Stocks are looking to have the best week since the 1930s. Of course this follows the worst week since the same time frame. The constant theme I continue to hear is "stocks are now undervalued" or "this is a once in a lifetime buying opportunity". The people saying this must be living in an alternate reality.

Let's walk through some charts and you can be the judge:

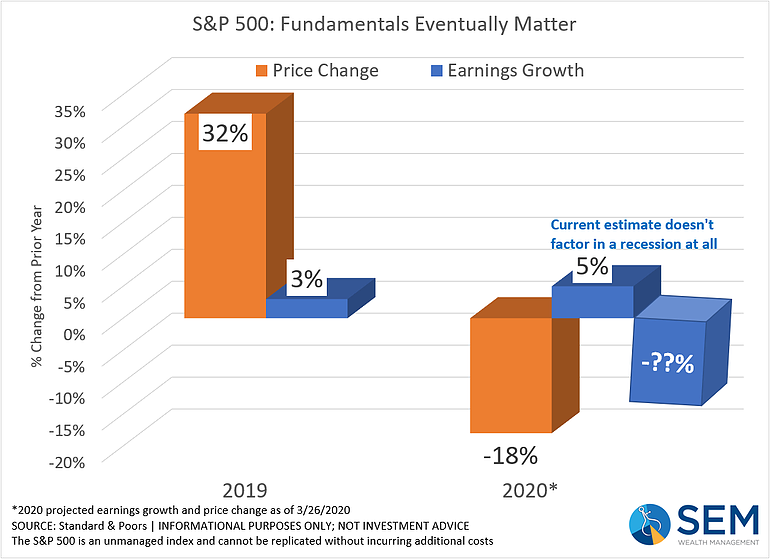

First off, as I said at the beginning of the year, the S&P 500 had no business going up 32% in 2019. All the market really did at the depths of the sell-off was give back the gains from 2019.

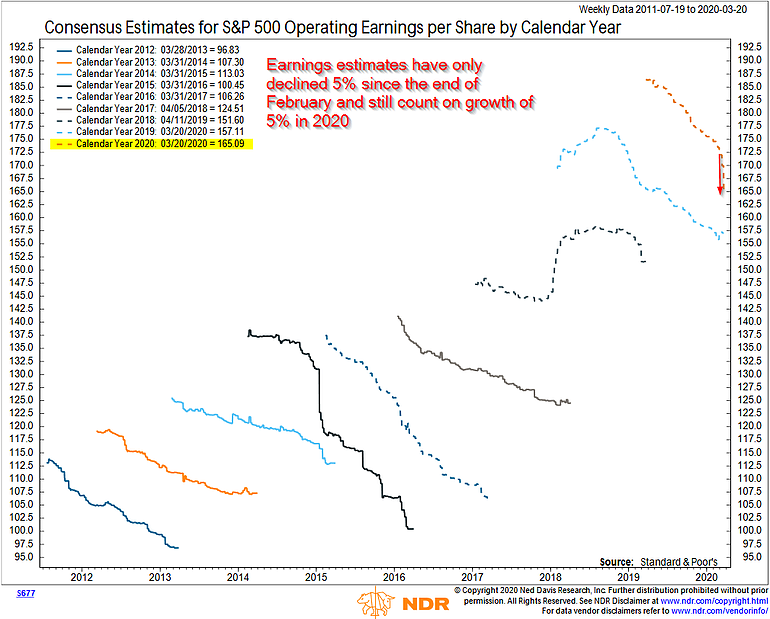

Second, analysts have still not adjusted their earnings estimates to reflect much slowdown at all. They expected 10% growth in early February, now they expect 5% growth. In other words, by the end of the year corporations will still be better off than they were when the year started.

Third, if you are buying (or choosing to still own stocks) today, you must believe that both the beginning of the year values were "fair" and companies will GROW their earnings in 2020.

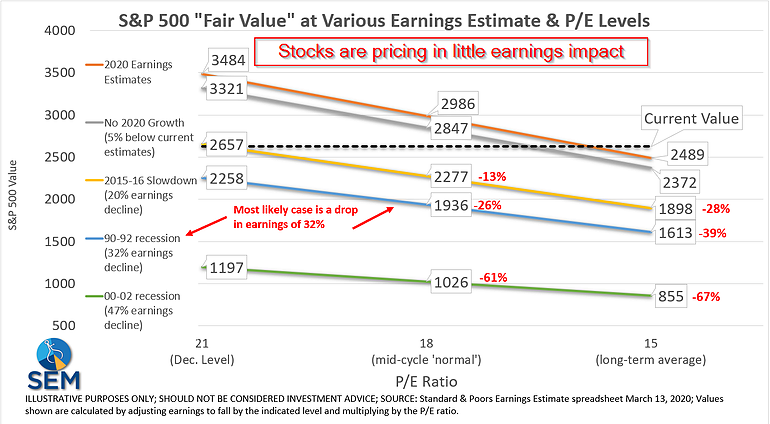

Fourth, if you look at long-term market history, this is nowhere near the "buying opportunity of a lifetime". Here are some charts from Ned Davis to put valuations in perspective. All use last year's earnings to calculate valuation.

