Back in 2019 the daily blog entries turned into a weekly "Chart of the Week". There just weren't a lot of different ways to say what was happening – stocks seemed to go up every week. Any drop of 3% was bought aggressively. Valuations were at levels that indicated long-term returns would be low or negative. The economy was much weaker than the market had priced in. Speculation was running rampant as nobody seemed to foresee any risk in the market. Our models were fully invested, but growing concerned of signs of underlying weakness in the market.

In late winter 2020, the news was hitting us like a firehose which shifted the blog to a Monday Morning Musings format where I would summarize everything I was seeing. We'd add video and other updates as necessary throughout the week. We've continued that format into 2021. It will likely continue, but I'm running out of ways to summarize what I'm seeing:

Stocks seem to go up every week. Any drop of 3% is bought aggressively. Valuations are at levels that indicate long-term returns will be low or negative. The economy is likely weaker than the market has priced in (after the temporary stimulus boost is over). Speculation is running rampant and nobody seems to see any risk in the market. Our models are fully invested, but growing concerned of signs of underlying weakness in the market.

Since there isn't many other ways to say it, this week I'll try to tell the story in charts.

First, let's remember what is driving the market. So long as these pillars remain in place, the market should be able to move higher. Any cracks or ultimate failures and the market will likely get crushed.

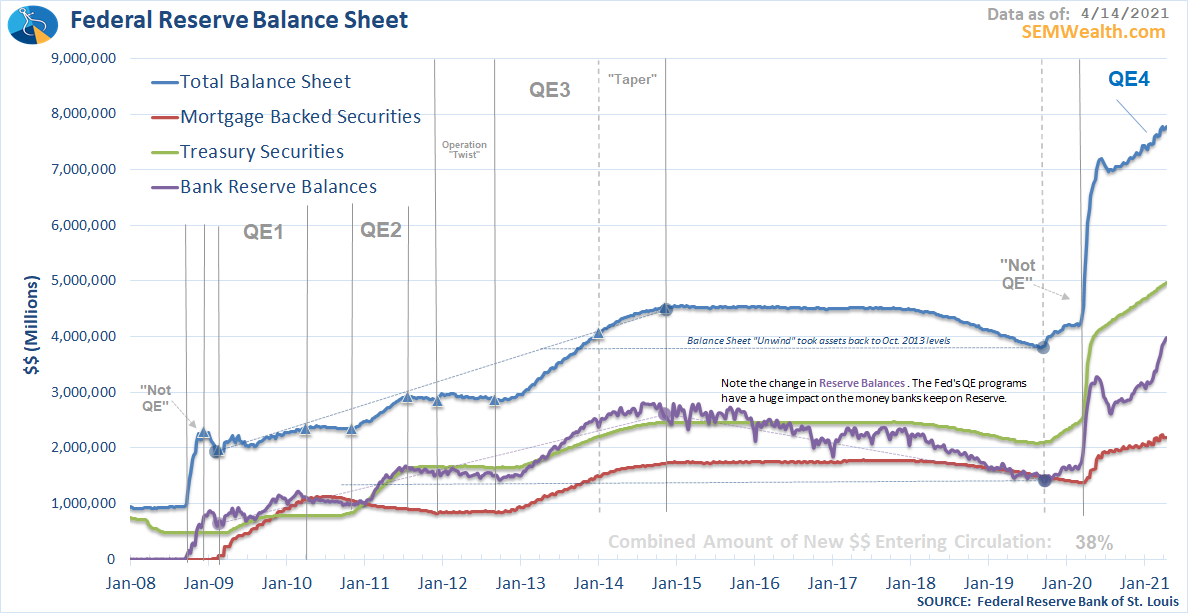

1.) Fed Support

The Fed certainly upped their game. This chart shows the Fed's Balance Sheet and where they have focused their purchases. They've essentially financed 1/3 of the budget deficit in the past year with their Treasury purchases. Sooner or later this support will end as they will not be able to continue at this pace without creating even more unintended consequences.

