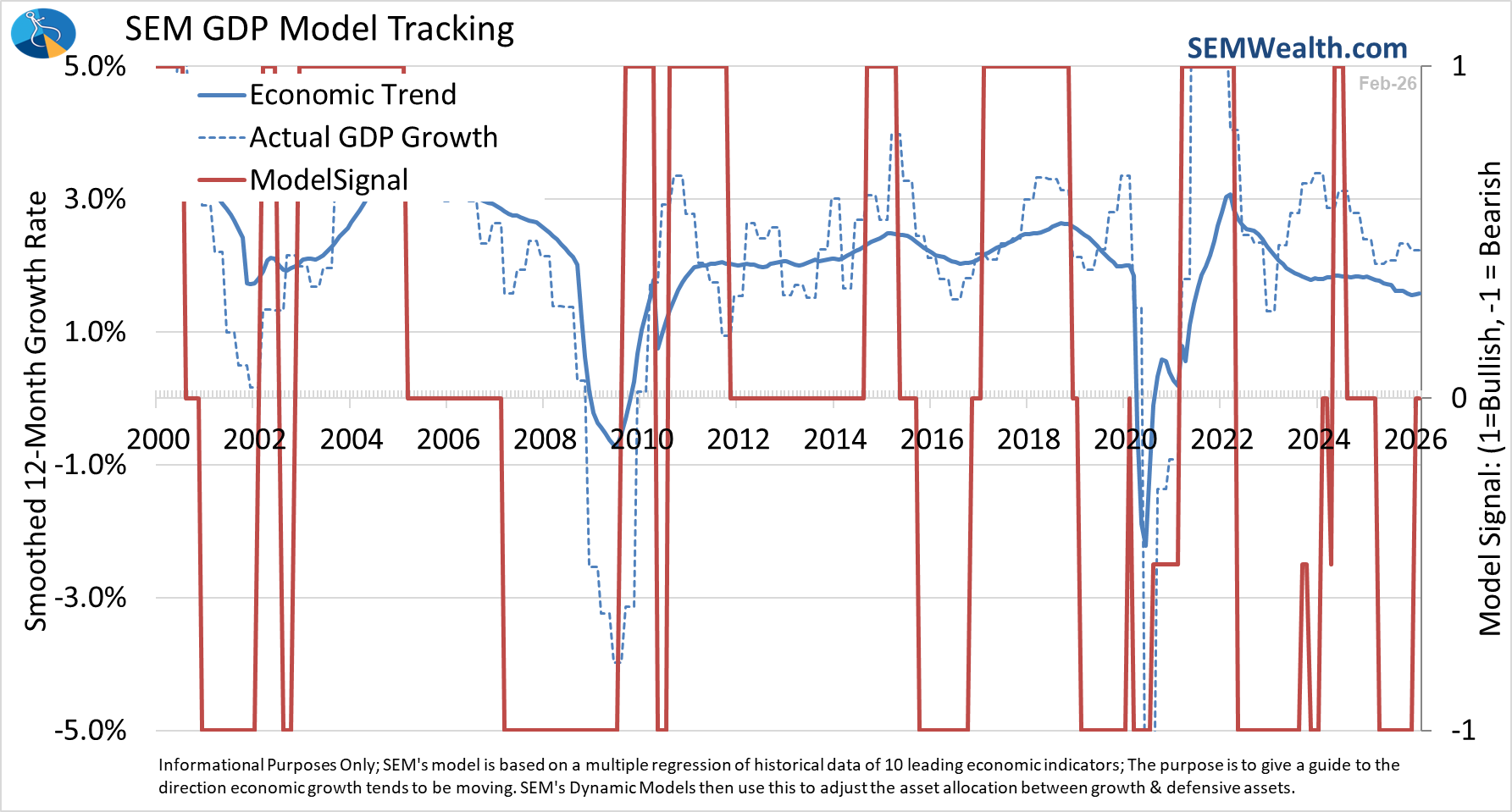

Combined with all of our other leading indicators I would summarize the economy as "stable". It does appear to be weakening, with more of our indicators negative than positive.

The model is hanging on by a thread to the "neutral" level. The rest of the economic data throughout the month will determine whether we move back to "bearish" in our model.

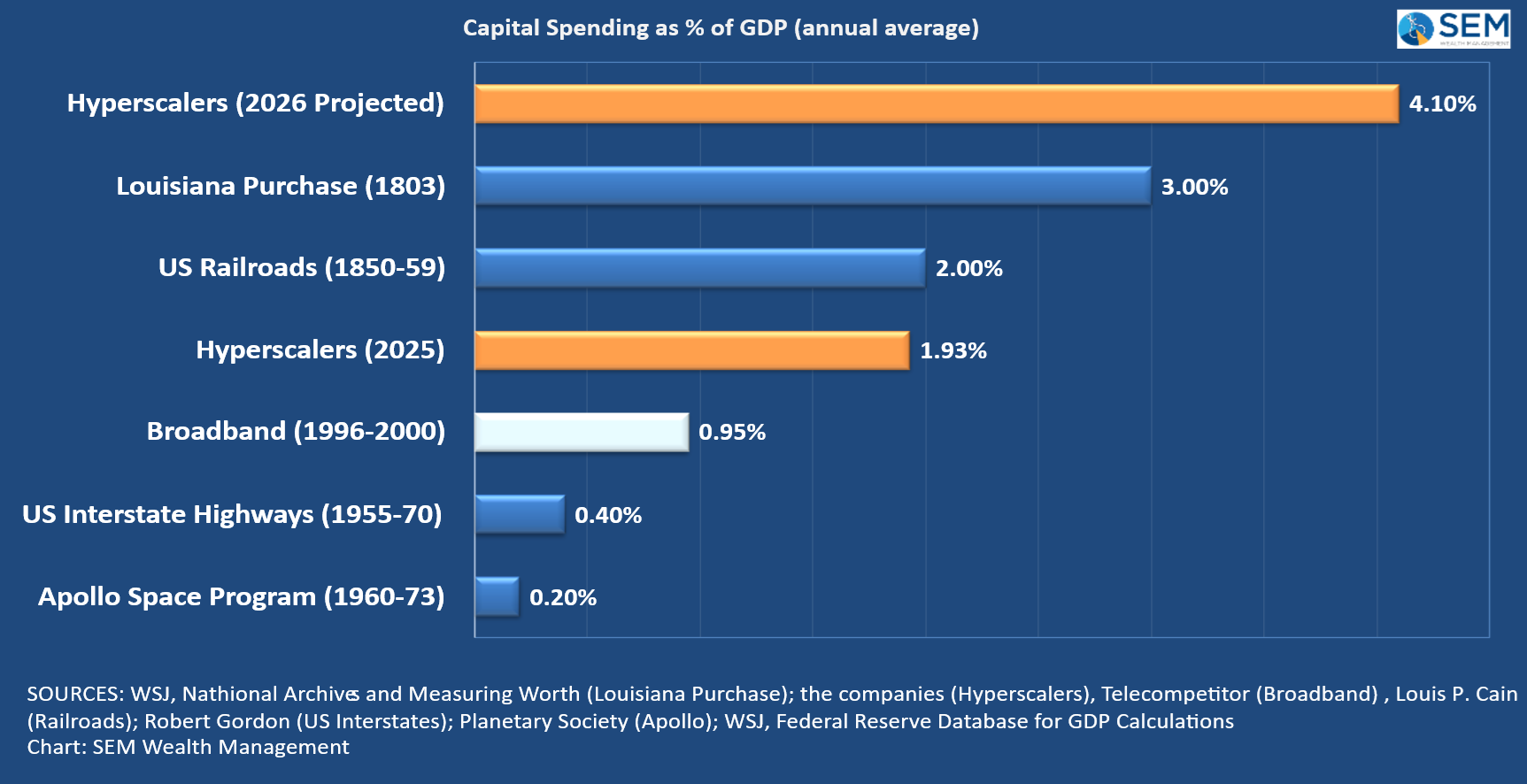

Will Data Centers Save the Economy (again)

Our economic model has obviously been out of alignment with the growth of the stock market. It went "neutral" in August 2024 and then bearish in July 2025. This came at a time of very strong S&P 500 earnings growth. While it is difficult to get an exact number, spending on data centers in 2025 represented 1/3 to 1/2 of our GDP growth last year. The 4 so-called "Hyperscalers" (Alphabet, Microsoft, Amazon, and Meta) spent 2% of GDP in 2025 and are projected to spend 4% of GDP in 2026. Without that spending, it is clear our economic model would have been correctly "bearish" and we would be looking at a recession.

