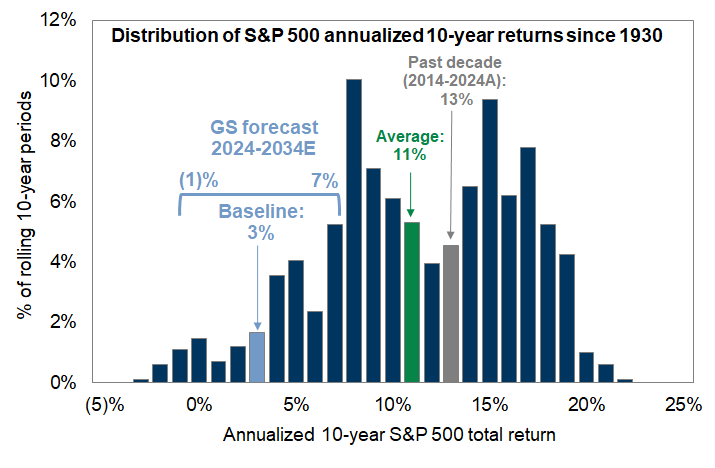

Proper Expectations are Key

Over the long-term, the S&P 500 has averaged a 10% return. Over the past 8 years, we’ve seen 5 years of 20%+ returns, including the past two years. Stocks also posted losses of 4% and 18% in 2 other years. When investing, one of the most important keys to success is properly setting expectations for your returns. Doing so (theoretically) would prevent you from being disappointed with short-term results and possibly making adjustments which would be detrimental to your long-term chances for success.

So what should you expect for the stock market? It depends on your time horizon. Over very long periods of time (15+ years) history tells us returns around 10% are reasonable. The shorter the time horizon, the more variable the returns. In addition to this, other factors such as the overall valuation of the market, the economic environment, and whether we are following an extended period of gains which were well above or below average will influence future returns.

Last quarter we discussed Wall Street’s expectations for stocks. Nearly every firm started the year believing stocks would post average to above average returns. Only one firm predicted below average returns. While this is possible, the simple fact stocks have had an extended period of well above average returns should be a warning that some sort of reset/correction is on the horizon.

For the latest market updates, subscribe to the blog.

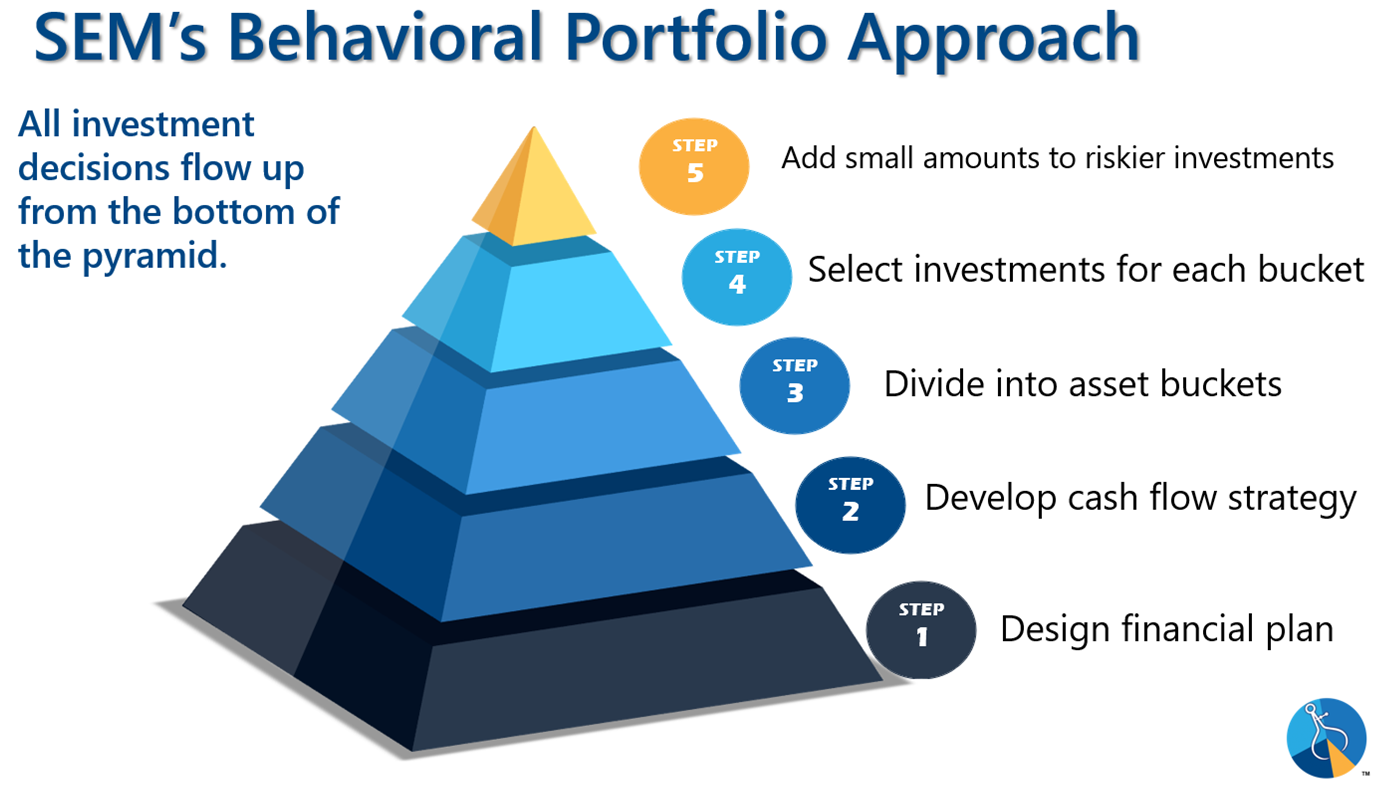

The Value of Financial Planning

Over the past several months the value of financial planning has been apparent. The more the markets fluctuate from seemingly non-stop headlines, the more important it is to focus on the big picture and the end goal. SEM’s Behavioral Portfolio Pyramid highlights this with the foundation of every decisions starting with the Financial Plan. These plans do not have to be sophisticated, 50+ pages of paper (although some situations may call for this), but rather a roadmap for how much money is needed and how it will be used in the future.

