The stock market continues its stampede higher following the re-election of Donald Trump. The assumption is apparently everything will be awesome. I truly hope that is the case, but as I outlined the week after the election, there are several areas where I believe voters, investors, and the President-elect himself may be surprised when they learn the assumptions they are making are not based on any sort of history, data, or economic reality.

The biggest of those are tariffs. Throughout the campaign, it seemed every question about economic growth, controlling the exploding deficit, fixing social security, and even lowering inflation was answered with the word "tariffs" somewhere in the response. The President-elect said it which led to enough voters believing it was true. I can't help to think of this clip whenever President Trump says tariffs will fix everything wrong with our country.

I want to be clear. This is not a political statement, but PLEASE understand tariffs and the subsequent retaliatory actions against the US (a Trade War) will cause prices to go up for the duration of the trade war. We were talking this week about the use of AI in our industry so I asked our Director of Technology to ask AI about tariffs. If you want to read the full response, you can do so by clicking here.

If the United Stated implemented tariffs on foreign goods today, would it reduce consumer prices over the next two years?

"Implementing tariffs on foreign goods today is unlikely to reduce consumer prices over the next two years. In fact, such a move is more likely to lead to higher prices for consumers in the short to medium term. Here's why......"

- Increased Costs of Imports

- Domestic industries may not fill the gap immediately

- Retaliation and Trade Wars

- Inflationary Pressures

Chat GPT also sited as evidence both the Smoot-Hawley Tariff Act of 1930 as well as the 2018 Tariffs on Steel and Aluminum. Studies of the 2018 tariffs from both the American Economic Review and the Tax Foundation found prices were HIGHER because of the tariffs implemented in 2018.

Conclusion by Chat GPT:

"In my opinion, imposing tariffs on foreign goods today would not reduce consumer prices over the next two years. The immediate and medium-term effects are more likely to be higher prices for consumers, strained international trade relations, and potential negative impacts on the economy. History and economic research suggest that tariffs act as a tax on consumers and are not an effective tool for reducing consumer prices."

We then asked if we should expect prices to be lower over the long-term (5+ years). The answer again was a resounding "no". This time Chat GPT discussed the anti-competitive (free market) dynamics these protectionist policies destroy including reduced competition, lack of innovation, and disruption of the supply chain causing increased production costs.

Overall, this is what I don't understand – the market believes Donald Trump is about "free markets" and "reduced regulations" but he is anything but. He still wants to go after Google and Microsoft for being monopolies. He still wants to take on the pharmaceutical industry. He still wants to limit immigration. He still wants government subsidies to support certain industries such as coal.

Long-term we probably do need to address many of the things the President-elect campaigned on, but the SOLUTIONS over the short and medium term are NEGATIVE for economic growth, consumer spending, debt, and corporate earnings. That is not being priced into the market (yet). When that happens is anybody's guess. My experience tells me it could be as early as inauguration day when we transition from the "idea" of Trump 2.0 and the reality of Trump 2.0.

We will be hosting a webinar at the start of the year titled, "Not another forecast webinar". Click below to register.