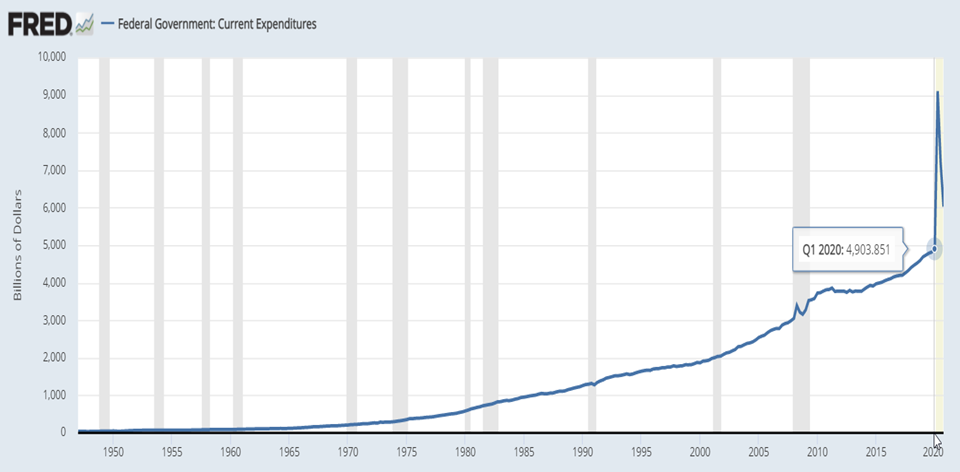

2.) Congressional Spending

Like the Fed, Congress brought a new level of support during the pandemic. I marked on this chart the pre-pandemic spending level for reference.

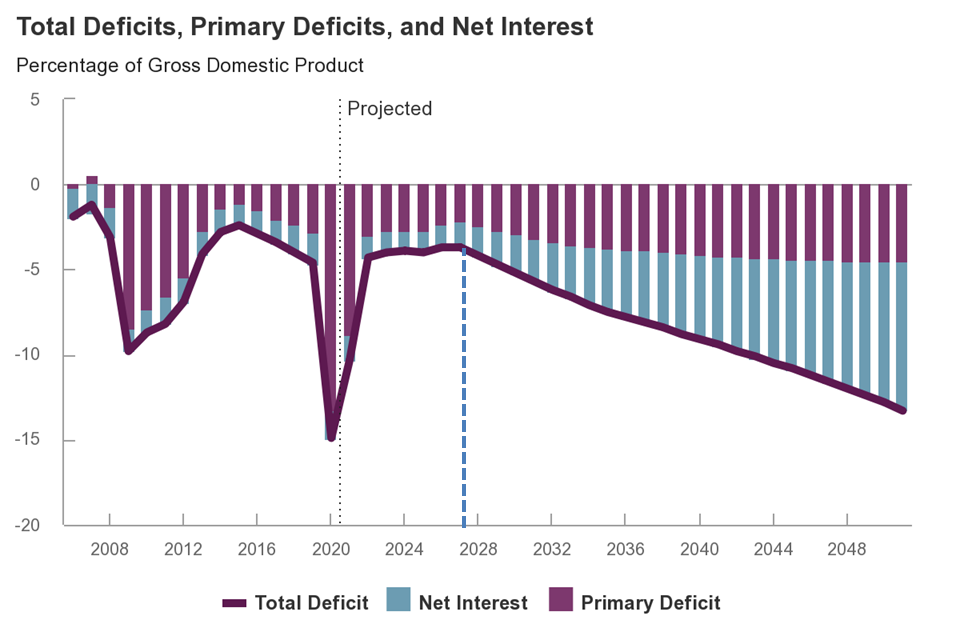

The issue is Congress has been running a huge deficit for years. "We'll pay for it later" seems to be the mantra. I'm often asked when the deficit will matter. My answer is always "when the market says it matters". A big concern all of us should have is when the debt comes due. Debt is future spending brought forward. If we don't INVEST the money we borrowed, it hurts future growth.