Whenever somebody asks us if they think they should increase (decrease) their allocation to stocks, our answer is simple – has your financial plan changed? If not, SEM’s customized investment portfolios were set-up to increase (decrease) the allocation to equities based on your customized financial plan, cash flow strategy, and risk personality. This is valuable in all markets, but especially in “noisy” ones like we have had the past few months.

If you would like a personalized review of your portfolio, go to Risk.SEMWealth.com

Economics 101

Part of setting proper expectations is understanding market and economic fundamentals. Here are a few important ones:

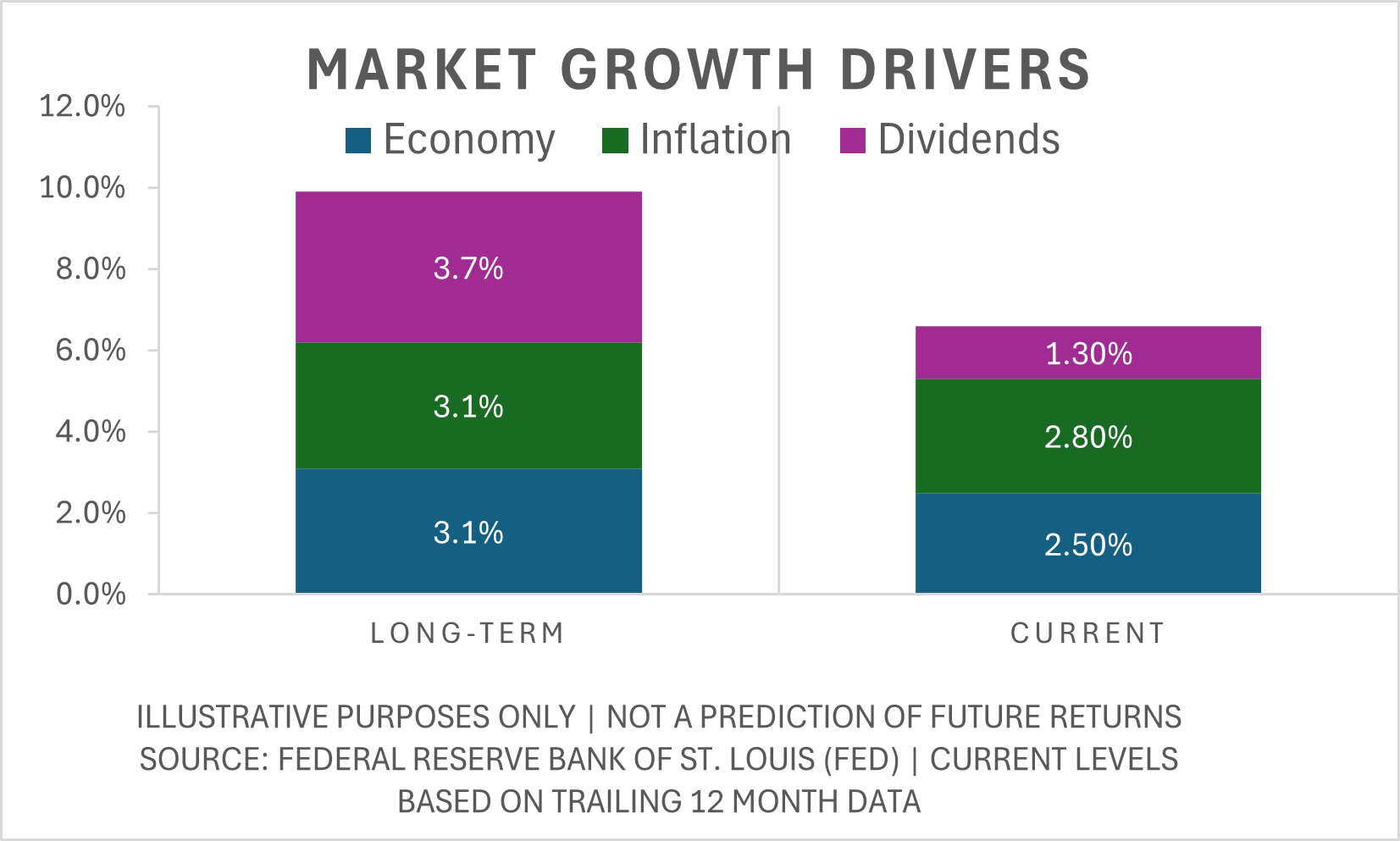

1.) Long-term market growth is driven by 3 factors

Mathematically, the growth of the stock market comes down to economic growth, inflation, and dividends. Going back to 1947, we can see these factors sum to 9.9%.

Looking forward, though, economic growth and inflation is tracking below average and the dividend yield is close to an all-time low set just before the technology bubble burst in 2000.

We need to see both economic growth accelerate and the dividend yield expand to get back to a sustainable long-term growth rate of 10%.

2.) Investors cycle between overly optimistic and overly pessimistic forecasts

The reason we see returns well above 10% for long periods of time followed by below 10% returns (or big losses) is because as humans we are programmed to believe the current environment will continue for the foreseeable future. When that doesn’t happen, corrections occur.