Economic Update

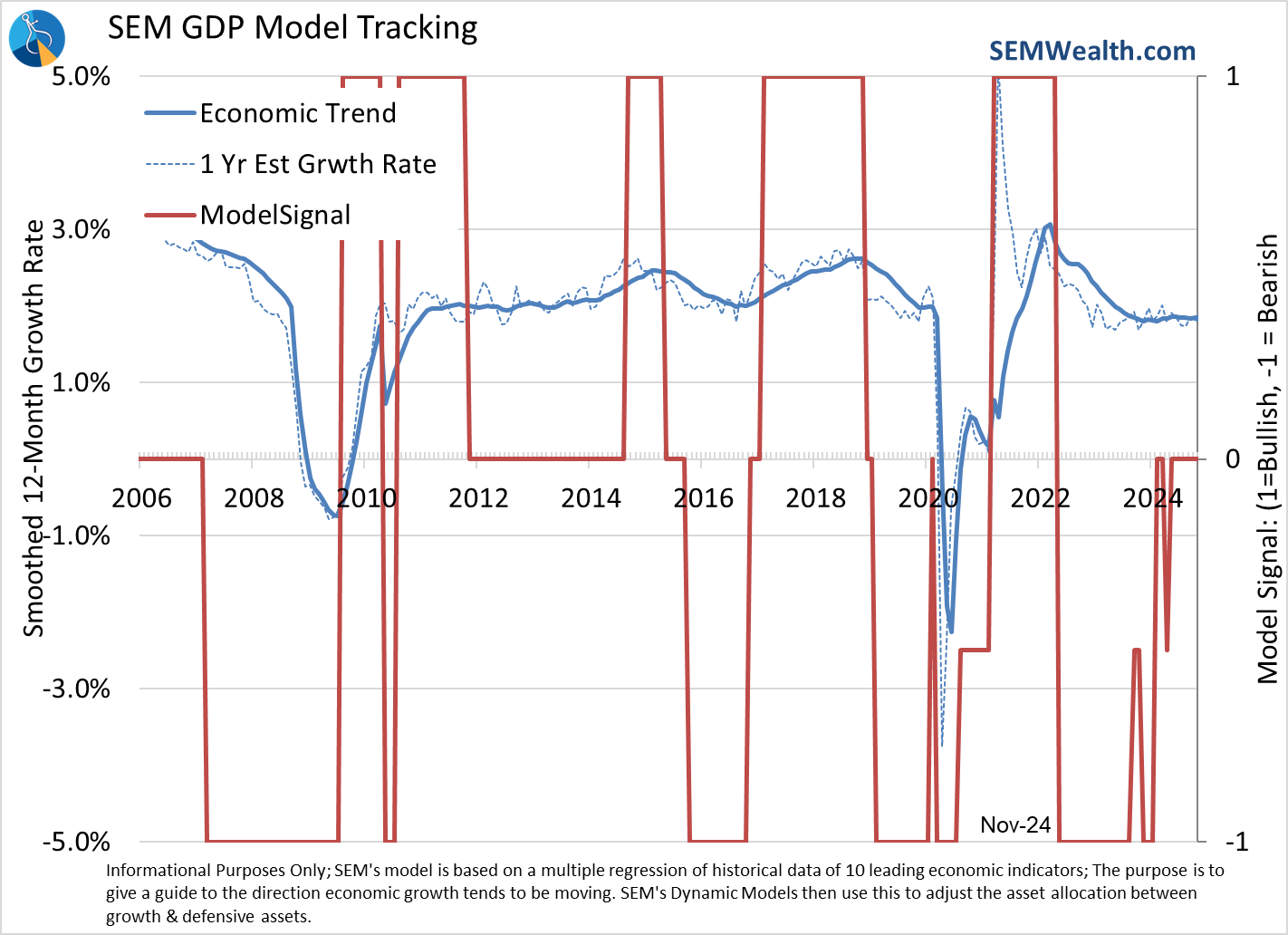

All of that said, it is hard to argue against the change in sentiment in both consumers and businesses following the election results. This is not yet showing up in the economy so I won't spend a lot of time this month diving into our model. It was neutral going into the election and remains there. I said in our pre-election webinar no matter who wins, they will have a tough time sparking a renewed economic expansion (which I define as annual growth rates in excess of the long-term average of 3% – something which was rare during both Trump 1.0 and Biden's terms.)

The big question will be whether the "vibe" change will turn into actual economic growth. Time will tell, but for now the DATA says the economy is in its most volatile period – trying to decide whether we are about to hit 'expansion' mode or are going to be going through a contraction.

Our economic model remains "neutral" as it has been.

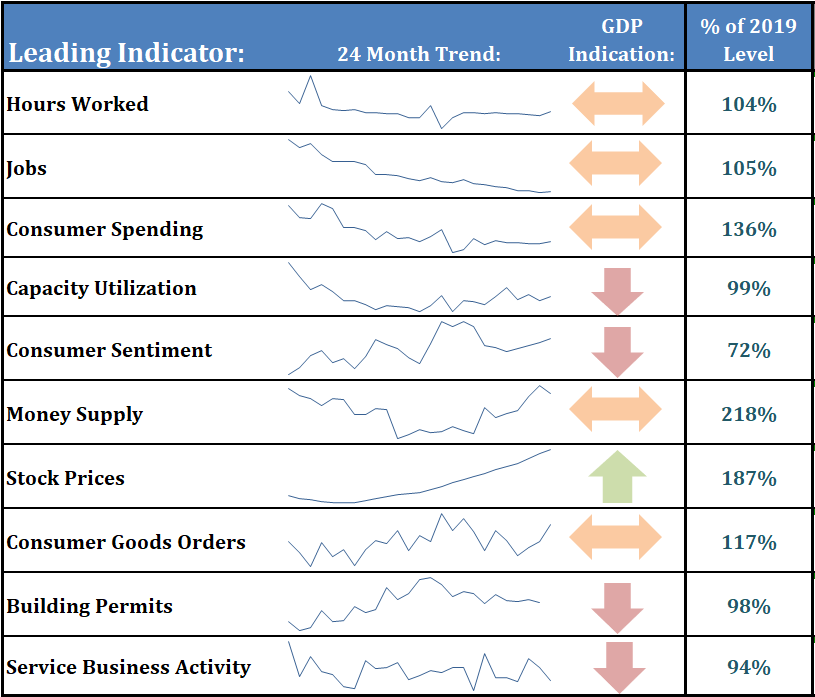

Like the last 4 months, the only leading indicator which is positive is Stock Prices. Maybe stocks know something and all of the economic numbers are going to finally start picking up under Trump 2.0. Or, with stocks at 22x 2025 expected earnings (which assume a 13% jump in 2025) stocks are priced near bubble territory (the only time the FORWARD P/E was higher was in 1999 when it hit 24 at the end of the year.

Why are we stimulating the economy?

I heard a JP Morgan asset manager on CNBC Friday say something I'm surprised more people are not talking about – especially those inside the Federal Reserve.

