Have we reached the end? Just as March 2020 marked the beginning of the COVID19 economic shock, March 2021 could go down as the end of the shock. As vaccine distribution hit critical mass, the weather turned nicer in the southern states, and yet another round of stimulus checks hit bank accounts, it appears Americans have become much more optimistic about their financial futures.

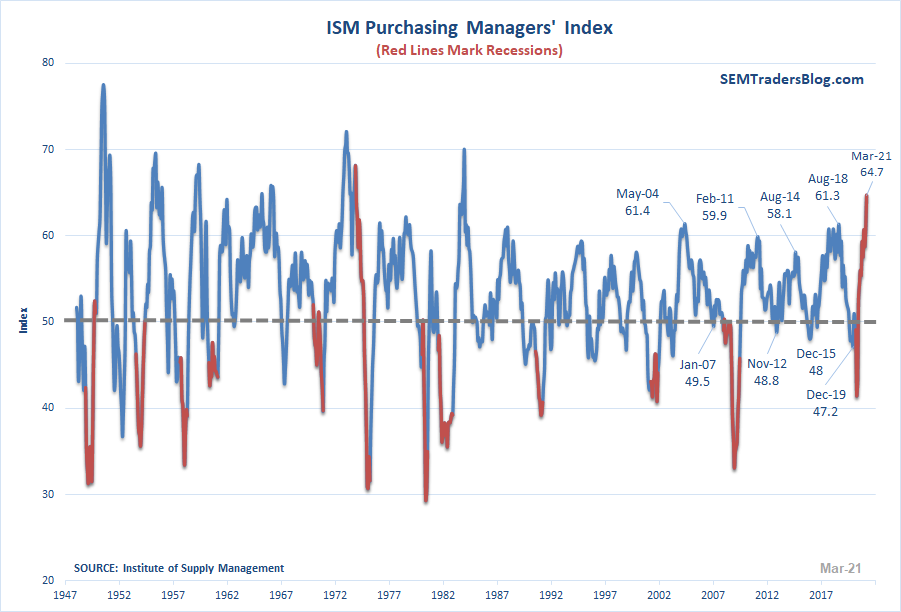

The bellwether of all economic reports is the Payrolls report. On Friday we saw numbers that were not only better than expected, but revisions higher to the prior two months. This came on the heels of a strong Manufacturing report and a big boost in Consumer Sentiment. All of those reports play a major role in SEM's Economic Model as they give us the first glimpse into what happened in the just ended month.

Was it really that great?

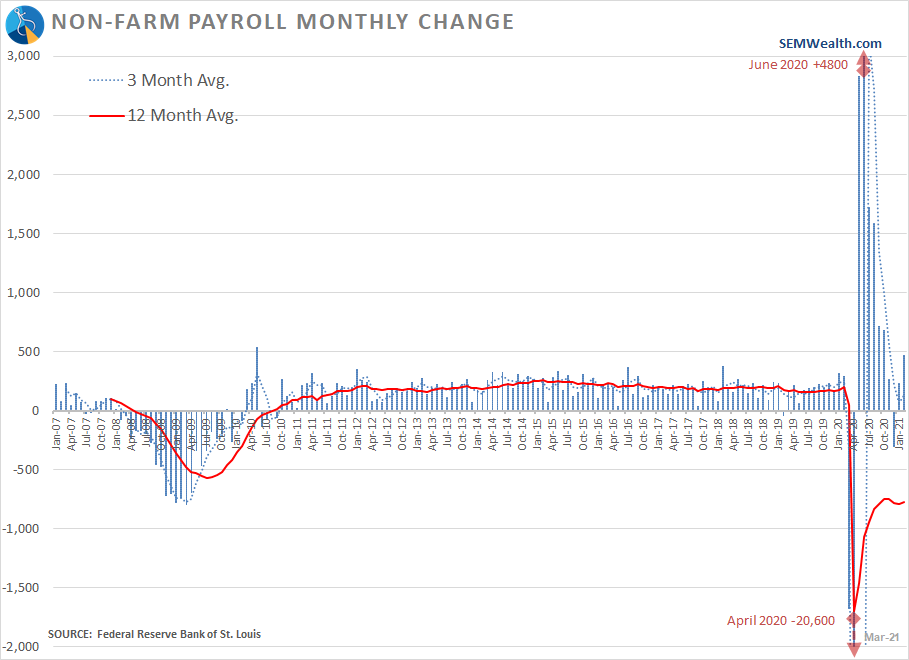

I wouldn't be called "Mr. Sunshine" if I didn't point out some concerns in the payroll data. First off, we still have a lot of damage to make-up. I truncated this chart so we could see the changes in the moving averages.