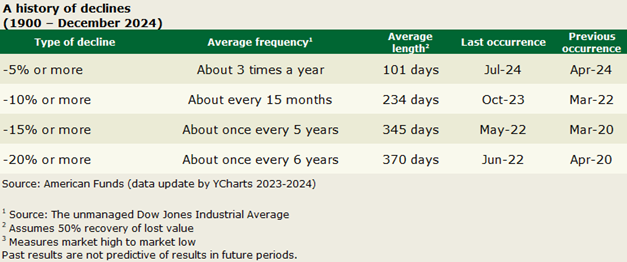

3.) Losses should be expected

Understanding the frequency and magnitude of losses is important for investors so they are not surprised when they occur. In the first quarter the S&P 500 lost 10% from the peak in early February to the low in mid-March. This came on the heels of a run-up of over 6% from election day through mid-February.

4.) Long-term economic growth comes down to workers and productivity

The growth of our economy comes down to a simple equation — how many people are working and how much are they producing. Any spending which doesn’t boost either of these reduces long-term growth.

5.) Deficits are a drag on long-term growth

When we borrow money to fund current spending or we import more than we export, we send money out of our economic system, which reduces long-term growth. If we allow the deficits to expand, the economy will not grow at its full potential, which means the stock market cannot grow at its full potential. This means future market growth would be impacted negatively.

For more, check out our bonus content below.

Bonus Content

"Liberation Day" Impact (short & intermediate-term)

After the market closed on Wednesday, April 2, President Trump announced sweeping trade policies. This so called "Liberation Day" event included both expected and unexpected changes that were seen as both positive and negative by the investment markets. SEM is by no means experts on trade policy, but we have been around long enough to understand the impact major economic policy changes could have on the markets.

Here are some of my notes:

- The tariffs were overall harsher than expected with a baseline level & on the surface a fairly opaque formula which will make tariffs significantly higher if there are any retaliatory tariffs.

- The way the "reciprocal" formula was said to be calculated is not the way most economists would have recommended, using things such as the "value added tax" charged on goods as part of the cost calculation as well as the deficit for that particular product, along with "currency manipulation and other trade barriers" (it's in the small print of the table presented by the President)

- This formula will hurt US companies who had relied on moving their supply chain out of China to more friendly countries such as Vietnam. Take Nike as an example. There are very few shoes made in the US with nearly all Nike shoes (and other brands) being made in Vietnam. This makes our shoe trade deficit with Vietnam over 90%. Using this formula, Nike will now pay significantly more to make their shoes there. Could they make shoes in the US? Maybe, but not at the price they are selling them today. They also couldn't find enough American workers willing to make the shoes even at significantly higher wages, meaning Nike will sell less shoes at lower profits.

