We recently conducted a survey of individual clients and professional investor advisors asking them to look at some data to select the most and least risky investments on the list. This is an exercise both groups are asked to do frequently. For individual investors, they have lists of investment choices in their employer plans, college savings plans, and for investments they manage themselves. Financial advisors are held out to be experts and more and more frequently are asked to do something they are not equipped to do — select the best set of investment options on the investment platform offered by their Broker-Dealers. Often these platforms have hundreds if not thousands of investment choices for the advisor to choose from.

In our survey (click here if you want to try it before reading about the results), we actually provided something I see very few of the platforms providing for those expected to determine the “best” portfolio for their clients — a measure of risk. I chose standard deviation, a measurement of volatility, but in our opinion an inferior statistic when determining how risky an investment may be, but a popular statistic used by many in our industry. Most of the time you only have the name and some performance numbers to base your decisions on. This helped most participants to zero in on what ended up being the second most risky fund on the list — Emerging Markets. Interestingly enough, very few people believed Select Income was risky even though it ended up being the third most risky fund on the list.

Check out my full discussion of the survey questions and “correct” answers here

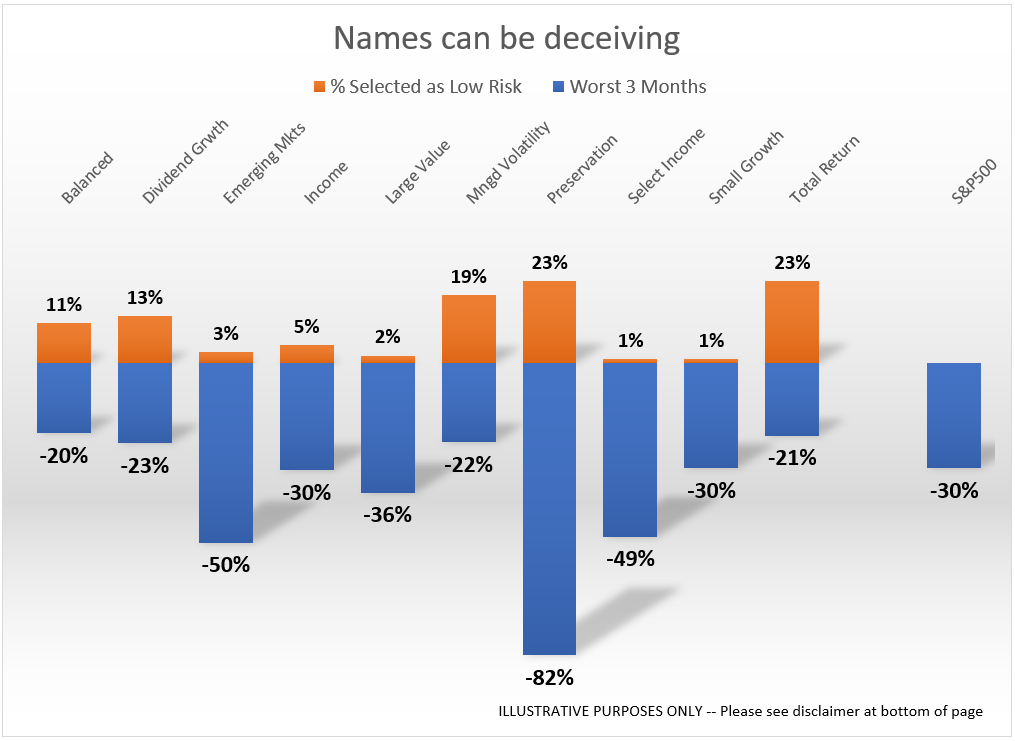

The critical mistake I saw both professional advisors and individual investors make was their choice of the “least risky” fund on the list. We saw a wide range of options chosen. This was partially because the standard deviation and returns of many of the funds were quite similar. The names of the funds can also be highly deceiving. What exactly does “balanced” or “income” or “preservation” or “total return” mean? This week’s Chart of the Week shows the results of the survey along with the worst 3 months for the fund AFTER the data for the list was gathered.

The most risky ended up being a fund most people would think would be the least risky — Preservation. The least risky is one I wouldn’t think would end up being the least risky — Balanced. Usually Balanced funds are close to 50/50 stocks and bonds. In both cases the only way to truly know what is inside the fund is to dig deeper into the holdings, to discuss with the manager how they allocate their assets, and to have a deep understanding of how the financial markets work. It is nearly impossible for an individual investor or a financial advisor doing full financial planning to have the time to do this properly. Even those trained with a full-time job managing money can sometimes be fooled.

We saw the platform investment manager for one of the Broker/Dealers recommending an allocation for “conservative” portfolios to the Preservation fund. These managers both hold the Chartered Financial Analyst designation that I have, further proof that simply having letters behind your name does not mean you’ll always make good choices.

I’m not slamming them for their decision, but I think it’s an example of how hard it is to pick investments on “platforms”. On paper the fund looked great, but if you dug deeper and saw how they generated their returns (heavy use of unhedged ‘derivative’ contracts) it would have raised red flags, especially if like me you had experience managing money through the collapse of Long-Term Capital in 1998, the tech stock crash in 2000-2002, and of course the 2008 financial crisis. These “weapons of mass financial destruction” as Warren Buffet calls them are something I try to avoid as much as possible with any allocations.

SEM has been working with investment platforms for over 15 years. We have seen so many advisors make really bad choices, not because they aren’t intelligent and good advisors, but simply because there are far too many choices out there and they are dealing with so many other things on a day-to-day basis. At SEM our only job is looking at all the investment choices on a daily basis. Not only can we help advisors on platforms set-up portfolios they can use that work well together, but we offer our own line-up of outside managers where we’ve done the FULL due diligence on each manager. (If you’re interested, ask me for the details.)

We won’t always be right, but there is something to say about somebody with nearly 3 decades of experience who’s full-time job is to manage money. We’re at a point in the cycle where the primary focus is on how cheap the investment offerings are. The old saying, “you get what you pay for” is likely to become apparent once again. I’ve seen this three times now. The other two times we saw so many managers and investment models “blow-up” it led to far too many investors losing more than they thought was possible.

By the way, overall the results of our survey showed both clients and advisors received a failing grade. Advisors did score somewhat better — averaging 62% versus an average of 43% for individual investors. Remember, the advisors working with us are experts in financial planning, not investment management. There are so many complicated choices to make on the planning side, we shouldn’t expect them to be experts in choosing investment models.

The more choices you have to make, the more likely you are to take the wrong mental short-cuts to make the decisions. Add in other emotional biases that may be present (such as clients saying they aren’t making enough money or clients saying they lost too much) the more likely you are to make the wrong choice. We do everything possible to remove those emotions and short-cuts.