I was chatting with a trader I’ve known since 1999 about the crazy reaction to the election of Donald Trump. He pointed out something most people have missed in the noise following the election:

“You could have called the election right and lost a ton of money. Those that called the election wrong probably made their year in 3 days.”

Think about the attitude before the election. Nearly every expert was predicting a crash of 3-20% should Donald Trump win the election. We heard hedge fund managers to billionaire investors taking significant short positions in stocks and loading up on Treasury Bonds to prepare for that scenario. On the other hand, experts predicted a Hillary Clinton victory would lead to a “risk-on” trade that would lead to a massive “short-covering” rally in stocks and a strong rally into the end of the year. Treasuries under that scenario would get hit as it would lead to a move out of the “risk-off” trade and also create the likelihood of a Fed rate hike in December.

[Click here for my assessment of what the Donald Trump victory could mean over the longer-term.]

Thus far the S&P 500 is up 1.5% since election day. That would lead many to believe the rally was widespread, but that is simply not the case. The two best performing asset classes before the election, Technology & Emerging Markets have lost money since election day. The NASDAQ losses have been tame (0.1%), but Emerging Markets have been crushed (down 7.2%).

Even more shocking, however is the drop in bond prices. The Aggregate Bond Index has lost 1.8% since election day. That is mild compared to the Long-term Treasury Index, which is down 6.5% since Tuesday. (That is not a typo!) Keep in mind the bond market was closed on Friday for Veteran’s Day.

Personally, my opinion is the reaction to the election is more a result of the “surprise” and too many traders being caught off guard. As I mentioned in my post-election re-cap, Donald Trump needs LOWER interest rates to make his plans work and the run-up in rates is bad news for his policies (as well as the overall economy which sadly will be how voters begin to grade his performance as president despite the fact the groundwork was already in place for a recession in the next 12-18 months regardless of who won.)

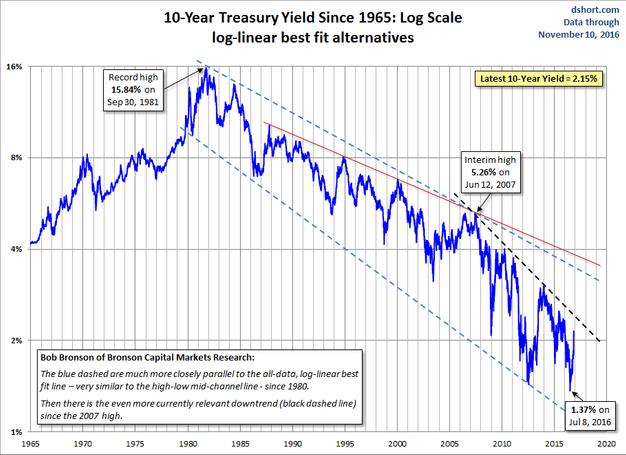

As far as interest rates go, I’m not sure when they stop rising. This chart from Advisor Perspectives highlights the 10 Year Treasury Yield from a longer-term perspective.

We are approaching some significant downtrend lines in rates. A break above 2.25% could bring a move into the mid 3% range over the coming months. This chart also shows that in the grand scheme of things interest rates are still relatively low and could produce some growth. I think the greater concern is the panic that could ensue given the size of the government bond market and how many investors had money there thinking it was “low risk.”

Our trading systems are also of the opinion this rally in the stock market could be short-lived. Our Price Divergence System, which sold a bit before the election went to a Bearish signal for the first time since 2014 just as QE 3 was ending. It did not like the fact the S&P 500 has approached the upper end of the trading band while the Advance/Decline line is not moving at the same rate (futures buying versus stock INVESTING occurring on this move.) The signals generated last week are rare, but have a 60-80% winning percentage historically and often generate drops in the market of 7-15% before the next reversing buy signal. Keep in mind in many cases these signals may be a few days or few weeks early. Most of our bond systems have retreated to the safety of cash or money market as well.

I think the biggest issue is the unrest going on across our country. Last night I again heard a subdued President-elect Trump trying to back away from the persona given out by Candidate Trump. I think the Republicans that voted for him hoping for a far right Republican platform forget that he defeated all of their preferred candidates by being the “change” candidate. He is far more likely to be a “moderate” President than the far right extremist so many Democrats fear.

Despite again backing away from some controversial plans, I was disappointed to see nearly every “news” website I visited last night and this morning was only trying to create more dissension in our country. Whether it was digging up dirt from 1993, talking about “deals” gone bad, reminding readers about the accusations of sexual misconduct, or simply highlighting things he said on the campaign trail (usually taken out of context), the media is not trying to bridge the gaps between the two sides, but rather make them wider. We do have to keep in mind the ratings go up and the number of hits to their websites jump if there are daily riots in cities across the country. If we were to actually have adult conversations about the issues, who would tune into their sensationalized “news” channels? If the leaders of the Democratic Party do not stand up and denounce these “protests”, things could escalate quickly and make it impossible for President-elect Trump to accomplish anything. As I tell my kids, “words vs. actions”. If Hillary Clinton & President Obama TRULY want to see things transition smoothly they can help do this.