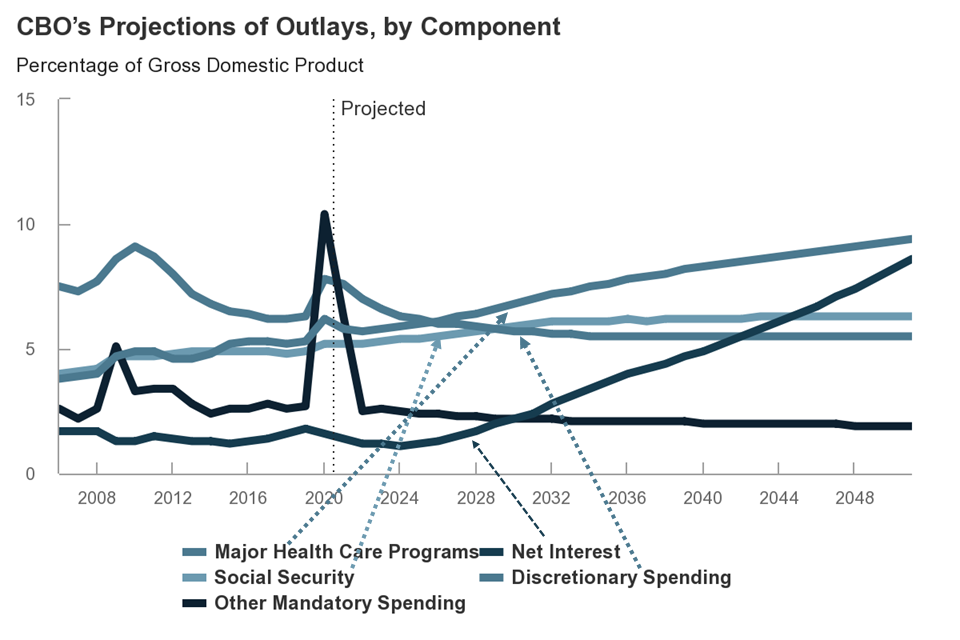

This chart from the CBO shows when the deficit will start to matter. Note in 2028 under current spending levels (ignoring the Biden administrations $3+ Trillion of planned spending–so far) interest expenses begin to become a problem.

This chart shows where the money will be going:

We're about to spend a whole lot of money on health care for older Americans. Social Security spending should level off in the next 10 years, but is still a large amount. In economic terms, both are a drag on economic growth, as is Interest on our debt. This is a serious STRUCTURAL issue that must be solved. Stocks are pricing in "average" long-term growth. These spending projections point to an environment that will be well below average.

3.) Improving Economy

For the short-term our economy is doing great.

The strength is a function of the Fed Support and Congressional Spending. Beneath the surface the economy is quite weak.

I discussed both the short and long-term outlook here:

Jeff Hybiak, CFA

Jeff Hybiak, CFA

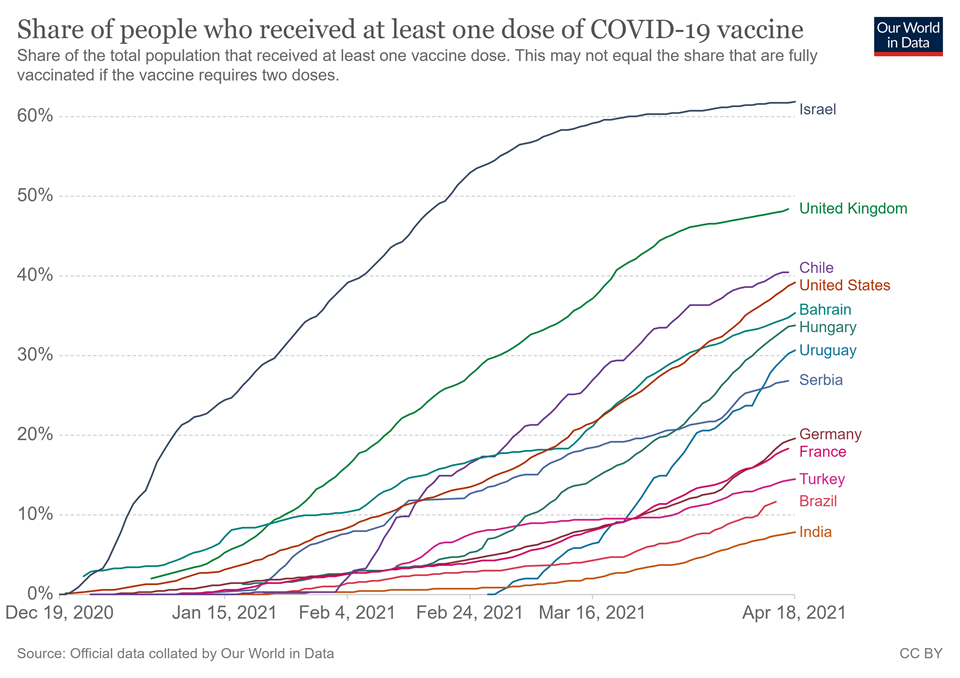

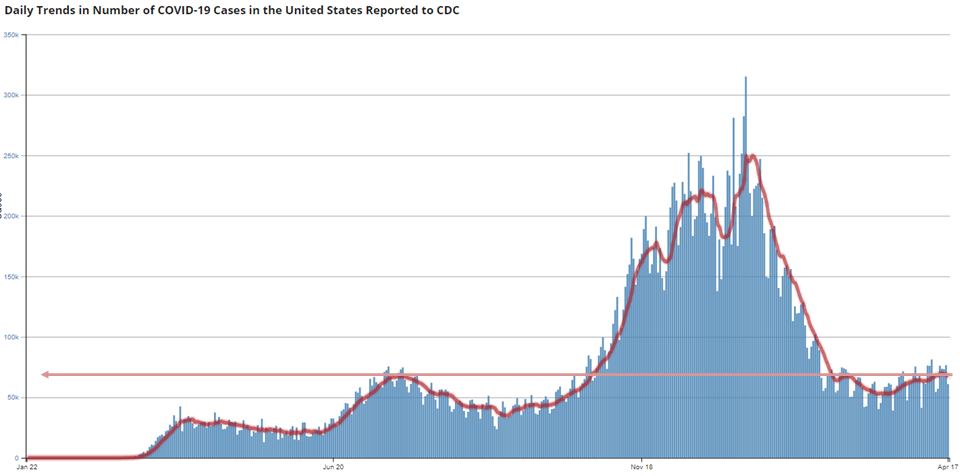

4.) Vaccine Distribution / COVID Cases

For us personally, this is the most exciting development. Throughout the pandemic I said we just needed to give our leaders some grace and do our part to buy time for the scientists. We have once again shown our leadership among all other developed countries, especially when you consider our population and the size of our country.

The concern remains in the unknown. We know there are people who will not take the vaccine this year. The variants are taking hold and our case count is still quite high. In fact, it is currently as big as the summer peak.

We cannot rule out the virus from at a minimum causing more Americans to stay home or at worse to cause enough fear later this year that we see more restrictions on businesses again.

