Last week we reported the shift to “slowing growth” in our economic model. This resulted in a significant decrease in risky assets in our Dynamic models. A few advisors have commented on how the economy doesn’t matter for stock prices. On the surface (and a great deal of ‘recency’ (availability) bias) they are correct. However, even during the recent bull market and looking at our economic model we can when it indicated slowing growth the stock market struggled (2011 & 2015/early 2016 are the two most recent examples).

Shortly after posting last week’s blog, I saw an article from “Fat Pitch” discussing the Corporate Earnings Recession. (Side note: the AI being used is handy, but scary — this article was in the “suggested sites” on my iPad, which I use every morning to catch-up on my reading. I’ve been finding many good articles in these suggestions.) Anyway, Fat Pitch digs VERY deep into corporate earnings and the trends they are seeing in the data. If you’re into that sort of thing, it’s a great read. For everyone else, I’ll give you the highlights.

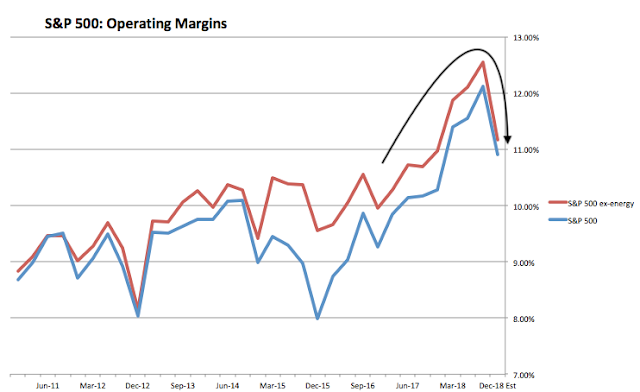

Profit margins in the S&P 500 are rolling over HARD. We hit record profit margins last year, helped by the tax cuts, but we’ve seen margins climbing to record highs even before the tax cuts took effect. The last time we saw a drop in margins was 2015/early 2016 and again in 2011.

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

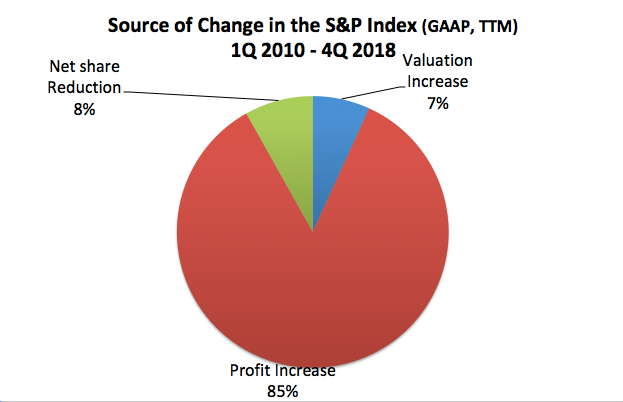

Margin expansion has been the overwhelming driver to the bull market growth for the S&P 500. Interestingly enough, contrary to popular opinion stock buybacks and expanding valuations only combined for 15% of the growth in the index during the bull run.

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

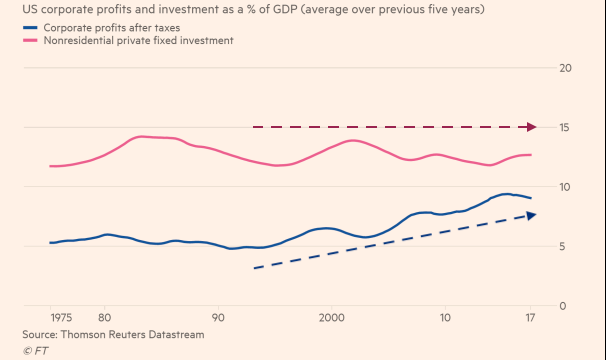

Not that valuations and stock buybacks do not matter for the long-term. Corporations continue to focus on short-term gains and are not investing in projects that will add long-term benefits to the company. Despite rising profit margins corporations simply are not re-investing in their companies.

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

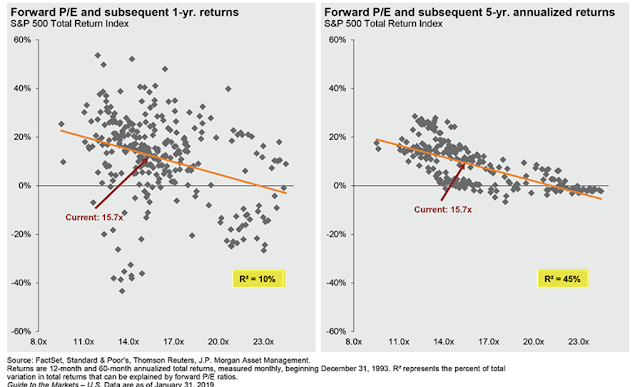

As for valuations, the final charts of the week show why valuations matter. They are terrible at predicting the returns for the next year. The predictive ability gets significantly better for forecasting the next 5 years.

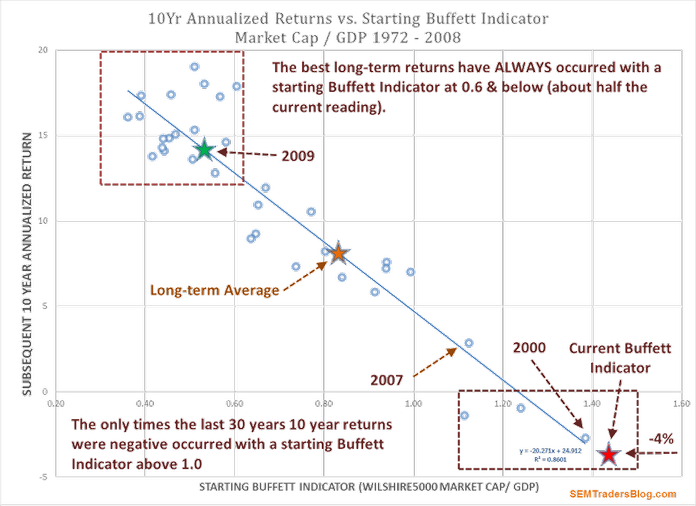

Of course using forward P/E is like using the Farmer’s Almanac to plan your Christmas trip in April. It’s literally a guess based on the current environment with some historical trends mixed in. A better predictor is the “Buffet Indicator”, which uses the economic concept that the US based companies cannot grow faster than GDP for a prolonged period of time (it’s mathematically impossible based on how GDP is calculated). Therefore, when the stock market is at a value significantly higher than GDP it is very likely to revert back to the mean (and most often BELOW) the mean as things reset. The current buffet indicator is predicting NEGATIVE 10 year returns for stocks. (for more see ‘What would Buffett do?‘)

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

If the corporate earnings recession continues, the Forward P/E will skyrocket. This will make negative 5 year returns much more likely as investors adjust to much slower growth. And don’t think bonds are out of the woods. A slowdown in margins will have severe impact on the unprecedented level of investment grade bond issues teetering on the junk bond breaking point (for more see Investment Grade Junk)