AI mania is back in the stock market as technology stocks continue to roar back after stumbling at the start of the year. The concerns over whether or not the hundreds of billions of dollars being spent on data centers will turn into actual revenue seems to be non-existent. Software stocks who were hammered over concerns that AI models would replace the usefulness of their products have been leading the charge. Once again, the market is acting like there is no risk in chasing stocks as they once again hit all-time highs.

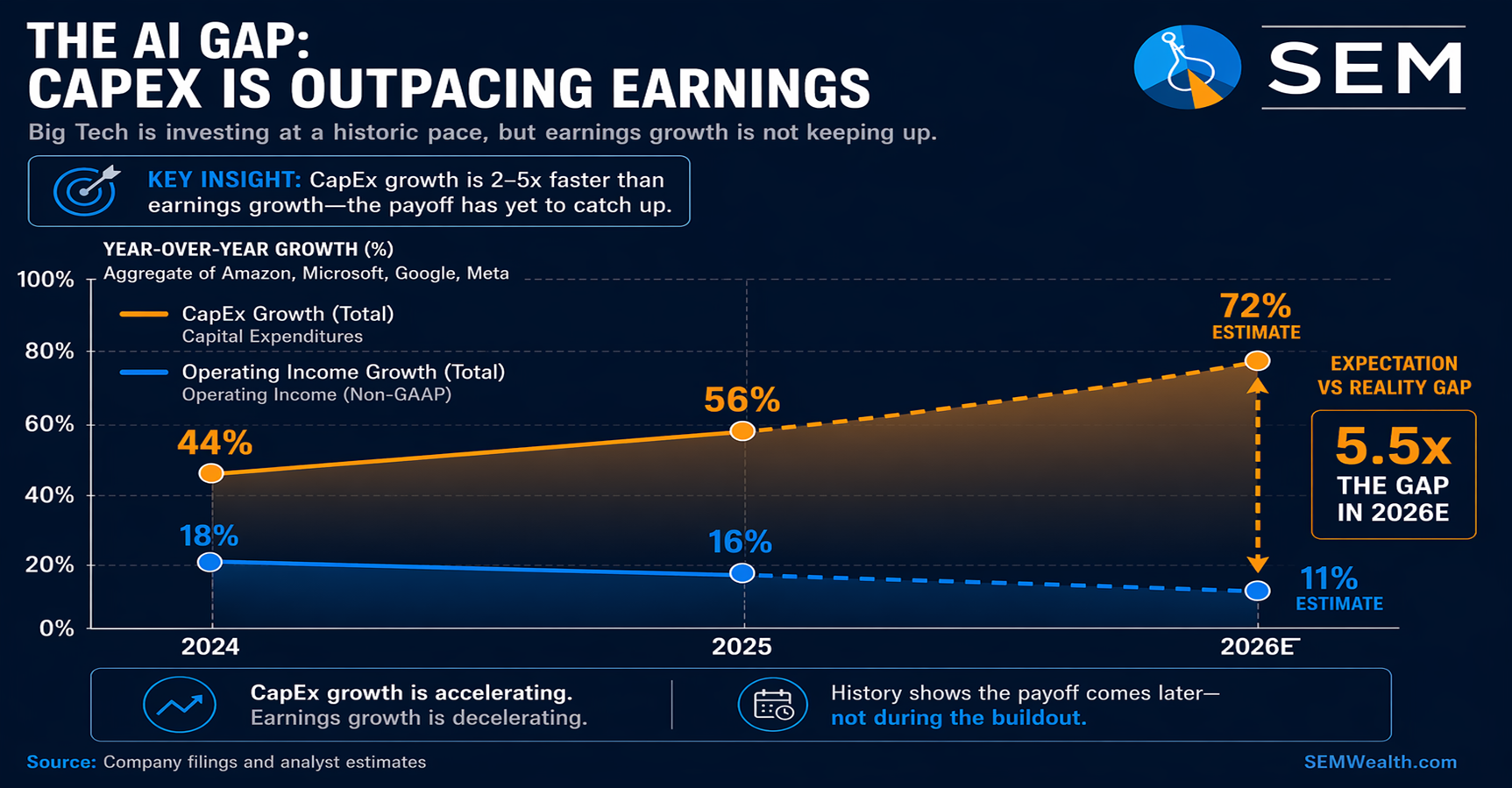

The amount of money being spent is staggering. The "hyperscalers" (Amazon, Alphabet (Google), Meta (Facebook), and Microsoft) spent nearly $350 Billion on data centers last year with plans to significantly increase that spending over the next three years. The question is when/if that turns into enough revenue to justify it as they all accelerate their investments in an attempt to beat their competitors.

The issue is, earnings growth is actually slowing for the hyperscalers which could be a problem.

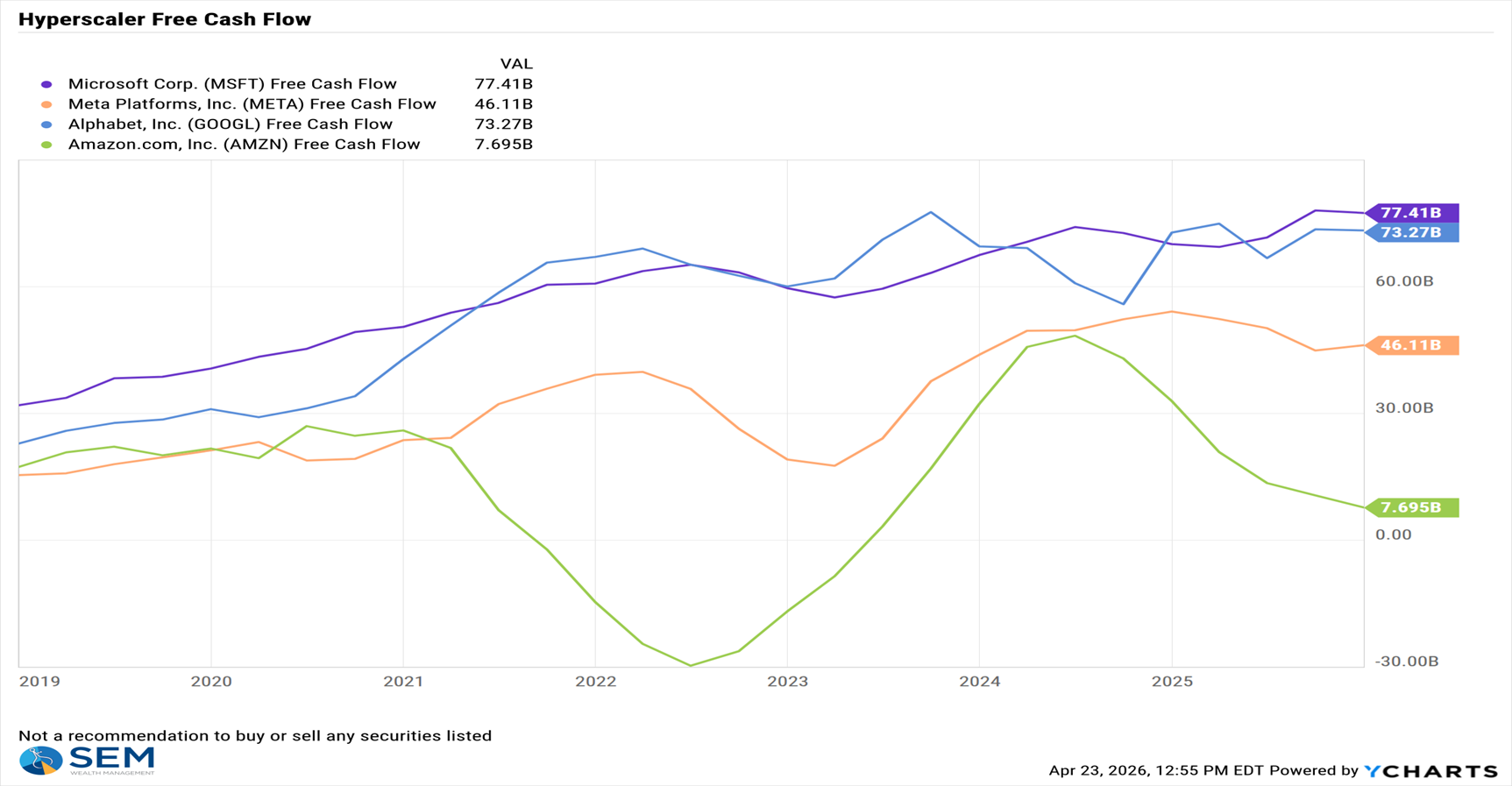

Right now, 3 of the 4 hyperscalers are generating enough cash flow to cover their planned 2026 investments (as measured by "free cash flow", which is calculated by subtracting capital expenditures form operation cash flow). Amazon will not and recently had to borrow $50B via a bond offering, yielding around 6.5%. While that is a relatively low amount, that is a new development for the AI buildout.

