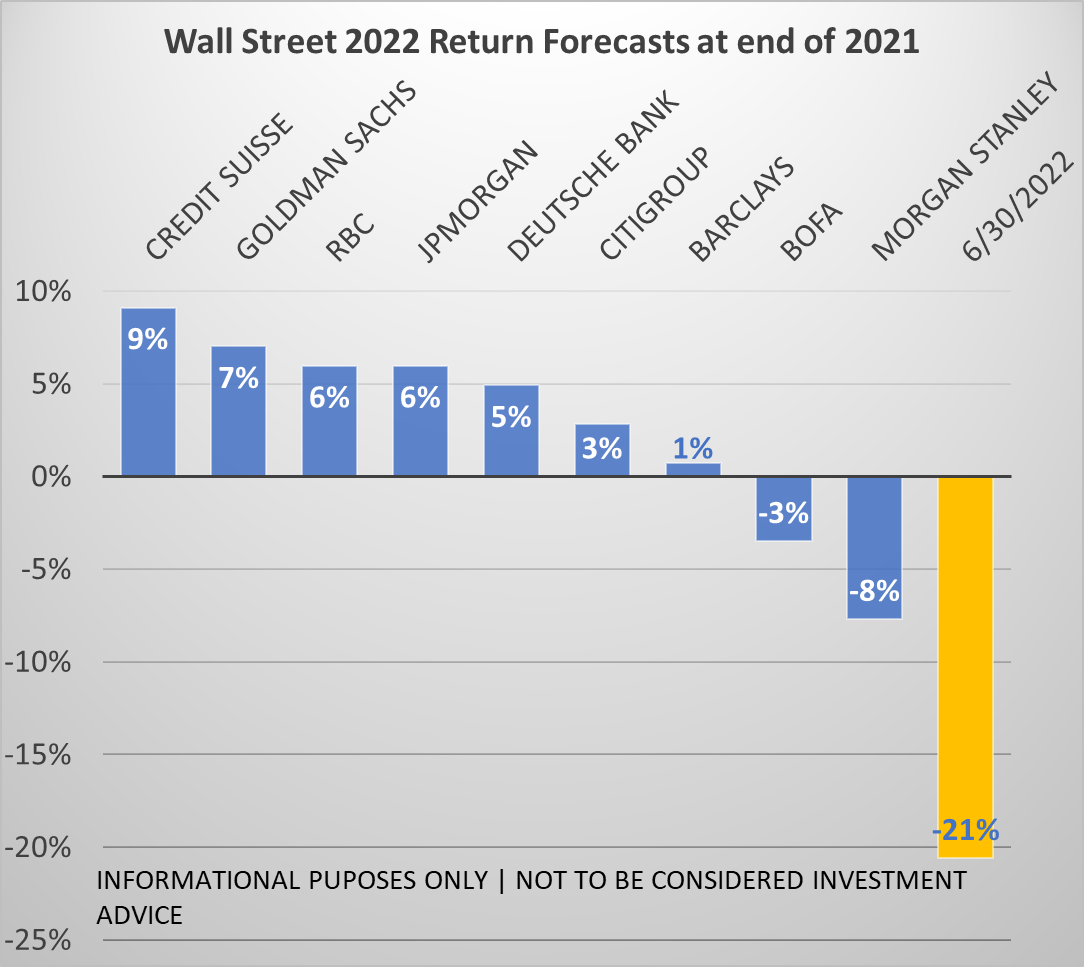

Worst start since 1970

After stocks posted a strong performance in 2021, the Wall Street experts warned investors to temper their expectations. The rosiest predictions had stocks posting only an average return around 7-9%. Surprisingly two firms actually predicted stocks would fall a bit. All firms were worried about the Fed raising interest rates to fight inflation, but they also all predicted continued strength in the economy and corporate earnings. At SEM, we were more blunt in our outlook to start the year, highlighting how all of the “pillars” that pushed stocks higher since the COVID panic were now gone and we’d have to see if the economy and markets could stand on their own.

With inflation running hotter than expected, the Fed has been forced to hike rates aggressively. Consumer Sentiment is at record lows. The economy is slowing rapidly. Profit margins are being squeezed. All of these things have led to a sharp drop in stocks and bonds. Is more pain to come, or is this a temporary bump? Time will tell.

What should we expect in the 2nd half?

Investors have been conditioned to “buy the dip”. Since over the long-term stocks tend to rise at an average rate of 7-9% per year, buying any “dip” eventually pays off. Of course, the experts tell us to always stay invested, which means you wouldn’t have any cash on the sidelines to buy the dip anyway. With stocks dropping so far, so fast in 2022, there are no shortages of predictions for what the second half will look like.

At SEM we rely only on the data, not our opinions. We have, however been around for over 30 years so we have seen all kinds of market environments. Here are some things we should expect the second half of the year:

1. One or more strong rallies. The 2007-2008 bear market had 5 rallies of 8 to 22%. The 2000-2002 bear market included 7 rallies of 8 to 22% before the worst was over.

2. More negative economic data. Right now consumer spending has remained strong as “revenge vacations” take place despite high inflation. Backing out travel related spending, indications are consumers are cutting spending fairly significantly which will show up in the data later this year. This means we are likely already in a recession or heading towards one before the year end.