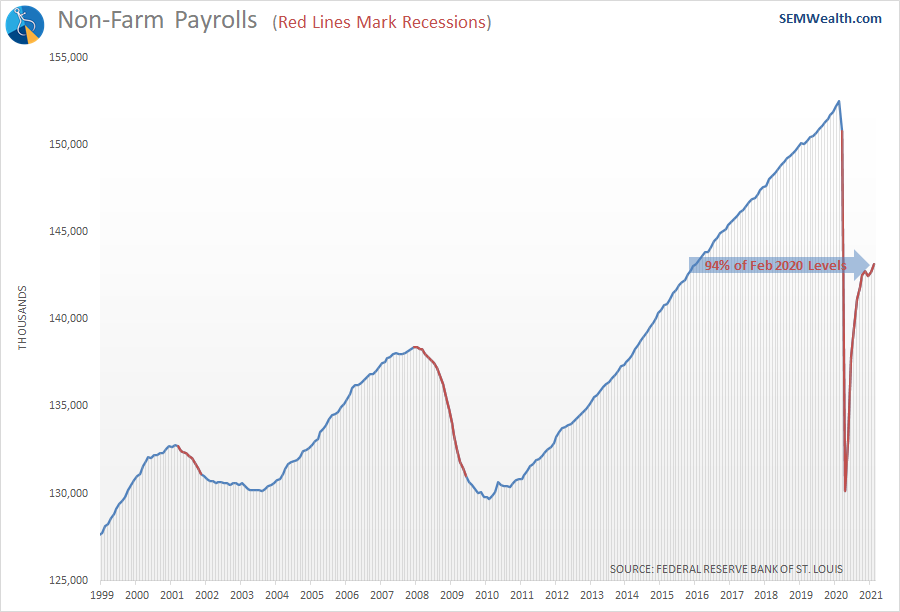

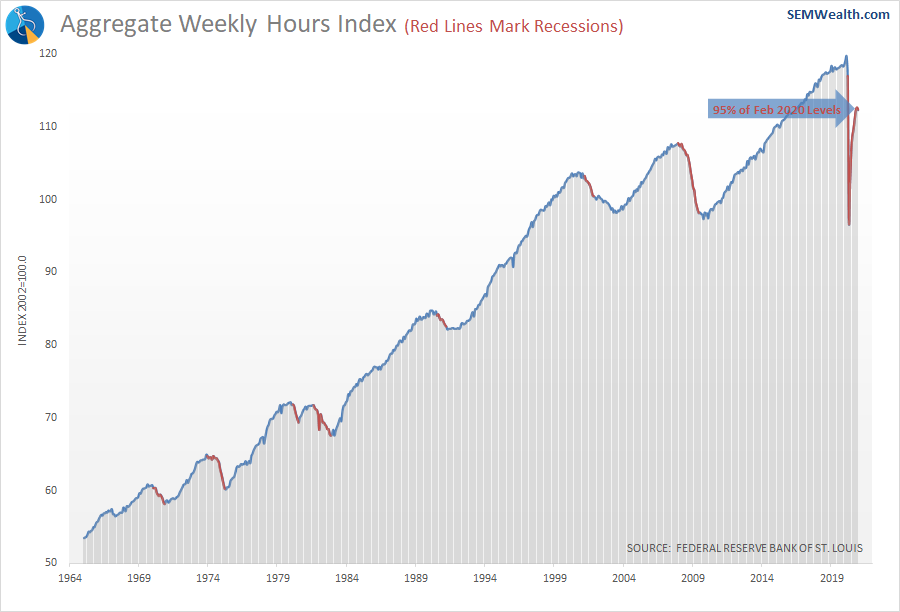

March 2021 was spectacular, but the 12 month average is still deeply negative. We are also still at only 94% of the peak from February 2020.