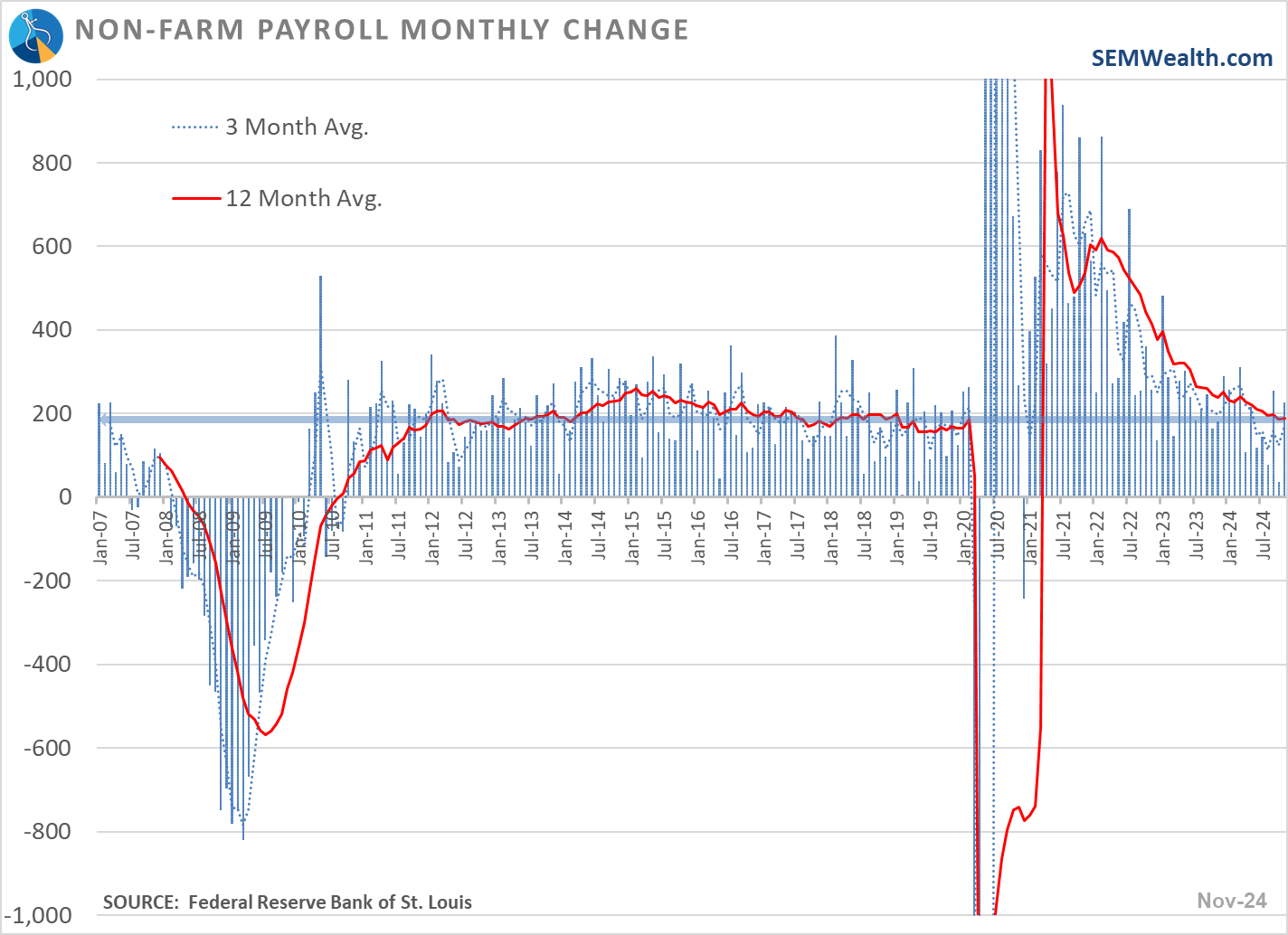

"If you were to drop an alien economist into our country and they looked at the data and saw, growth is running at 3%, jobs are increasing at a steady pace, inflation after falling near 2% has risen the last 3 months, the stock market is at an all-time high, and meme stocks are back in vouge, the alien would say, 'the Fed must be raising rates.' Instead the Fed is CUTTING inside of this environment and we are about to see the President and Congress also be stimulating growth. Just like the Fed waiting to raise rates until inflation was over 6%, this stimulus will be viewed as another big misstep by the Fed."

Tell me why the Fed is concerned about the jobs market? It seems pretty strong to me based on last Friday's report.