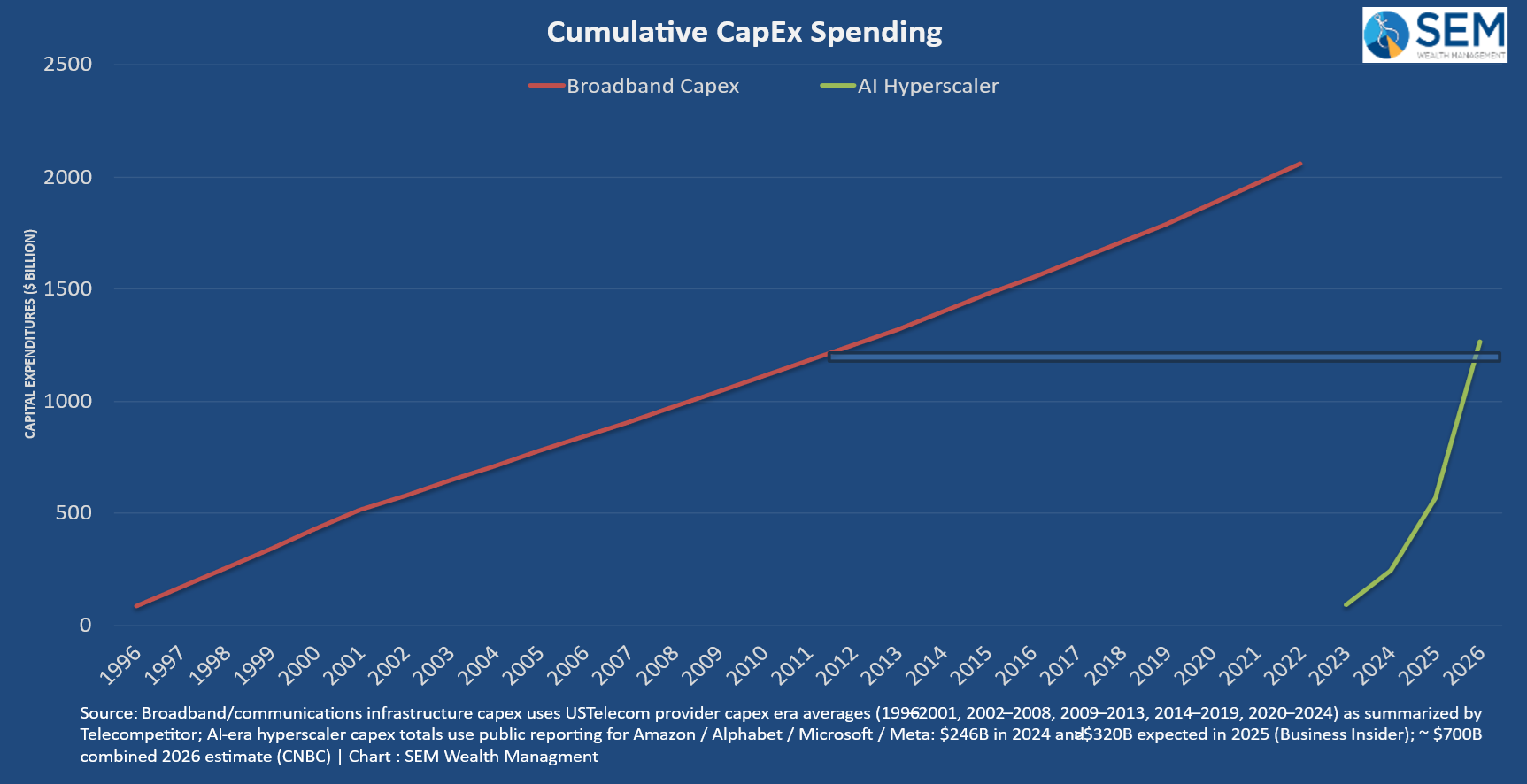

To put the spending in perspective, I plotted the cumulative spending to buildout our broadband network with the cumulative spending of these 4 "Hyperscalers". In 3 years, these companies have spent 15 years' worth of "broadband" investments.

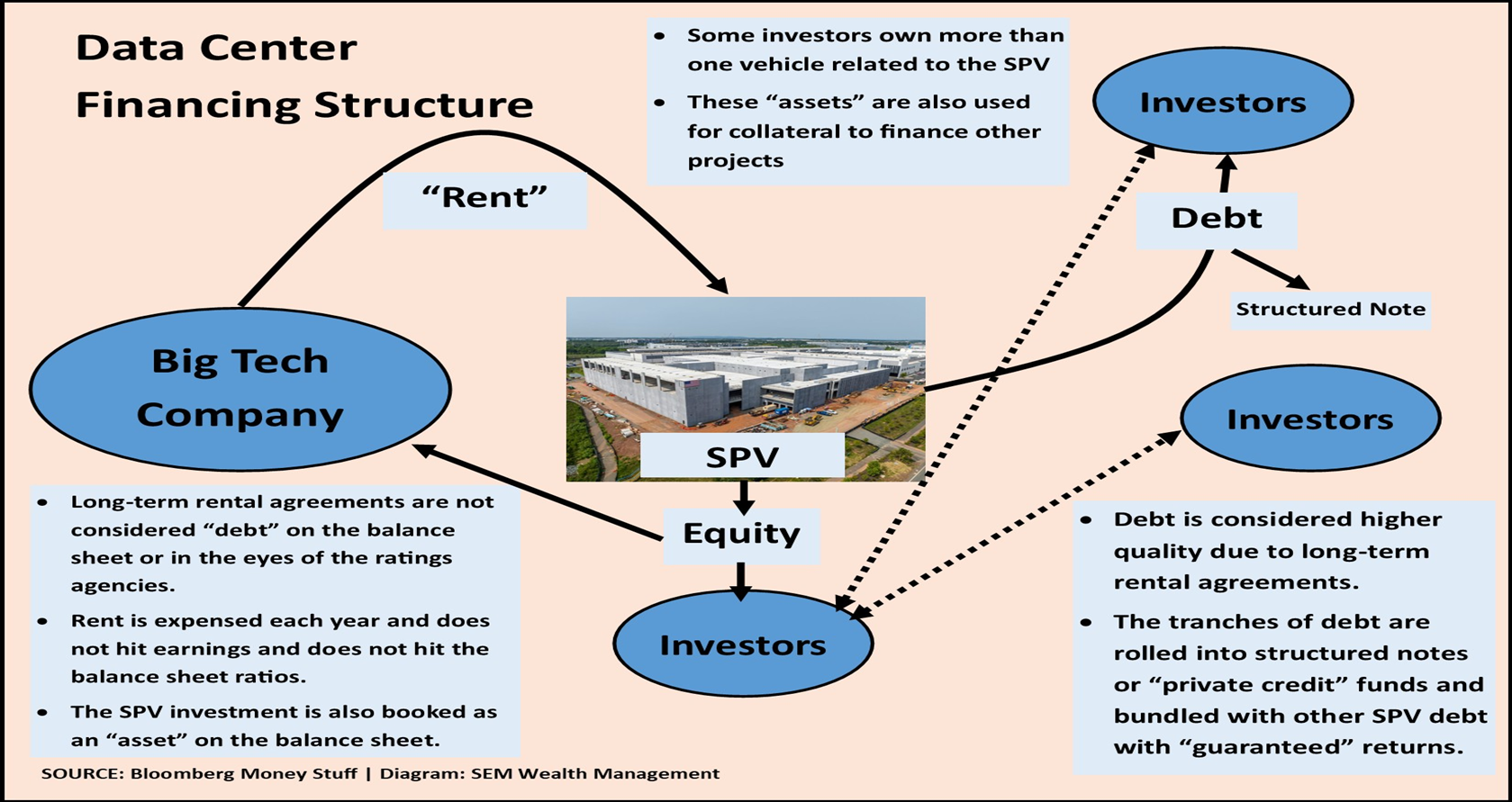

Throughout the 4th quarter, I lamented how my accounting brain was becoming increasingly uncomfortable with the creative financing for these data centers. Whereas early investments were from "free cash flow", most of the new data centers being developed last year were tapping the "private" markets. I put together this diagram illustrating how these deals work:

Last week we saw Blackrock join Blackstone and Blue Owl in "gating" any withdrawals from their private credit funds. While we have zero visibility into what is in these funds, we do know which publicly traded firms have issued the most of them. The market is obviously concerned, which means future data center spending may be more difficult to finance, taking out a key driver of economic growth.

Inflation Pressure Ahead

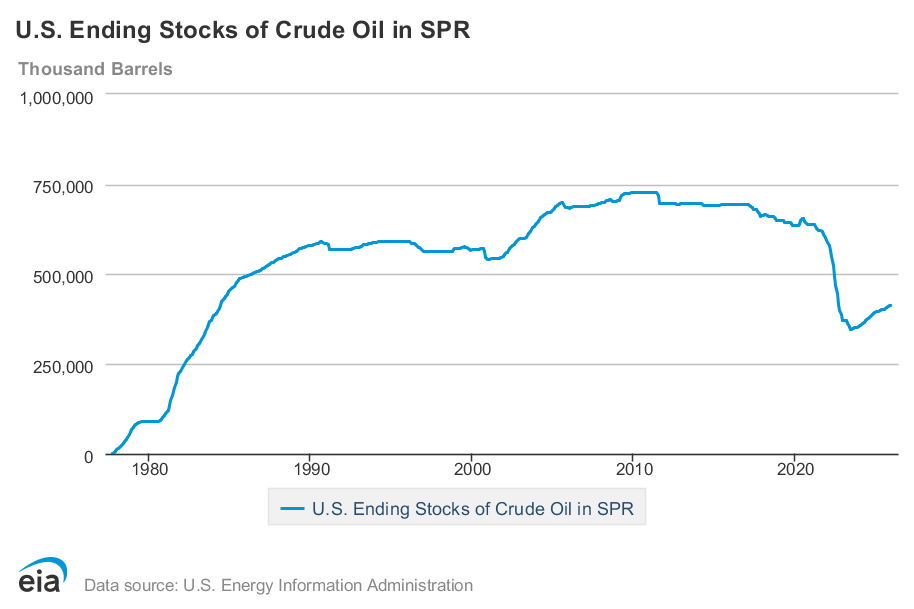

The news of the weekend was the huge spike in oil prices as the Strait of Hormuz is essentially closed.

There is talk this morning of the White House releasing inventory from the Strategic Petroleum Reserves (SPR). The last time this was done was in March 2022 to fight the oil price spike related to the war in Ukraine. While that didn't immediately help, prices did start to come back down. They'd been in a nice downtrend since the middle of 2023.

