For too long, investors (speculators) have relied on the Federal Reserve to prevent any and all economic speed bumps to keep stock prices propped up. The so-called "Fed Put" just celebrated its 25th anniversary on Saturday. Not sure what I'm talking about? If you have a WSJ Subscription you can read the Barron's article from September 28, 1998 describing the bailout here.

The Cliff Notes version – a relatively unknown hedge fund named Long Term Capital (LTC) placed currency bets using money borrowed from several big name Wall Street banks. The Wall Street banks had no idea how much money LTC had borrowed from their brethren to purchase currency swaps (with no collateral) or how big the bets were. When the bets went against LTC they had no money to repay these loans. Oh by the way, thanks to recent deregulations, the Wall Street banks also were investors in the LTC, so they were wiped out on both sides.

As fears of contagion among the Wall Street banks spread, the Federal Reserve secretly met to arrange loans to LTC so LTC could in turn pay back the banks and returns some money to their investors (also the Wall Street banks). The so-called "Greenspan Put" was born (now known as the "Fed Put").

A Put option is a contract to protect against losses, so the Fed Put assumes the Fed will step in at a certain price to save the stock market from further losses.

I've discussed this countless times in this blog about the dangers of trusting the Fed to always save the economy. First and foremost, the fact the stock market has lost 50% TWICE since the Greenspan Put was born

The Fed Put has most recently been put in play during COVID following a 35% drop in stocks – more on that later.

Last week the Fed did not raise interest rates, which somehow "disappointed" investors (speculators) because Chair Jerome Powell emphasized the Fed's inflation fight "had a long way to go." Chair Powell and his merry band of Fed voting members released projections showing interest rates are likely going to stay "higher for longer" than most people expect.

Dichotomy of Expectations

The stock market (or at least growth stocks) have had a great year. This has been on the backs of these expectations:

1.) The economy will continue to grow throughout 2023 & 2024 (along with corporate earnings)

2.) Inflation will come back down to "normal"

3.) The Fed will cut rates in 2024

The problem with these expectations is they do not make sense. #1 & #2 are certainly possible and would be good for stocks, but why in the world would the Fed cut rates if the economy was still growing? Even with a Fed put, we've seen they only cut interest rates when the economy has slowed significantly. With stock valuations at or near all-time highs, there is no room for any type of slowdown.

Based on the reaction in the stock (and bond) market, there was a lot of hope baked into #3.

The chart of the S&P 500 tells the story. The market is barely below recent 'support' levels around 4325 & needs to get back above there soon. From a technical perspective this looks like a "head & shoulders" pattern, which is a dangerous topping pattern when a market has a "blow off" top. A confirmed breakdown below 4325 would take the S&P down to around 4000 (minimum).