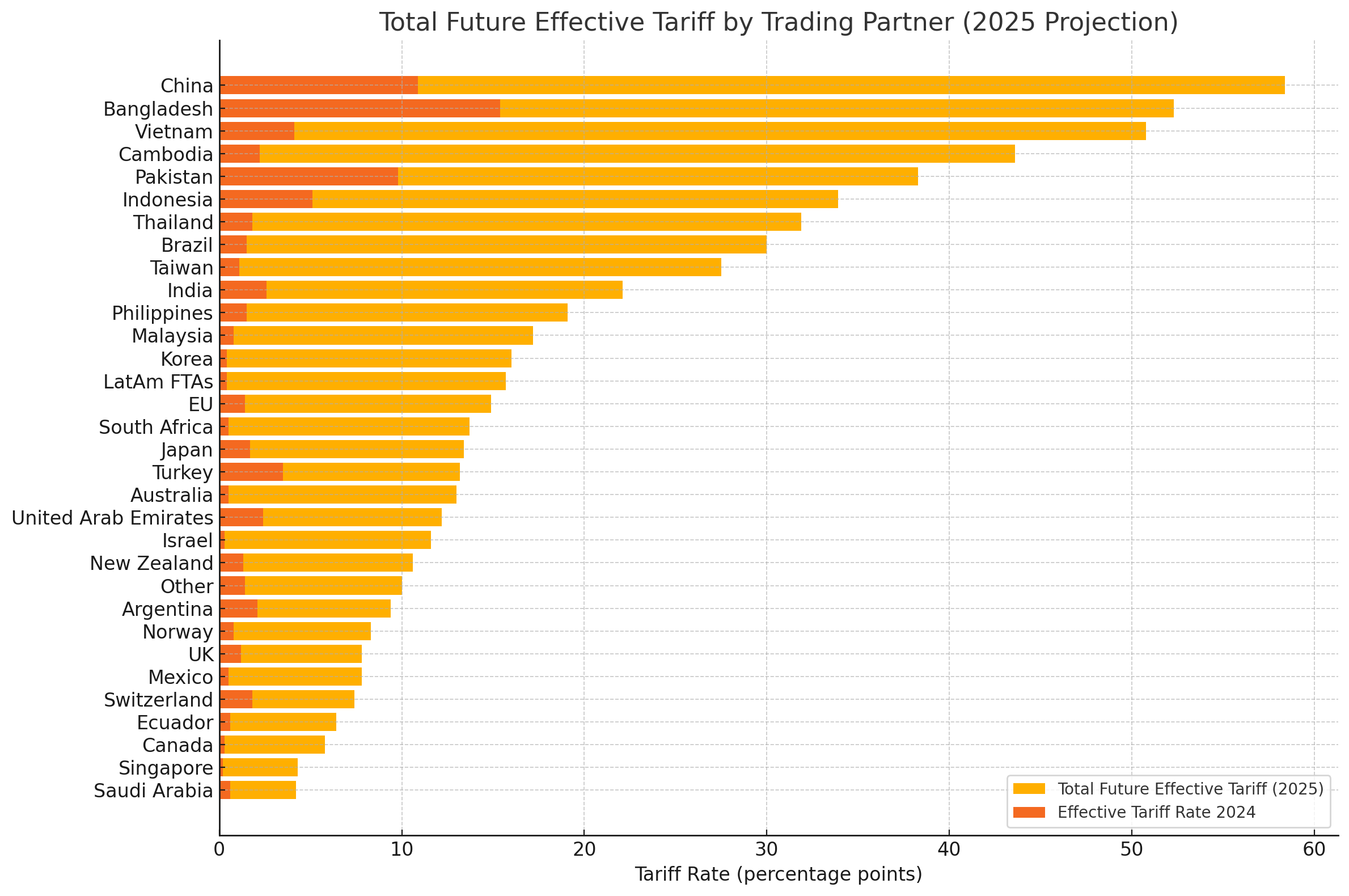

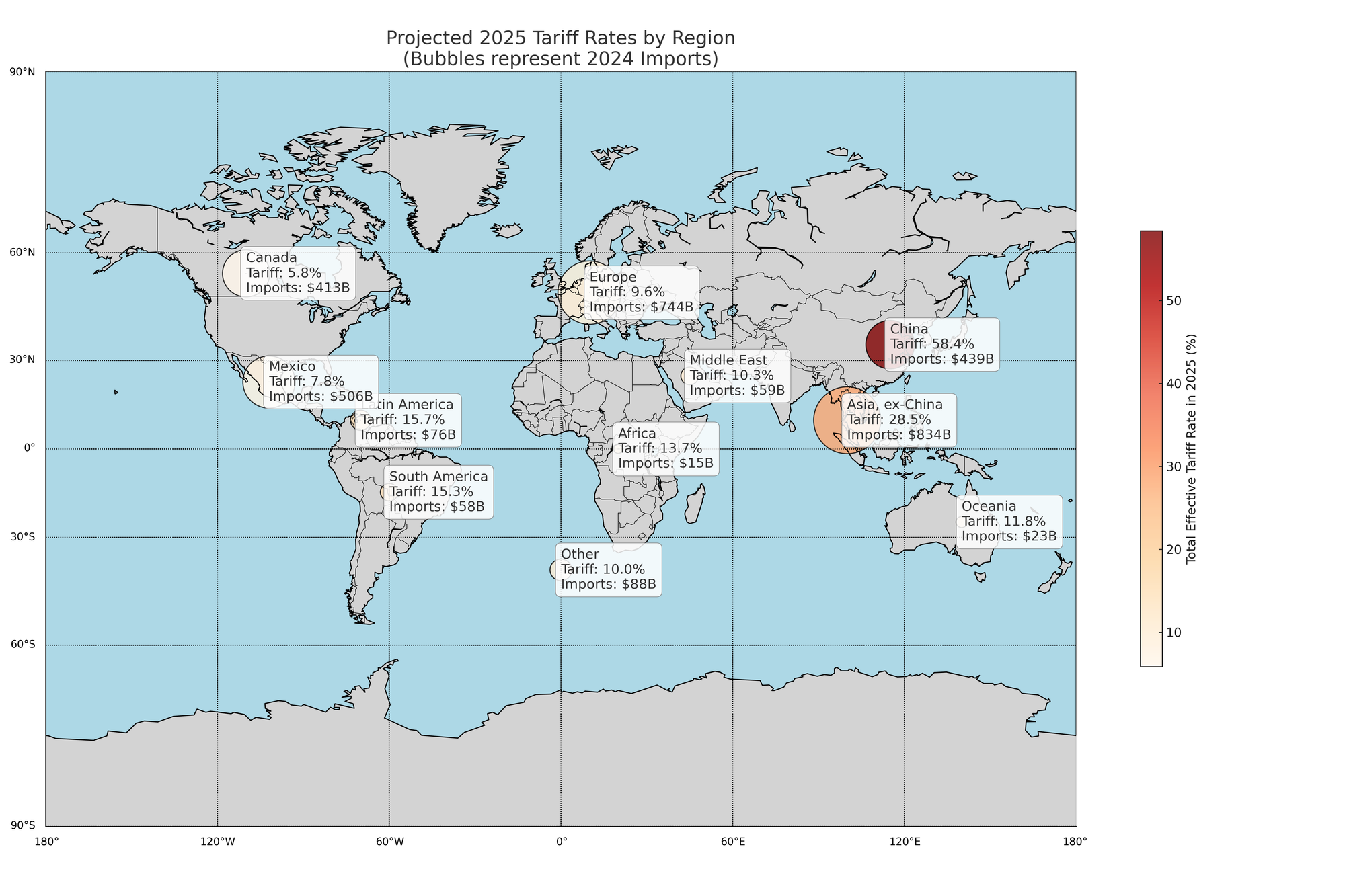

- The tariff on China is now an eye-popping 60% with 34% of that coming from the new "reciprocal" policy (matching the tariffs they charge on US goods)

- Despite an announced reciprocal tariff of 20% on the EU, the overall EU tariff rate jumped 13.5% to a new effective rate of 15% (due to exclusions listed below)

- No end game is apparent – the stated goal is to make for a more competitive landscape and equal treatment, but what that means in reality is anybody's guess.

- There were no new reciprocal tariffs for Canada & Mexico, but the "fentanyl/immigration" tariffs remain

- Will take years to see if this is successful

That last point is key. These are LONG-TERM problems which will take a long-time to fix and evaluate.-The economy was already slowing and inflation has been increasing ahead of this announcement. Short-term that is likely to accelerate as these new policies are implemented.

There was some 'good' news in the announcement:

- These rates were called a 'ceiling', which implies there is room for negotiation

- Did not change Canada/Mexico policy already implemented, which included exemptions for a long list of the USMCA compliant goods (the revised "NAFTA" agreement President Trump negotiated during his first term).

- The administration left the exemption for chips from Taiwan & pharmaceuticals from Europe (which is why the effective EU rate did not move up ass much as other countries)

- Small shipments from China (less than $800) remain exempt – if this didn't happen it would crush many of the small businesses who sell goods from China on sites such as Amazon.com.