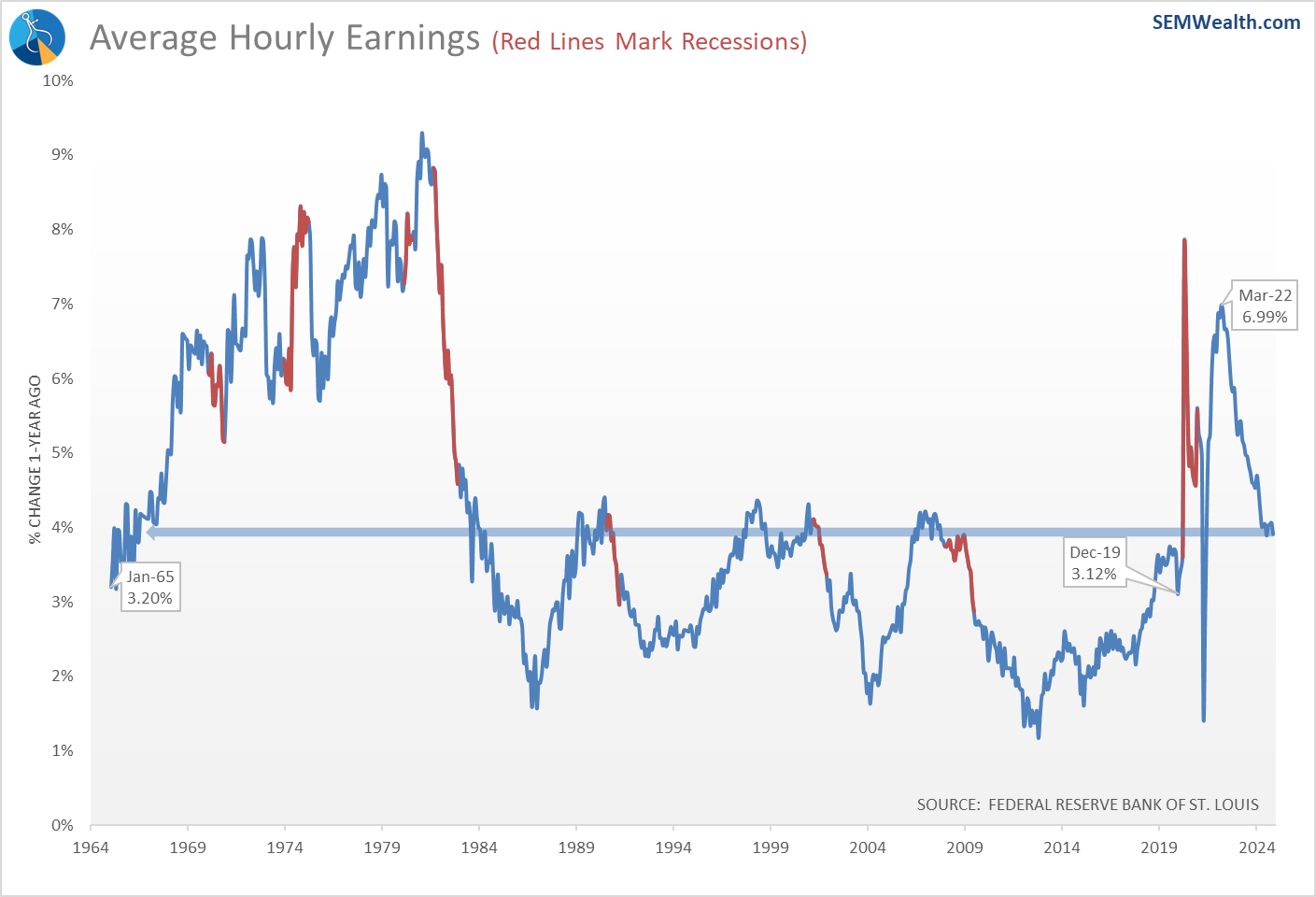

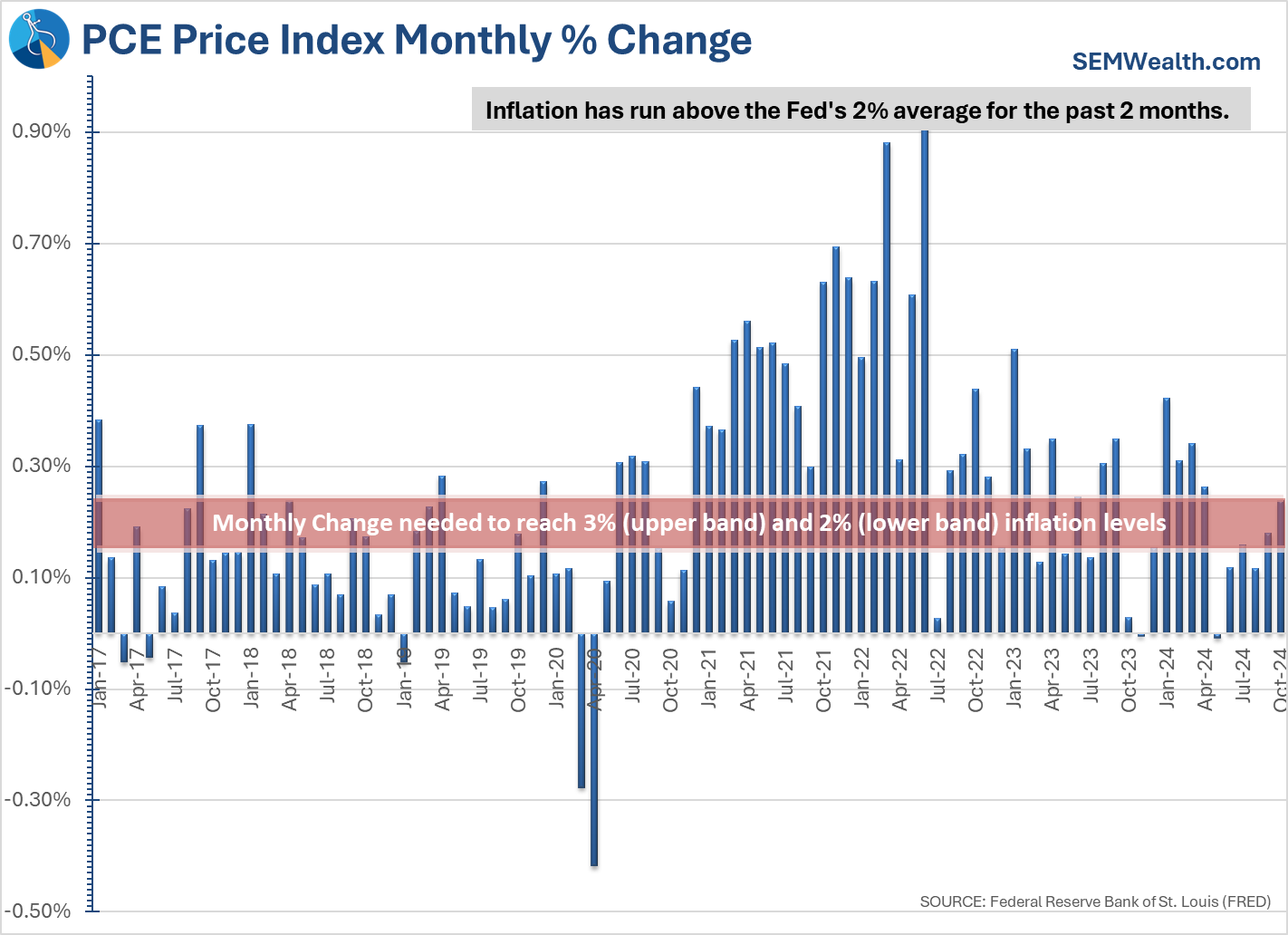

Tell me why the Fed is NOT concerned that inflation seems to have bottomed based on the most recent data? Wages again increased at a 4% annualized rate.

The Fed's preferred inflation measurement just increased for the 2nd month in a row and is again running above the Fed's 2% target.

Following the jobs report the Fed Funds Futures contract for December jumped from a 60% chance of another 1/4% cut in December to 90%. The commentators tried to justify this by saying "the Fed doesn't want to disappoint the market". One of the in studio guests is a professor from Harvard and he asked, "does what you all are saying not give you alarm bells? The Fed is purposely creating a stock market bubble and nobody seems to be worried."

We are all programmed to focus on the short-term. If the market is going up most people believe there is nothing to worry about. They believe the Fed knows best despite a miserable track record that would only be acceptable if you were coaching the Dallas Cowboys. I hope I'm wrong, but I don't think I am.

Please exercise caution. The fact the Fed is "on your side" should not be encouragement. The DATA says they should not be cutting rates and should actually be raising them. When they are forced to reverse course, possibly because of the Trump 2.0 plans, you will not want to be overly exposed to stocks.

Risk Premiums

In addition to what could be another volatile 4 years of governing by social media quips in the US, last week we were reminded it is not just the US which is going through some social upheavals. South Korea's president briefly declared marshal law, creating much angst and calls for his immediate replacement. Far more important is France's vote of 'no confidence'

For the better part of 40 years the US has enjoyed a relatively calm political environment where no major changes could happen thanks to the filibuster and 2-year elections which often swung control of at least one Chamber of Congress the opposite direction. We've seen a mass reduction in the regulatory environment, a big influx of cheap immigrant labor and the exporting of jobs which helped reduce costs and boost corporate profits. Interest rates declined for most of the period helping boost the availability of cheap financing.