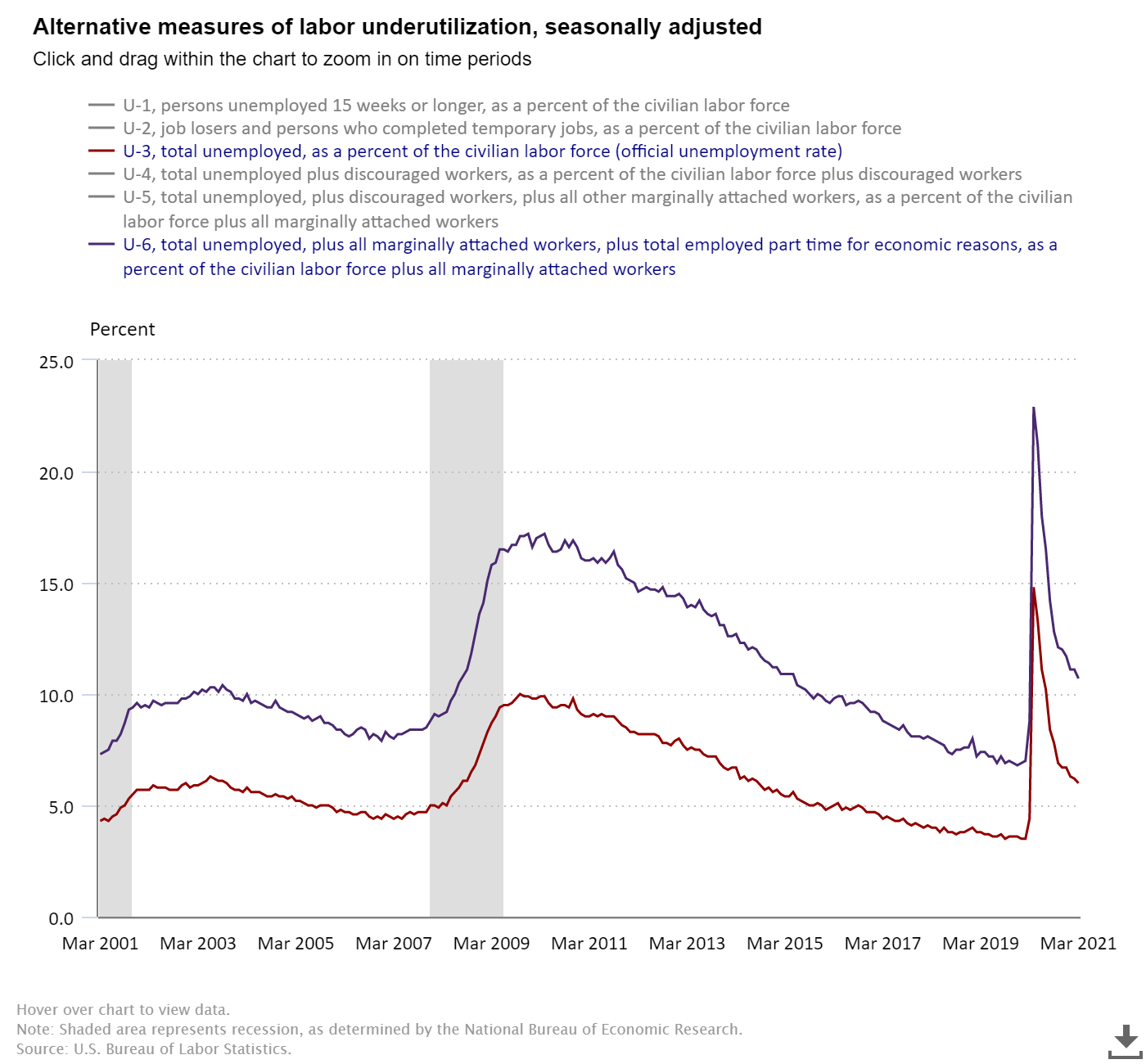

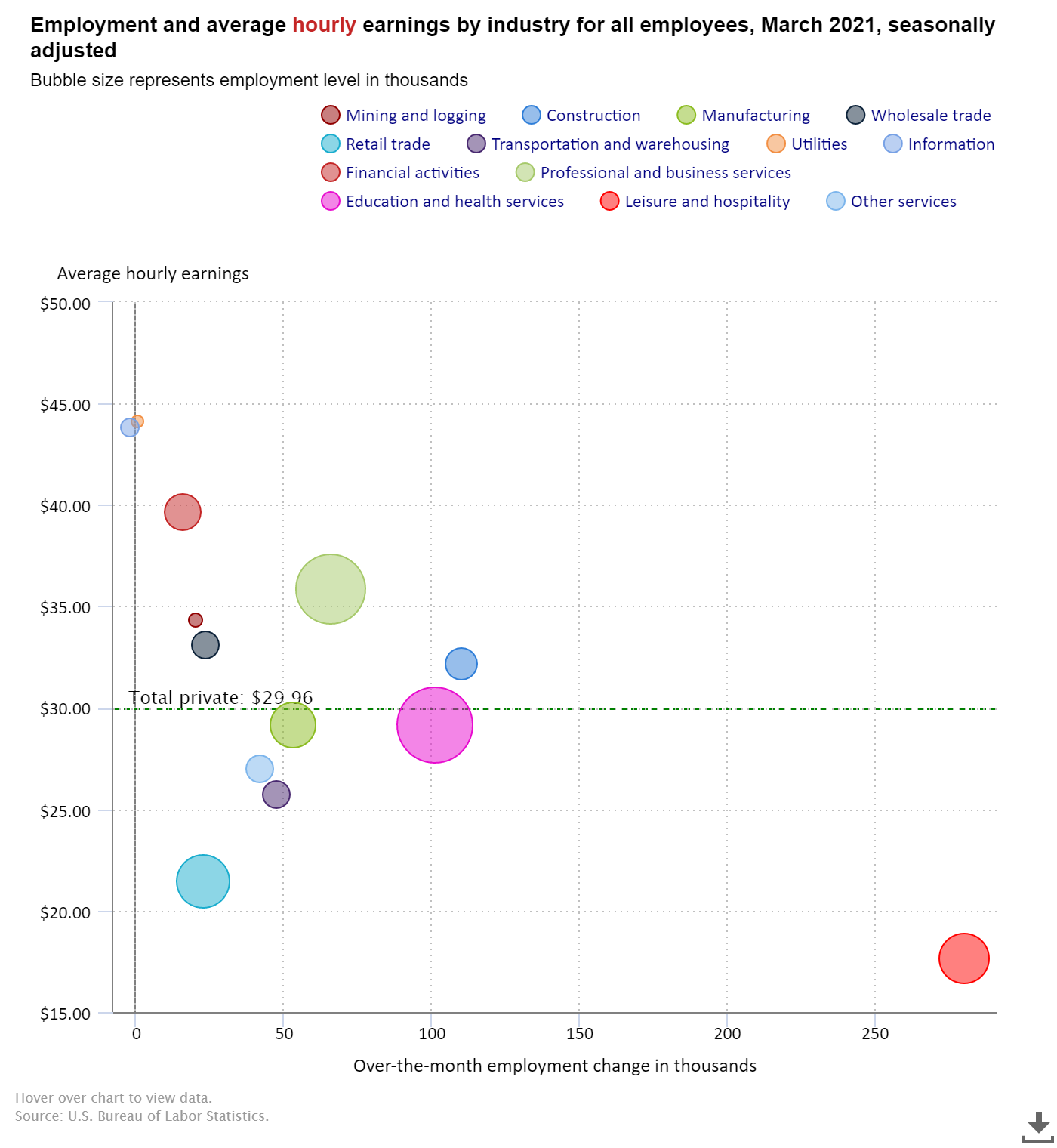

The official unemployment rate hit 6%, but the "real" unemployment rate is 10.7%. The "U-6" takes into consideration workers who have part-time jobs, but would like full-time along with those "discouraged" workers who dropped out of the labor force. For those people the crisis is still real and if not solved soon will become a bigger problem for our economy when things "normalize".

The bigger issue for our economy is the quality of the jobs. 30% of the new jobs in March were in the "leisure & hospitality" space, which pays just 59% of the average private sector job.

Those jobs also have fewer hours (which shows up in the U-6 number as well). The aggregate weekly hours index is one we'll be watching.

We have to keep in mind the "K-shaped" economy. While overall numbers may look solid, the stock market has priced all of this in. The market expects the economy to be better than it was by the end of the year, but as our readers know the economy wasn't that great for many Americans before the pandemic.