It is far too early to know what the impact will be on the markets. This map shows the disparity

- (Thursday night update) Digging deeper into the formula (or in this case, seeing dozens of economists calling out the administration on the formula), it actually does not come down to tariffs imposed, trade barriers, currency manipulation, and other barriers, but simply, our trade deficit as a percentage divided by 2 (plus the 10% baseline in some cases). Here's a breakdown of the math for those who care..

For the latest on the market action and how SEM's models have reacted, check out the Traders Blog from Monday, April 7:

In the article above, I touched on the driver of economic growth – how many people are working and how much they are producing. Running budget deficits and trade deficits REDUCES potential growth which makes it harder to put more people to work and/or make them more productive. It's a downhill spiral.

Putting politics aside and ignoring the implementation of these policies, SOMETHING has to be done by SOMEBODY to address this. Here is a short video I created discussing how I would message the American people if I were trying to address the dual deficits which are hurting our long-term growth:

As of this writing (Thursday, April 3 at noon ET), several of our systems are close to taking risk off the table. It is too close to call. Either this is a buying opportunity (short-term dip) or we could see the selling accelerate over the coming weeks/months. We will let the DATA make that determination, which is critical during times like this.

Rather than waiting for this to resolve, we're going to post the newsletter now and encourage anybody wanting more frequent updates to check back in to the blog each Monday for additional updates.

You can also click here to Subscribe to our weekly blog newsletter.

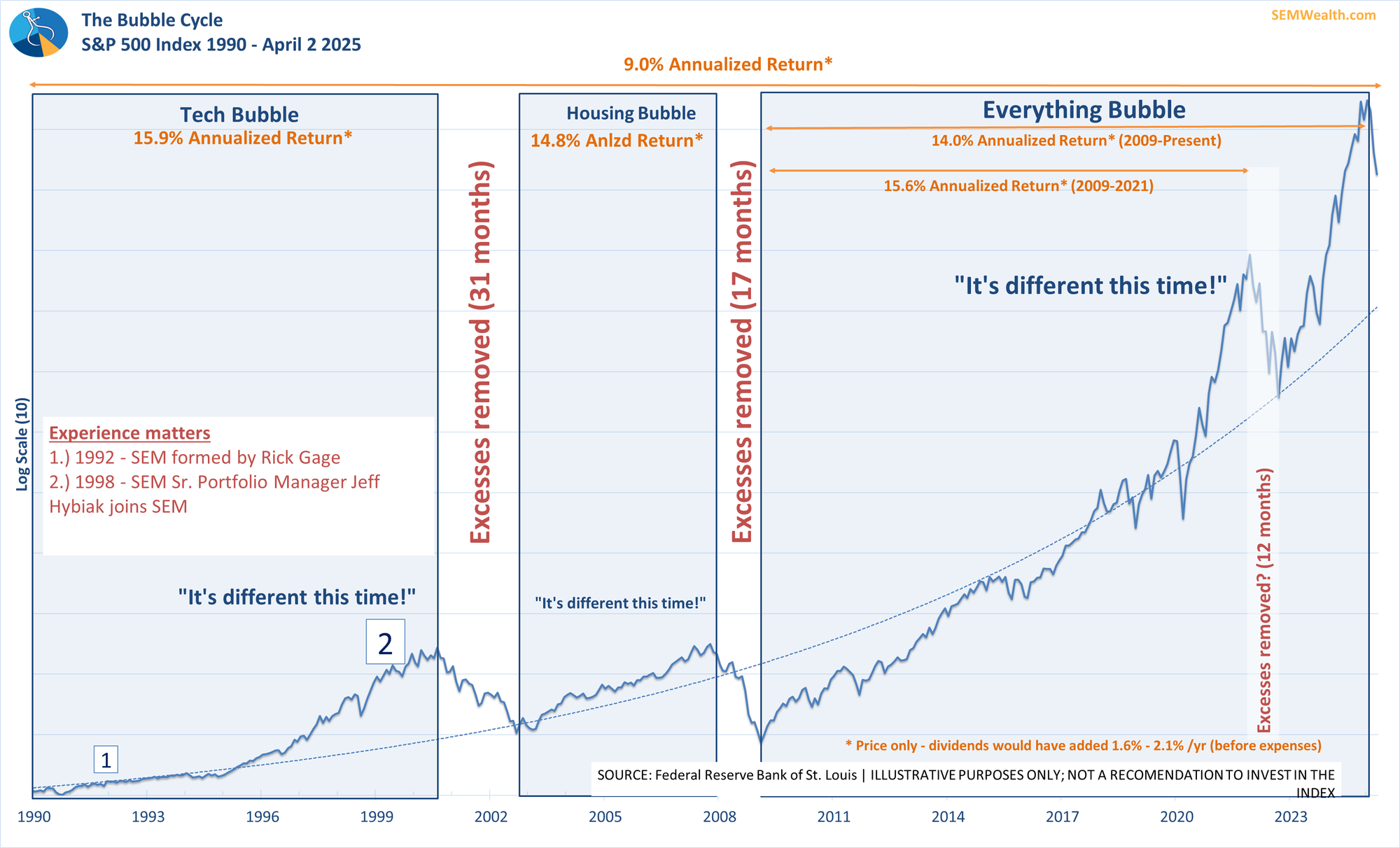

"It's Different this Time"

During a market bubble we often hear arguments about how the current situation is "different this time". The most recent "difference" has been via the "AI revolution". [More on that below]. After the announcement of the "Liberation Day" tariff policies, we've heard from several clients who said something along the lines of "it's different this time". Unlike a market bubble, their concern is that in our lifetimes we've never seen anything like the level of tariffs we are facing. We've never lived through a protectionist government. What we have lived through is "scary" drops in the market due to "unprecedented" events.