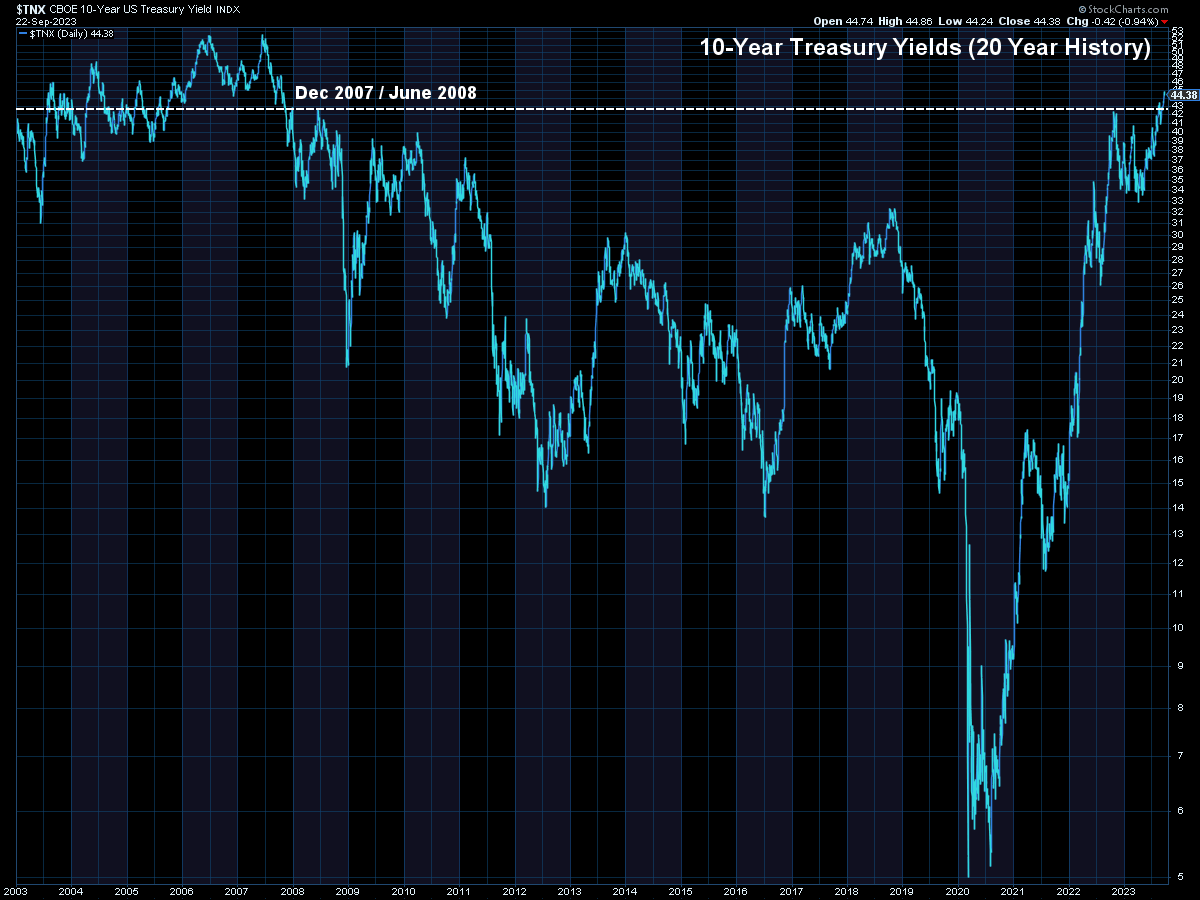

The bond market reacted even more negatively, with yields blowing past the high points from August and last October.

Interest rates are now at the highest levels since September 2007!

Broken Economy

I've been spending a lot of time with advisors and their clients explaining the current economic and market environment. It is important to take a step back and look at what has happened the past 3 or 4 years. The Fed and Congress broke the economy in three directions, causing big disconnects in what is "normal".

1.) Economy was shut down to beat COVID

2.) Congress & the Fed added 50% of GDP output to the economy in less than 12 months.

3.) The Fed hiked rates at the fastest rate in 40 years to fight inflation.

I discussed this in a series of videos last year:

We are now 'normalizing' and that is not a good thing if you are betting on stocks (and the economy) to continue ramping higher without any big losses. Prior to COVID our economic model was "bearish". Our economic indicators were slowing rapidly & things were breaking in the financial system. The triple 'breaks' by the Fed & Congress are only causing more issues beneath the surface.

I've been talking about my "forest fire" analogy quite a bit lately. Recessions are necessary "cleansing" events to wipe out the excesses. The bailouts by the Fed & Congress only create more fuel for an event they cannot prevent.

We're not fighting a 'Common Enemy' this time

One of the things I often remind people who trust the Fed (and Congress) to always bail the economy out is the only time this type of coordinated effort has happened has been when Americans were fighting a "common enemy".

- 9/11

- Financial Crisis (eventually)

- COVID

The other thing I remind people about is the scary losses which occurred before Congress and the Fed got together to "rescue" Wall Street (and the stock market). Two 50% losses in 2000-2002/2007-2008 and another 35% drop in 2020. In every period the losses came a.) before a 'crisis' was apparent and b.) continued after the 'bailouts' were eventually agreed upon.

Looking ahead to the rest of the year and into 2024, what is the 'Common Enemy'? Our country seems to be more divided that we were in 2020. Congress is more dysfunctional (as we are witnessing with the Republicans reneging on the deal they made with President Biden to raise the debt ceiling). I would not want to be holding out hope Congress would bailout Wall Street or the economy next time around.

