All year we've been discussing the extremely optimistic growth outlook driving stock prices higher. Last week more economic data continued the euphoric hope that the Fed is in line to pull off a rare event – control inflation without causing a recession. The release of the first estimate of 4th quarter GDP showed much higher than expected growth rates. Included in the data was "softer" inflation data. It appears everything is perfect or to use another piece of Wall Street jargon, we are in a "Goldilocks" environment.

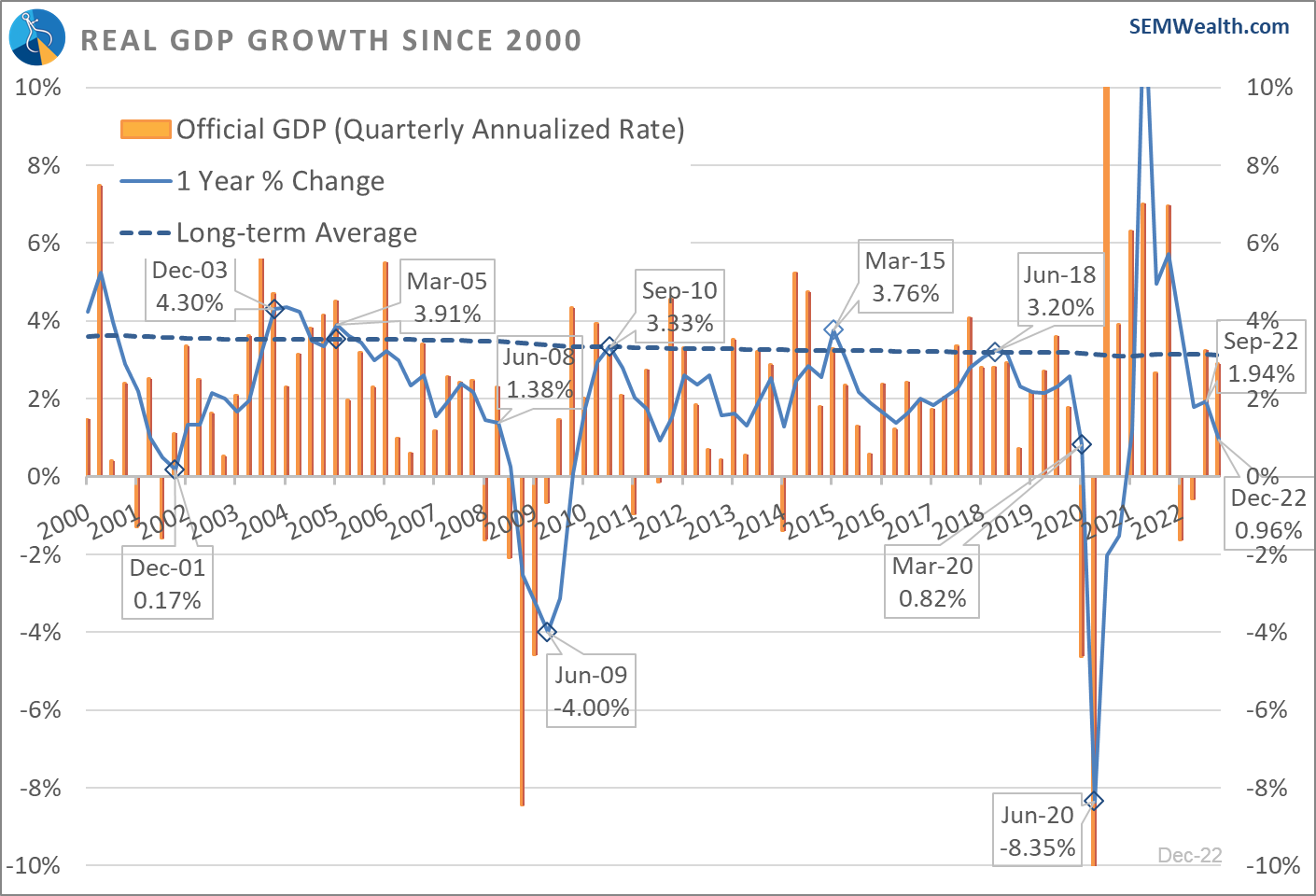

Looking at the charts and underlying data, I'm less impressed. First, the GDP release has again highlighted how misleading the way the government reports economic growth. Instead of looking at an annual growth rate, the GDP report annualizes the growth rate from the last three months. There are also seasonal factors used to further tweak the data. The problem with seasonal factors is rare events, such as 9/11, the global financial crisis, and the pandemic will skew those factors.

This chart illustrates the difference between the official (last 3 months essentially multiplied by 4) and the change over the past year. The "official" number for the 4th quarter was a surprising 2.9%. However, over the past year the economy grew just under 1%. A 1% or lower 1-year growth rate has only occurred this century when we were in a recession.