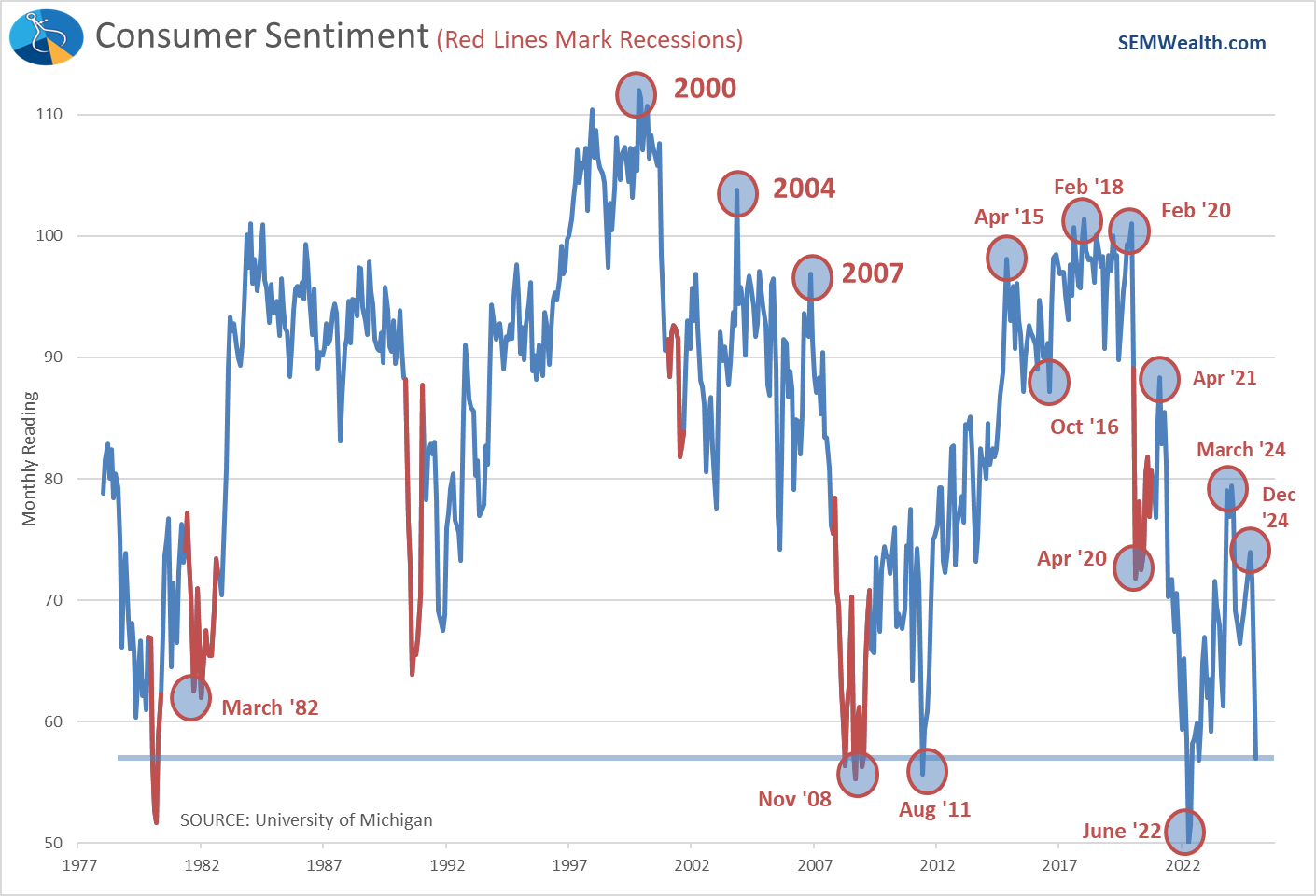

We show the chart below frequently because it helps put things in perspective. I heard a host today on one of the financial news programs say, "(Guest name) I'd like to hear from you because you've been around the markets since the mid-90s and you've seen a lot. The fact that you're still here says something." This is something we point out a lot — Since our founding in 1992 we've seen a lot of investment managers come and go. There is a select group which has been around as long as SEM and while that longevity does not by itself mean we won't make mistakes or are considered better than others, it does tell you one thing — we've seen a lot of different markets and had to adapt to the latest "it's different this time" environment in order to survive.

While the REASON behind the latest sell-off might be "different", the core driver of market fluctuations has remained the same – natural human behavior. Our models are designed to track the behavior behind the market, not the reason for the behavior. This allows us to have a sense of calm when we have big down days (or weeks) because we have a well-tested, robust plan to navigate a "different" environment.

