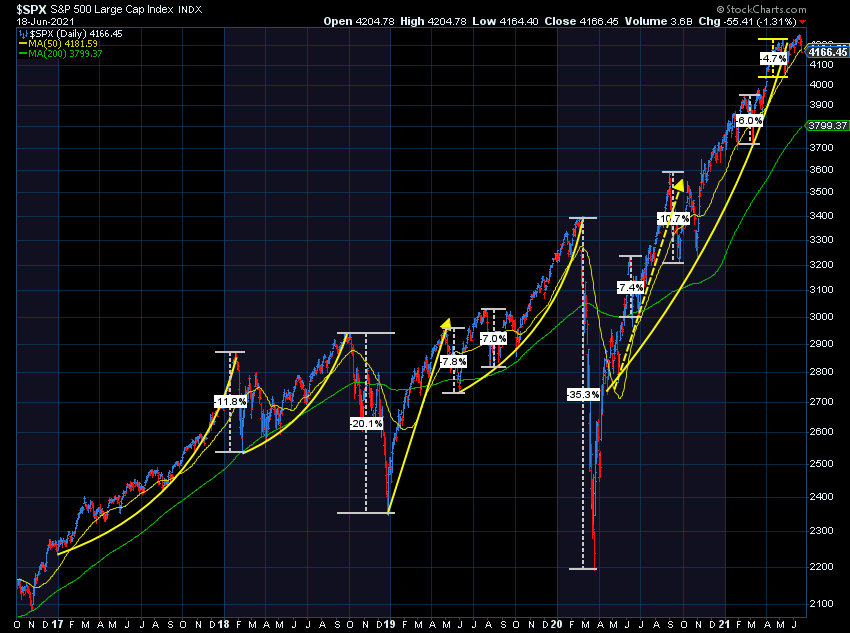

Summer is officially here and based on the weekend traffic, the lines at the grocery stores, the lack of inventory in the summer aisles at Target and Wal-Mart, Americans are out and about in full force. At the same time the stock market has stumbled, which begs the question, 'why would the market struggle when the economy appears to be so strong?'

The answer really comes down to the market already pricing all of this in. Stocks staged a ferocious rally starting in the spring of 2020 despite the economic lockdowns. The rally has continued in 2021.

The parabolic move was based on 4 Pillars, which we've been outlining throughout the year. In the last few weeks, we've seen some cracks emerging which have caused stock investors (speculators?) reconsidering what is in their portfolios. Let's take a quick look at each:

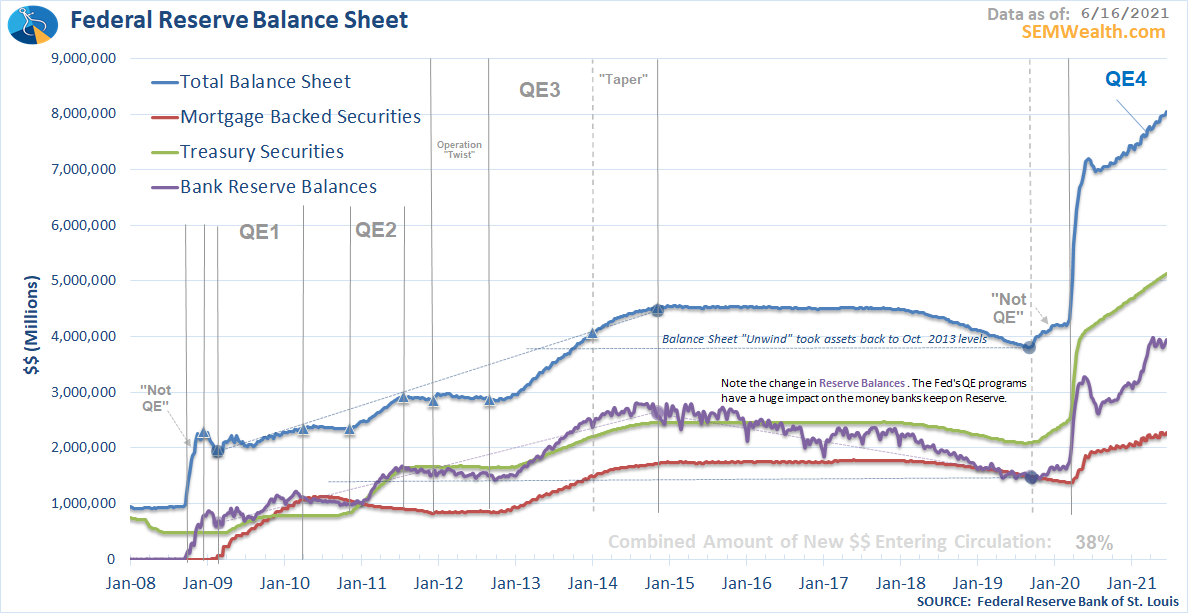

1.) Federal Reserve Support

This one took the biggest hit last week following the Fed's latest policy meeting. The "dot-plots" which are the projections of all the Fed members showed expectations of two rate hikes in 2023 (versus 1 after the last meeting). Other projections also shifted, which led the market to start looking at the end of the Fed's QE programs by the end of this year. The language around inflation and ending stimulus programs also shifted, with Chair Powell saying they are "talking about talking about" how to unwind these unprecedented programs. Throughout the year, he had said the Fed wasn't even "talking about talking about" an unwind. While subtle, it was enough for the market to become concerned.

They should be concerned. The Fed currently owns 18% of the US debt. Just since March, the US has added $66B of new debt, yet the Federal Reserve has purchased $164B of Treasuries, meaning they have been been financing the rollover of maturing debt as well as buying other Treasury issues from the Wall Street banks. Tapering QE and eventually ending it does not mean the market cannot rally, but it does mean it will have to stand on its own, something it may not be ready to do.

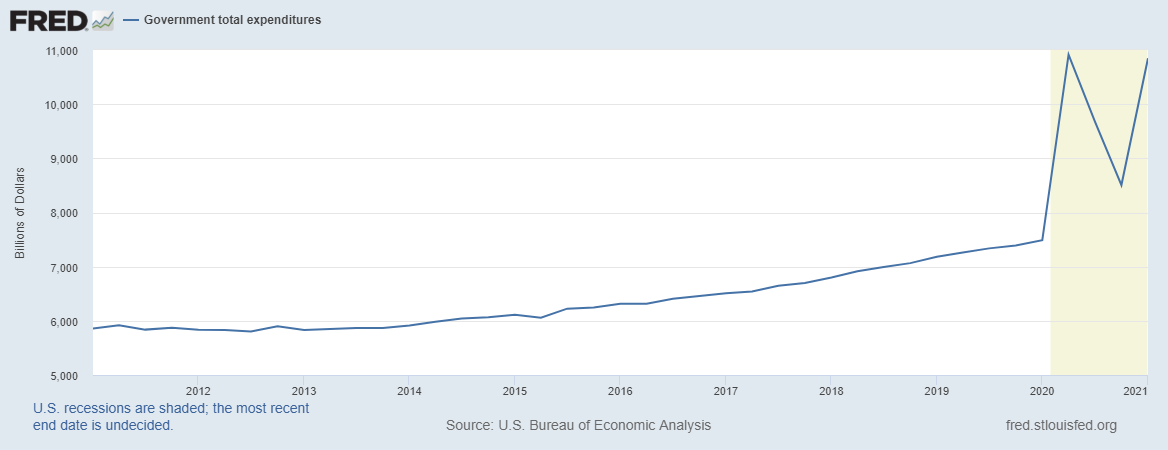

2.) Congressional Spending

I won't pretend to have any ability to predict what will happen in Washington. I do know the chances of President Biden getting his $5 Trillion + in proposed spending (investment?) bills through Congress are close to zero. Republicans have proposed logical ways to help pay for them (such as increasing the gasoline tax, which hasn't been indexed to inflation), but that would technically violate the President's campaign promise to not raise taxes on those making less than $400K per year. Raising corporate taxes or doing too much to tweak the capital gains tax could cause a short-term shock to the economy and markets. This would also put moderate Democrats at risk and possibly swing the House and Senate over to Republicans in the 2022 mid-terms if the economy is struggling next summer.