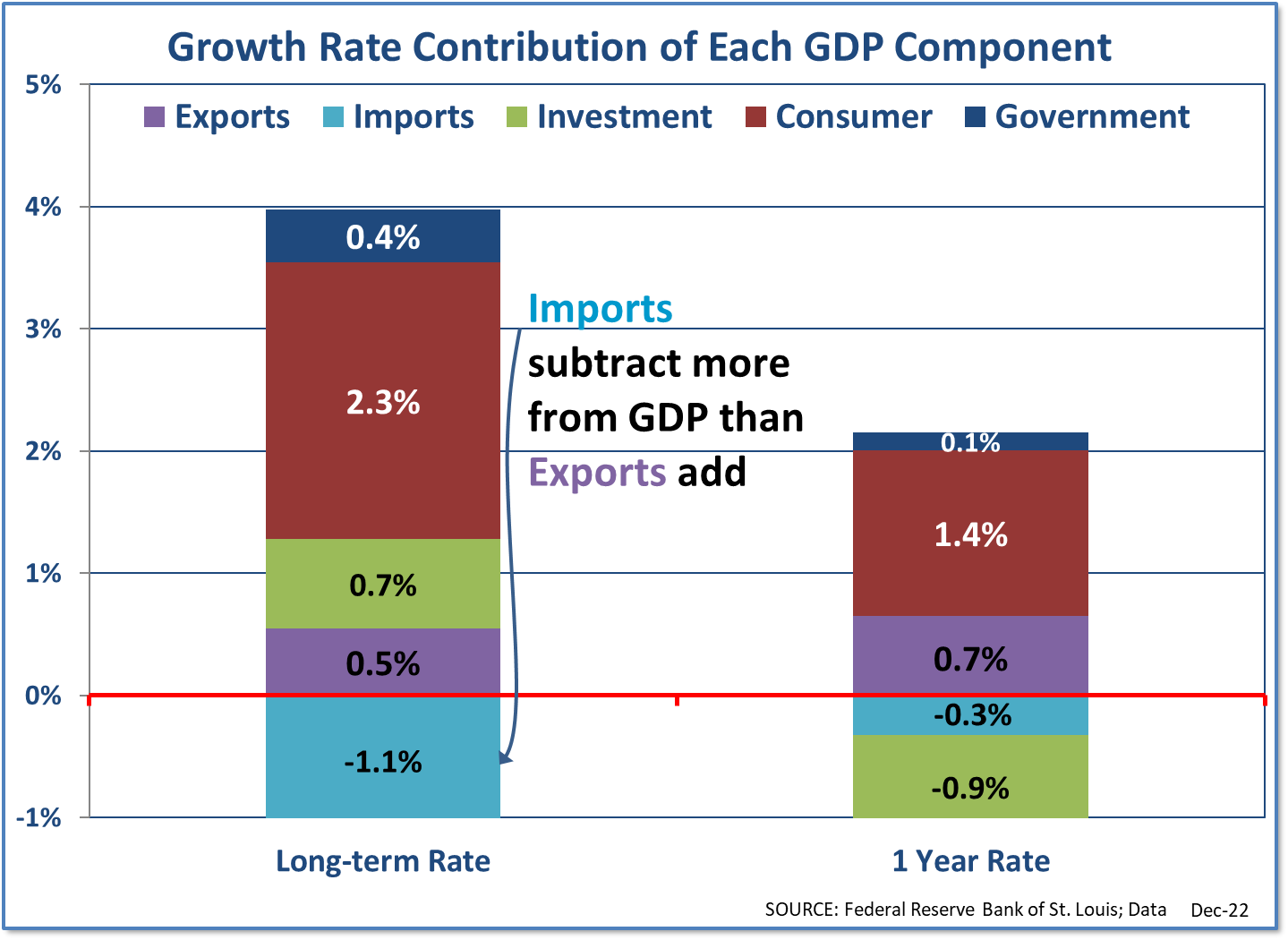

Even the 2.9% growth was not as strong as it sounds beneath the surface. Half of the growth was due to a surge in inventory. While in normal times that could be a sign of optimism at businesses, the pandemic fueled supply chain issues caused a disruption in normal inventory cycles. Businesses were finally able to sell inventory purchased over the previous two years during the last half of 2022. They were then forced to replace it. You can think of inventory purchases as borrowing from future growth. The longer it takes to sell the inventory the longer the drag will be.

Looking at the one-year numbers and their contribution to GDP there are a few glaring issues. The first and most damaging is the decline in private investment (the green box). We saw a surge in investment during COVID as the economy shifted due to in-person meeting and gathering restrictions. That was growth borrowed from the future (similar to the build-up to Y2K we discussed last week).