You can see the last drawdown here:

The big question here is why didn't the US replenish the SPR when oil prices were so low the past 12 months? There was talk about doing so and we did add a little to our reserve, but we are in a much weaker position than where we should be at this point. This spike in oil should be temporary, but it will have an impact on the months ahead.

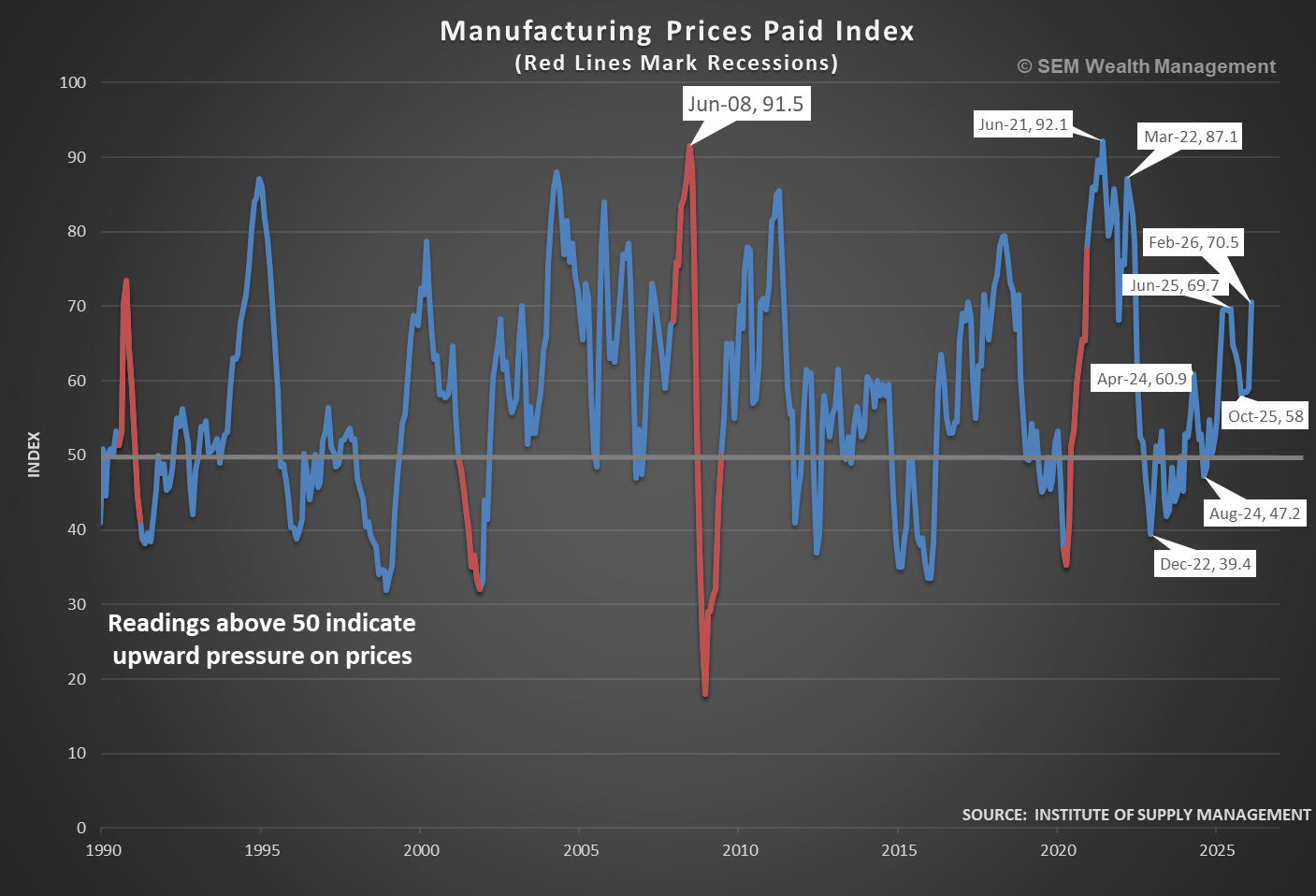

The bigger problem is, the inflation pressure isn't just due to the attacks on Iran. The ISM Manufacturing Prices Paid Index spiked to the highest levels since 2022 in February.

This comes at a time where the inflation indexes appear to have flattened over the past 12 months.