3. Predictions that the "worst is over. We’ve already seen this several times in 2022. Every time there is a rally Wall Street experts will declare the worst being over. As illustrated at the top of the page, they can be very wrong. Just because the data is “less bad” does not mean we’ve hit the bottom.

4. Political wrangling. Mid-term elections are in full swing. With both sides blaming the other for runaway inflation and the economic pain it is creating, we should expect many big “ideas” to be floated that could move markets. Campaign promises rarely come to fruition, so tread carefully.

5. Stocks (and/or bonds) could "bottom". At some point, stock valuations become attractive. At the end of the quarter, the P/E ratio had returned to it’s 20-year median level. Bear markets typically see the P/E ratio go well below the median, so if stocks keep dropping we may hit the final bottom. The same can be said for bonds. Who knows. As we said, we rely on the data, not our opinions (or others) to make market adjustments. They will bottom and when they do we will have cash ready to be put to work.

In case you missed it, please watch/read our Bear Market Tips:

Working according to plan

The first half of 2022 has proven once again the value of a disciplined, quantitatively based plan in the midst of uncertainty. For over 30 years, SEM has been calmly handling all sorts of different sources of uncertainty. We thought it would be helpful to walk through the recent moves SEM took to reduce the risk in our clients’ investment accounts:

- October 1: SEM’s economic model moves from "bullish" to "neutral". Dynamic Income Allocation (DIA) along with Cornerstone-Income sells half of dividend stock exposure. Dynamic Aggressive Growth (DAG)sells half of small cap exposure. Bonds are added in place of these positions. This model issued a bearish signal on April 1, 2022, eliminating small cap (DAG) and dividend stocks (DIA)

- January 3: AmeriGuard & Cornerstone Balanced & Growth core positions eliminate small cap growth and added Large Cap Value.

- January 10: First sell signal in High Yield Bond system, reducing exposure by 1/4 in Tactical Bond (TB).

- January 19: Second sell signal in High Yield Bonds, reducing exposure in TB, Tax Advantaged Bond (TAB), and Income Allocator (INA).

- January 24: Third and fourth (final) sell signals in High Yield Bonds, reducing exposure in TB, INA, and Cornerstone-Bond (CS-BND). This put TB & CS-BND in full "risk-off" positions.

- January 31: INA sells last high yield bond position, placing this model fully in "risk-off" mode.

- February 22 (two days before Russia invaded Ukraine): First trend indicator triggers in AmeriGuard & Cornerstone Balanced & Growth models, cutting stock exposure to half of the target range (Balanced now at 50% stock, Growth at 85%).

- March 7: Second trend indicator triggers in AmeriGuard & Cornerstone Balanced & Growth models, cutting exposure to minimum of the target range (Balanced now at 30%, Growth at 70%).

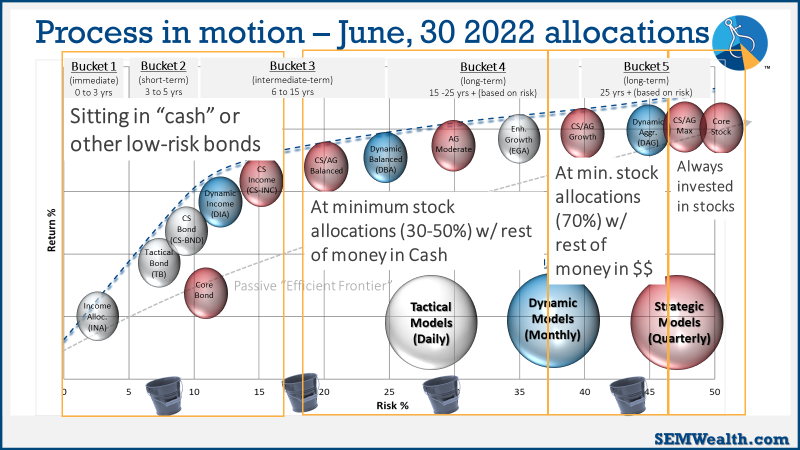

We did endure some losses in our bond models in early June. Our high yield bond system received a buy signal at the end of May only to have the upside momentum reversed a week and a half later. We took some small losses, but that will happen at times. The key is we didn’t guess this was a bottom and when the market reversed we moved back to the sidelines. The chart to the right shows how each model is positioned currently.

While each of our investment models are designed to stand on their own, the real value comes when we combine multiple models into one investment portfolio. This allows the longer-term bucket to stay invested longer and the shorter-term bucket to focus more on managing risk. The allocation to each management style and investment model is determined by the financial plan, cash flow strategy, investment objectives, risk tolerance, and investment personality of each individual. If you would like a review of your portfolio go to risk.semwealth.com

Download / Print version of the newsletter

What is ENCORE?

ENCORE is a Quarterly Newsletter provided by SEM Wealth Management. ENCORE stands for: Engineered, Non-Correlated, Optimized & Risk Efficient. By utilizing these elements in our management style, SEM’s goal is to provide risk management and capital appreciation for our clients. Each issue of ENCORE will provide insight into investments and how we managed money.

The information provided is for informational purposes only and should not be considered investment advice. Information gathered from third party sources are believed to be reliable, but whose accuracy we do not guarantee. Past performance is no guarantee of future results. Please see the individual Model Factsheets for more information. There is potential for loss as well as gain in security investments of any type, including those managed by SEM. SEM’s firm brochure (ADV part 2) is available upon request and must be delivered prior to entering into an advisory agreement.