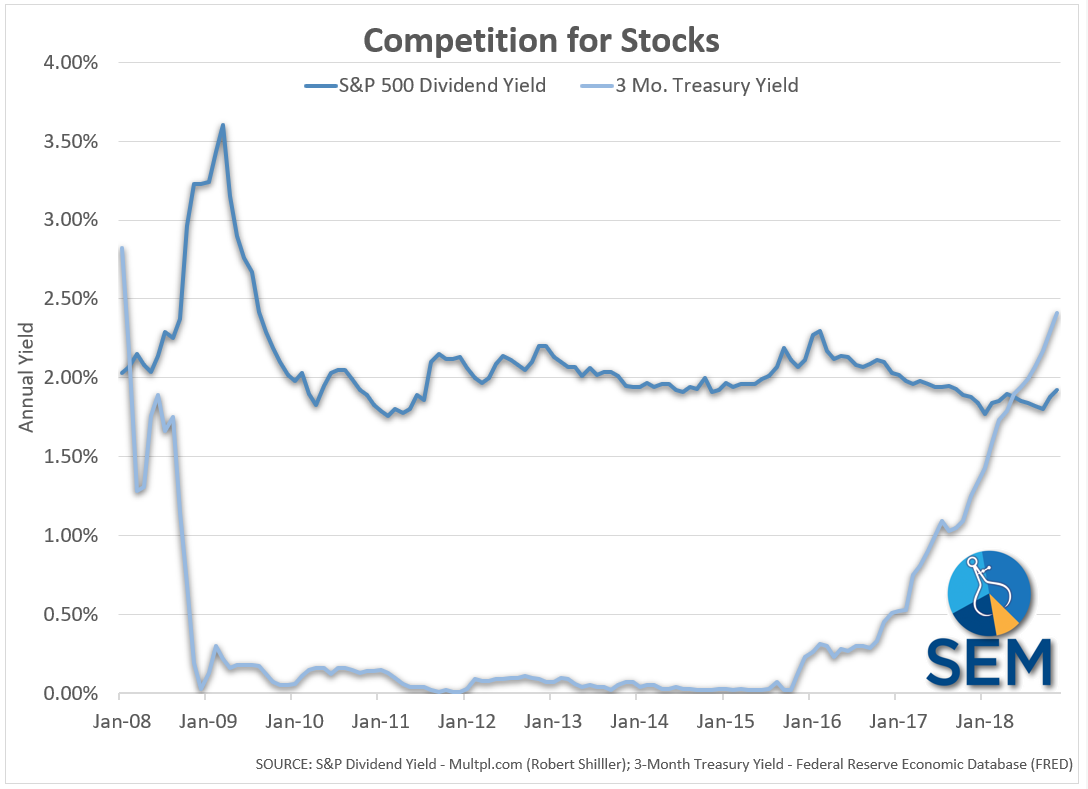

For the past 12 years I’ve heard market cheerleaders compare the dividend yield on the S&P 500 to Treasury Bond yields. The argument was simple…….why would you invest in such low yielding instruments when you could get this “nice” yield by owning stocks. With the Fed gradually raising interest rates the past few years few people have noticed the erosion of this relationship. As of this week you could earn 2.4% annually by purchasing 3-month Treasury Bills or you could receive a 1.9% worth of dividends by purchasing an S&P 500 index fund.

Now, those same bulls who argued about the attractiveness of stocks versus bonds the past 12 years will quickly point out the upside potential for stocks versus bonds. I agree with them — over the VERY long-term. However, after a 10 year rally in the stock market the chances are VERY high the S&P 500 will go through a steep decline (history tells us a 25 to 50% drop is well overdue). Those types of drops typically occur during a recession. You know what companies do with their dividends during a recession? They cut them. Despite dividend cuts, the dividend yield often spikes during a recessionary bear market because the prices of the stocks (the denominator in the dividend yield calculation) falls so quickly as can be shown on the left hand side of the Chart of the Week.

Conversely, unless we are heading towards complete Armageddon, at which point the only investment that matters is where you stand spiritually, it is difficult to foresee a situation where the US Government would fail to make the promised interest payments for lending them money. I’m not advocating owning Treasury Bonds for the long-term instead of stocks, but the fact you get MORE yield and significantly LESS risk is something weighing on asset managers the longer the bull market and economic expansion continues. The more people decide it is not worth the risk of owning stocks, the more stocks will be hurt. Eventually you get enough selling to spark a panic and a bear market drop of 25 to 50%.

For more information on the risks in dividend stocks see DIVERSIFIED LOSSES.

When that occurs is anyone’s guess. At SEM our daily monitored “tactical” investment models have already taken a significant amount of money off the table. For the first time in 12 years we are actually making a nice return when we do this. Each time the Fed raises interest rates we celebrate because our defensive positions make MORE money. Our monthly monitored “dynamic” models shifted to neutral last month as economic growth appears to be decelerating. The more interest rates go up, the more likely the economy will begin heading towards a recession. Our quarterly managed “AmeriGuard” models remain fully invested, but are ready should a recessionary bear market begin to take a large chunk of money off the table as well.

This is the beauty of SEM’s Behavioral Approach to Investing using our Scientifically Engineered Models. There is no guesswork or subjective comparisons between stock and bond yields. We let the data speak for itself and adjust our allocations accordingly.

How does SEM compare to traditional approaches? See ACADEMIC MISCONDUCT.

Please, please, please do not let the pundits lull you into a false sense of security. Risks are building rapidly for a decline in the market and dividends WILL not protect you. Having a plan to pro-actively take money out of the riskier assets is the only way to handle what could be an ugly couple of years.