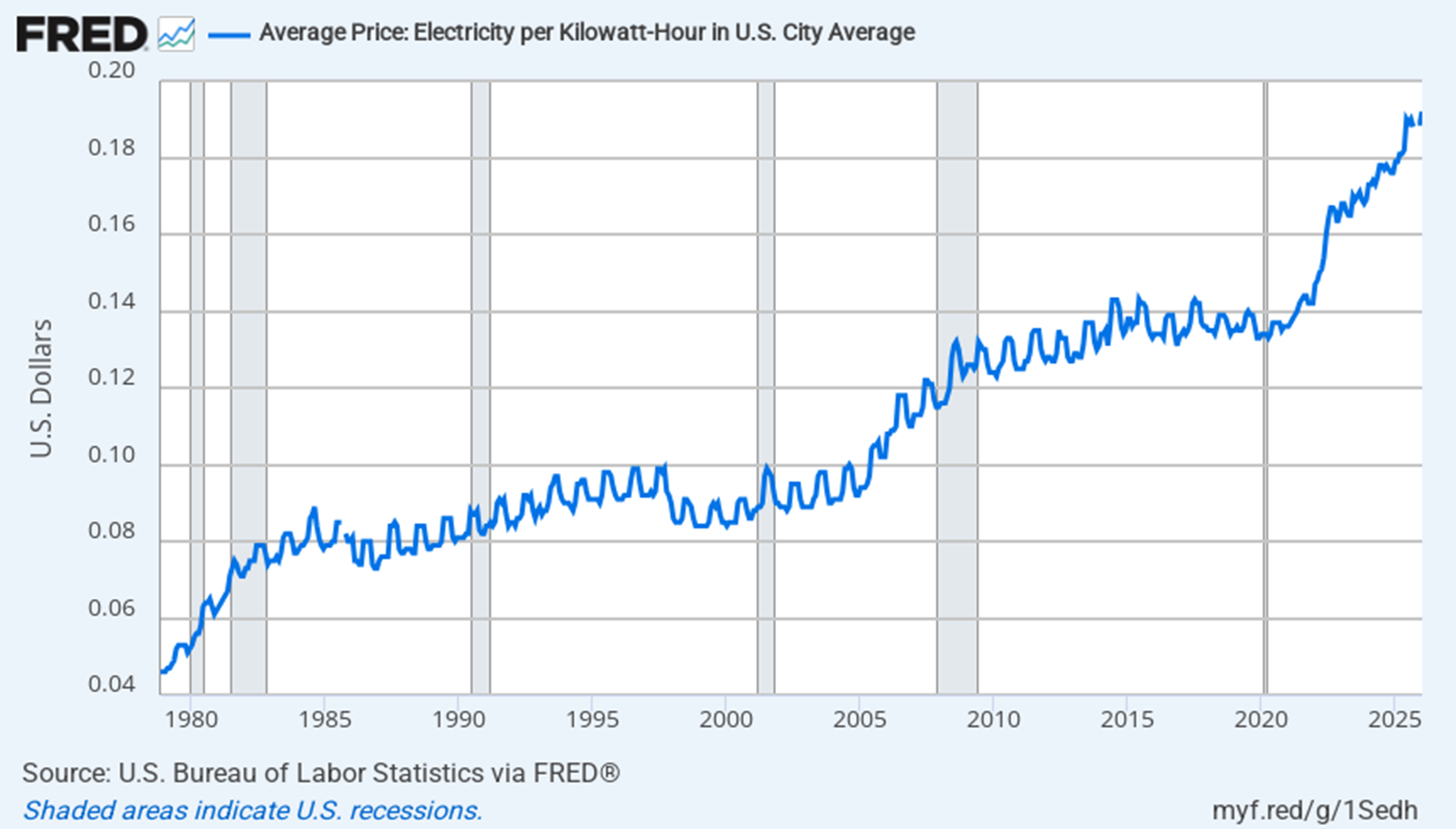

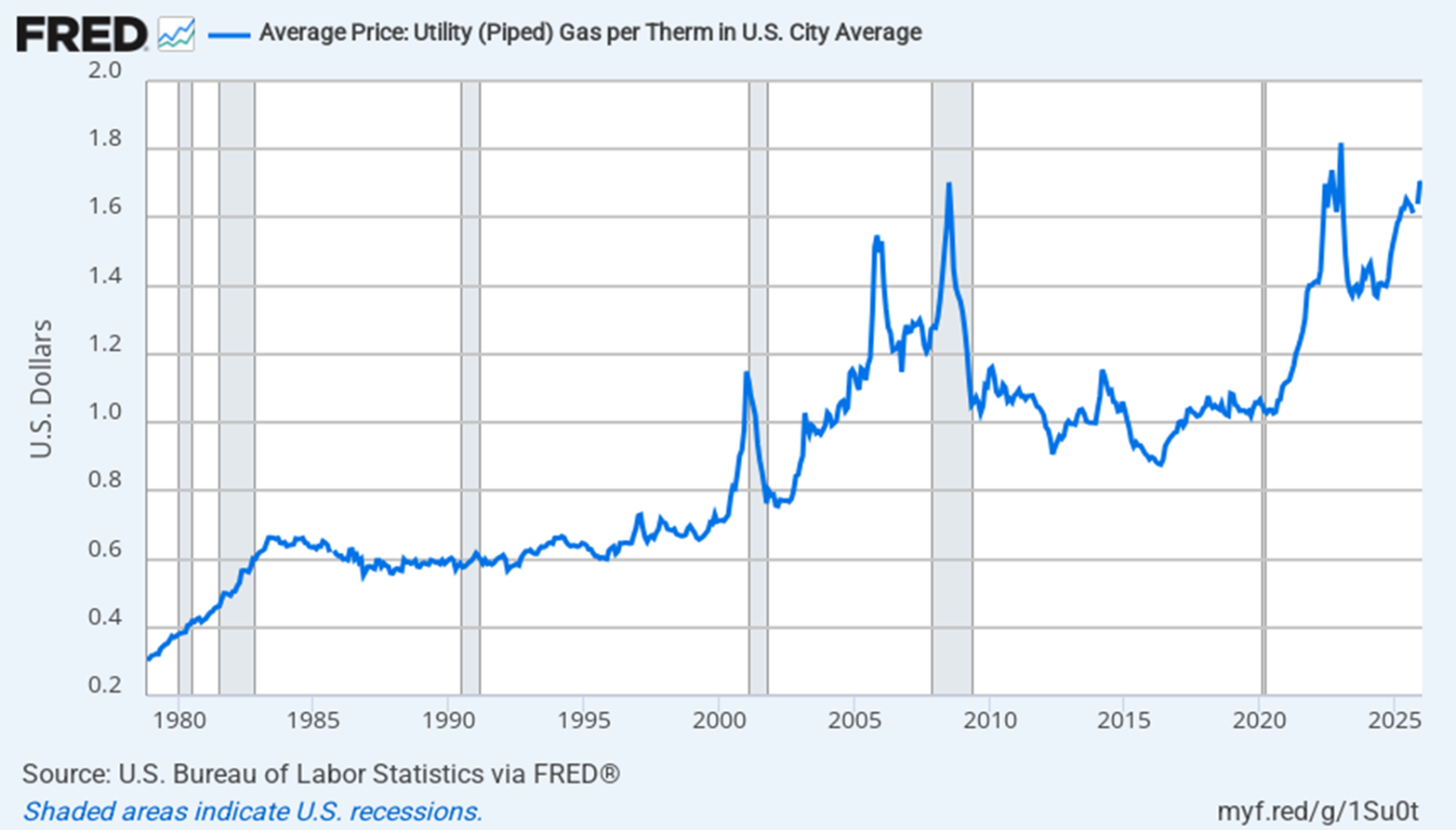

Even before this spike in oil, consumers have been complaining about a big increase in their utility bills. States with large data centers are seeing the biggest spike. While the White House has said they will make the technology companies pay for the necessary improvements to the infrastructure, that's easier said than done given that each state has different laws. For instance, in Virginia, Dominion Energy cannot add the surcharge for data centers until 2027. This means the consumers will continue to pay higher rates throughout the year.

Regardless, the increasing demand from these data centers with not enough supply is making utility bills higher.

I should be clear – we are nowhere near the stagflation years of the 1970s, but we are on some very unstable footing where the wrong policy decisions could easily throw us into a recession. As always, we will be watching all of our models closely, ready to take action when the DATA dictates.

Toby's Take

A look at our intern's top WSJ articles from last week

3/2/2026 - Trump’s Shifting Goals for Iran Complicate Military’s Mission - WSJ

The talk of the weekend going into today has been all about the U.S. attack on Iran. This has been planned for some time now having a specific goal in mind, restricting Iran's nuclear weapons. However, President Trump has had multiple different goals surrounding the conflict. The intention was to reduce nuclear and missile threat from Iran, but later President Trump said in a video to "take back your country" causing confusion of the initial intent. He has also changed the timeframe for this action originally saying on social media that it will last a week or more, but a day later he said that the fighting has "always been a four-week process." The confusion surrounding this can disrupt the analysis on when this conflict will be over and what the outcome is going to be.

3/3/2026 - Iran Conflict is Starting to Boost Gasoline Prices - WSJ

The conflict in Iran is causing lots of uncertainty here at home already causing lots of stock values changing. However, another side effect of this conflict is it is causing oil prices to go up! We are already struggling with expensive gas, but with them going up even more it is threating to our pockets. Try to be conservative with driving to limit spending until this conflict is over to have things level out again. Hopefully.

3/4/2026 - In a Day of Wild Market Moves, Oil Is a New Haven - WSJ

Oil is easily one of the most talked about resources in exports and imports. We use it every day as citizens going about our life. The United States is the World's biggest oil producer. The conflict in Iran right now is causing a rise in oil prices which should be benefiting our companies, but it is tied to higher inflation which is actually hurting us. Also we feel it with more expensive gas!

3/5/2026 - Judge Orders Government to Begin Refunding More Than $130 Billion in Tariffs - WSJ

After the Trump administration's global tariffs were invalidated by the Supreme Court last month, over 2000 companies started to file lawsuits for refunds. This includes big names like Costco Wholesale, FedEx, and Pandora Jewelry. There is no doubt that the Federal Government and national debt benefited from these tariffs, they just weren't done the right way. This could shake things up in the market while it gets resolved.

3/6/2026 - Its Missile Threat Degraded, Iran Is Taking Fewer Shots at More Targets - WSJ

The United States and Israel have worked together to blunt Iran's sword by taking out their missile stockpiles and launchers. So far, they have done a great job lowering their missile launches by 90% from the first day and their drone attacks by 83%. However, Iran still has a retaliation plan of using their low cost drones to fire at their neighbors across the Persian Gulf, causing trouble in markets and shipments of oils and goods from a crucial part of the world's economy. The result of other countries getting hit because of this conflict is those countries putting pressure on Washington to end the attack. We wait for more news on this development.