Jeff Hybiak, CFA

Jeff Hybiak, CFA

Manufacturing roaring back

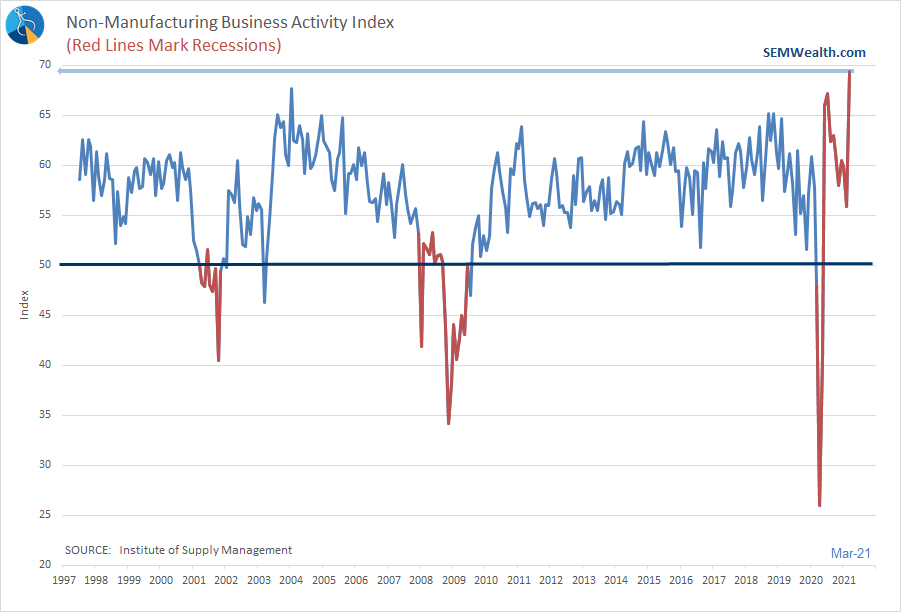

On the plus side, the manufacturing added 66,000 new jobs in March at an average hourly rate of $36. This also showed up in the Manufacturing Index for March, which hit its highest level since the early 1980s.

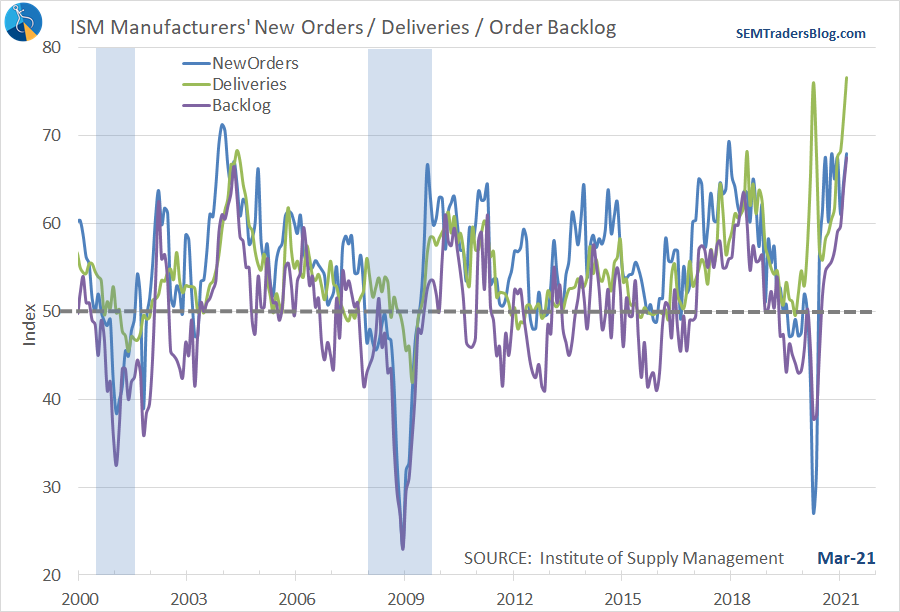

The internal characteristics were also quite strong, which should bode well for the coming months.

The service sector also posted it's best all-time reading in March.