It is entirely possible this 'easy' environment is shifting, which means at a minimum the "risk premium", the extra 'return' investors demand to compensate for taking risk, should increase. This means, unless growth rates are going to accelerate, the 'intrinsic value' of stocks should be lower.

I truly HOPE everything will be as awesome as people believe during Trump 2.0, but hope is not a strategy. When everyone is as complacent and optimistic as they are right now, my experience and study of history tells me we need to be extra cautious.

The nice part about working with SEM is we do not have to base our decisions on my opinion or anyone else's. Instead we will let the DATA dictate when to make any changes. For more on what the DATA is saying and how SEM is positioned, check out the next two sections.

Market Charts

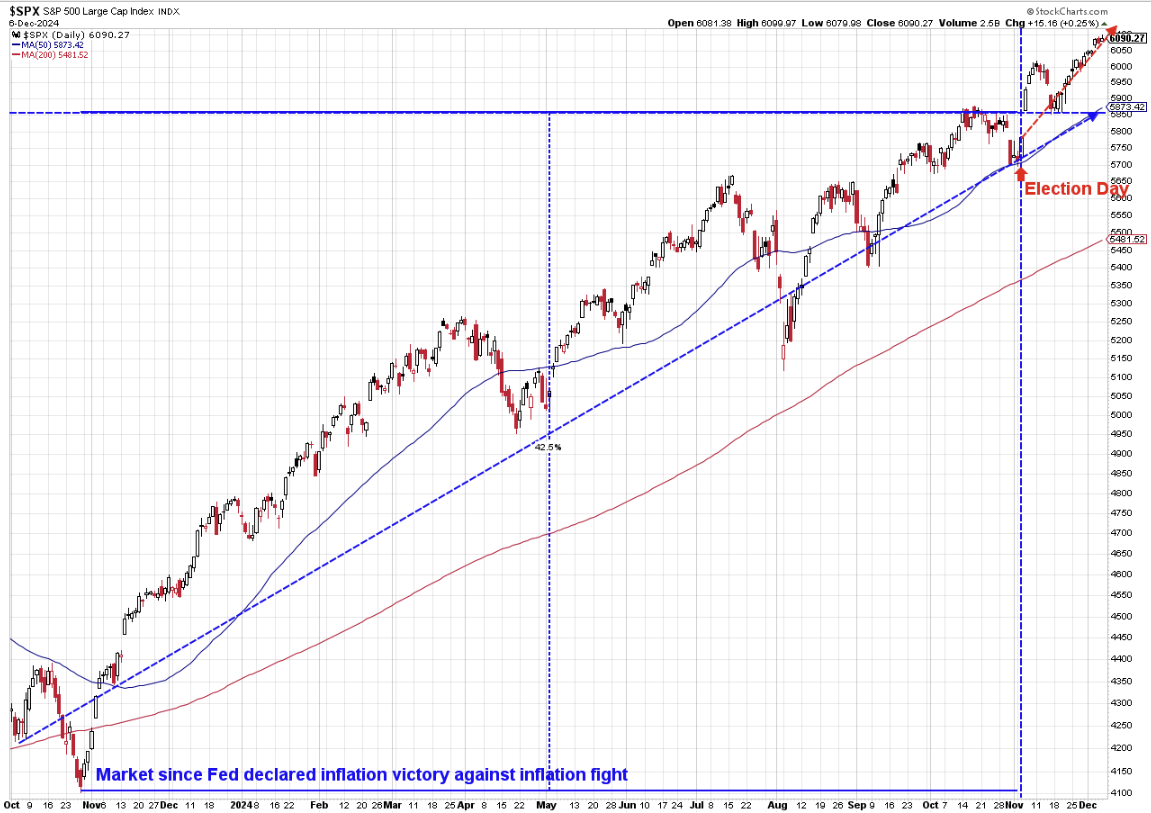

If you listen to most of the pundits, this seems to be the only chart that matters. Since the election, stocks are now up 5%.

I kept the blue trendline at the bottom for perspective. That is the trend that started when the Fed declared "victory" over inflation a little over a year ago. The trend already higher, but Trump's election victory accelerated it.

I know it might be unpopular to say, but if you look at the data, the stock market had a pretty impressive run, even including the 10-month bear market in 2022.

Right now the assumption is things will be even greater under Trump 2.0, but that would mean even stronger performance than we enjoyed the first time around.