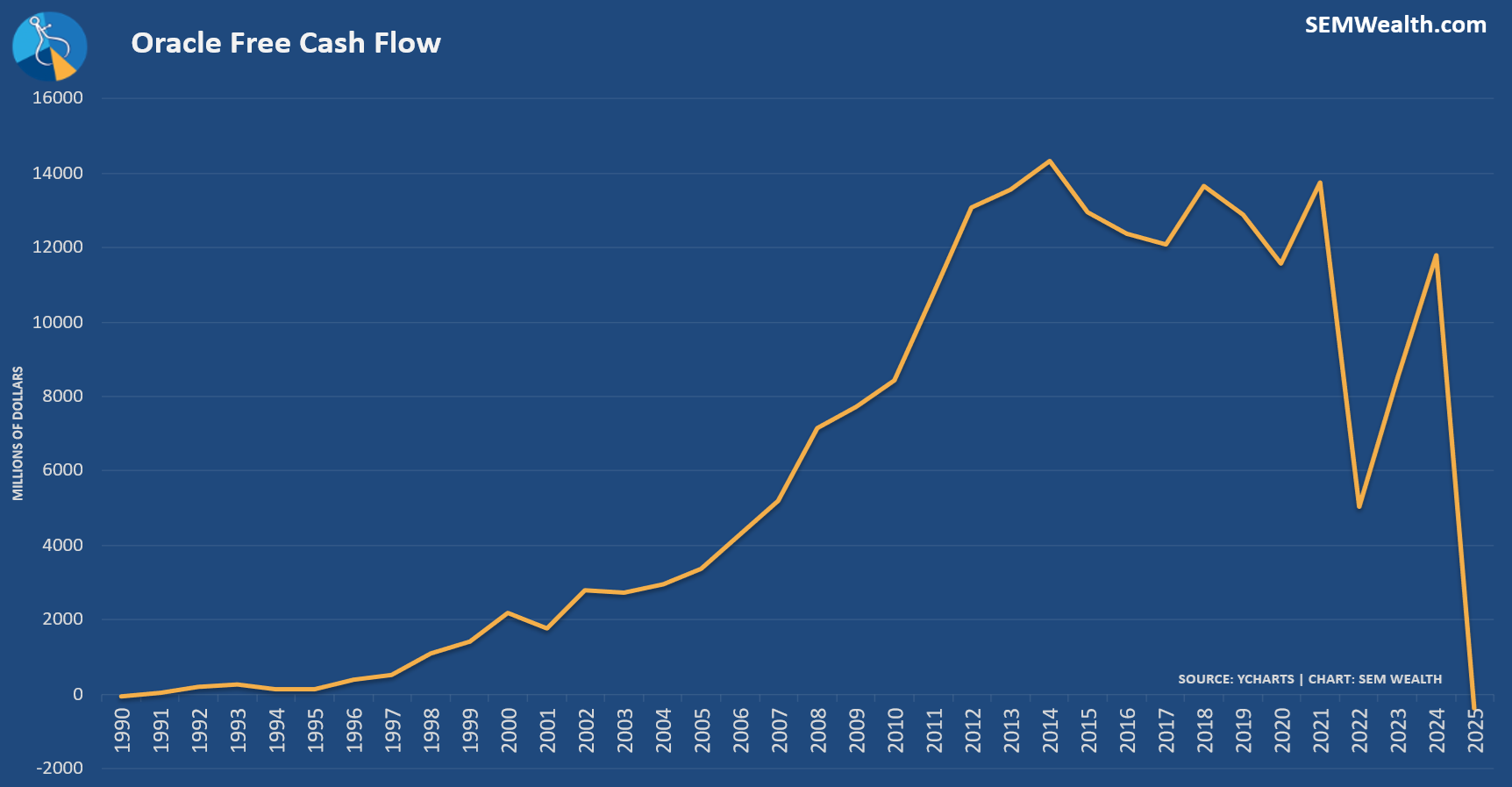

Based on current Free Cash Flow, Meta may be next in having to tap into the bond market to cover their planned investments. While not considered a hyperscaler, the company actually helping build the data centers, Oracle, has run into a much bigger problem. They are having to borrow to cover the construction costs with major questions about how much revenue they will earn.

For the first time since 1990, Oracle's Free Cash Flow is now negative.

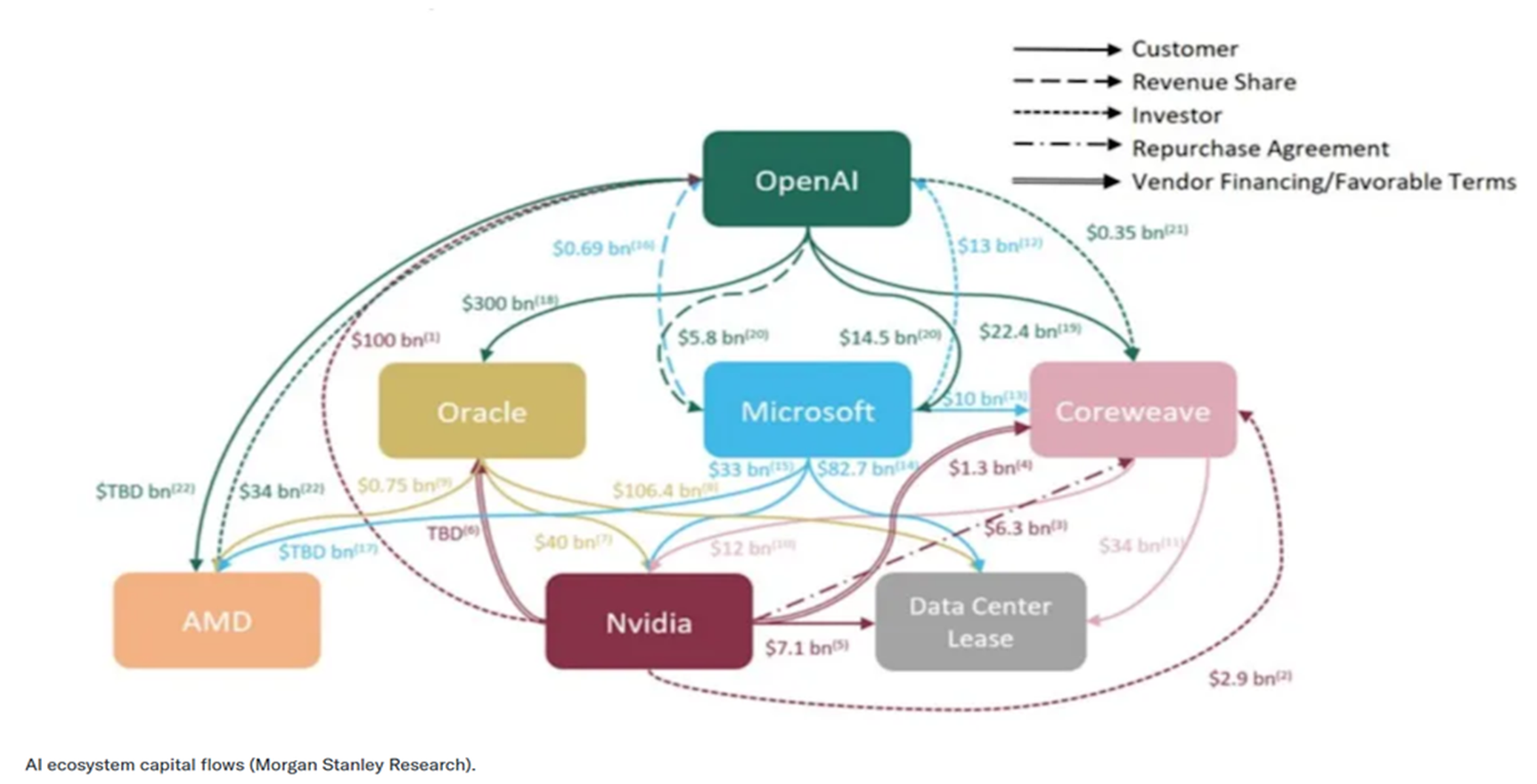

The issue Oracle is facing when it comes to borrowing more money is the regulations banks and other financial institutions have when it comes to counter-party exposure. This comes back to this diagram I've been sharing since last fall.