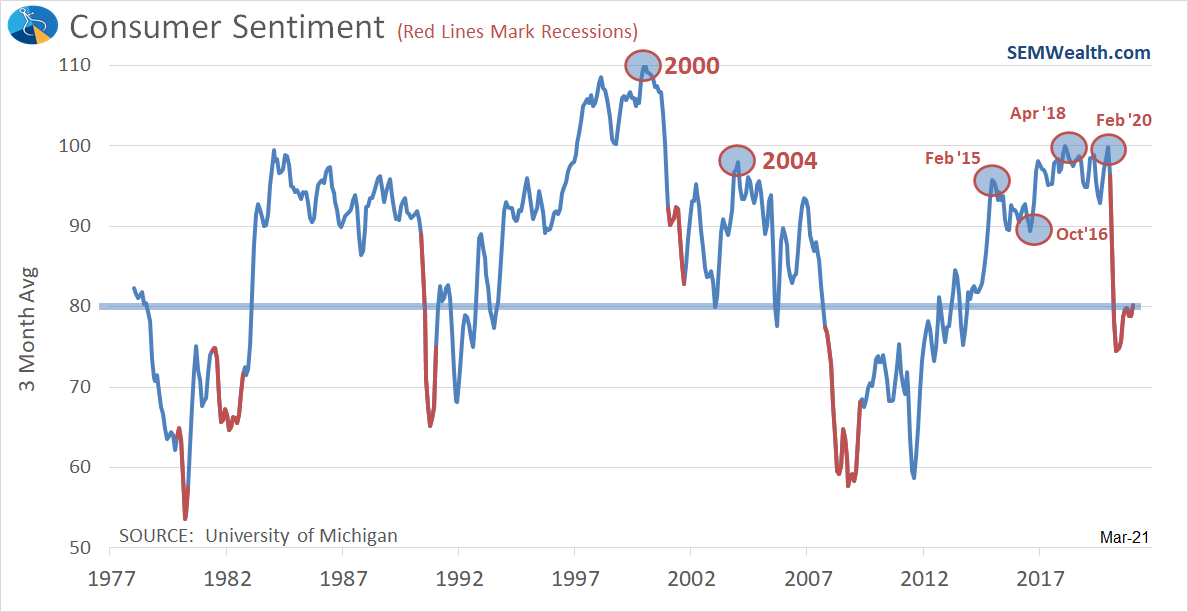

Improving sentiment, but.....

Consumer Sentiment also made a strong jump in March. That headline was encouraging, but it is still well below the peak in February 2020.

Our economy relies on consumers spending most (or all) of their income, so the market needs confident consumers. This chart in the coming months will be telling.

A lot can go wrong

Last week I took a look at the structural problems our country is facing. We cannot solve 40 years of dual deficits (government and trade) by a list of pet projects in an "infrastructure" bill. It's not the amount of money spent, but what it is spent on. It is a waste of money if it doesn't go towards:

- Increasing the labor force

- Increasing productivity

Our economic output over the long-term comes down to those items. Any money not used to INVEST in them means it will slow future growth, something the stock market (and pension funds, insurance companies, municipalities, etc, etc, etc have not priced in.)

Jeff Hybiak, CFA

A few weeks back I also gave you questions you should be asking as you work on your post-COVID investment plans.

Jeff Hybiak, CFA

I followed that up with 3 items not considered by most investors:

Jeff Hybiak, CFA

I'd encourage you to take some time to read those 3 articles. Everywhere I look I see euphoria. Don't get me wrong, I'm excited to see things moving in the right direction, but if everyone expects a "rocket ship" and it doesn't happen, the correction in stock (and bond) prices will be severe.