Market Charts

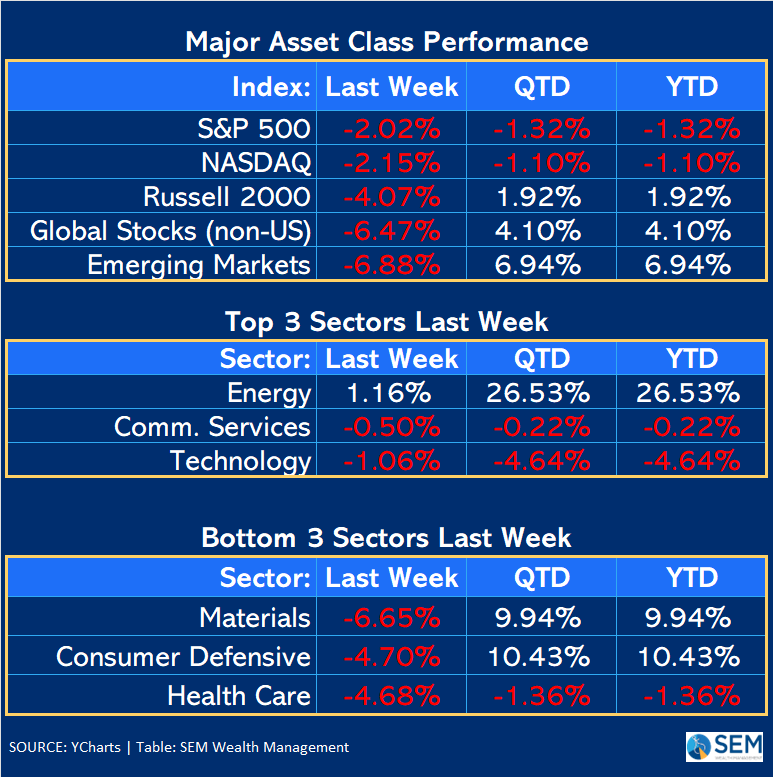

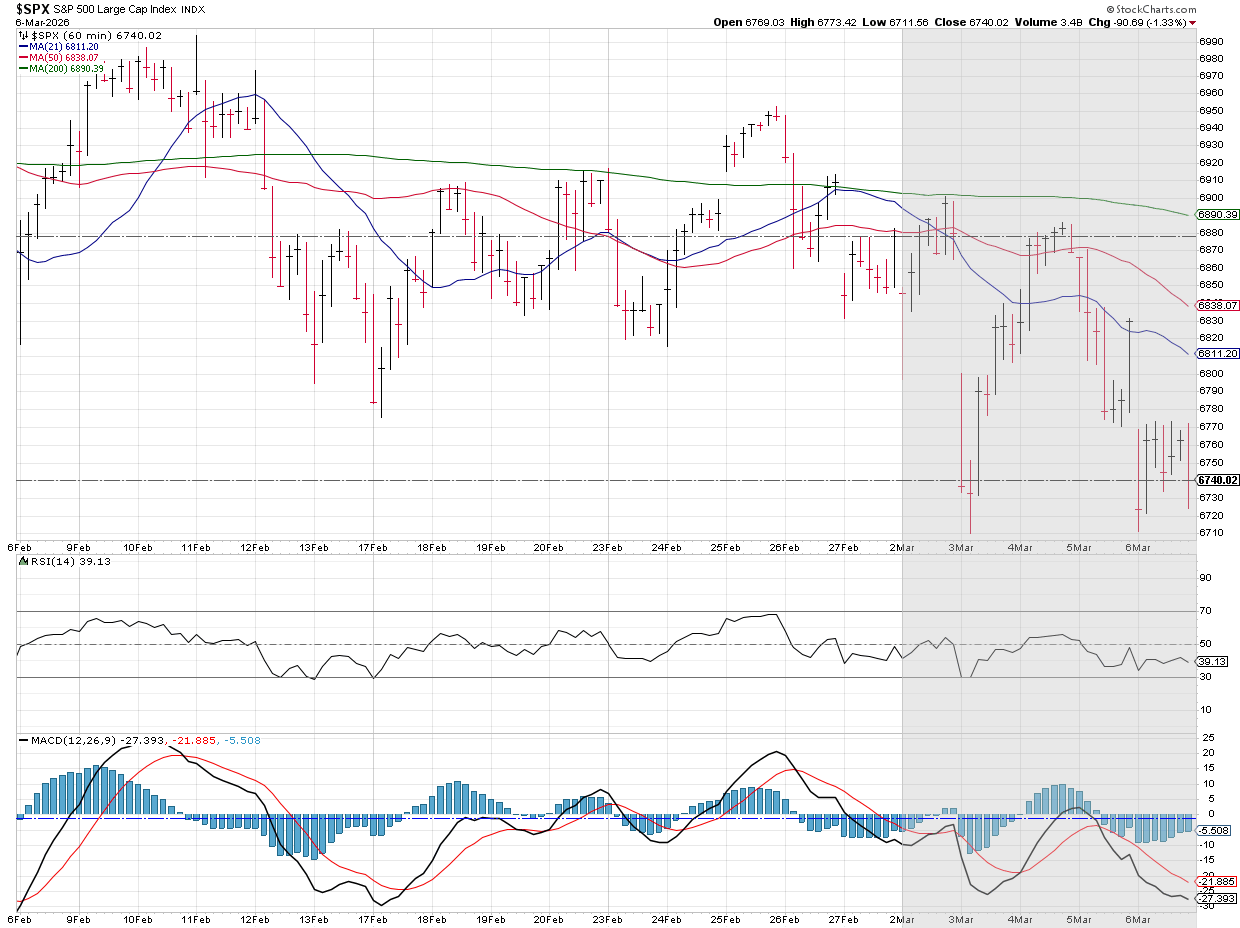

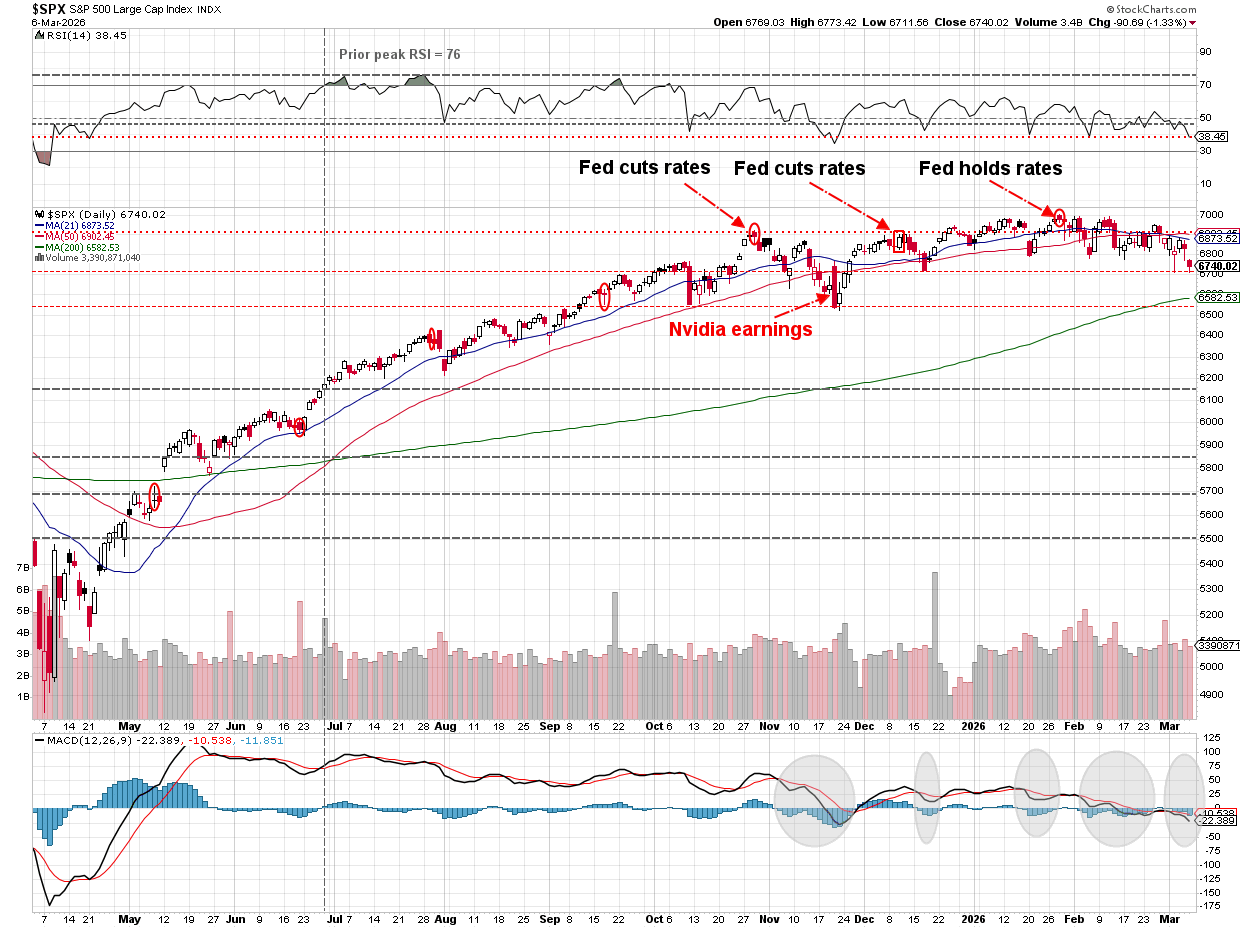

It was a rough week for stocks.

The S&P 500 is still stable, but the techncials are weakening. It looks like it will break 6700 this morning, with 6500 (the Q4 2025 lows) the next level we'd like to see hold.

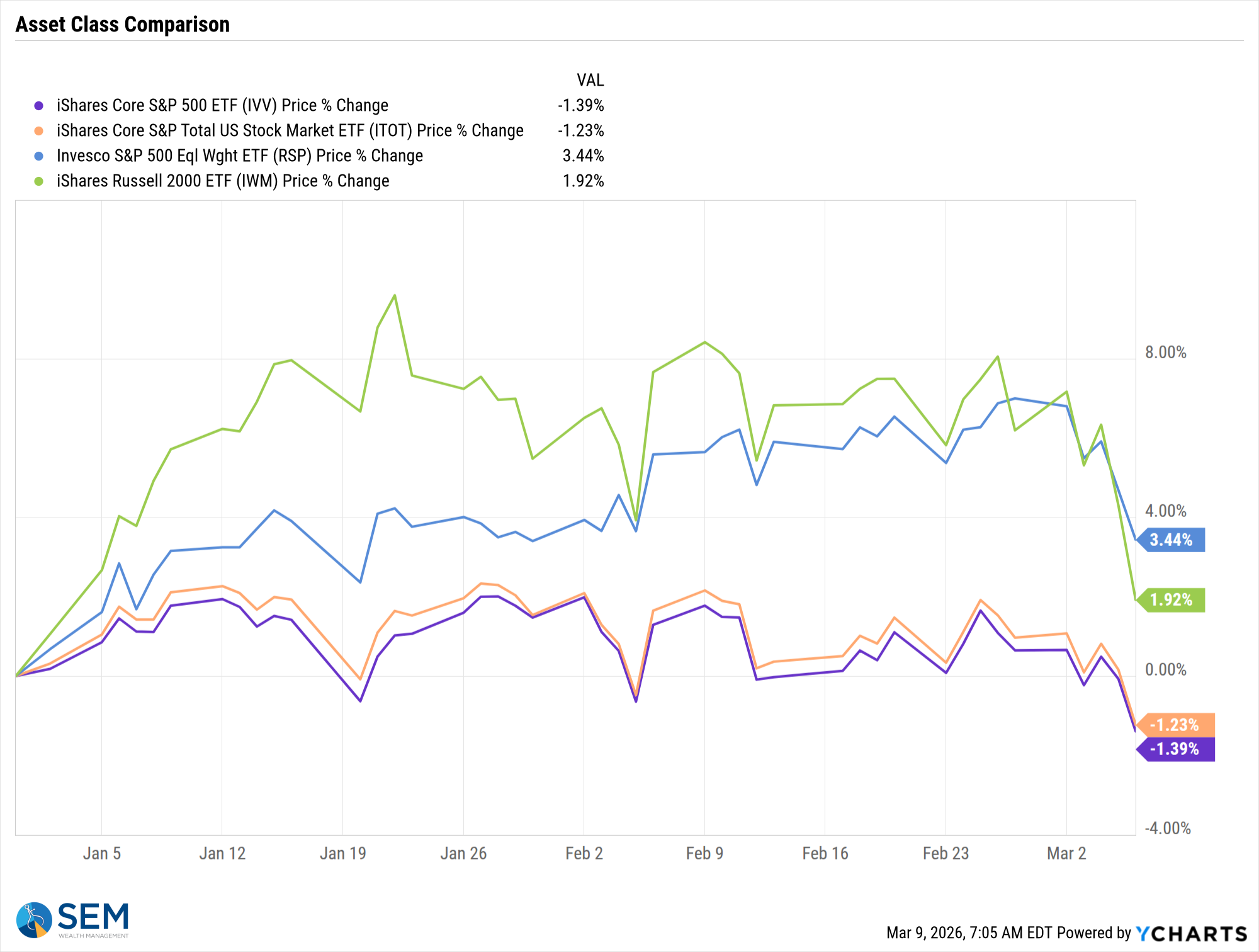

The "broadening" we've been enjoying in 2026 took a hit last week and logically so – if the economy is slowing and inflation is increasing, the smallest companies will be hurt the most.