Also, while encouraging if this was a long-term trend, exports exceeded imports over the past year. For now this appears to be a function of Europe's economy doing relatively better than ours as well as a shift in their energy purchases from Russia to the US. (As a reminder, the US is a net EXPORTER of energy products – the problem is when you add the dollars we receive to the dollars we pay for energy we have a deficit. This is because the quality of US energy products is sub-standard relative to what we purchase from the middle east.)

Finally, and likely more importantly is the slowing growth in the consumer section. My hypothesis since late 2021 was after we saw "revenge travel" slowdown following the 2022 holidays we would see consumer spending slow. We are already seeing a surge in credit card usage and an uptick in delinquencies on both credit cards and auto loans. Those are typically very early signs of a stressed consumer.

All told, declining investment, a surge in inventory, and a slowing consumer still lines up with the liklihood we are going to see a recession this year (which is bad for stocks pricing in a 13% jump in corporate earnings.) I hope I'm wrong. I'd love to see the economy withstand this hit from the Fed and resume strong growth, but hope is not a strategy or something we base our decisions on.

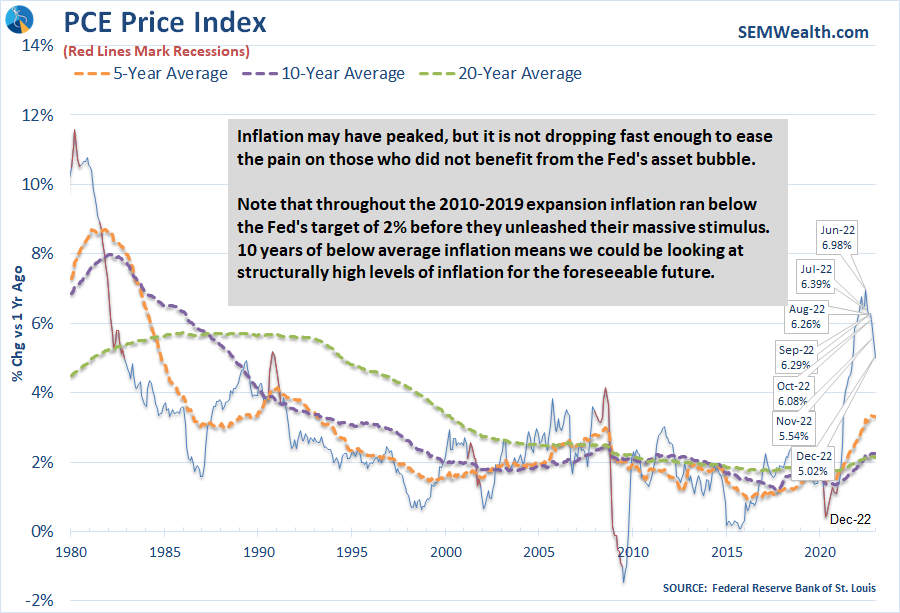

Turning to inflation, the market celebrated the release of the Fed's preferred inflation measurement, the PCE Price Index. It is now down to 5% after peaking just under 7% in June. The biggest unknown here is how much of the inflation we saw the past 18 months is permanent. Because it took the Fed so long to begin fighting inflation there is a chance a big chunk of it is permanent, meaning it may take a while to get down to the Fed's 2% target level. Remember, just because they might slow their rate increases, they have continued to warn the market they will not CUT rates unless they see inflation running below their target levels.