Bullish Mode

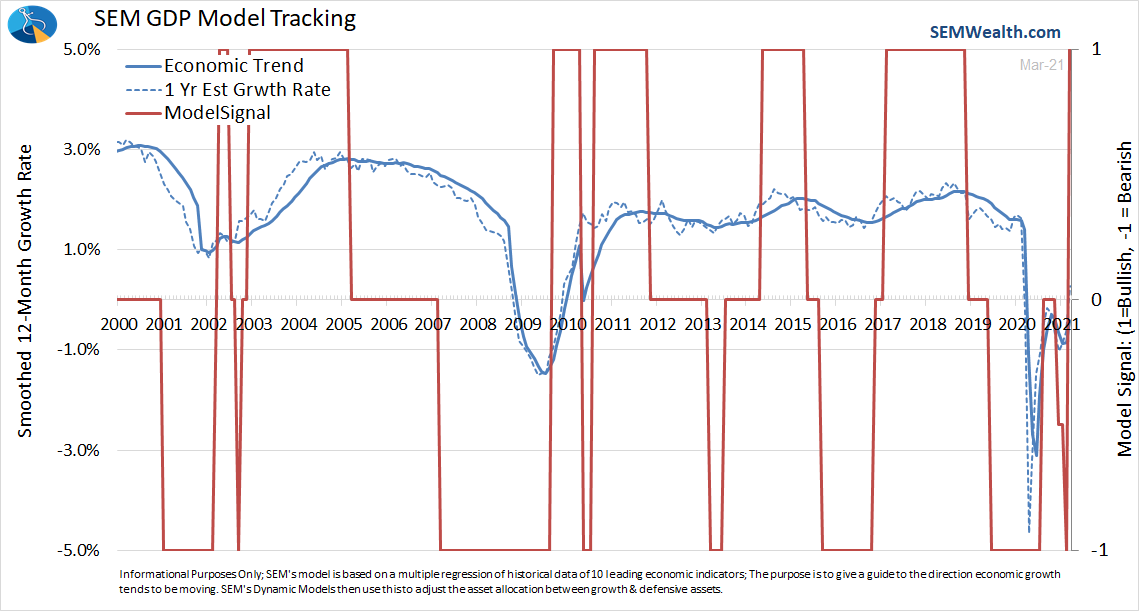

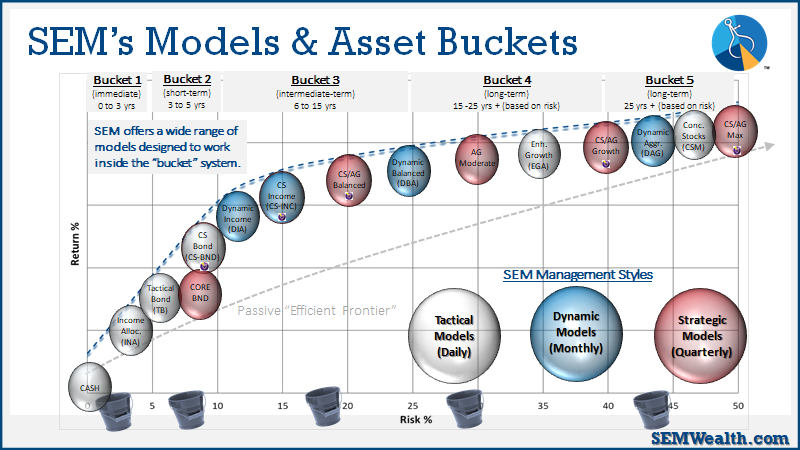

All of that said, our quantitative economic model is quite optimistic. The data from March mentioned above (sentiment, manufacturing, and payroll) led to a sharp reversal in the model. For our Dynamic Models this means higher risk bonds and dividend stocks on the income side, and more small caps on the aggressive side. Dynamic Income also adds a position in a Treasury "Bear" fund which makes money as Treasury yields go up.

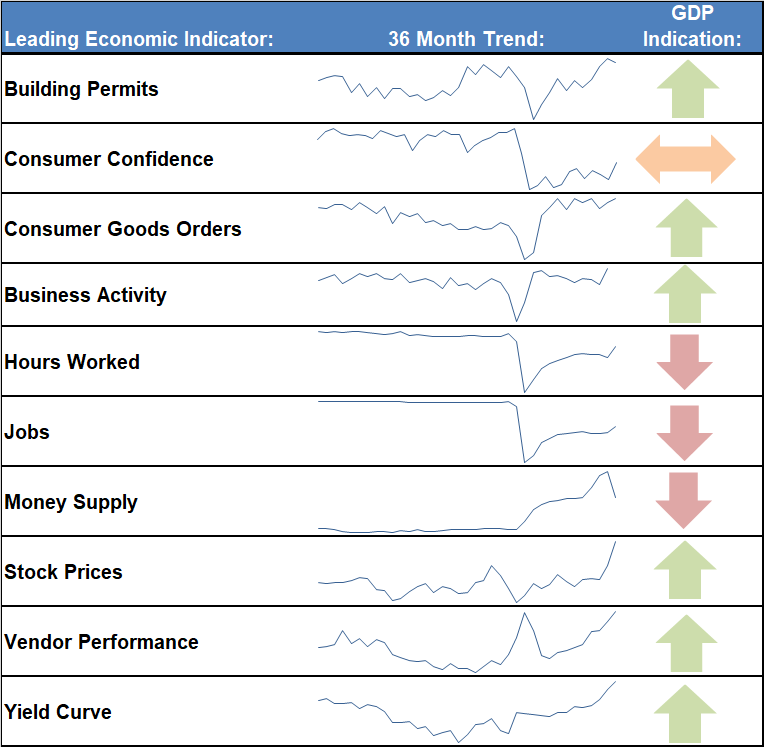

Here's our dashboard of indicators:

Our allocations in our "strategic" models (AmeriGuard and Cornerstone) also are continuing the moves they started in October – reducing the large cap growth stocks that served us well the first 3 quarters of 2020 and adding small and mid cap stocks. This quarter they are also picking up some large cap value allocations.

Our tactical models had reduced exposure in mid-March. Tactical Bond (TB) is back to fully invested in high yield corporate bonds. Income Allocator (INA) is also fully invested in higher risk bonds (high yield, emerging markets, convertible bonds) as well as preferred stocks. EGA remains skeptical due to the extreme overbought condition and high sentiment readings.

**For conservative/income investors: We continue to recommend a combination of our Tactical Bond (and Income Allocator) with Dynamic Income. The spreads and overall yield in high yields have gotten so low we are likely to be in a slow period. Adding Dynamic Income to the mix gives income investors an opportunity to make some income outside of bonds while still having risk controls. If you have clients who have thought the last few months in Tactical Bond have been "too slow", I'd encourage you to look at Dynamic Income. **

One thing that we should keep in mind, our economic model adjusts to the current environment. Extrapolating the numbers out, it is looking at a 12 month GDP growth number of around 2.5%, which is close to the average we've seen for the past 20 years. That's with nearly $10 Trillion of stimulus from Congress and the Fed. Most of that money will be gone in a few more months. With little reason to add more "stimulus" the economy may be left to stand on its own. Please do not take the "bullish" stance of our models as a sign to pour money into risky investments. These are all "trading" positions that may reverse at any point in the coming weeks or months.

This is the key advantage of using SEM — we all have our opinions. We all may get sucked into overly euphoric or overly pessimistic states of mind based on what is happening now. With SEM our 3 distinct management styles offer a way to put aside our emotions and focus on what the DATA says. Sometimes they all say the same thing, sometimes they disagree, which is why we almost always recommend having all 3 styles in a single portfolio.

I've been doing this for 25 years and do a lot of research on other managers (partially to learn where we can improve, but also because we will include other managers in our allocations where they add value). I have yet to see any manager offer the diversified line-up you get at SEM in a single account. Yes, some platforms allow you to pick your line-up, but that leaves too much up to you doing the research, optimization testing, and allocation decisions.

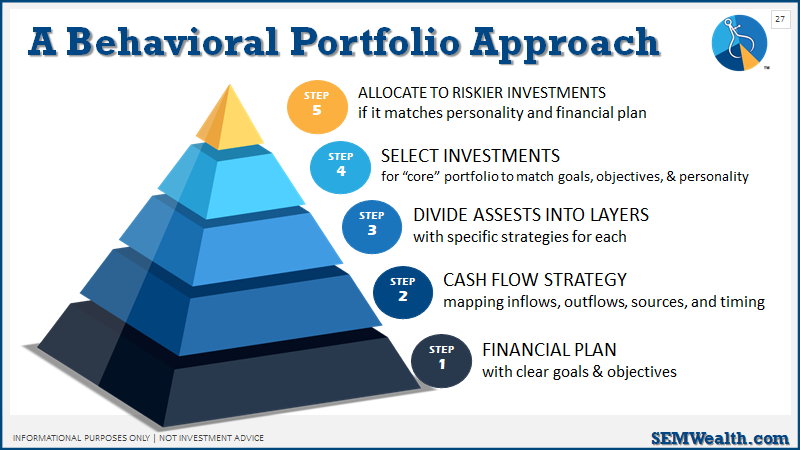

How you allocate, whether with SEM or not, shouldn't be a function of how you (or the experts) feel about the current environment, but rather as part of a well-constructed plan. The last year has proven the value of our behavioral approach. With out the bottom layers in place, your investment allocation will likely end up with issues at some point down the road.