The problem: For most of the data centers being built, Oracle is the primary tenant, with OpenAI as the secondary tenant. Banks now have too much exposure to these two companies to lend them much more, which threatens their ability to fulfill the backlog of orders they've taken. With the now well-publicized problems in Private Credit, that funding source is also limited. Not being able to build more data centers limits Oracles revenue which threatens their ability to service their debt. This is something we will need to continue to monitor.

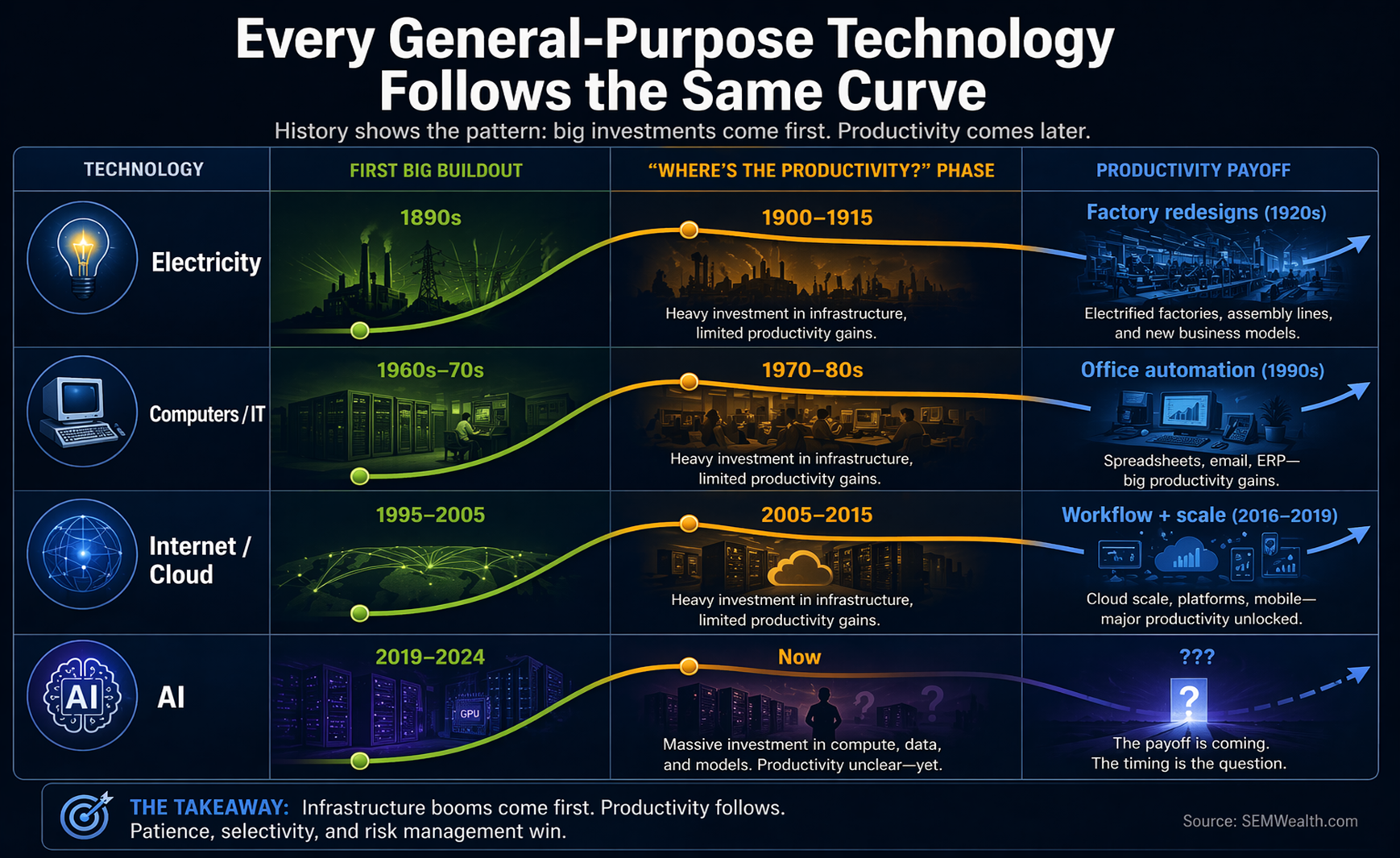

On Tuesday I'll be presenting my theme for 2026: AI: Boom, Bubble, or Both to the FPA of Maryland. One of the things I've been quite vocal about is the fact we can be right about the productivity boost this exciting new technology will bring, but wrong in the timing, the winners (and losers), and the actual payoff. I put this image together with ChatGPT describing the technology/innovation cycle.

By all accounts we are nearing the problematic phase – we've spent all this money, but haven't seen the payoff. Some companies will fail while others will emerge as the (eventual) winners. While we are living in the moment it may not be obvious when the lack of revenue starts to matter to the stock market. This is why we follow an unemotional, data-driven approach. As noted in the SEM Market Positioning below, we are aggressively positioned to continue participating in this rally. The key difference is we stand ready to take risks off the table if the data indicates a tougher market is coming.

News to Watch

This week we have several key events that could move the market:

Wednesday

- Fed Rate Decision and Press Conference

- Hyperscaler Earnings (after the close) – Microsoft, Amazon, Alphabet, and Meta all report on the same day

- Building Permits (from February) – not market moving, but the last leading indicator to report for February

Thursday

- GDP (Q1 – first estimate)

- Personal Income, Spending (March)

- PCE Price Index

Friday

- ISM Manufacturing (April)

