A common theme in my conversations with advisors across the country is frustration with the move towards passive, “free” investment solutions. In four years $1 Trillion has flowed into passively managed Exchange Traded Funds, with Vanguard sucking up 90% of those assets. Vanguard and many others are now offering ‘robo’ type advice for little or no cost. Like in the retail space, there is a legitimate fear from advisors of becoming “Amazoned” by these low cost offerings.

While the emergence of low-cost, do-it-yourself solutions are a function of a 9 year bull market (anybody remember the day traders quitting their jobs and utilizing the $5 dollar commissions at Ameritrade in the late 90s or the boom of “life cycle” funds in the mid-2000s?), sitting back and waiting for the next bear market to send a shockwave to those utilizing ‘robo’ advice with passively managed investments is not a strategy I would recommend. Granted, I am confident those solutions will fail for one simple reason — they are based on how investors SHOULD behave. The robot advisors expect the humans utilizing their solutions to behave like robots. Very few people have the personality nor the discipline to stick to these robo platforms in a severe decline. Most importantly many people already retired cannot afford the damage that will occur in the next bear market. Based on the simple fact they are human and human emotions have not changed since the beginning of time (regardless of technological innovations), the losses will be compounded by changing investment strategies at some point during the decline (often somewhere near the bottom.)

That said, there is a shift in our industry landscape that will leave far too many advisors going the way of Circuit City or Sears by failing to adapt to the new landscape. In our work with other advisors we are seeing a distinct difference in asset growth during these late stages of the bull market. Those that are simply standing by waiting for the next bear market are seeing accounts leave for the likes of Vanguard or other “free” advice platforms. Those that have changed the conversation and adapted their business to the new landscape are seeing significant growth.

How can you avoid being ‘Amazoned’?

Yesterday, WealthManagement.com posted an interview with United Capital CEO Joe Duran. Untied has enjoyed significant growth by encouraging their advisors to change their model. Here is a summary of how to adapt:

1. Be Where the Clients Are

Embracing technology means going mobile with your business. The next time you are at a restaurant look around. I often see more older adults looking down at their devices than the young adults that are criticized for always having their eyes on their phone.

Is your website mobile friendly? (Pull it up on your phone and if it’s not easy to navigate, then the answer is no.) Do you have an app? What’s your social media strategy? (and I’m not talking about canned links to articles — successful advisors truly interact with their clients via social media by providing more personalized content to your client base — they want to hear from YOU not some internet journalist.)

By the way, SEM has an app for both advisors and clients to view their accounts. Search SEM Wealth in the Android or Apple Stores.

2. You Must Live Where the Clients’ Money & Lives Intersect

Too often advisors want to deliver a canned solution. All the financial plans are the same and they only have one option on how to invest the money. Successful advisors focus on life management. They are there to walk them through all the stages of their life. They become the first person they call whenever something major happens. Figure out a way to become that resource for your clients and you’ll be able to charge for that advice regardless of the investment markets.

3. Understand Clients Better than Anyone Else in the Industry

This goes deeper than #2. Being able to truly understand the priorities the client has, their personal financial situation, their greatest fears and long-term goals allows you to be a life-long advisor for them. Being able to dig through their employee benefits, becoming an expert on social security, understanding their tax situation, working with them on their estate plan are all ways to continuously add value throughout your relationship.

4. Be a Guide and Coach for Your Clients

Robos are great when the stakes are low, such as when somebody is just beginning to get into investing. (SEM’s AmeriGuard platform is perfect for those investors–let me know if you’d like to learn more.) As the stakes increase, it becomes necessary to have a guide there to prevent serious mistakes from occurring. Most people realize what they SHOULD do, but few people will actually follow through with that. As an advisor you are a client’s financial personal trainer. You are there to encourage positive activities, correct mistakes in technique, and help the client achieve all of their goals.

5. Practice at the Top of Your License

Find out what you are good at and outsource the rest. This is where too many advisors lose their focus. If you are truly following #2 through 4 it is difficult to also select, monitor, and manage your client’s investments. There are so many details and intricacies involved in personal financial planning to take up your day as an advisor, investment management becomes secondary. You add over ten thousand investment solutions, unprecedented “emergency” actions taken by the Fed for the past 10 years, political instability, geopolitical risks overseas, a growing social divide, and the second longest bull market in our history and it becomes impossible to excel at both financial planning and investment management. When the market trend changes, you will have to devote your time to managing the investments at the same time your clients are also going to need somebody to hold their hand (see #4).

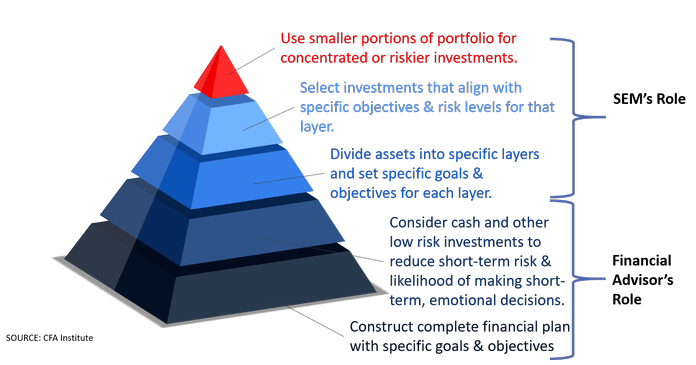

SEM’s new platform at TCA allows you to focus on financial planning while still having a full spectrum of investment strategies to choose from. This allows you to focus on being a financial planner and SEM to focus on being the investment manager. The chart below describes the “Behavioral Portfolio” approach. The foundation of this portfolio starts wit the personalized, detailed financial plan, moves into cash flow management, and then separating the investable assets into specific layers (or buckets). From there SEM can work with you to determine a suitable and efficient mixture of investments. For more information see “Our Portfolio” which describes our Behavioral Approach to investing.

6. Charge for Advice & Guidance (not investment selection)

If you are truly doing #1 – 5 you deserve to be paid the same no matter what happens with the investments. It should not matter if a client is in a daily monitored “tactical” strategy or a quarterly monitored “strategic” strategy such as AmeriGuard. Your job as the financial advisor is to work on the plan and then with the investment manager to make sure the investment solutions line-up with that plan.

One of the primary reasons we moved to TCA was the ability to allow the fees charged to the clients to be separated. We have encouraged our advisors to select a level fee for their financial advice (based on the service level they provide clients). On the statements the fees will clearly state “Financial Advisor Fee” and “SEM Management Fee”. We also have put together this piece on our website titled “What am I paying for?”

Splitting the fee like this completely shifts the conversation. You are now being paid for your advice & guidance, not the performance of the investments. What’s truly game-changing with SEM’s new TCA platform is the ability to adapt the investment allocation to each individual client’s personal risk tolerance, investment objectives, and personality profile.

If you would like to learn more how we can help you avoid being “Amazoned”, let me know.