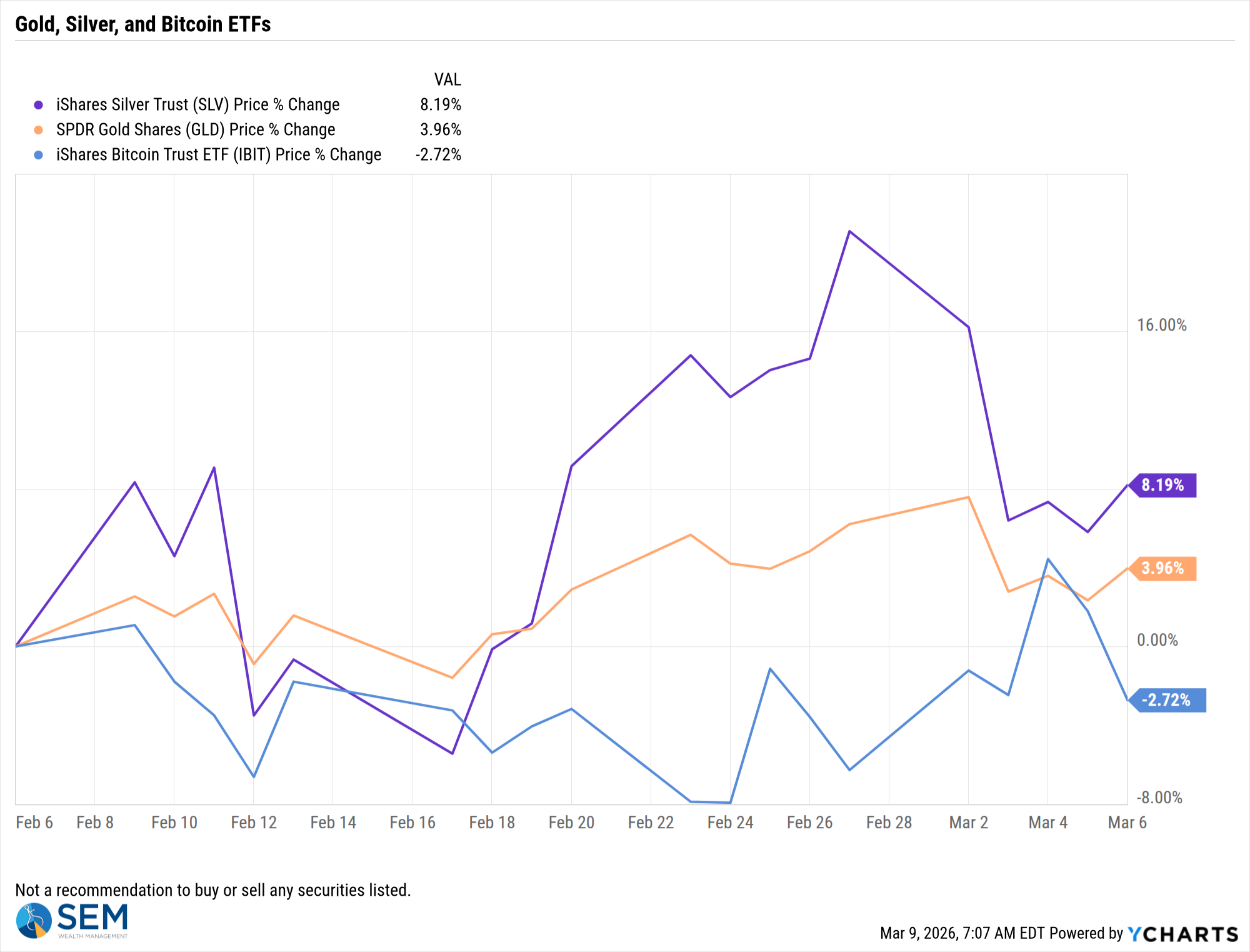

Gold, Silver, and Bitcoin continued to march to their own drummer. In "normal" times, Gold should have had a strong week, but instead lost ground last week.

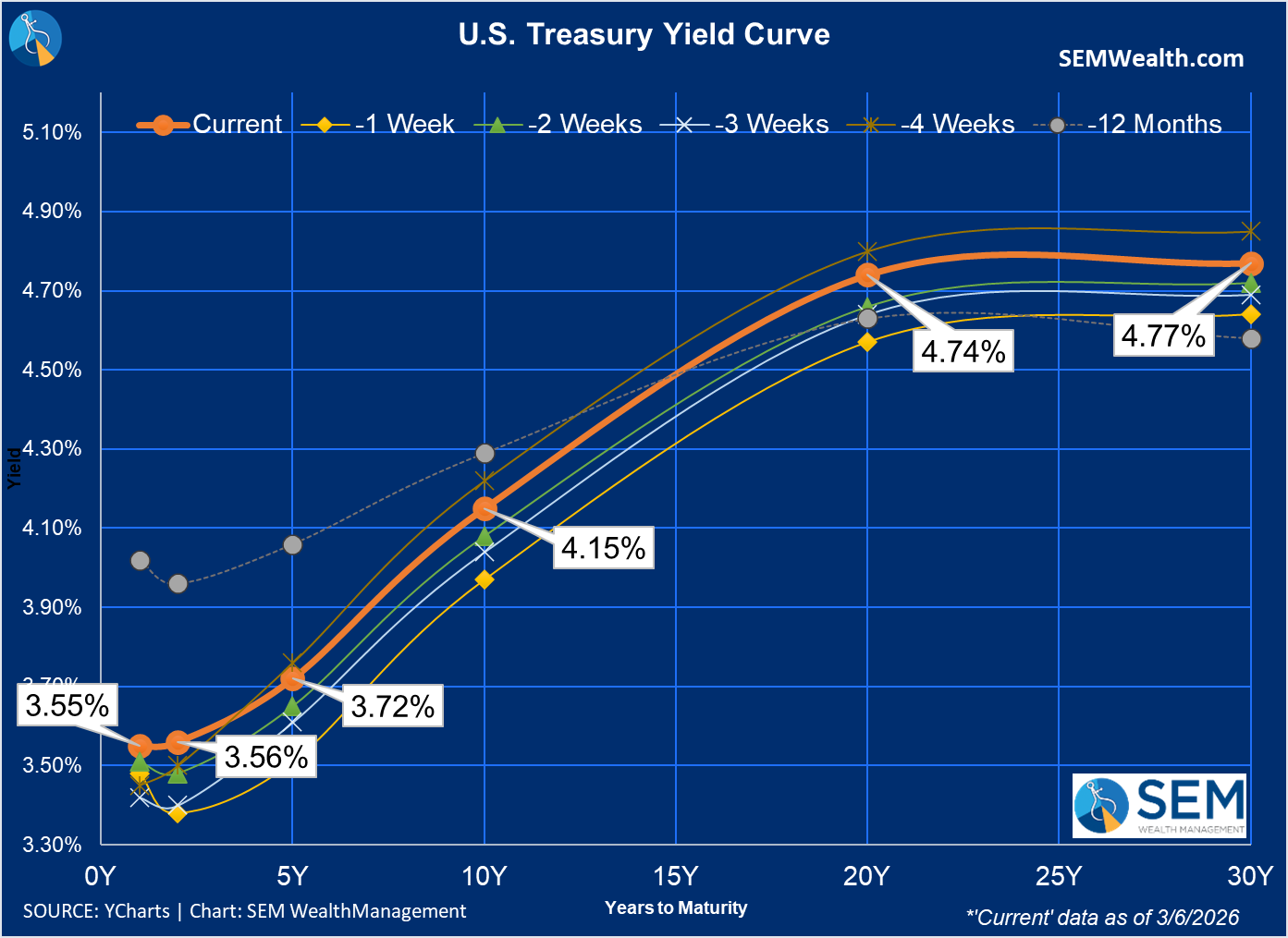

Interest rates were higher across the board last week.

The 10-year Bond Yield Chart shows how volatile the longer-end of the yield curve has been.