Market Charts

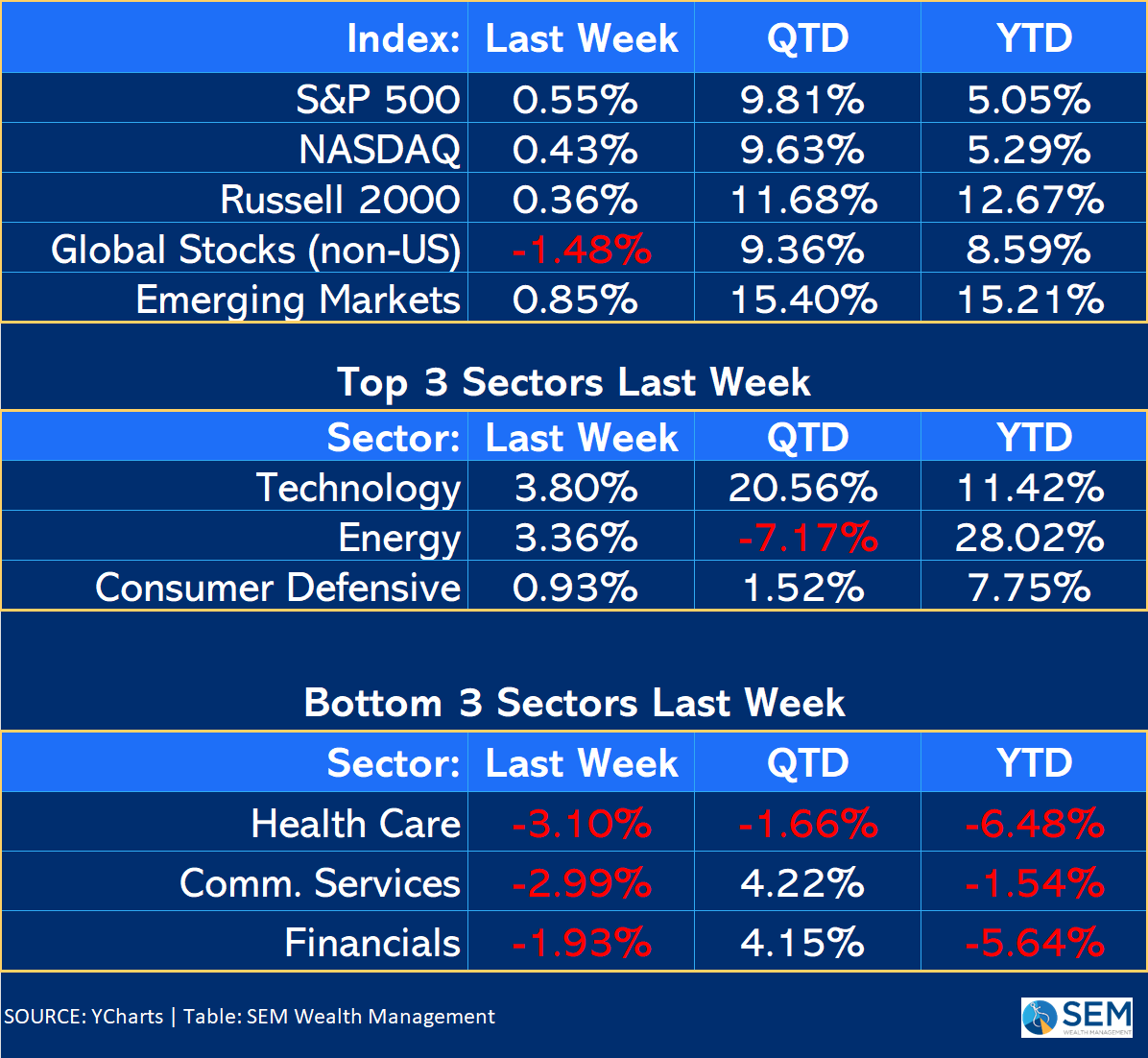

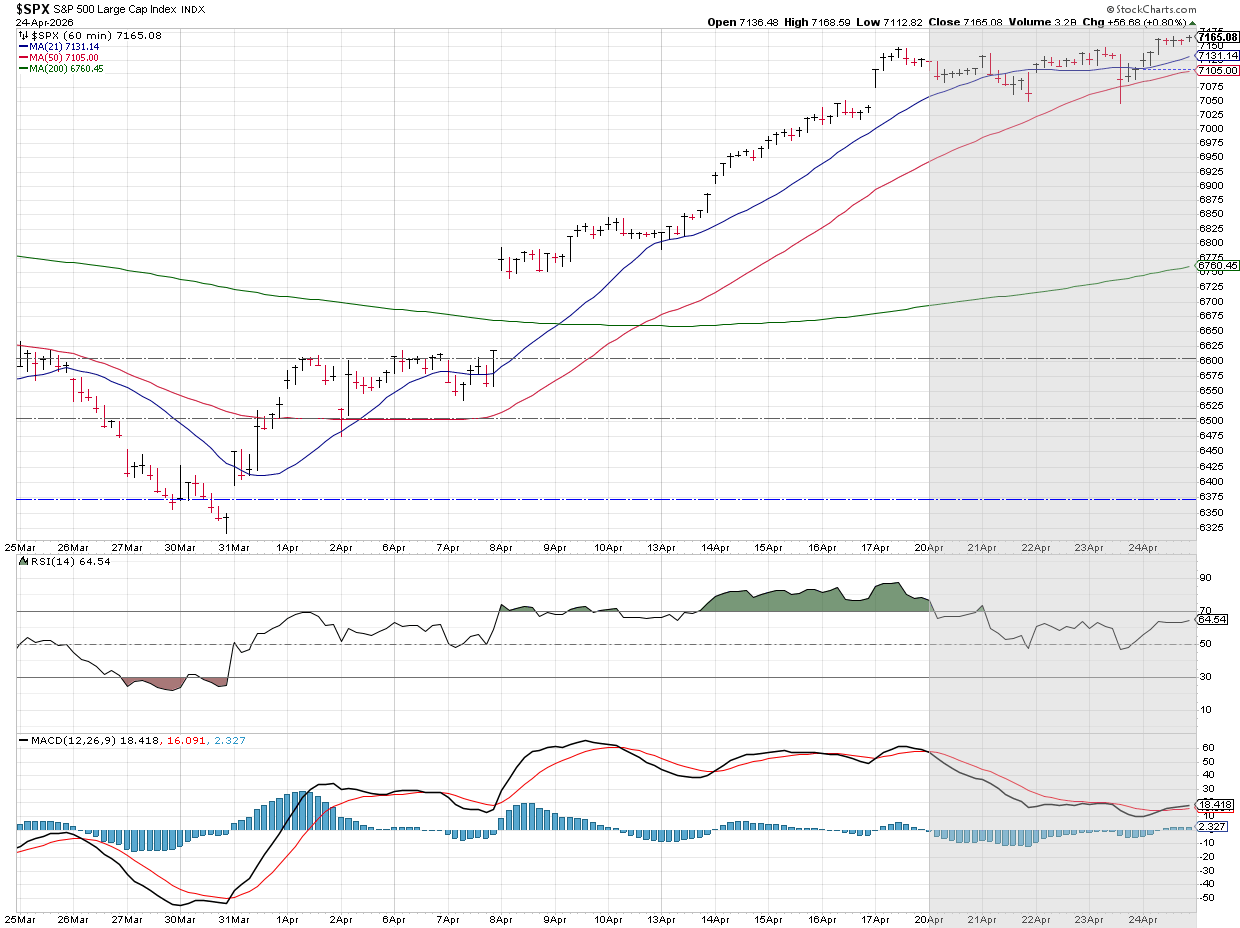

Technology stocks again led the way with Energy making a surprising appearance in the top 3 sectors after a tough 3 weeks. The S&P consolidated the huge move from the week before, which isn't a bad thing after a move like that.

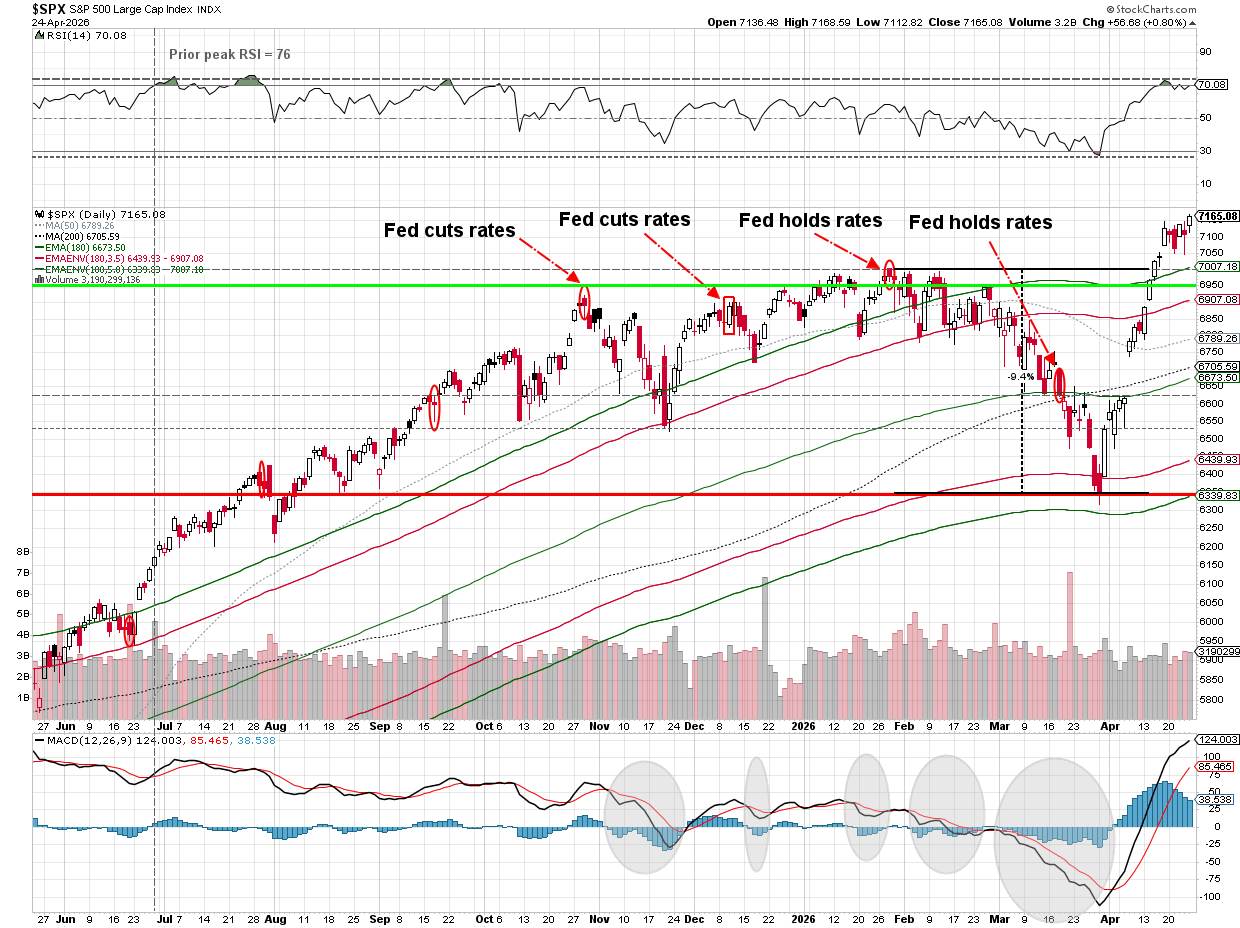

The market is at an all-time high, but also over-extended.