Spending will likely not exceed the peak in the second quarter of 2020, but it also will not settle back down to the longer-term pre-COVID trend.

Either way, something I've challenged people who are overwhelmingly optimistic is this question — do you think Americans will receive more or less in stimulus checks over the next 6 months compared to the second half of 2020? I think the answer is obvious, which means there will be less free money in Americans' hands. This doesn't mean the market cannot rally, but it does mean it will have to stand on its own, something it may not be ready to do.

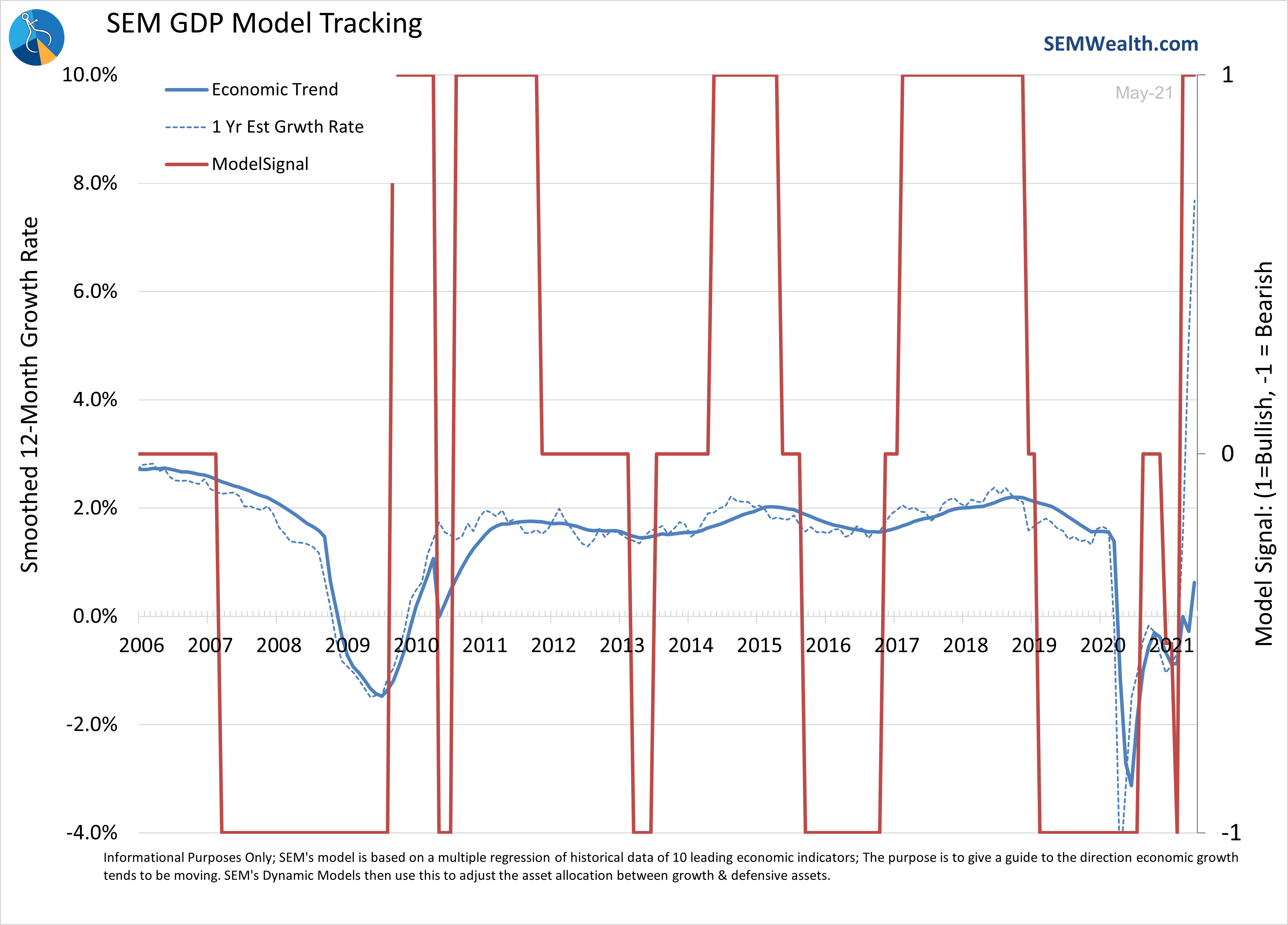

3.) Improving Economy

I've spent the last few Monday Morning Musings discussing the economy. Our quantitative economic model is still saying the economy is strong, but in addition to reduced benefits from the two pillars above, we have the question of how much inflation will weigh on economic growth, what the "new normal" looks like, and how much of a boost will the summer reopening bring to the economic numbers.

For a more in-depth look at the economy, check out the link below:

Jeff Hybiak, CFA

Jeff Hybiak, CFA

One of my favorite leading indicators, building permits have slowed a bit in recent months. This may be temporary, as we may see continued strong demand from Millennials entering the housing market over the next 5-7 years, but the economic boost new homes bring cannot be ignored.

Whether the housing market slows or not, the more immediate question is what happens AFTER the summer is over. Obviously most people had their vacations cancelled in 2020. They were able to use their stimulus checks to upgrade their homes, buy cars, and spend on other items, so they may still have some extra money in the budget to spend. After Labor Day, we should have a better gauge of real economic activity. Those who couldn't work due to child care issues should be able to return to work, the extended unemployment benefits will be over, and as I said in item 2 above, there won't be stimulus checks arriving every few months (other than the pre-payment of the child tax credit on a monthly basis from July - December).

In other words, come September, we'll have a better idea of whether or not the economy is able to stand on its own.

4.) COVID Cases / Vaccine Distribution

I know anytime we discuss COVID we risk getting political. For what it's worth, I'm an Independent so have no dog in this fight. I try to base anything I say on data and research. As expected the distribution of the COVID vaccines has helped reduce COVID down to manageable levels in most parts of the country. This has led to pretty much the whole country being open with fewer (if any) restrictions.

The number of Americans receiving the vaccine is far below what scientists have said would help stamp out COVID completely. Already we are seeing the "Delta" variant (the one that originated in India) cause severe problems in other countries. It is also now showing up in the US. This is worth watching.

