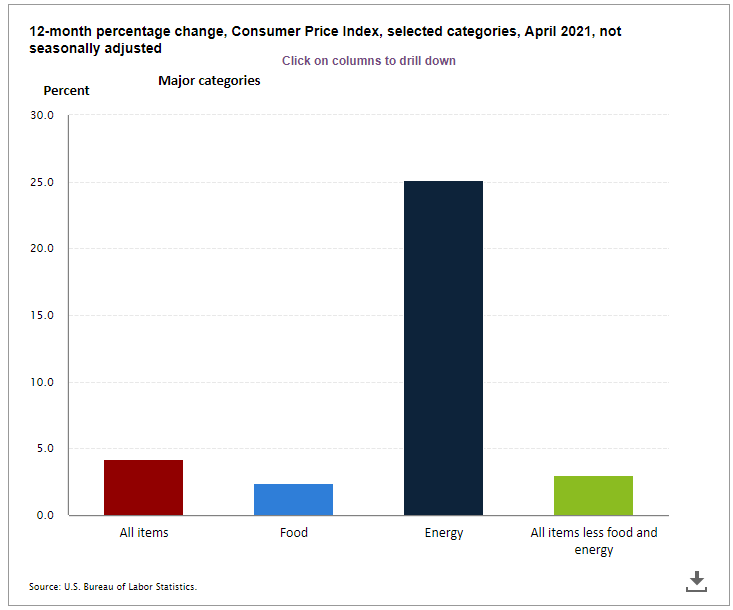

Based on the sensationalized headlines last week, one would think the market was at risk to give back all of its gains. This came on the heels of a much worse than expected inflation number on Wednesday. While "base effects" which is economists speak for what things looked like a year ago certainly had an impact, the 4% jump in inflation was even higher than the already high expectations.

The fear of course is higher than expected inflation will lead to the Federal Reserve pulling back some of their stimulus. I highly doubt that will be the case as Chair Powell has gone out of his way to ensure markets the Fed is ok with what they believe are going to be temporarily high inflation readings. The expectation is inflation will peak in May or June and then begin declining back towards the 2-3% level the Fed is comfortable with.

I won't bother going into the details of the report this month other than to show a chart that highlights changes in various components.

The gasoline panic in the southeast and mid-Atlantic states last week certainly won't help the upcoming numbers. On-going supply chain shortages may also play a role longer than the Fed is expecting. It is certainly worth watching.

I (virtually) attended the Mauldin Strategic Investment Conference every other day for the past two weeks. Unlike prior years, nothing has yet crystalized in terms of a short and intermediate term outlook. I guess that’s what happens when you have an unprecedented amount of money dumped into the economy by the government --- nobody knows what will happen, but they certainly have their opinions.

I think not having an opinion is ok. That’s why we’ve structured the portfolios the way we have. We have expert, experienced managers in the lower risk bucket and a diversified set of strategies in the medium and higher risk buckets. We use the financial plan, cash flow strategy, and investment personality to guide the client allocations – not our opinions. Blending that with investment models that also have no opinions couldn’t be more valuable at this point.

That said, risks are certainly quite high. Anything can spark a huge correction in stocks and bonds, but we could also see a huge melt-up in prices. I have my opinion and will be attempting to crystalize some sort of summary of the Mauldin conference in the coming weeks. I think most of you know my general assessment --- the use of debt to prop up the economy over the short-term is dangerous. Last week's inflation numbers could be a warning about the consequences of this, although I tend to think deflation is a much bigger problem over the longer-term.

One speaker in jest said this:

“The White House announced a $2 Trillion spending plan to study the reason today’s inflation numbers were so high.” - Louis Gave

He followed with:

"How do you know when a Fed stimulus program has failed? When they launch the next round of stimulus"

I've said for over a decade the Fed is playing a dangerous game. They could be approaching the end game if prices do not calm back down in the coming months. They are essentially funding the runaway deficit spending by purchasing 1/3 to 1/2 of all new Treasury issuance via their Quantitative Easing program. With stock and high yield bond valuations both near or above all-time highs, the risks of any Fed slowdown in stimulus could be met with mass selling.

We aren't quite there. The small panic last week was severe, but the market has been in a tight range for over a month. Friday's big rally took it back to the mid-point for the last month.

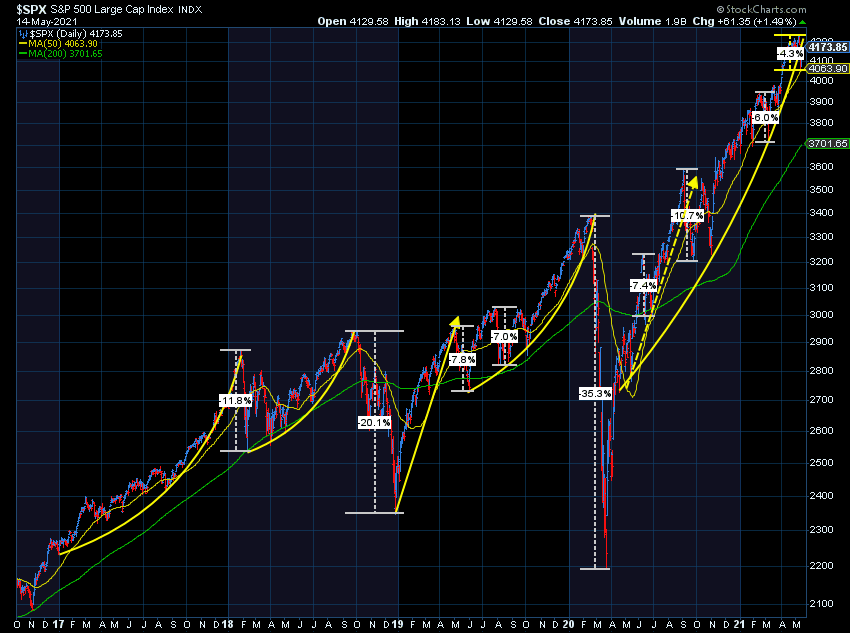

To really put it in perspective, here's the updated parabolic move chart I've used throughout the last several years.

The pattern is clear — we get a move that goes "parabolic" followed by a large sell-off. We clearly are due for another one. It could start at any time.

Our models remain nearly fully invested. We did trim a small amount (around 10%) of our high yield bond positions in Tactical Bond last week and our Enhanced Growth Allocator model has been "bearish" for over a month with just 25-35% exposure to stocks. The other models remain "bullish"

As we learned in 2020, it is impossible to predict what will cause the market to fall. Whatever it is, if the market is at stretched valuations, the losses can be far greater than most of us believed were possible.