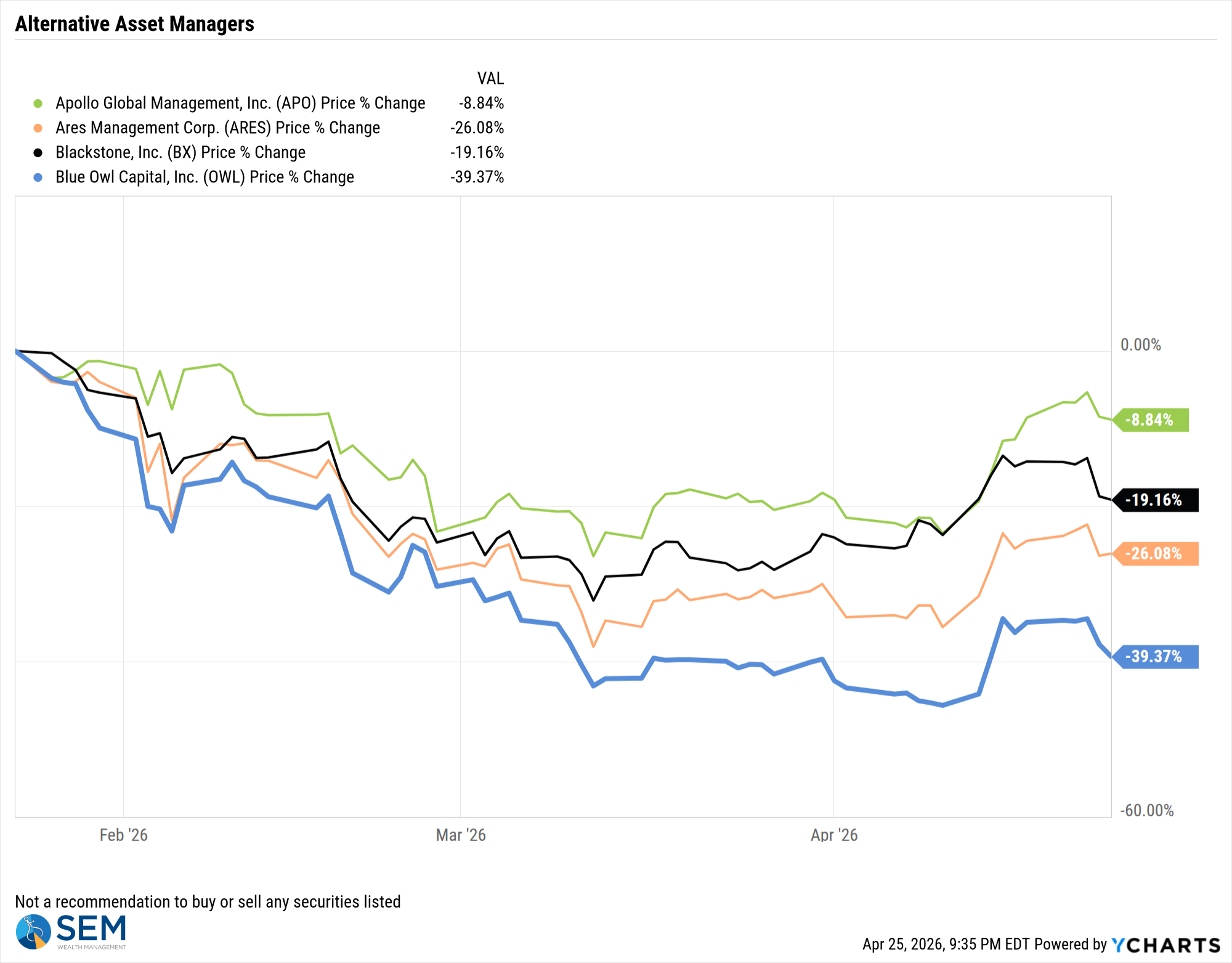

While AI-related tech stocks resumed their tear, the Private Credit related Business Development Companies fell again as concerns remain about how much exposure they have to data centers and software companies.

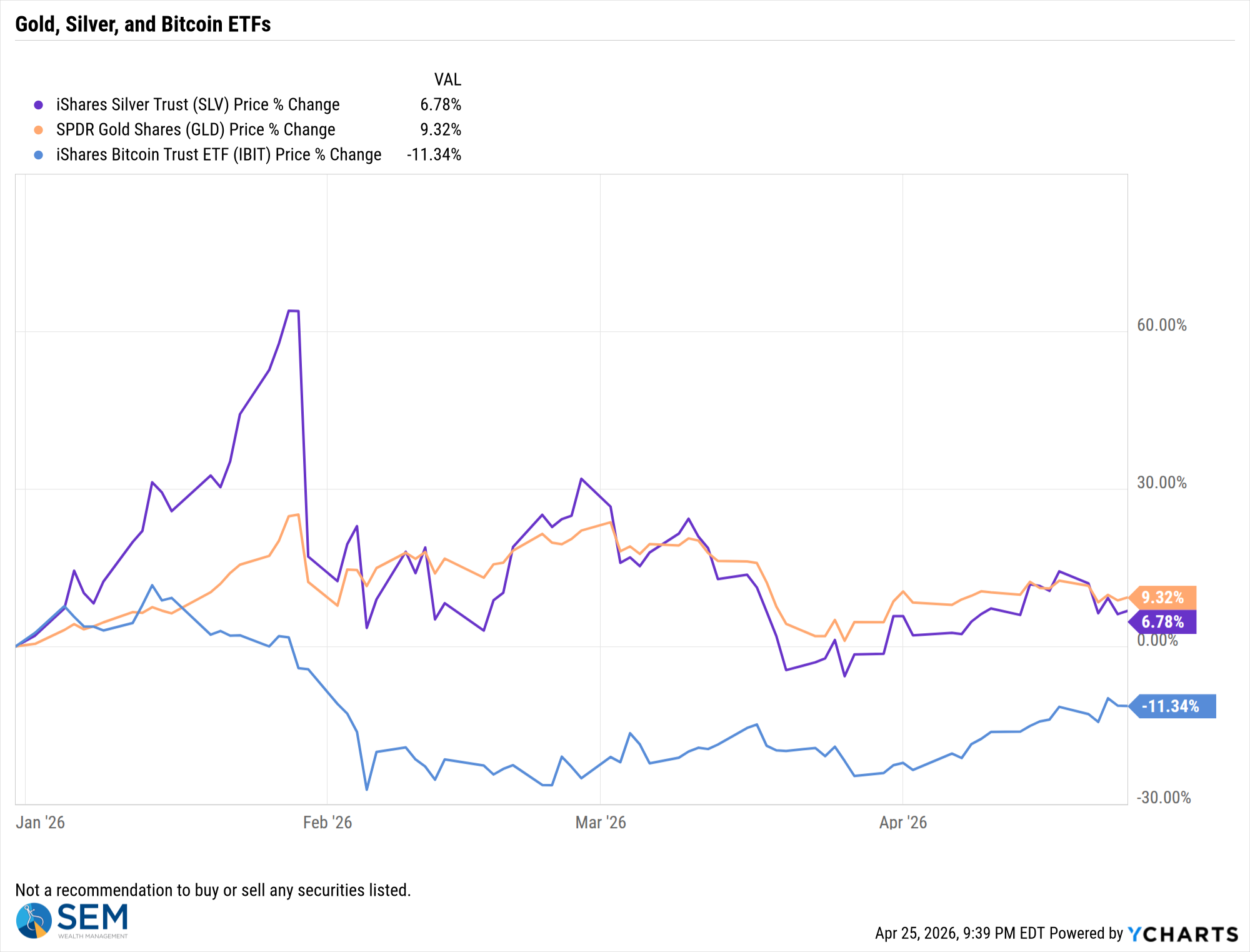

Bitcoin continued to rally off the lows of late March, but remains down for the year. Silver lost 6% on the week, and gold was down 3%. Both are up nicely for the year, but well off their highs from before the war with Iran started.