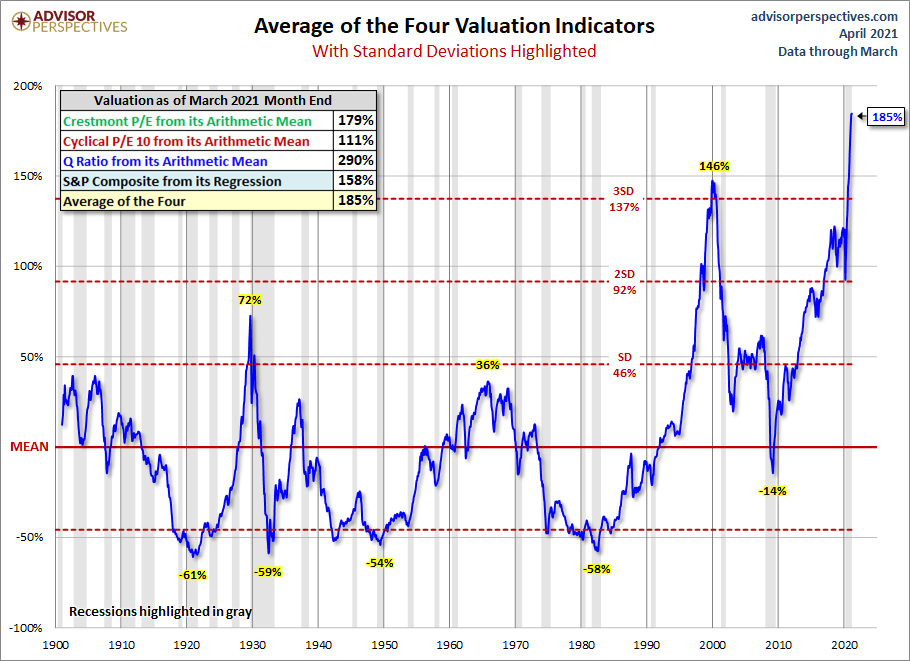

Valuations Matter

My take after reviewing the charts of the 4 pillars – I question the strength of the market. All are susceptible to falling, which makes investing at this point quite risky. There are certainly positive things, but EVERYBODY expects those positive things to develop. Our job is to look at what could go wrong.

Whatever your assessment, if you are in the market right now, you have to look at your potential returns. If you are in a buy and hold investment you are supposed to be a long-term investor. The adage "buy low, sell high" is something you should pay attention to. Right now, valuations are near record levels. In some cases we've never seen valuations this high.

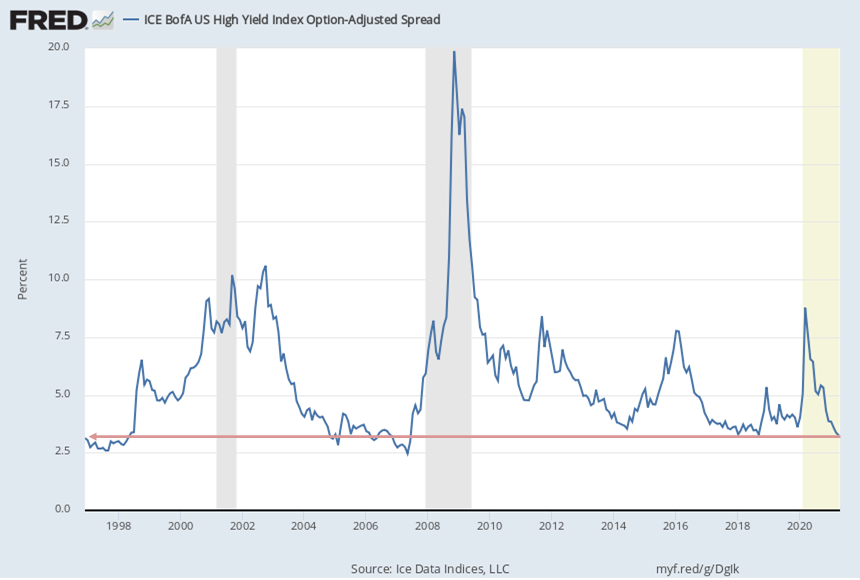

Let's start in the bond market, where valuations can be measured by the difference in yields versus Treasury Bonds. While not quite at a record, we are certainly near the lows of the cycle.

Historically when we are down here, we see bond issuers begin to default, lenders tighten their standards and more bond issuers default. The weak are wiped out. Speculators lose a ton of money. Eventually the bad issuers are gone and the good issuers remain. We've been managing high yield bonds since the 1990s and this is always the case. Nothing has changed that will prevent this from happening again.