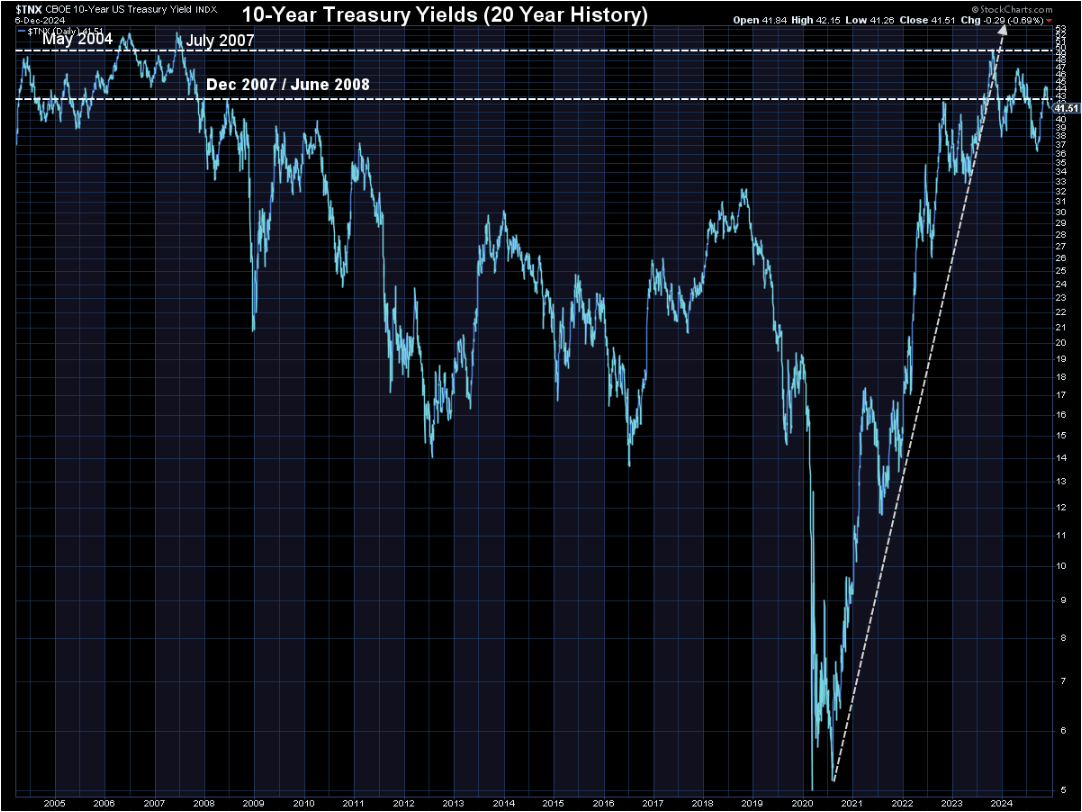

Of course the real focus needs to remain on the bond market. Rates have come down a bit the past couple of weeks, which is good news.

SEM Model Positioning

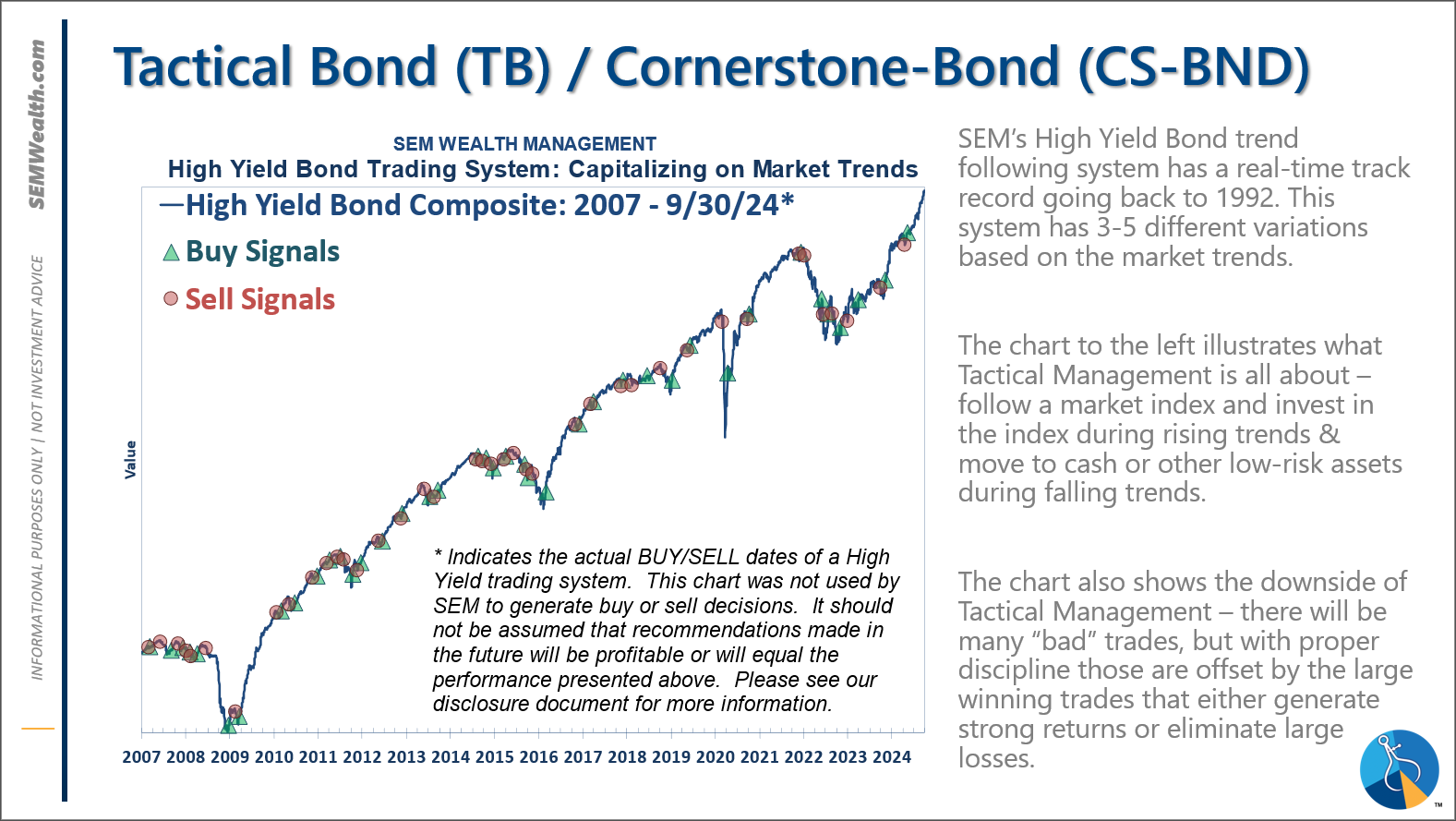

-**NEW** Tactical High Yield added a 30% position in floating rate bonds, which currently have a 9% yield compared to a 6% yield in high yields and 4.6% in money markets. This follows the partial (about 67%) buy signal on 5/6/24.

-Dynamic Models are 'neutral' as of 6/7/24, reversing the half 'bearish' signal from 5/3/2024. 7/8/24 - interest rate model flipped from partially bearish to partially bullish (lower long-term rates).