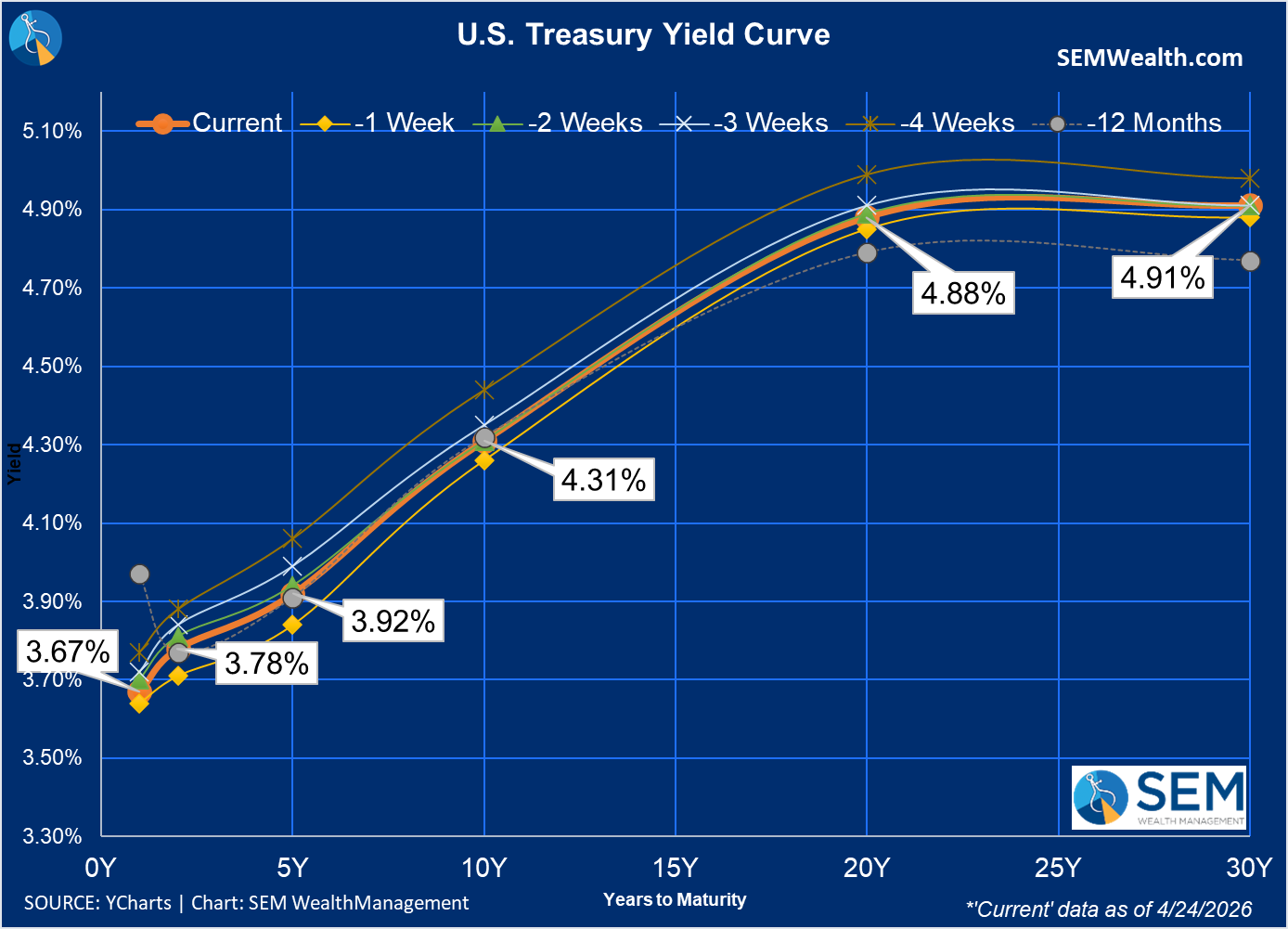

Bond yields crept higher last week even after the DOJ announced they were ending the investigation into Fed Chair Jerome Powell. That is expected to expedite the confirmation of Kevin Warsh to the Fed as some Senators had said they would not confirm him until the DOJ closed their investigation.

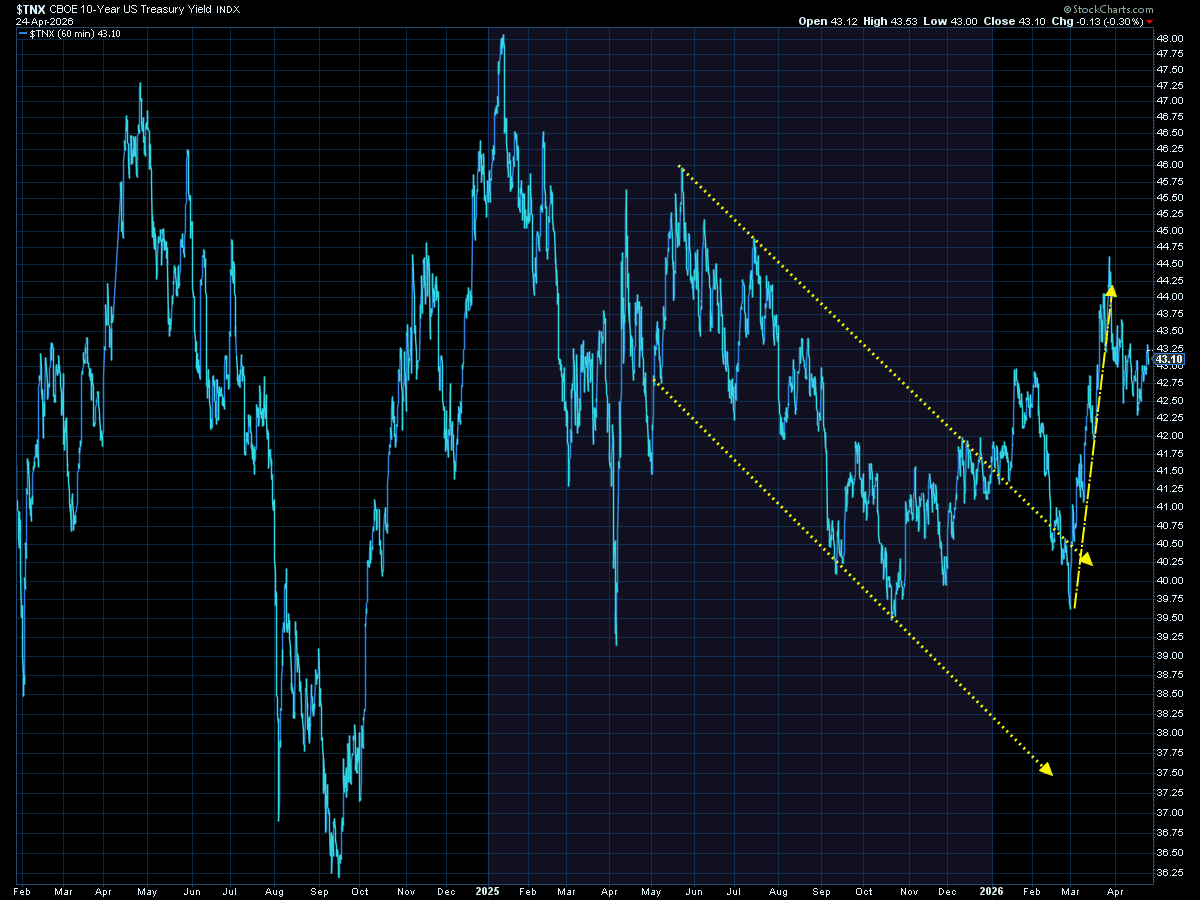

The 10-year Treasury still remains well above the pre-Iran war levels, which will remain a drag on the economy.