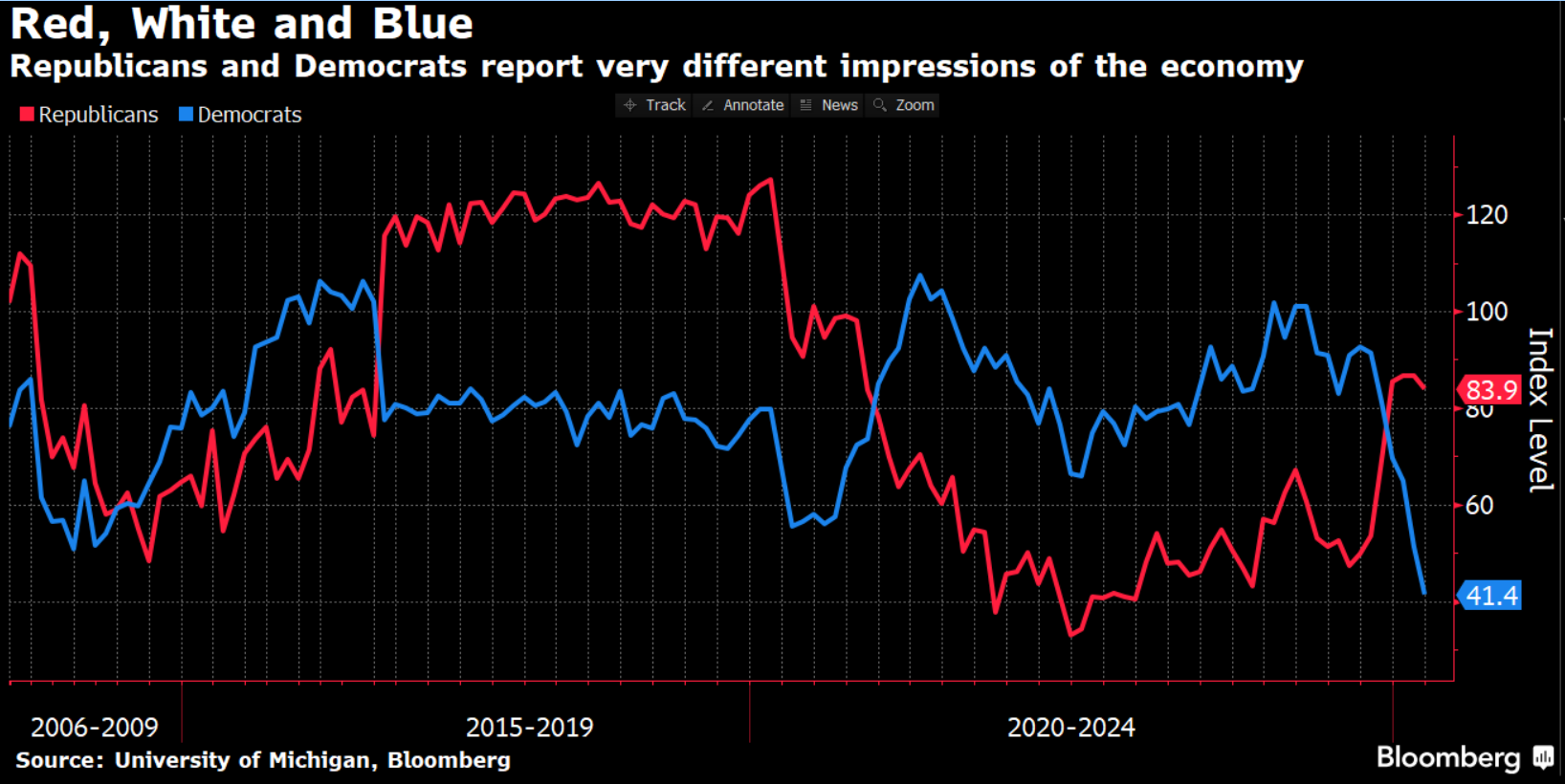

A Politically Divided Economy

How bad is the economy? That apparently depends on which political party you're affiliated with. Historically, this has always been the case – people generally believe their party is a better steward than the opposite party, but it is not always this divided.

Based on the latest polls, about 30% of Americans are Republican and 30% are Democrats, leaving the other 40% as registered Independents. So while Republicans may believe the economy is the best we've had since just before COVID hit and Democrats believe it's the worst we've had in 20 years, the overall sentiment number is approaching the lows of 2022 when inflation was nearly at its worst.

While everyone is entitled to their opinion on the economic outlook, it is important to follow our primary piece of advice on investing: "do not let your political opinions influence your investment decisions". History and experience tells us our economy is far too complex to allow one person, one president, one Congress, or one party to completely change the direction immediately.