Looking across our programs, given the sharp, strange movements we have seen the past two weeks, I am pleased with the reaction. They were by no means perfect, but I do not know a MECHANICAL system that could have handled these types of moves. If some investors/traders guessed right, good for them, but I do not expect them to guess right every time, which means significant losses would lie ahead. As mentioned in the outset, the person that got the election call WRONG made a ton of money. The one that got it RIGHT lost a ton of money.

The most important programs to highlight are our Income Programs as that represents the vast majority of our assets. Tactical Bond, Income Allocator, & Dynamic Income were down just 0.3 to 0.4% since the election. Losses are not ever fun, but they are also not preventable every time. Remember, the Aggregate Bond Index (total market bond index) was down nearly 2% and Long-term Treasuries down over 6%. All 3 are now even more conservatively invested and will wait patiently for opportunities to emerge (and they will emerge again……they always do.)

EGA & EPA were caught too defensive and also invested in the wrong sectors (remember the sectors that got crushed following Trump’s victory were the BEST performing sectors BEFORE the election). Despite this, both were down just around a third of a percent since the election. Both are now HIGHLY DEFENSIVE, meaning if chaos breaks loose, those clients will be protected.

Most importantly, in my opinion, our Dynamic Aggressive Growth program did its job of providing CONSISTENT EXPOSURE to stocks, but also LOWER RISK exposure. While it did not quite generate the 1.5% since election day performance of the S&P (it was up 0.9%), it is still ahead of its benchmark. It remains in a “neutral” position, with a slight bearish leaning. Should things unravel, this program should lose less than the overall market.

Right now there seems to be more questions than answers, which makes me glad we have well-tested, diversified, mechanical trading systems inside our investment programs. Anybody that tells you they know what happens next will be lying.

Tuesday, November 15

The strange reaction to Donald Trump’s election continued on Monday. Small cap stocks & banks celebrated. Technology stocks sold off again. The S&P 500 was flat. Emerging markets plummeted. Most concerning is the route in bond prices, which saw the 10 Year Treasury Yield hit 2.3% intra-day before backing down to 2.24%. Thus far this morning the nearly straight up move in interest rates has abated.

I would be extremely cautious making any sort of decision on your investments at this point. What I’ve seen so far from President-elect Trump is nobody knows for sure what portions of his campaign platform he will actually pursue. Based on that we then have to wonder how much support he will receive from Congress.

Wednesday, November 16

Even the weak sectors rallied on Tuesday as the Trump rally continued. This morning a touch of reality has set in as the 2nd Fed member in 2 days (Rosenberg yesterday & Bullard today) hinted the Fed is very likely to raise rates in December. While I still have questions on President-elect Trump’s ability to actually push his policies through, if they do make it through they are going to be highly inflationary and most likely do significant damage to the deficit (at least over the short-term). The long-term impact on economic growth will depend on how much the tax cuts, slashing of regulations, and infrastructure spending actually improves the productivity and size of the labor force.

It is still far too early to make investments based on the predicted government policy. Doing so is simply speculation & if wrong could do significant damage to a portfolio. Our systems are erring on the side of caution right now, waiting for more clarity. To me that is the prudent thing to do and I’m pleased with how our individual trading systems and programs have handled the pre & post election markets. “Defense First” is always our mantra. That has paid off well for us and our clients the past 25 years.

Thursday, November 17

Stocks took a breather on Wednesday, but appear ready to rally again. The highlight of the day today is likely going to be Janet Yellen’s testimony in front of the Congressional Joint Economic Committee. We are certain to hear questions regarding the plans for the December meeting as well as her thoughts on the economic impact of a Trump presidency.

The markets are already pricing in an almost 100% certainty the Fed will hike rates. I guess we could take the fact they have rallied at the same time this probability has increased as a good sign.

i would still urge caution as we wait for more clear signs on what actually may be accomplished when the new president is sworn in.

Friday, November 18

Surprisingly the markets were able to shake off Fed Chair Janet Yellen’s testimony on Thursday when she hinted a rate hike is “probably warranted. The focus remains on the prospects of the Republicans running the government with visions of Ronald Reagan dancing through their head. Even Chair Yellen reminded Congress it could take significant time for any of Trump’s proposals to even be approved. She also told Congress the financial regulations put in place following the financial crisis have strengthened the financial system and warned about Donald Trump’s campaign promise to repeal them.

I will again remind our leaders to be cautious making investment decisions based on what they believe the outcome of the next government will be. Goldman Sachs also struck a cautious tone in their outlook on the expected fiscal impact of the economy. Before jumping into the market, take a look at their research.

Ned Davis also provided some interesting research to their subscribers on the “bullishness” of an all-Republican government. Much to the surprise of many people, the results have been mixed. Going back to 1901 the Dow has been up just 4 times out of 13 three months later & only 8 out of 13 a year later. The data shows big gains at times, but also big losses.

As we move forward the direction will be more clear. Until then our programs remain cautious.