SEM Market Positioning

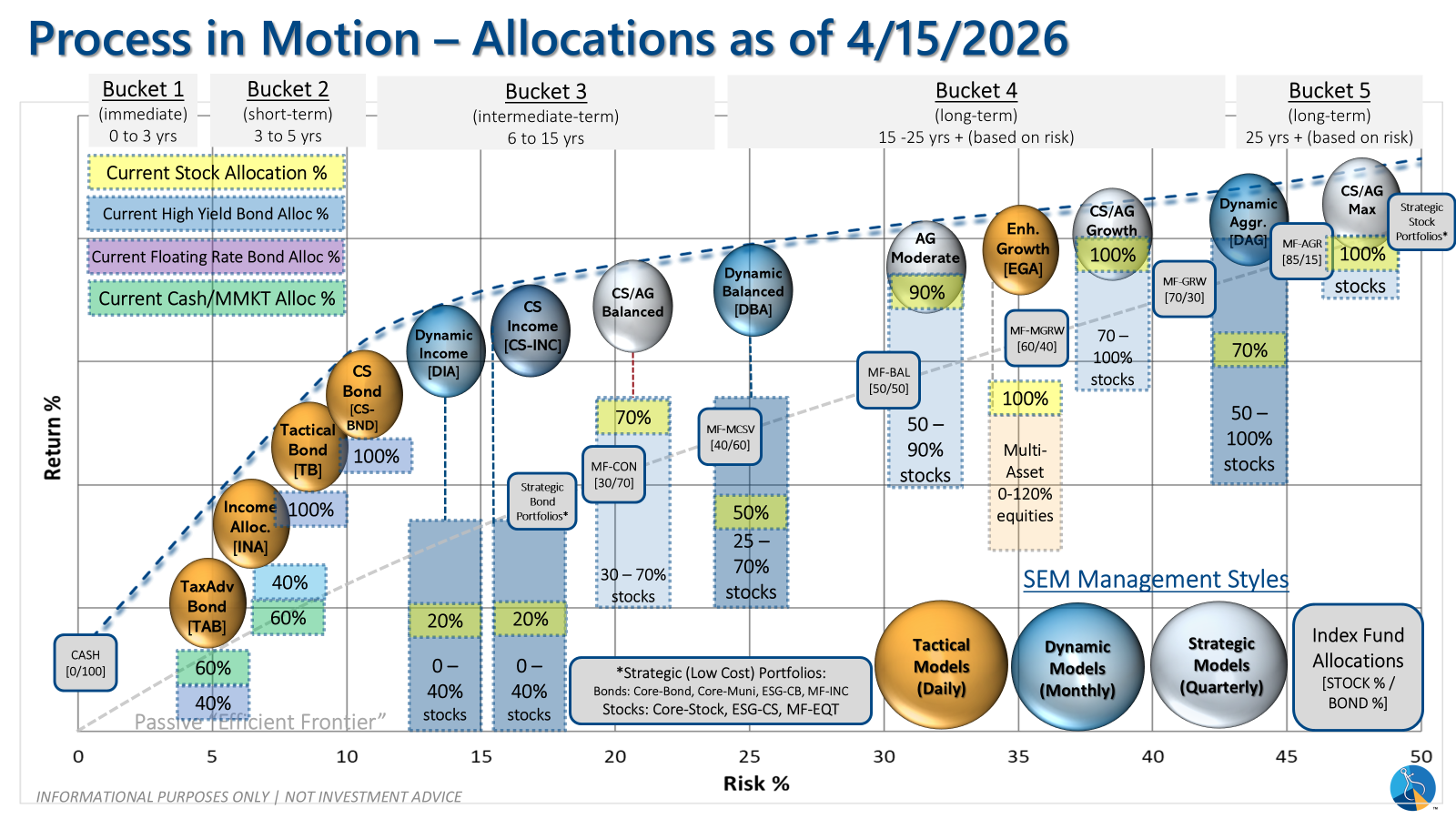

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

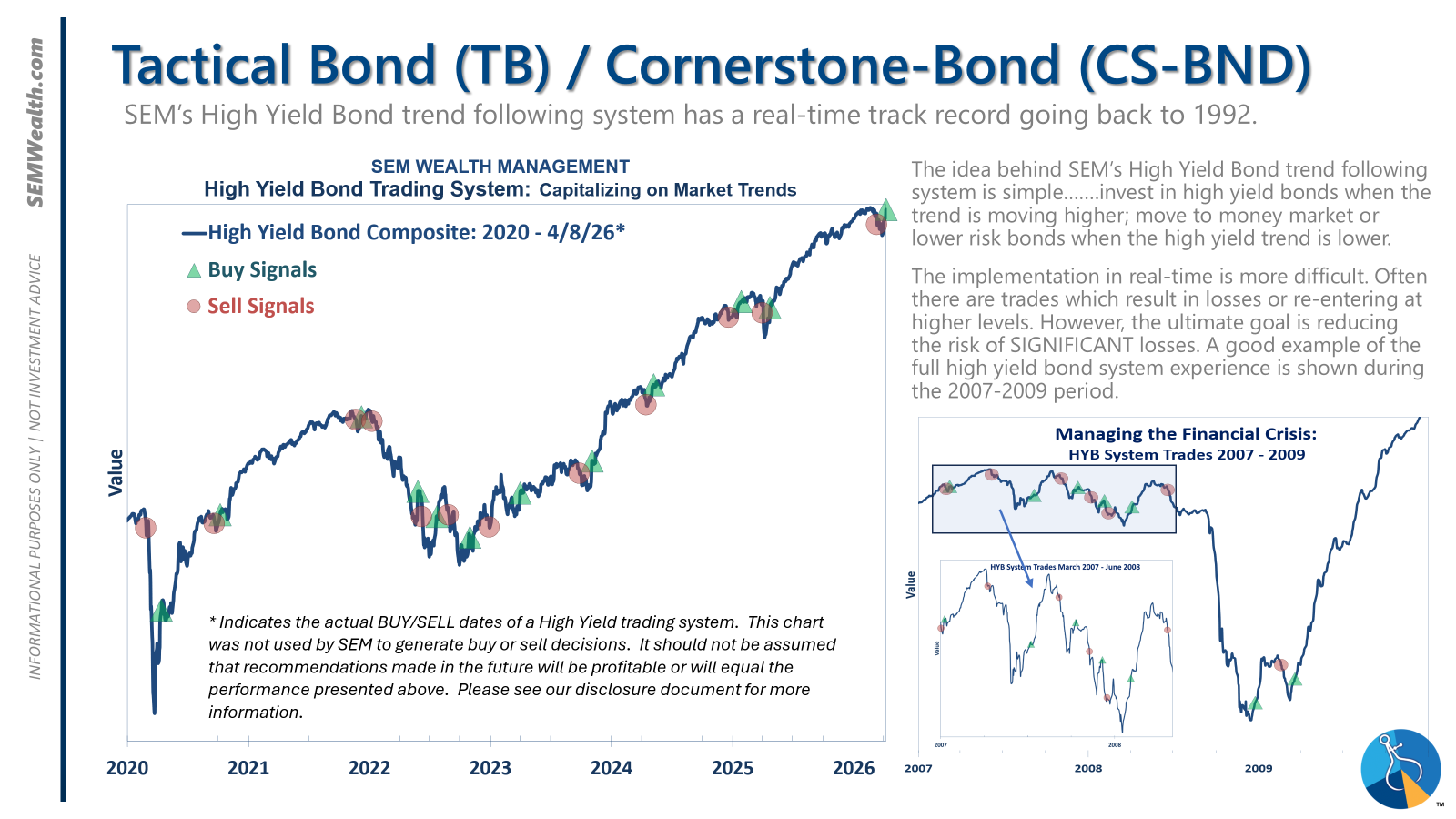

- Tactical = BULLISH | 100% High Yield Bond (4/8/2026) | High-yield spreads remain narrow but trend is slightly higher

