It's been bad enough trying to remember what day it is the past 11 weeks. Throw in a Monday holiday and we'll be confused all week. Today feels like Monday, with a slightly refreshed feeling thanks to an extra day away from the computer screens. More importantly, despite the "hardships" we all feel right now, we have to remember how relatively comfortable our lives are thanks to the men and women who gave their lives to defend our freedom.

Given the compressed week, I'll try to keep my musings short this week.

-The End of Conferences? The last two weeks I was at the "virtual" Mauldin Strategic Investors Conference and the CFA Institute National Conference. The efficiency of being able to attend these conferences from the comfort of my desk chair (or couch) while sleeping in my own bed each night and getting work done before and after each day's session is certainly a huge change. You do miss out on the networking and extended conversations with attendees, but you have to wonder about the trade-offs going forward. We also saved probably $5000 or more in hotel, food, and travel costs between the two conferences. That's money we can spend on technology, trading system development, or other things to help our clients. It is also money not going to the businesses and employees who rely on conferences.

I'm sure we won't see an end to conferences, but a "virtual pass" may be something attendees demand going forward. I've been wanting to attend both these conferences the last five years, but scheduling has always been an issue for whatever reason this time of year.

I also noticed both conferences were able to jam in many more presentations than they would have for an in person event. While this was exhausting, it was also refreshing to be able to hear from so many different speakers with such diverse backgrounds. As I always do, I focused on trying to find reasons my outlook is wrong. Unfortunately, most of those taking the opposite side of the argument had little data and a whole lot of "hope". The rest of this week's musings will be a portion of my summary notes from the conferences:

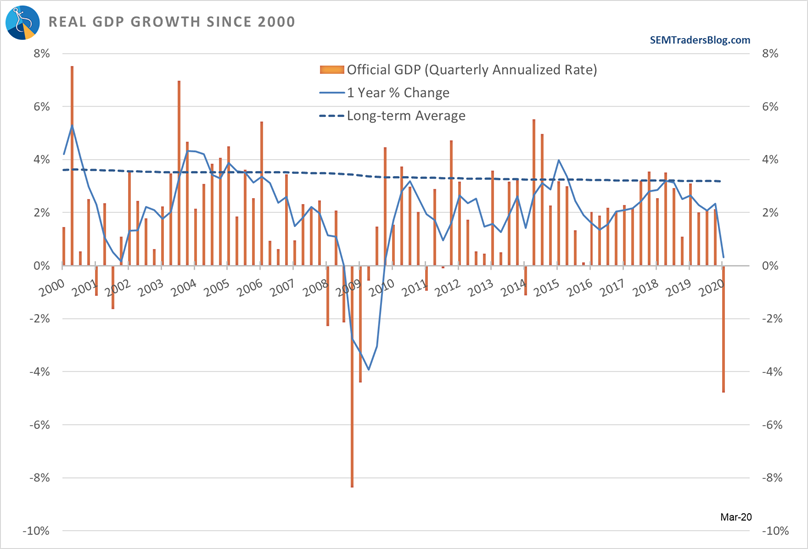

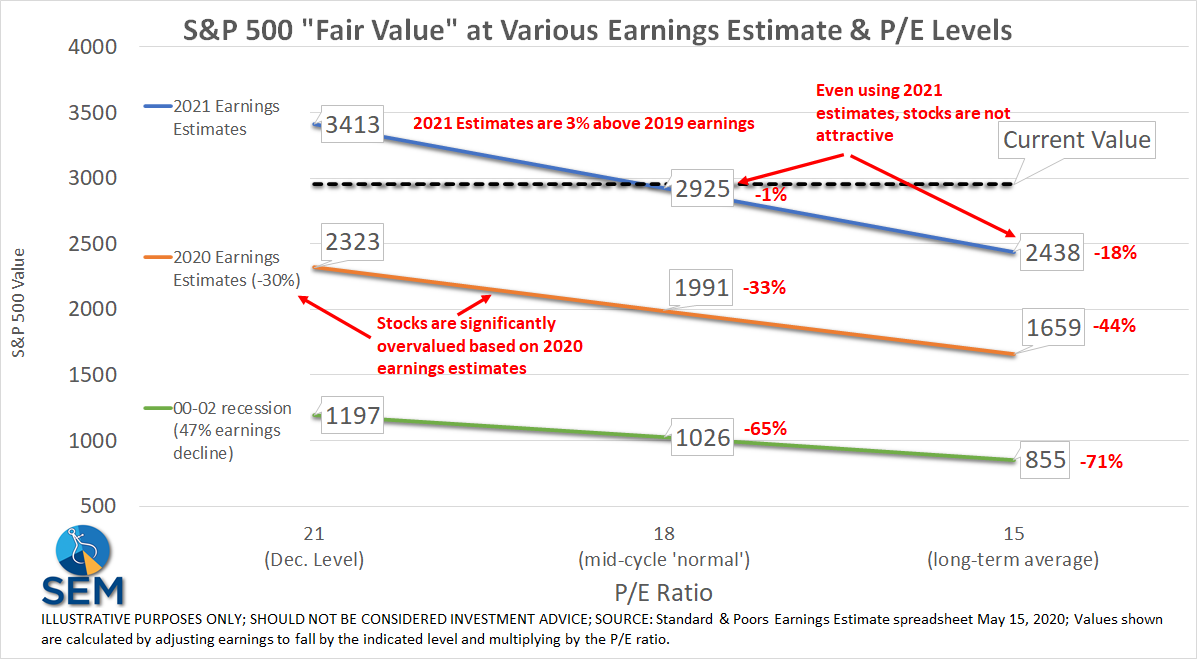

-Relative versus Absolute: Stocks are currently being priced based on a relative economy (how soon we get back to normal) versus absolute economic output (the long-term output) — we are seeing a significant shift lower in output levels; We will not get back to the old levels for quite some time, yet stocks are assuming we'll be back to "normal" in 18 months. In other words think of December 2019 as 100%. March 2020 with just 1 month of the pandemic saw output levels drop to around 90%. Economists estimate June 2020 we will see output around 70-75%. Going back to 90% or even 95% or 98% is not good enough to support stock prices as they assume we'll be at 103% of normal by the end of 2021.

Keep in mind we barely eclipsed the long-term average growth rate the last 20 years despite 20 years of deficit spending. We were already worried about this "structural shift" prior to COVID19 (due to demographics, a heavy debt burden, underfunding of pensions, social security, and medicare as well as a huge and increasing gap between the "haves" and the "have nots" the last decade). COVID19 has simply accelerated this and stocks are not pricing this in.

-Middle class again being hit the hardest: They had no savings going into the crisis due to stagnant income growth the last 10 years. They are now facing more job losses as the slowdown drags on, and the likely permanent reduction of those jobs. A struggling middle class is not good for anybody and leads to all kinds of problems, starting with political upheaval.

-Social Cycle will rear its ugly head: Speaking of upheaval, the stage we are at in the social cycle will not allow us to return to the old normal. We will see more class and generational clashes, none of which are good for the economy. This is an important concept and was mentioned by three different speakers who used three different methodologies to calculate the various cycles. All point to the 2020s being the "undoing" of all the excesses and collapse of all the social institutions created over the past 40 years. My most recent in-depth look at this was in "The Consequences of Political Polarization".

-How our brains process new information: I've said it multiple times the past 11 weeks – social media is making the crisis worse. Cody wrote an excellent piece last week I'd encourage you to read. Our brains are fascinating. I think if we're honest with ourselves we'd admit we've been subject to some of the biases Cody mentions. Click here for "How our brains are adapting to COVID19".

-Useless Stimulus: The massive amounts of debt being added by our country for the most part is not generating consumption, but paying obligations. This means we'll have nothing meaningful to show for it other than paying bills, but we will have to pay it back. This creates a drag on growth. Too many people cite the "stimulus" as the reason to be optimistic. Unlike the New Deal which created massive infrastructure projects which led to both jobs and increased long-term productivity, giving people money to pay their rent, mortgages, credit card bills, auto loans, utilities, and to buy groceries and other necessities does not have a long-term benefit (other than helping reduce short-term pain, which is of course necessary).

-No such thing as a free lunch: There will be consequences (again) of saving companies who should have failed. This creates a long-term drag on the country and reduces potential growth. A healthy economy does not continue to allow companies to take on excessive risks that never generate enough revenue to compensate for those risks and then to absorb future tax dollars via a bailout. While painful over the short-term, letting businesses fail and bonds default shifts capital away from failures and towards businesses who have ideas which will generate future growth. Which would you rather do, have losses spread out over 10 years which generates sub-par growth or take your losses now with above average growth over the next 10 years? Congress and the Fed has chosen the former for the second time in 12 years.

-Just because they say its cheap, doesn't mean it's cheap: When you buy stocks you're supposed to be looking at it from an ownership point of view. This means looking at the potential future streams of cash flow (earnings) and discounting the value back to today's dollars based on the risks to those earnings. The current earnings estimates do not reflect a STRUCTURAL shift, but assume a return to the old normal in 18 months. Worse, the "risk premium" has barely adjusted higher during the crisis, meaning if you're buying (or holding) stocks right now you're not being compensated for the excessive amount of risk you have now versus what you had in January before we'd heard of COVID19. I've heard some people argue P/Es can be higher due to lower interest rates. This is a theory with no basis in reality. In fact if you look at Europe or Japan who both have negative interest rates and have had rates much lower than the US for years (or in Japan's case, decades) their P/E ratios are significantly lower than the US.

Why are P/Es lower in Japan and Europe? The same reason interest rates there and the US are so low — the potential growth rate of the economy is much lower than "normal". We're talking P/Es in the 10-12 range if we follow the Europe or Japan model. Even if you argue P/Es should be higher than average, I cannot be more direct when I say, "YOU ARE TAKING EXTREME AMOUNTS OF RISK BY BUYING OR HOLDING STOCKS AT THESE LEVELS."