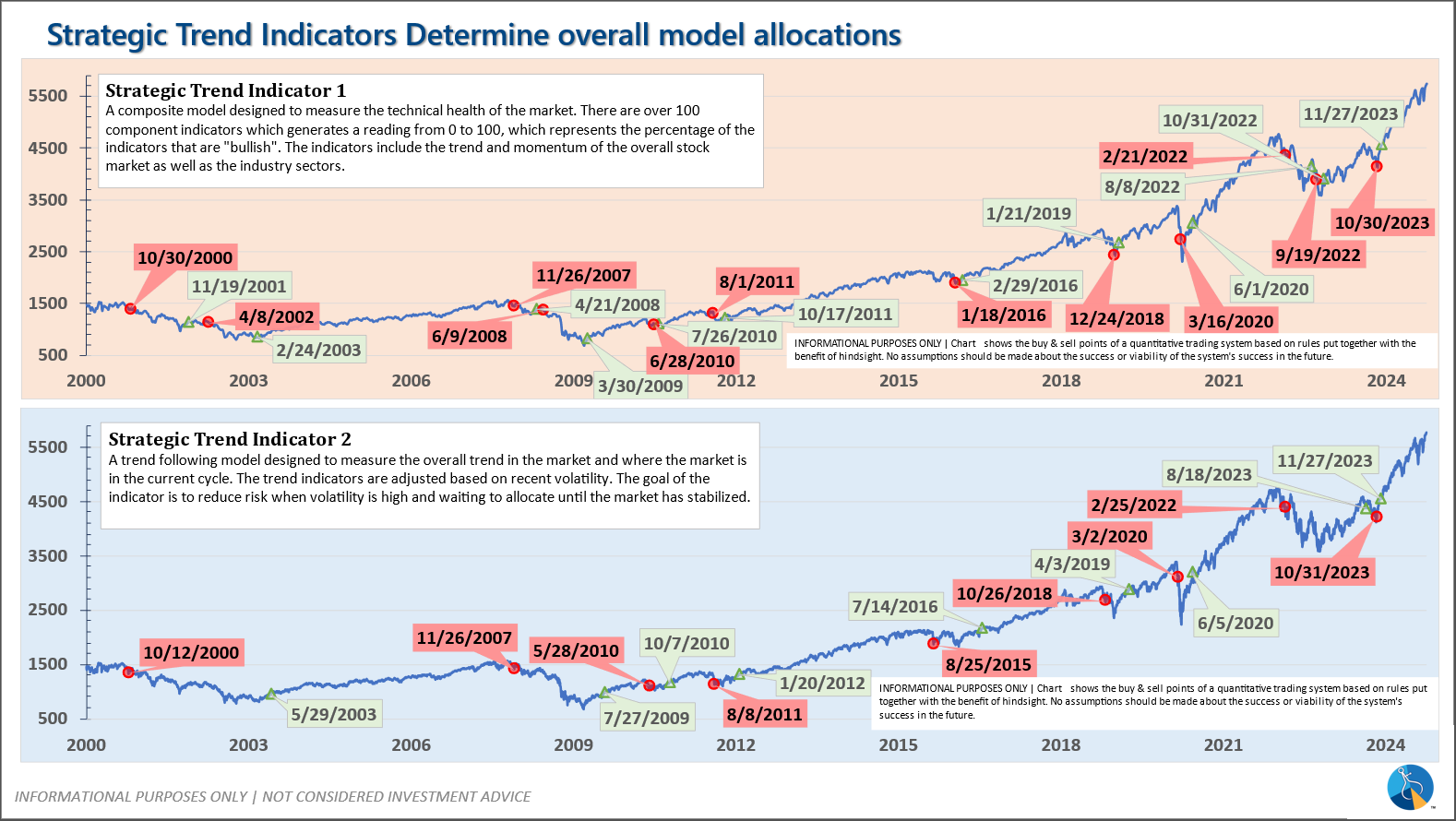

-Strategic Trend Models went on a buy 11/27/2023; 7/8/24 – small and mid-cap positions eliminated with latest Core Rotation System update – money shifted to Large Cap Value (Dividend Growth) & International Funds