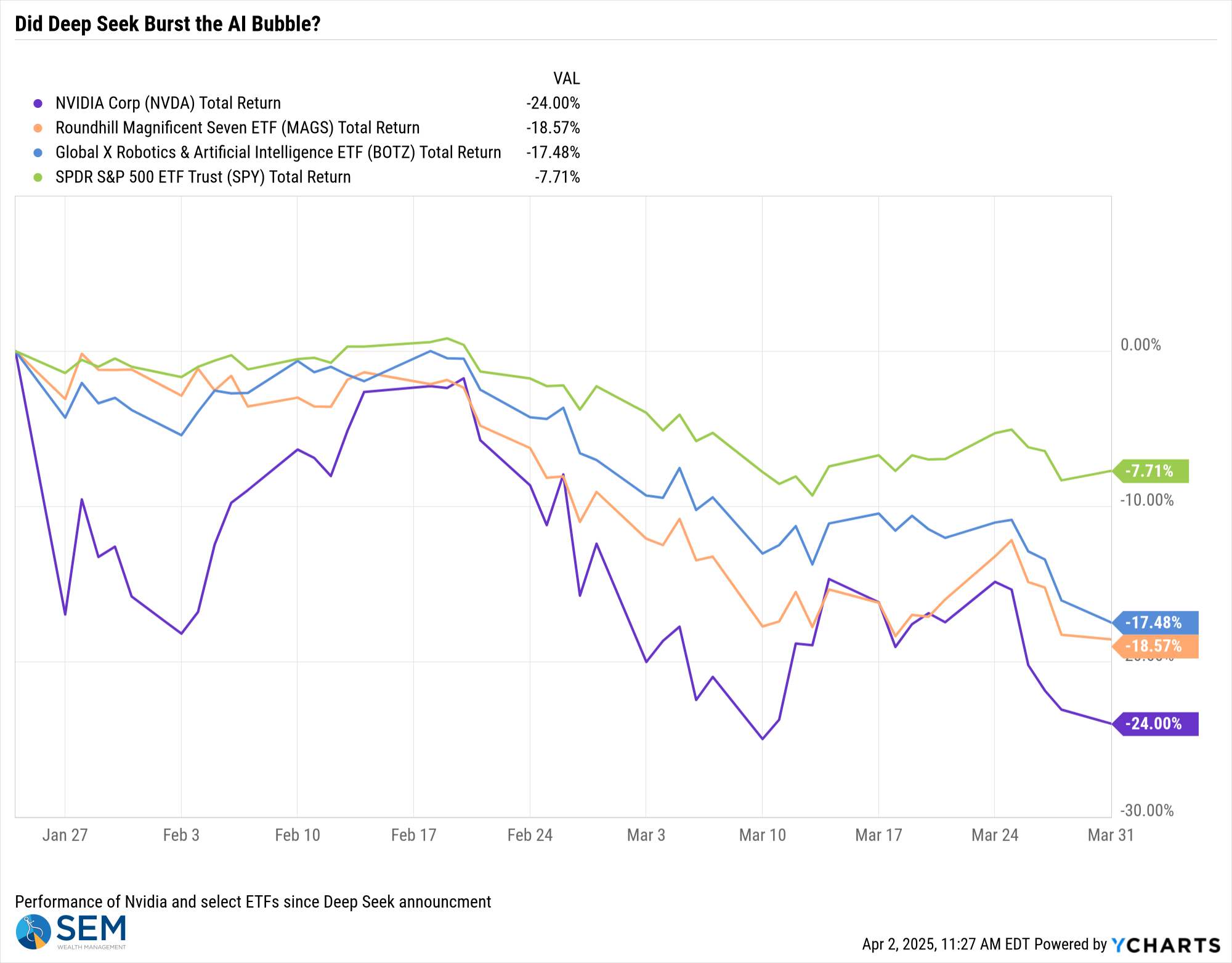

Did Deep Seek burst the AI Bubble?

On Monday January 27 it was reported Chinese AI start-up Deep Seek surpassed Chat GPT as the top downloaded app in both the Apple and Google app stores. Deep Seek allegedly was developed at a fraction of the cost of Chat GPT and other AI software, using low end processors and computers. It also was said to be just as fast and efficient, if not more so than Chat GPT. This of course called into question the hundreds of billions of dollars being poured into AI development (and the companies thought to be best positioned to profit from it.)

We won't know until we have the benefit of hindsight, but this could be the thing which ultimately bursts the AI bubble. A look at AI darling Nvidia's stock since then along with the top AI ETF, the Magnificent 7 ETF, and the S&P 500 shows severe losses since that announcement (we do need to keep in mind Trump's Trade War started heating up in mid-February so some of the sell-off could be related to this.)

In our last newsletter we included a link to a blog article I wrote discussing finding the next "big" AI stock and comparing the current environment to the end of the tech bubble. You can view that article here:

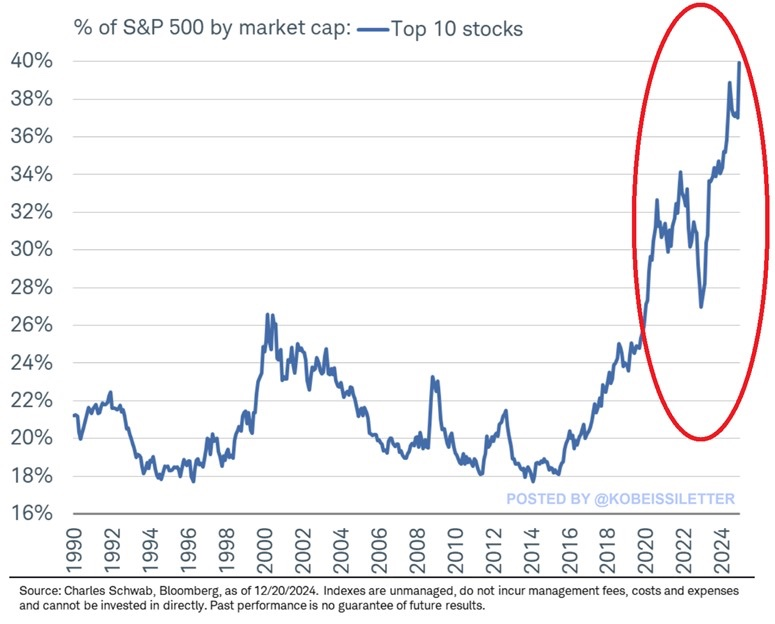

We also showed this chart in the last newsletter, which highlighted how 'narrow' the S&P 500 had become due to the strong performance of the so-called "magnificent 7".

Again, it is too soon to tell whether or not the bubble has burst on AI-related stocks, but regardless this is a good example of the dangers of being invested too heavily in just a handful of stocks.

Money Talks with Dad: Financial Literacy for 'normal' people

Seven months ago we started a financial literacy monthly podcast/vlog to help take complex topics and explain them for normal people. Last week we posted our 8th episode. We encourage you to share it with any friends and family who could use some help getting their finances in order or who are just starting off in their money journey. Check it out below and make sure you subscribe to get notified of the latest updates.

Don't be a victim

We continue to see an increase in both the number of scam attempts and the level of sophistication of these scams. We urge everybody to be extremely cautious when you receive an email or text message regarding an account or bill. It is always best to navigate straight to a financial firm's website to log in there.

As we've been doing the past few quarters, here is your reminder to review the Cyber Security Resources compiled by our Director of Technology, Dustin Briles:

Download/Print version of the Newsletter

What is ENCORE?

ENCORE is a Quarterly Newsletter provided by SEM Wealth Management. ENCORE stands for: Engineered, Non-Correlated, Optimized & Risk Efficient. By utilizing these elements in our management style, SEM’s goal is to provide risk management and capital appreciation for our clients. Each issue of ENCORE will provide insight into investments and how we managed money.

The information provided is for informational purposes only and should not be considered investment advice. Information gathered from third party sources are believed to be reliable, but whose accuracy we do not guarantee. Past performance is no guarantee of future results. Please see the individual Model Factsheets for more information. There is potential for loss as well as gain in security investments of any type, including those managed by SEM. SEM’s firm brochure (ADV part 2) is available upon request and must be delivered prior to entering into an advisory agreement.