-The danger of a service economy: An economy based on services and consumer spending is a fragile economy. We were essentially paying people to do things we could have done for ourselves in our own households. Most services are "luxuries" when it comes to budgeting. I think we've all learned there are things we were spending money on that was probably not necessary. As we go forward with the "recency" bias of losing our jobs in an instant, many Americans will keep a tighter rein on their cash flow. Many of those service jobs may never come back. Several of the panelists at the conferences said to expect unemployment in the 9-12% range at the end of 2021. This is not healthy and leads to longer-term economic and social issues.

-Punishing Good Behavior (again): Savers are being punished (again) with low interest rates; taxes will inevitable go higher; fiscally irresponsible state and local governments will see their obligations shifted to the entire country. This has both economic and social consequences and certainly won't be good for long-term growth.

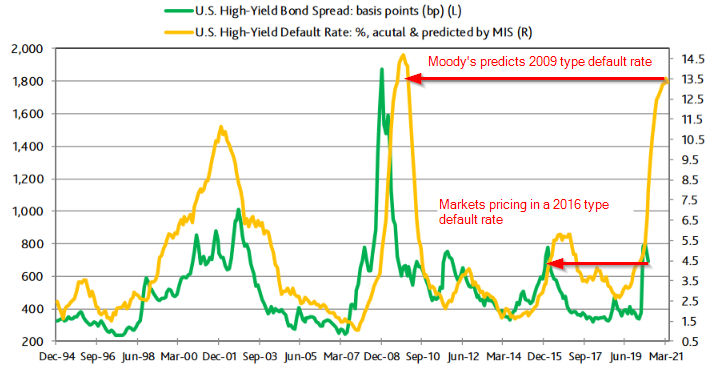

-Not Everybody Can be Saved: Bankruptcies / defaults will still happen; small businesses will fail at a heavy rate; These losses will create significant damage to the economy, similar to the Global Financial Crisis (or worse). Stocks lost 53% in 2008-2009. They are only down 12-15% today. The markets seem to think this will be just a small speed bump. Moody's disagrees. They are predicting a huge spike in defaults, which the market is not yet pricing in. If they are right, this will have very negative consequences for both stock and bond investors. Who would you trust – the people who look at each underlying issue or the people investing under the belief the Fed will save everyone?

-The economy was weak BEFORE this happened: Everyone keeps yearning to get back to where we were before COVID19. The problem is, the economy was not that great. 2019's stock market gains should not have happened. Economic growth was slowing. Earnings were flat. Consumers spent 3% more than they earned. We pointed this out at the beginning of the year. The weakness in the economy clearly shows up in small cap stocks. Our economy needs small companies to thrive. Sadly, we're seeing the mega companies get the bulk of the stimulus.

Small company stocks are down 30% from their 2018 highs (yes I said 2018) and are back to the same level they were at at the end of 2017 — just before the Trump tax cuts went into effect. In a healthy economy these companies would be thriving, instead they are clinging to life. COVID19 has only made it worse.

-This wasn't "great": We were running a $1T deficit at full employment when we started the year and not generating much growth. In fact we were above the long-term growth rate of 3% just a few quarters under Obama and barely touched it again in 2018 following the Trump tax cuts. This was a symptom of a STRUCTURALLY WEAK economy BEFORE COVID19. Returning to this "great" environment with $4-8 Trillion of additional debt is not something that should excite anybody....especially those buying (or holding) stocks.

Because we've used so much debt and not paid it back, the velocity of money has been declining steadily since late 2007. (Velocity of money measures how many times one dollar entering circulation gets spent. The lower the velocity, the lower the impact of stimulus.)

-It's all about discipline and humility: We don't have to be right to be successful. Keep in mind NONE of our investment allocations are determined based on my opinion or anyone else's at SEM. Our systems are designed to adjust to whatever environment the market gives us. If you're banking on a "return to normal" then everything has to go perfectly. When the structural damage becomes apparent, stocks will need to be repriced to reflect the lower level of growth and higher amount of risk.

I actually have a sign on my trading monitor I made in 1998 when I joined SEM. It has moved to every computer monitor since then and has served me (and our clients) well over the last 22 years.

-A welcome reprieve: Re-reading all of my musings I couldn't help but notice the negative tone. Maybe that's how I got my nickname, "Mr. Sunshine". I don't enjoy pointing out the negative, but instead attempt to find things that are being missed by the market participants. I don't want our readers to be surprised when the current "everything is awesome" environment is slapped back to reality.

All that said, it is a welcome site to see so many people getting to leave their homes and enjoy our beautiful country. Maybe it will lead to a spike in cases, maybe it won't. The science behind the virus says we should expect it to struggle in warmer and more humid weather. It also struggles to spread when we're outside. This doesn't mean it won't come back in the fall, although I'm concerned most people will take a drop in cases even with widespread crowds at the beaches, lakes, restaurants, and parks as a sign we've conquered the virus. Time will tell.