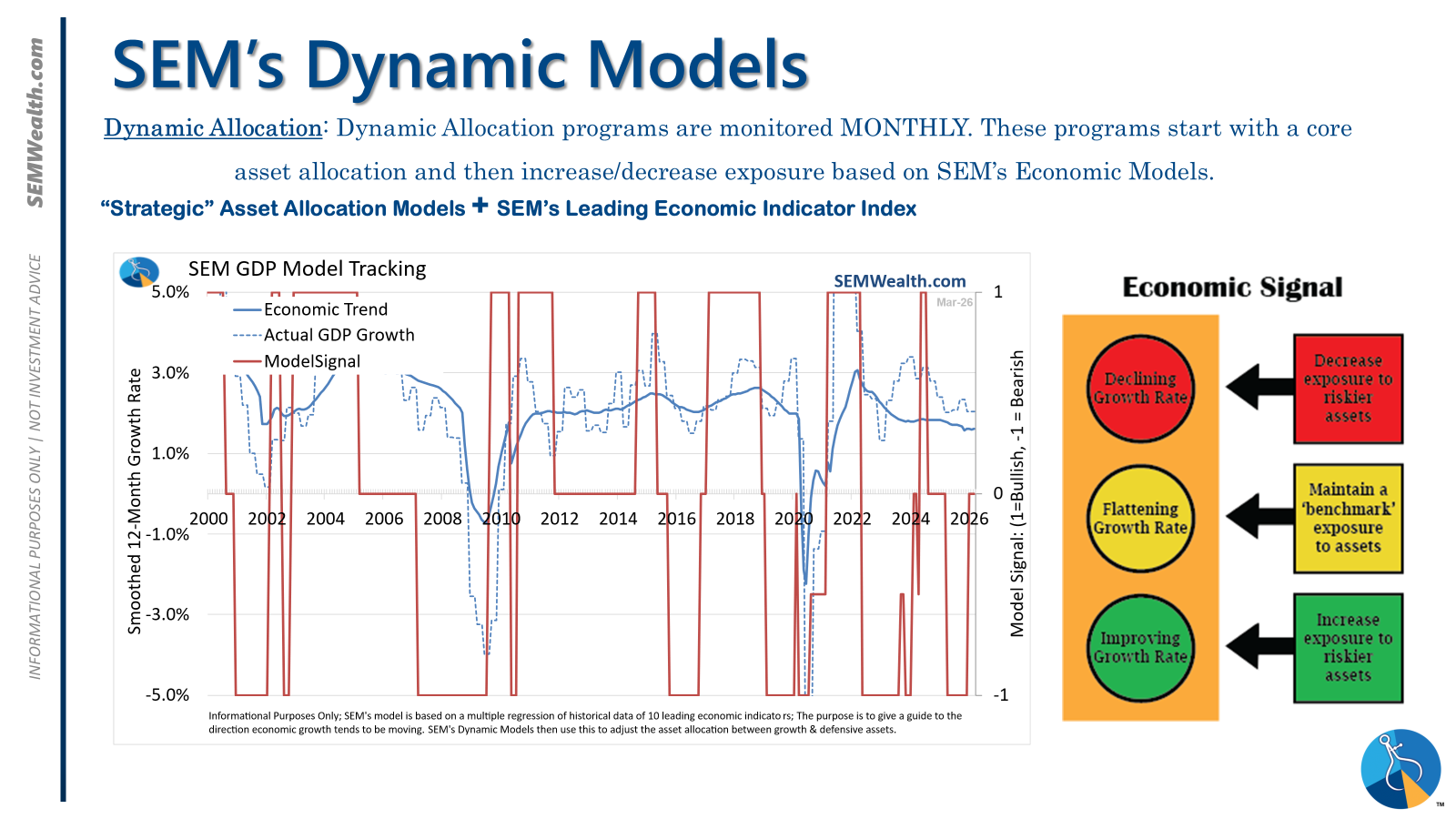

- Dynamic = NEUTRAL (2/15/2026) | "Benchmark" Allocation | Economic model inconclusive

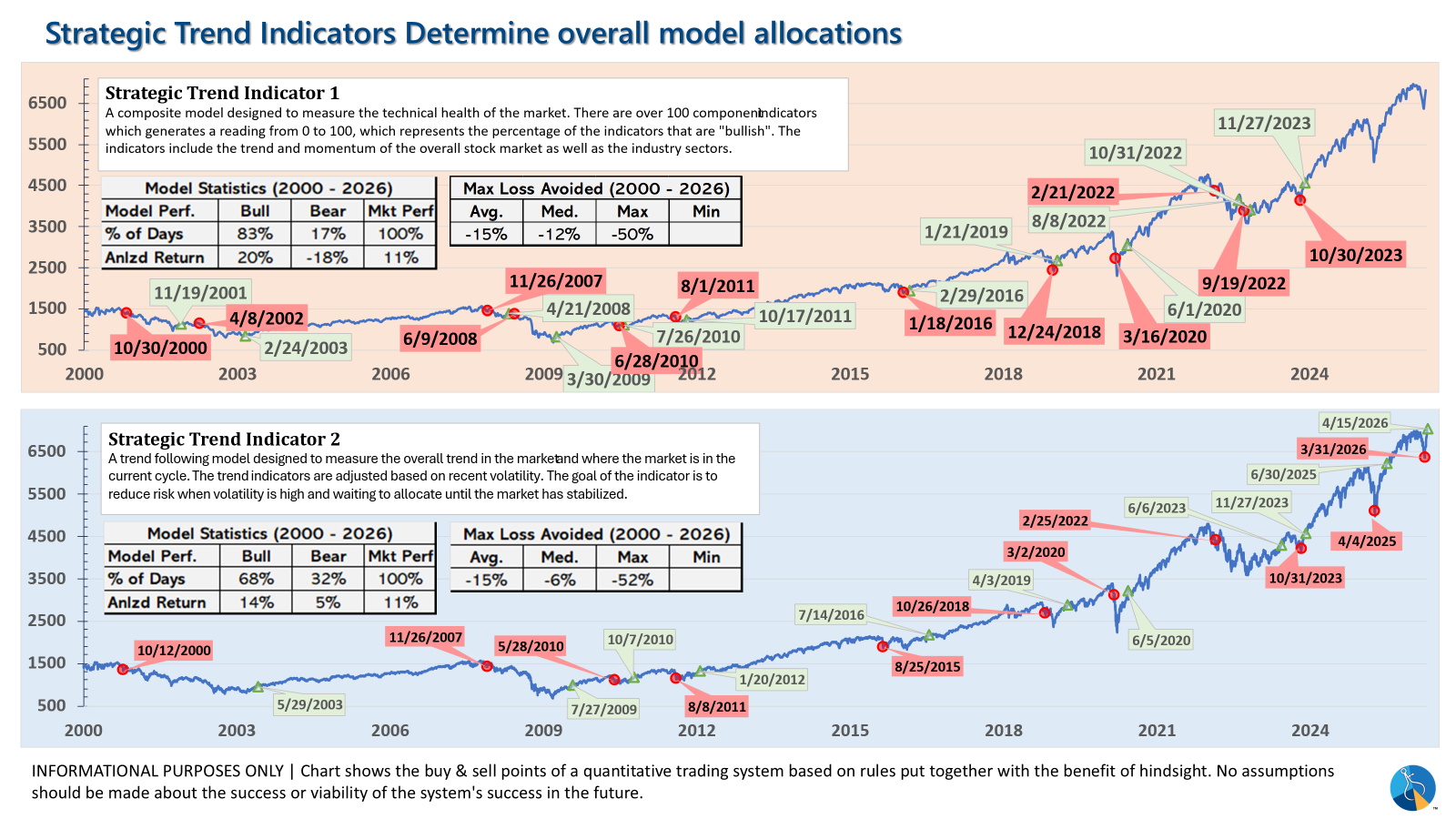

- Strategic = BULLISH (4/15/2026) | V-Bottom projecting "end" of Iran War

Tactical (daily):

- Monitored DAILY

- Models: Tactical Bond, Cornerstone Bond, Income Allocator, Tax Advantaged Bond

- Designed to follow the trends for use in our lower risk models

- BUY Signal issued April 8, 2026 (exiting the sell from March 13)

Dynamic (monthly):

- Monitored MONTHLY

- Models: All "Dynamic" Models (Income, Balanced, Growth, and Asset Allocator)

- Uses SEM's Quantitative Economic Model

- Designed to overweight riskier assets if economic trend is higher & underweight those assets if economic trend is lower.

- NEUTRAL signal issued February 15, 2026 (following BEARISH signal from July 2025)

Strategic (quarterly)*:

- Monitored QUARTERLY

- Models: AmeriGuard (Balanced, Moderate, & Growth) and Cornerstone (Balanced & Growth)

- Core Component: Quantitative Filter using 4 different time horizons across universe of asset classes

- Trend Indicator: Two different Quantitative Systems monitoring the intermediate-term trend, health of the market, and volatility

- CORE has been overweight small cap and international since October 2025 – overweight increased slightly in January

- Both TREND INDICATORS are BULLISH following 10% drop and "V-Bottom" reversal in early April

- AmeriGuard & Cornerstone Max DO NOT use the Trend indicator and are always 100% invested in stocks using our CORE rotation model.

The core rotation is adjusted quarterly. This quarter we saw half of our international positions reduced (we sold developed markets and kept our emerging markets exposure). We also saw the remaining share of mid-cap reduced in favor of more small cap exposure. We remain with a "barbell" core portfolio – about half in large cap and half in small cap as the models expect the market to "broaden".

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

Overall, this is how our various models stack up based on the last allocation change:

Curious if your current investment allocation aligns with your overall objectives and risk tolerance?