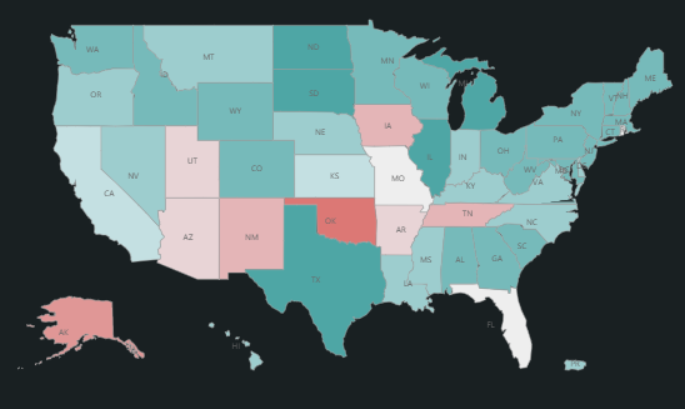

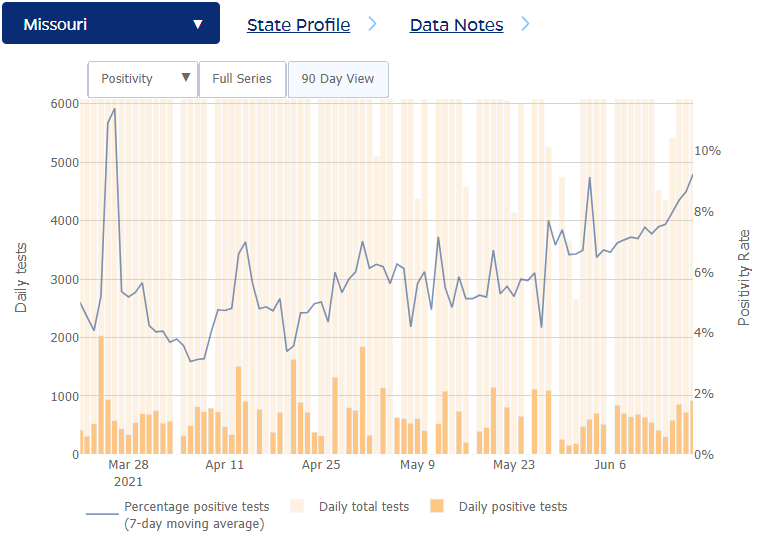

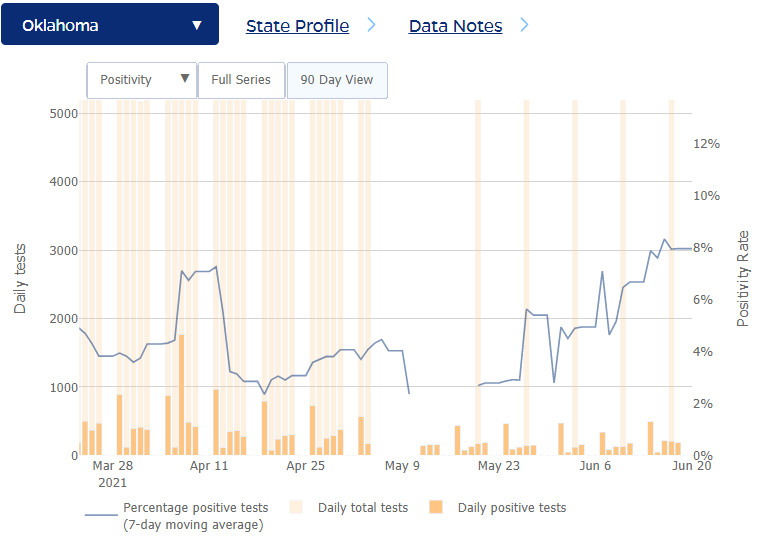

Cases have already been increasing in parts of the country.

So far, most states positivity rates are below the 3% level scientists have used to indicate the need for restrictions. Missouri and Oklahoma for whatever reason are outliers, with both approaching a 10% positivity rate.

I think it's safe to say we are all fatigued and don't want to regress back into restrictions on businesses, activities, and personal freedom. From an economic perspective, I think it's safe to say this would damage the economy meaning. Whether or not the market could withstand a fall return of COVID restrictions would depend on how much economic damage the restrictions would cause and how quickly the Fed and Congress would jump in to try to save it.

What do the cracks mean for our investments?

At this point, nothing has changed. While some of our models are growing cautious, all remain at or near maximum bullish indications. Remember, we follow the data, not anybody's opinions (including our own). If the big market participants start growing concerned about these cracks, it will show up in the data, and our models are designed to pre-emptively get out ahead of them.

Just as we illustrated during COVID, the 2011 Debt Ceiling Circus, the Financial Crisis, and the 2000-2002 Tech Crash, we ignore the noise and can quickly shift from bullish to bearish in our positioning.

If you have money outside of SEM and especially if you are retired or planning on retiring in the next 5-10 years, I would encourage you to take our free financial check-up to ensure your money can withstand any additional damage to the pillars that have been holding up the market.