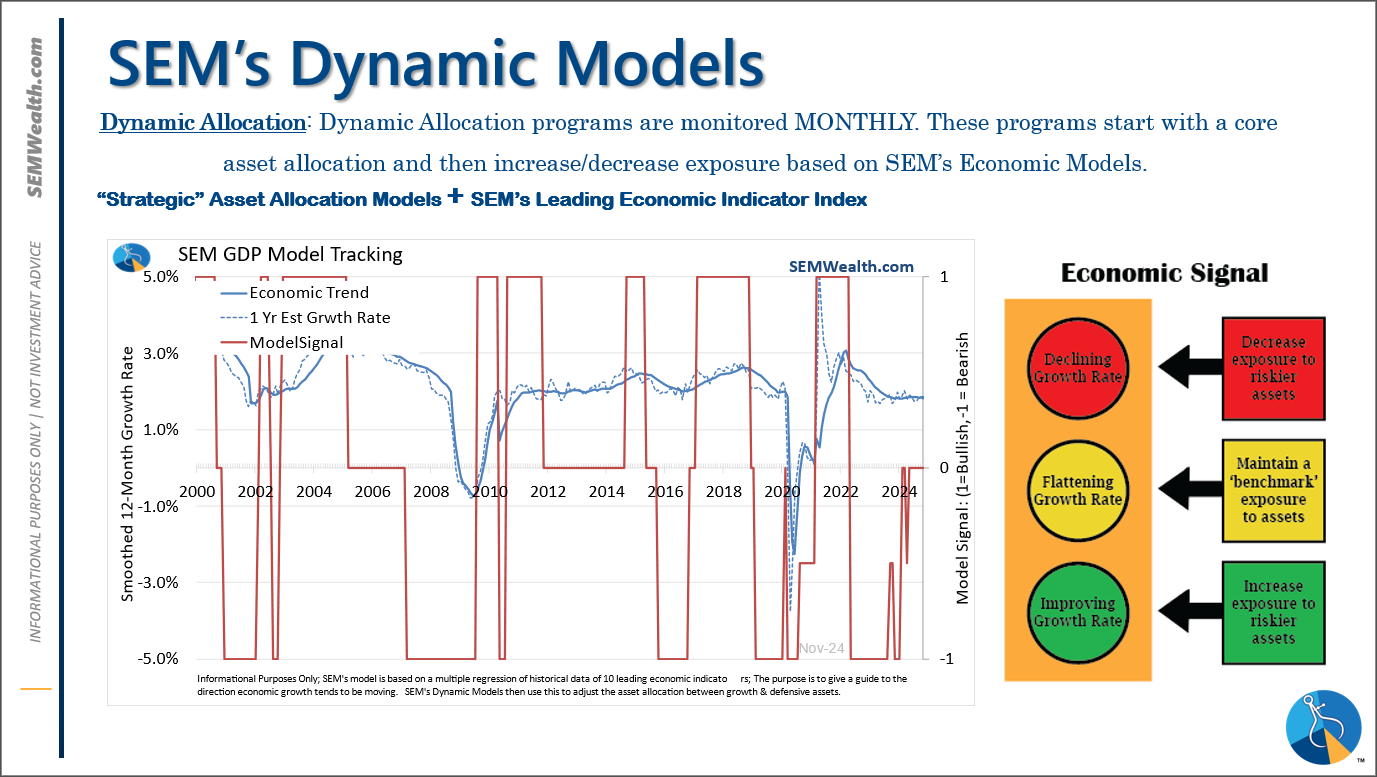

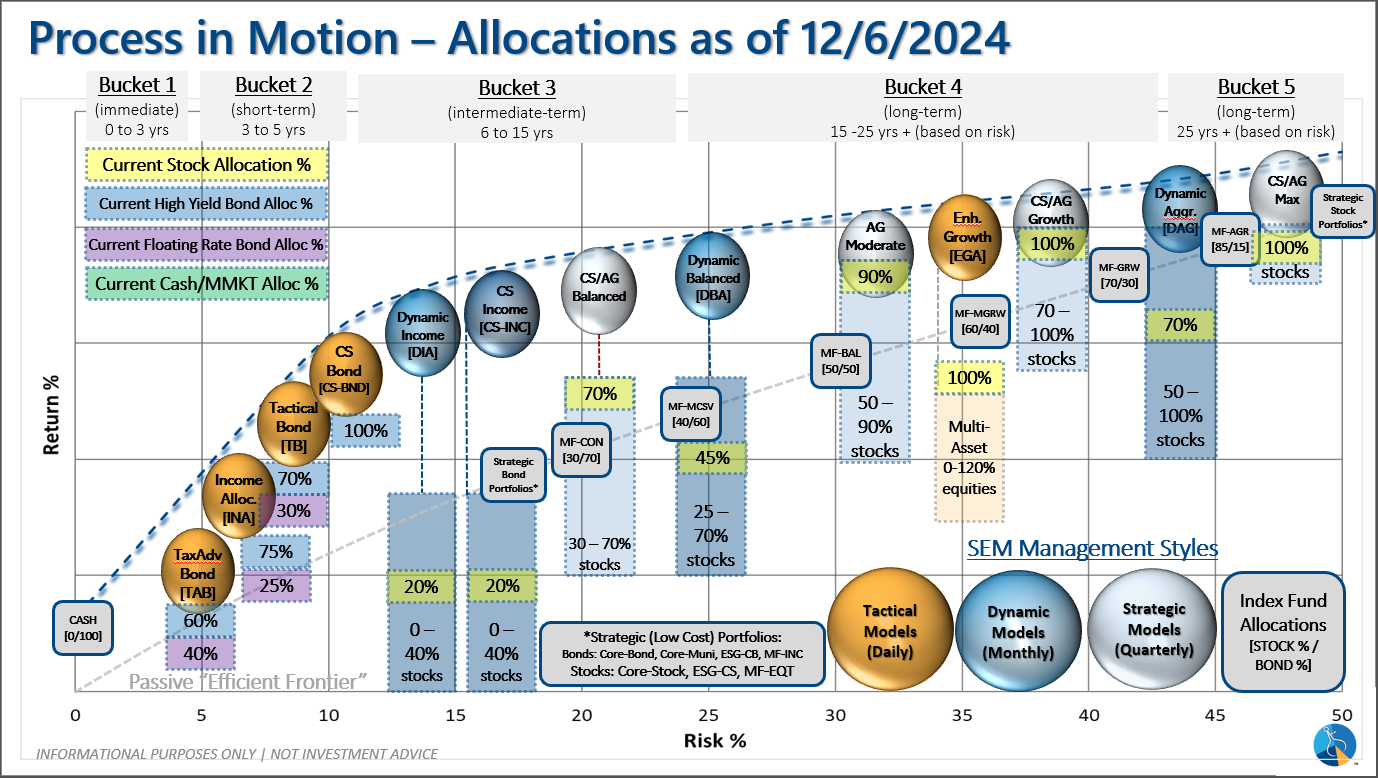

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

Tactical (daily): On 12/6/2024 our tactical high yield model allocated about 30% of the portfolio to floating rate bonds, which are shorter duration and have a higher yield than traditional high yield bonds. These instruments are not as sensitive to credit risk and are typically allocated to in the early and late stages of a high yield bond move in our model.

Dynamic (monthly): The economic model was 'neutral' since February. In early May the model moved slightly negative, but reversed back to 'neutral' in June. This means 'benchmark' positions – 20% dividend stocks in Dynamic Income and 20% small cap stocks in Dynamic Aggressive Growth. The interest rate model is slightly 'bullish'.

Strategic (quarterly)*: BOTH Trend Systems reversed back to a buy on 11/27/2023

The core rotation is adjusted quarterly. On August 17 it rotated out of mid-cap growth and into small cap value. It also sold some large cap value to buy some large cap blend and growth. The large cap purchases were in actively managed funds with more diversification than the S&P 500 (banking on the market broadening out beyond the top 5-10 stocks.) On January 8 it rotated completely out of small cap value and mid-cap growth to purchase another broad (more diversified) large cap blend fund along with a Dividend Growth fund.

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

Overall, this is how our various models stack up based on the last allocation change:

Questions or comments - drop us a note?

Curious if your current investment allocation aligns with your overall objectives and risk tolerance? Take our risk questionnaire