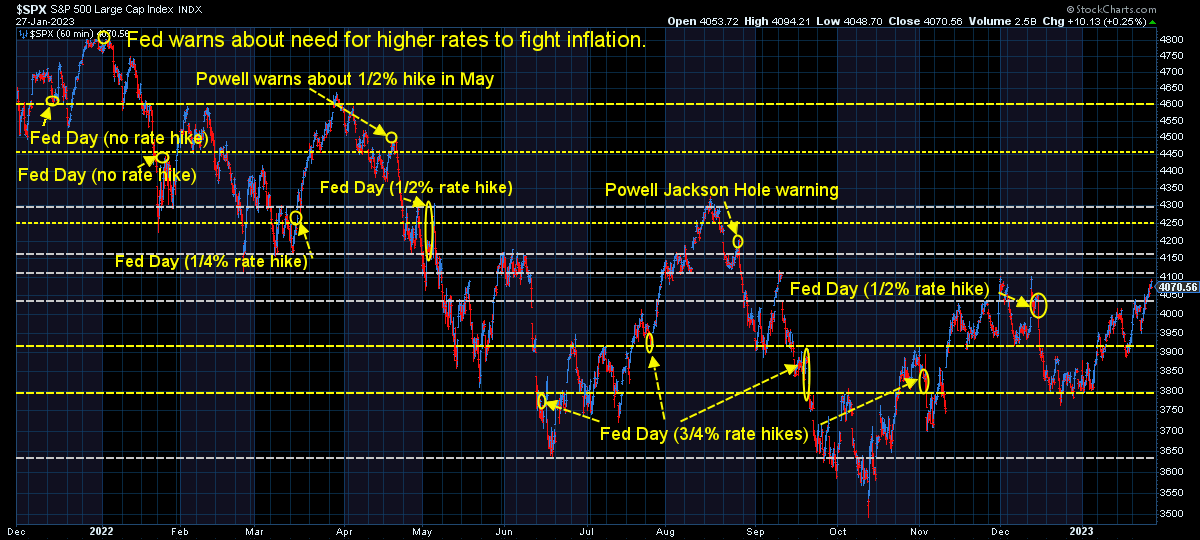

Turning to the market charts, the round number of 4000 has been solidly passed with the market ready to take on the next level around 4100. The market failed at 4100 in both September and December 2022. The "downtrend" line is technically broken for the first time of the bear market. It could be a sign the worst is over or this could just be a consolidation before the next leg down. Our models have not flinched (yet) and remain skeptical on this rally. (AmeriGuard and Cornerstone's trend models continue to have half of the normal allocation, a position they took at the end of October last year.)

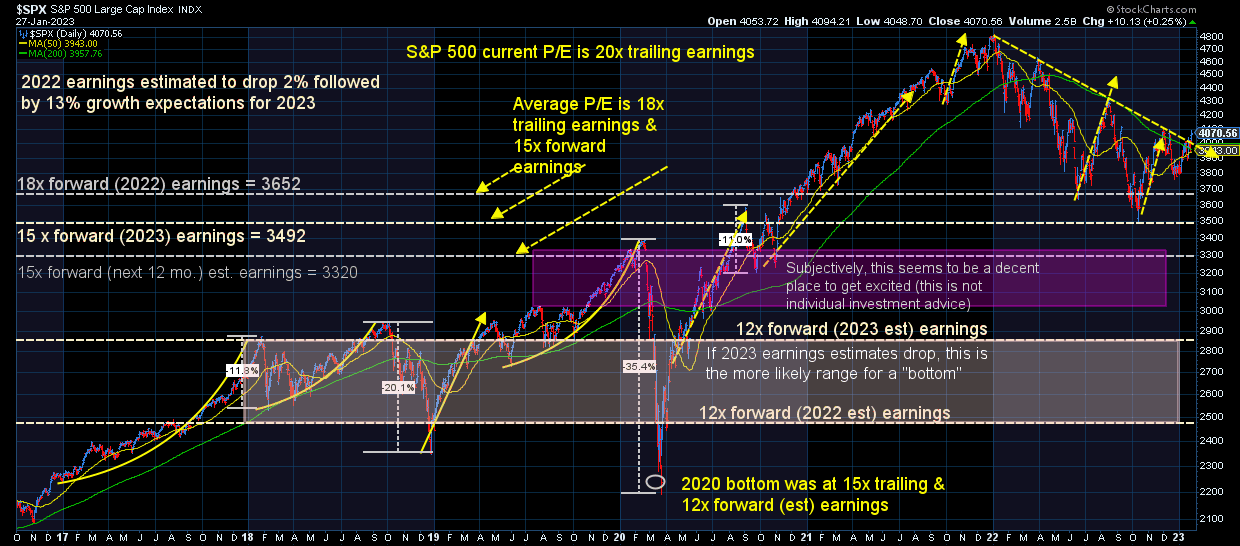

This chart is important to understand. Even if we hit the 13% earnings growth estimate the market is pricing in, stocks are at above average values, meaning the potential risks outweigh the potential rewards.

Turning to bonds, the 10-year yield bounced of the key 3.4% level. This could mean one of two things – the bond market is still concerned about the Fed's inability to control inflation --OR– the bond market believes the economy is going to grow strongly in the second half of the year. Our data says the former is more likely.

While the gains in January are welcome, we will continue to do what we've done the past 30 years – let the DATA dictate where, when, and how we invest. By design, the longer-term focused AmeriGuard and Cornerstone models are capturing a large chunk of these gains. The Dynamic models, which use our economic model are still participating, but at a slower rate. Our shorter-term focused income models (Tactical Bond and Income Allocator) are cautiously invested. You're not really being compensated by taking risks in high yield bonds so these models are leaning towards shorter-term and lower risk bonds. We may not be seeing strong price appreciation, but they are currently earning around 0.3-0.5% in dividends per month (which post a couple of days after the end of the month.)

Slow and steady with a focus on risk management is the key to long-term success.

Back to the economy, the bigger issue long-term is how few times the 1-year growth rate has exceeded the long-term average of 3.1%. Our economy has STRUCTURAL issues that need fixed. We've discussed that quite often. We also have been discussing the "K-shaped" economy since the middle of the pandemic. Over the past week we've been running a TikTok (and Instagram/Facebook) series talking about our broken economy. You can catch-up here:

@finance_nerd