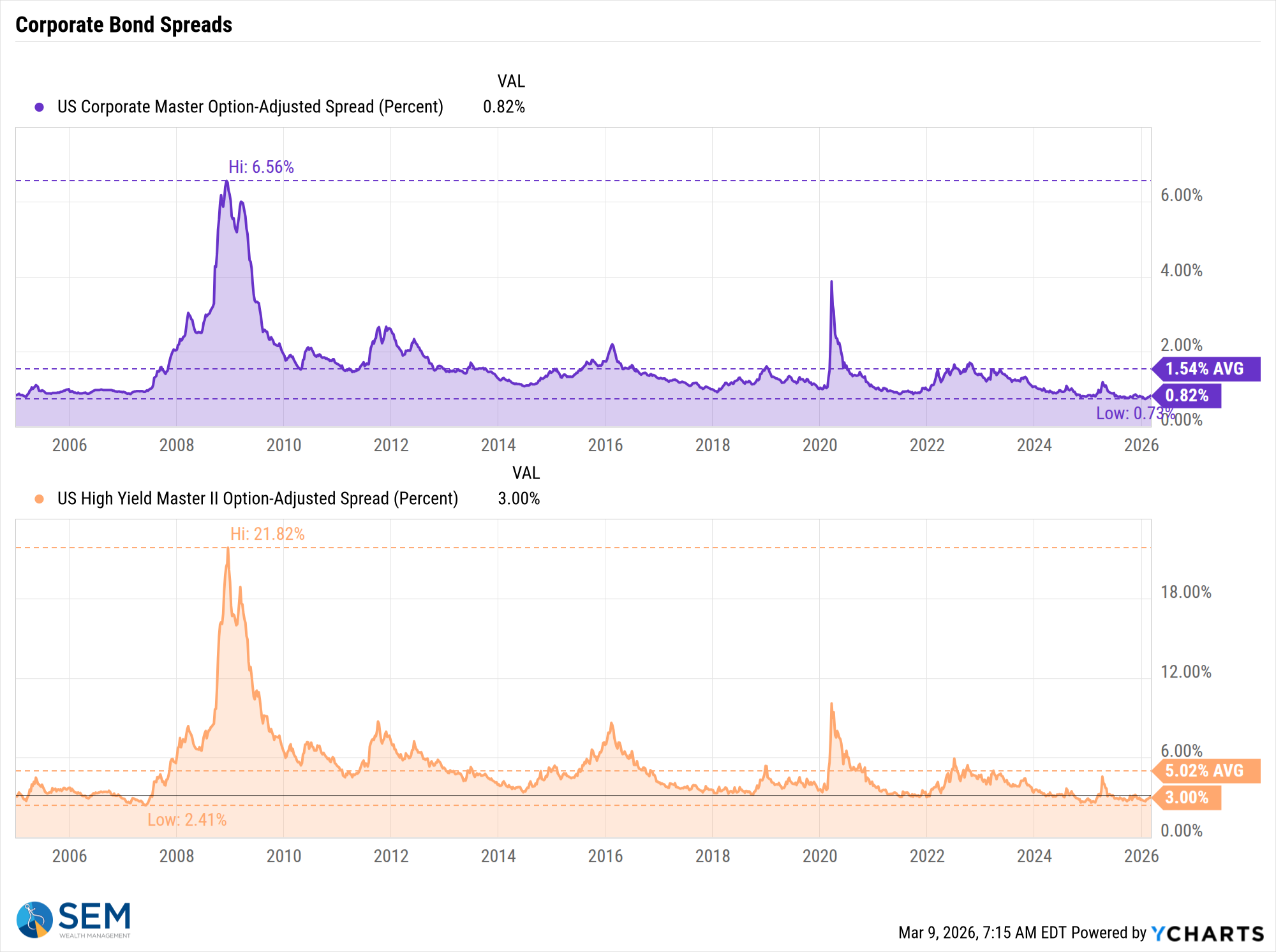

Despite the weakness, the public bond market does not seem to be concerned (yet). The spread between corporate bonds and treasury bonds has barely moved up.

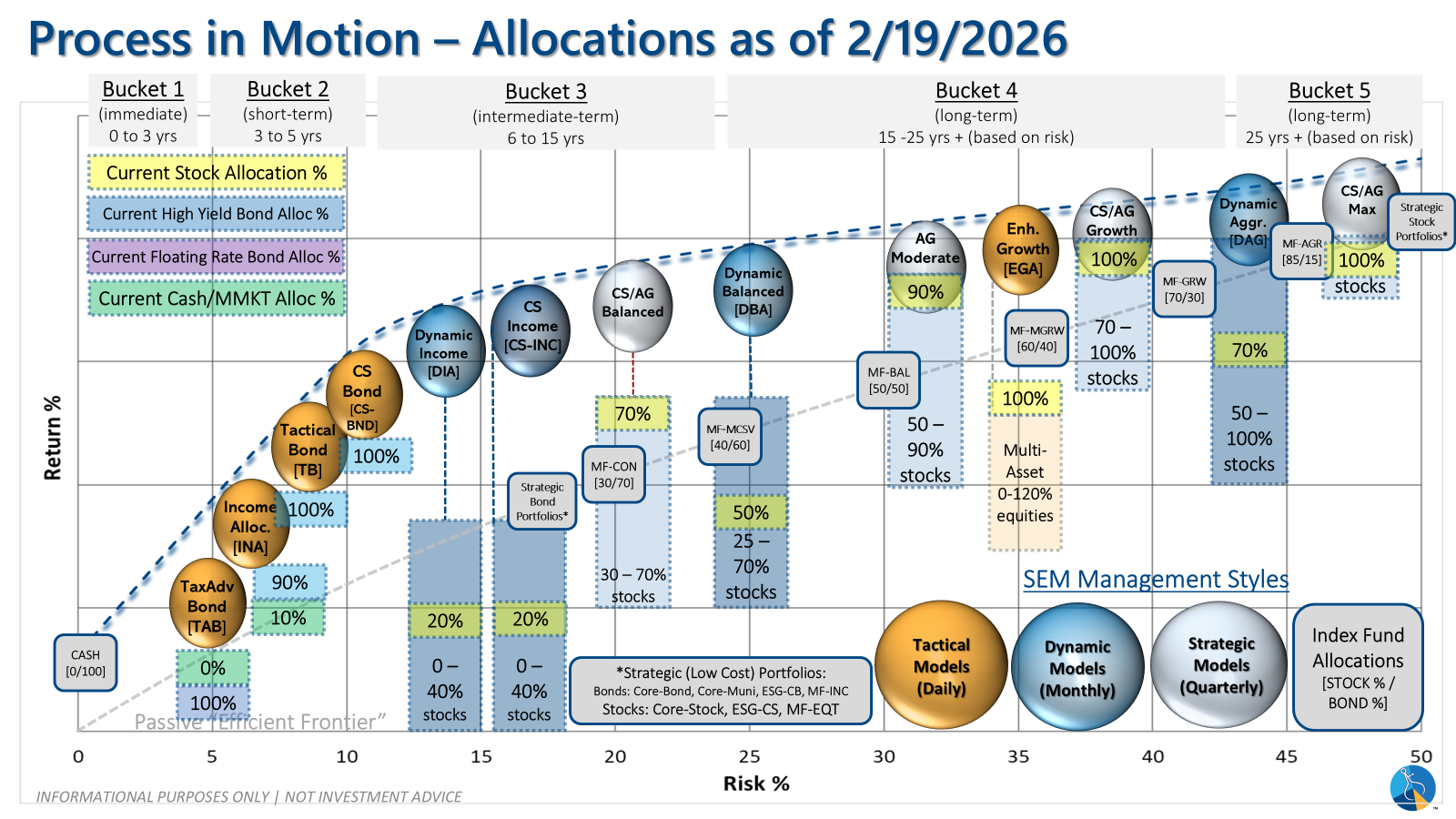

SEM Market Positioning

| Model Style | Current Stance | Notes |

|---|---|---|

| Tactical | 100% high yield | High-yield spreads holding, but trend is slowing-watching closely |

| Dynamic | Neutral | Economic model turned neutral Feb 15 '26' – benchmark weightings |

| Strategic | Fully invested | Trend overlay shaved 10 % equity in April -- added back early July |