I'm not saying a 'failure' is inevitable or looming, but I do find more and more people believing nothing bad can happen, which makes me worry that something bad could be on the horizon.

SEM Model Positioning

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

Tactical (daily): The High Yield Bond system which bought the beginning of April remains very close to a sell (again).

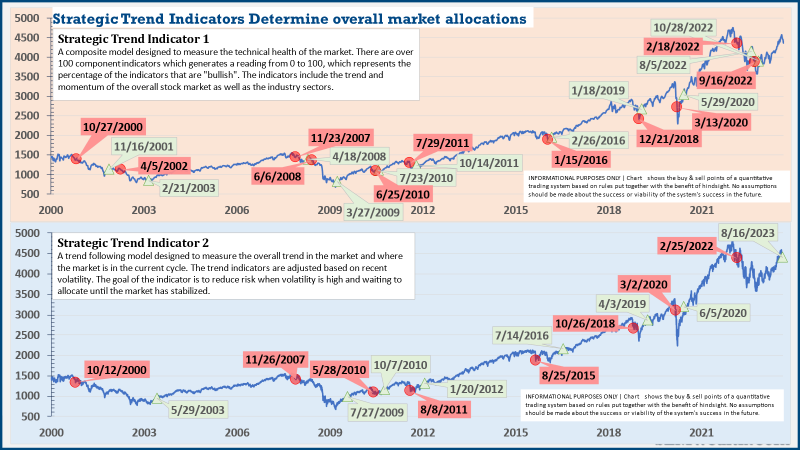

Dynamic (monthly): As we've been since April 2022, our economic model remains "bearish". This doesn't mean we are predicting a recession, but rather a slowdown which means a difficult environment for corporate earnings. Other than the technology and discretionary sector this has been the case.

Strategic (quarterly)*: The core rotation is adjusted quarterly. On August 17 it rotated out of mid-cap growth and into small cap value. It also sold some large cap value to buy some large cap blend and growth. The large cap purchases were in actively managed funds with more diversification than the S&P 500 (banking on the market broadening out beyond the top 5-10 stocks.)

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The second indicator triggered on August 16, brining the strategic models to a fully invested position. We are NOT locked into these for the next quarter. The 'sell-point' for this system is down around 3-4% from here.

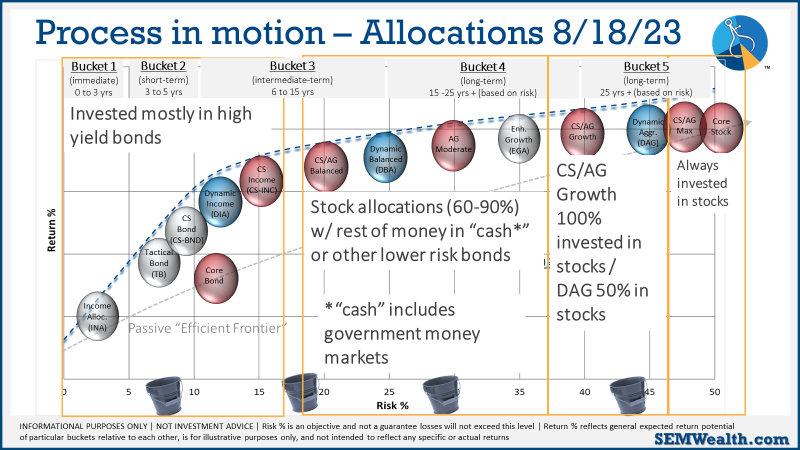

This is the beauty of SEM's truly diversified approach. You get 3 distinct investment management styles inside one portfolio. We can customize models to match nearly any objective, risk level, and investment personality.

Our "bucket" approach allows for different parts of the portfolio to be positioned differently based on where we are in the market cycle. Whenever we are at a crossroads moment it is especially risky. This requires a disciplined approach which is what SEM brings. There will be much easier times to invest. Our goal is to get there with as much capital in tact to take advantage of that opportunity.