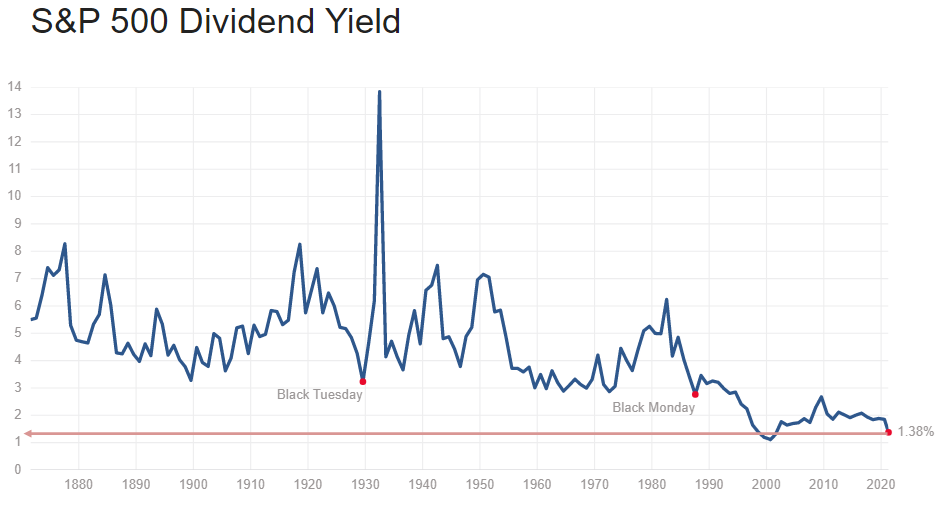

I've heard too many times people saying, "with bond yields so low, you should buy dividend stocks." This is TERRIBLE advice! Even if you ignore the fact dividend stocks have historically lost more money than the S&P 500 during bear markets, the current dividend yield is close to a record low. The only time it was lower was at the end of the tech bubble.

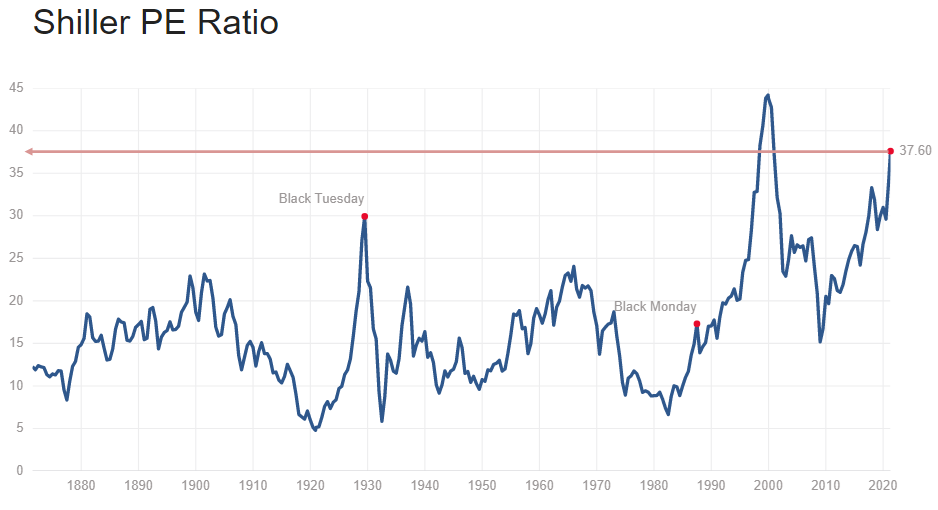

The P/E ratio tells the same story. Again the only time it was more expensive to buy stocks was the end of the tech bubble.

It's not just P/E. Every valuation metric I've looked at points to a historically expensive market.

If you are in a buy and hold investment now, you must ask yourself — is the economic outlook today better than it was back in 2000? Be honest with yourself. At least during the tech bubble we had game-changing developments that had the potential to make us all more efficient.

What do we have now? Yes it's exciting the economy is re-opening and getting back to "normal", but the "normal" of 2019 is much worse than the "normal" of 2020 from a growth stand point.

Please be careful. Better times to invest will come. History and logic tells us this is not it.