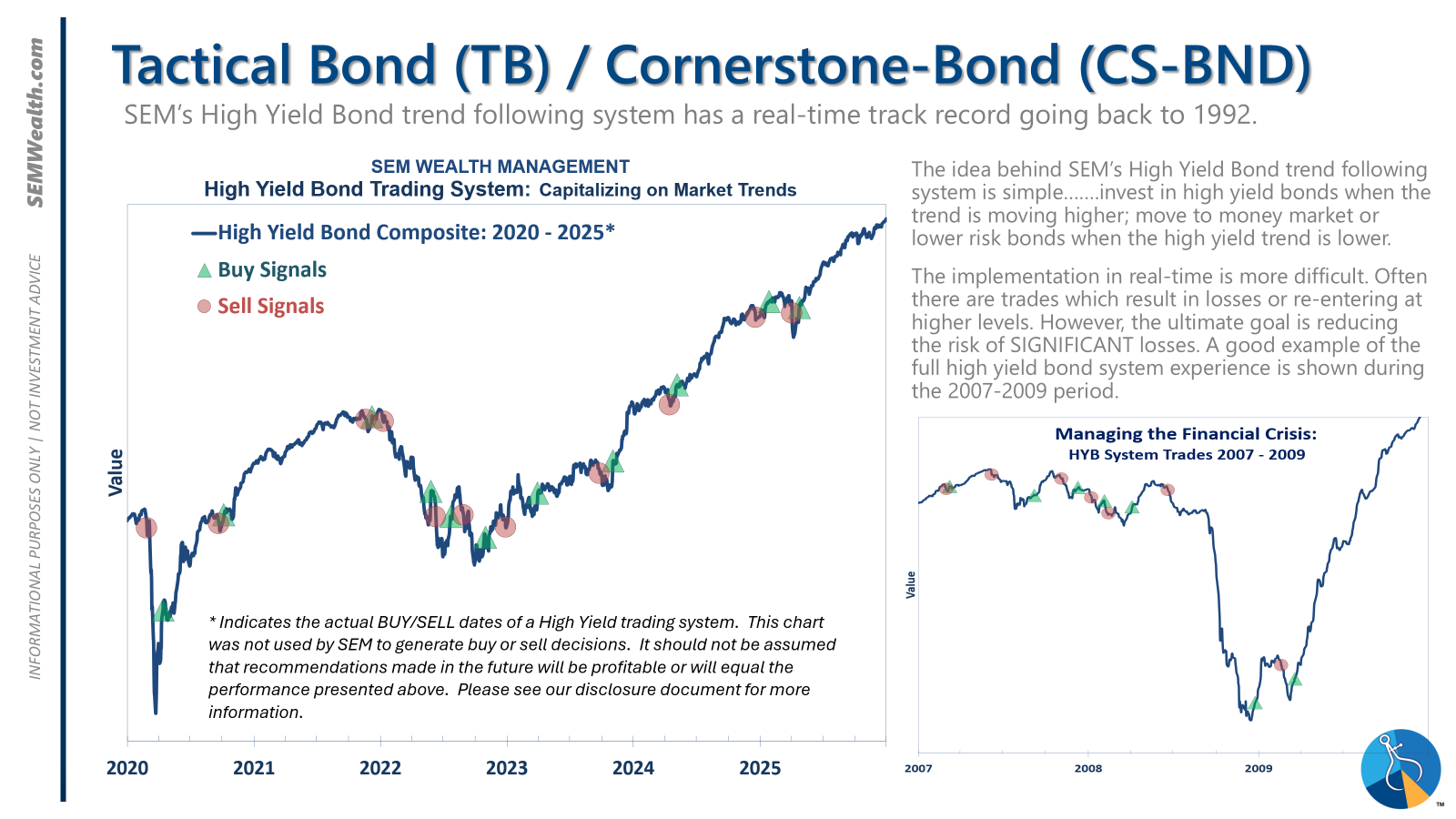

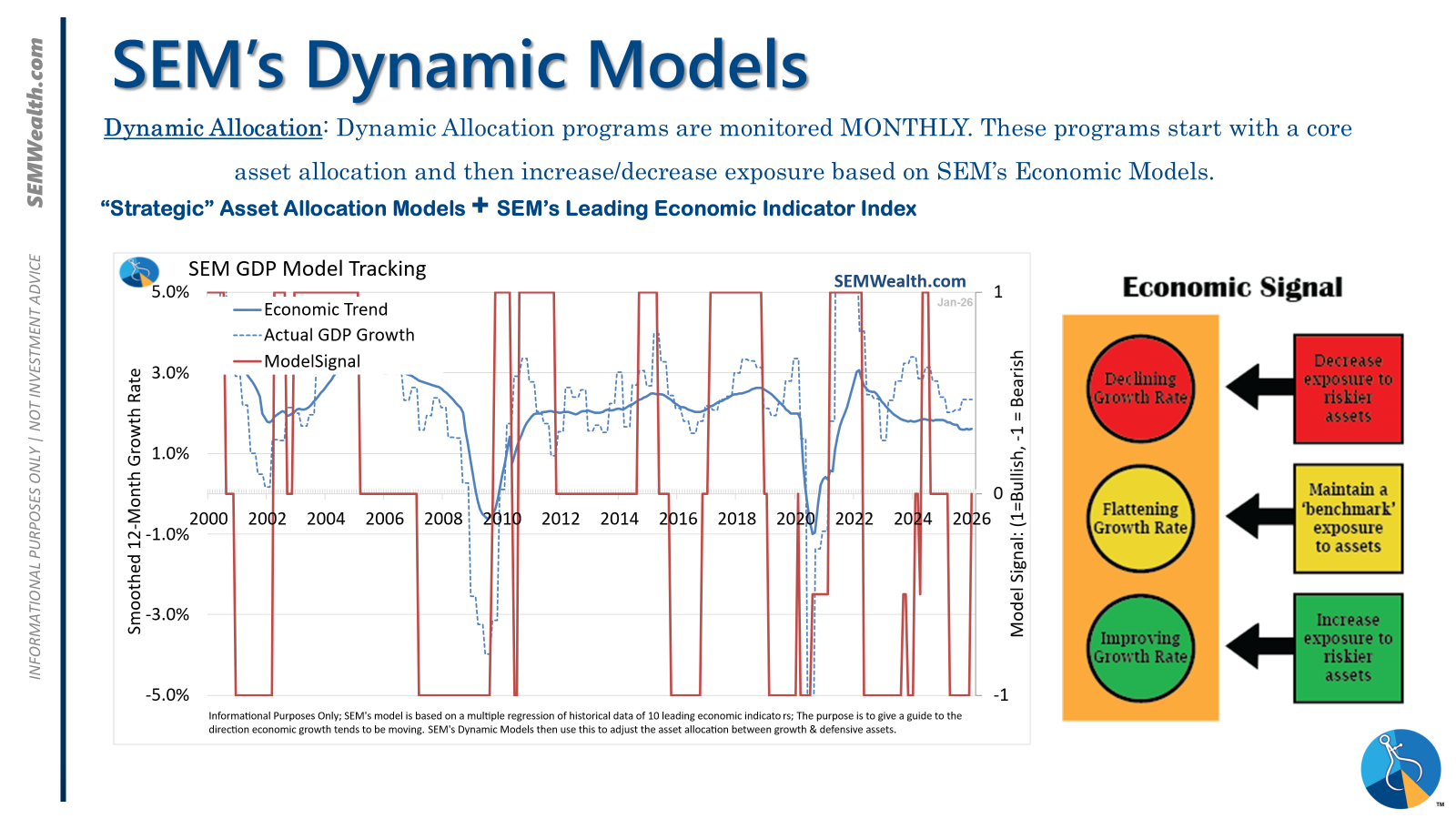

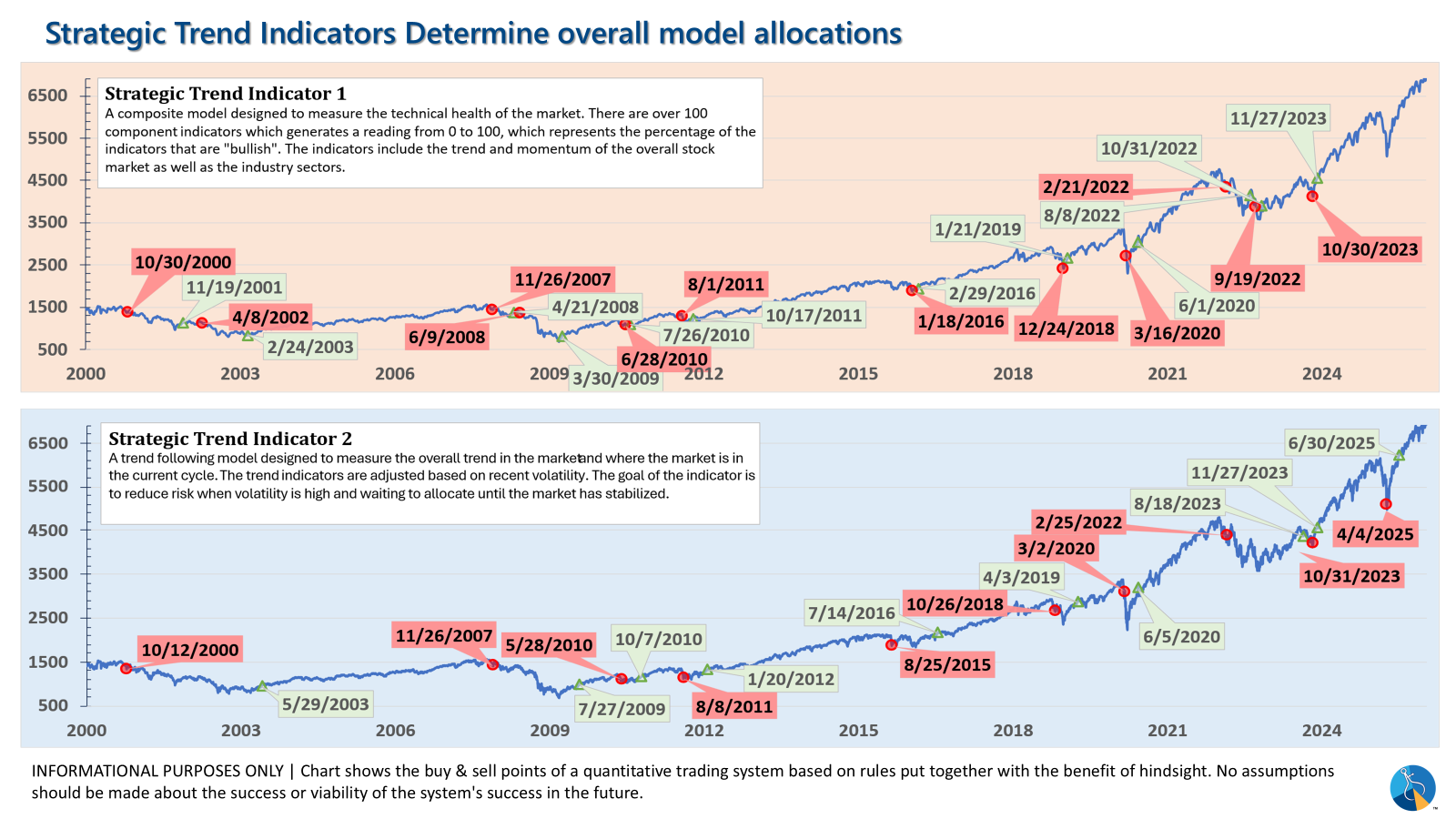

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

Tactical (daily): The high yield system has been invested since 4/23/25 after a short time out of the market following the sell signal on 4/3/25.

Dynamic (monthly): The economic model went 'bearish' in June 2025 after being 'neutral' for 11 months. This means eliminating risky assets – sell the 20% dividend stocks in Dynamic Income and the 20% small cap stocks in Dynamic Aggressive Growth. The interest rate model is 'bullish' meaning higher duration (Treasury Bond) investments for the bulk of the bonds.

Strategic (quarterly)*: One Trend System sold on 4/4/2025; Re-entered on 6/30/2025

The core rotation is adjusted quarterly. This quarter we saw half of our international positions reduced (we sold developed markets and kept our emerging markets exposure). We also saw the remaining share of mid-cap reduced in favor of more small cap exposure. We remain with a "barbell" core portfolio – about half in large cap and half in small cap as the models expect the market to "broaden".

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

Overall, this is how our various models stack up based on the last allocation change:

Curious if your current investment allocation aligns with your overall objectives and risk tolerance? Take our risk questionnaire