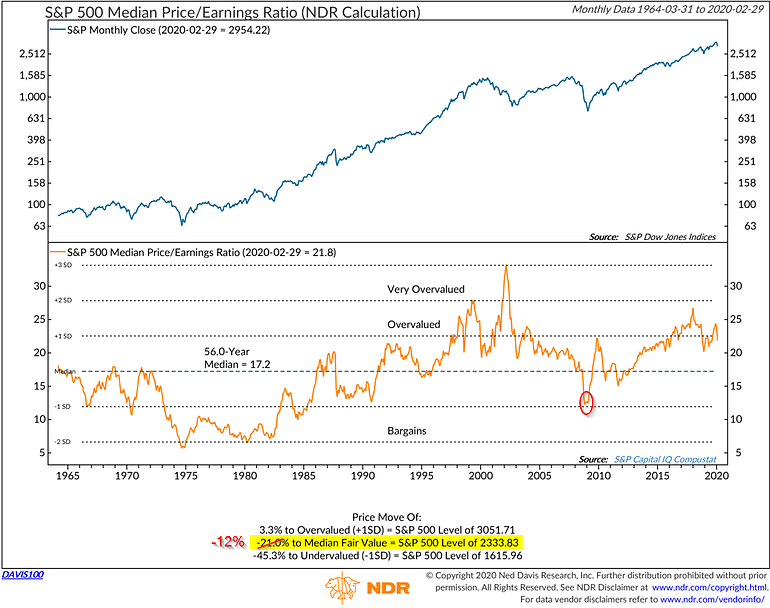

Using Median P/E ratio (throws out extremes), stocks are 12% above "median" value and remain in "overvalued" territory (before any earnings slowdown). The "buying opportunities of a lifetime" come when stocks are BELOW their median value.

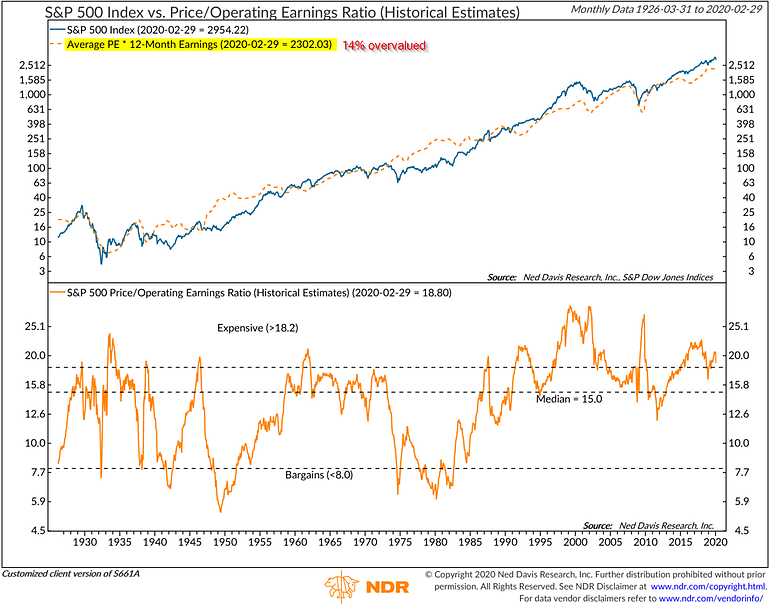

Using Operating Earnings (excluding all the special items companies want us to ignore), stocks again are still overvalued (again with NO IMPACT from COVID-19).

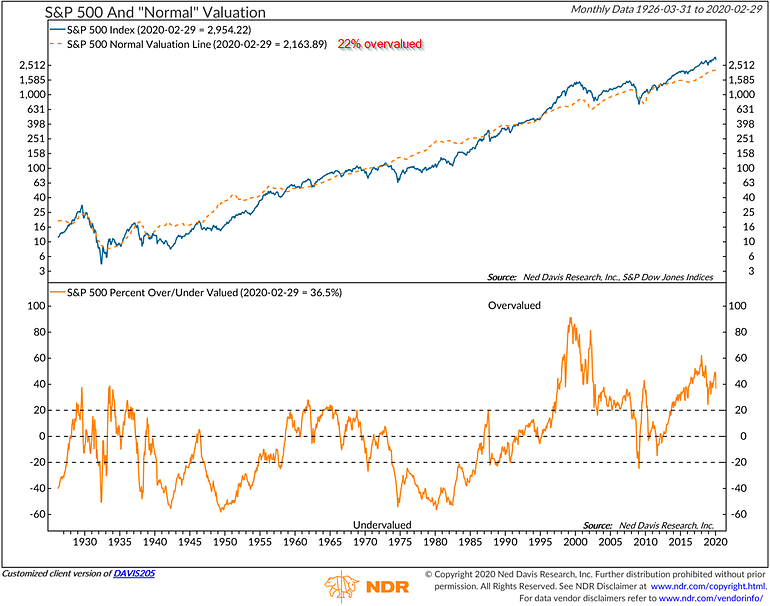

NDR also calculates a "normal" valuation using dividends, earnings, cash flow, sales, inflation-adjusted P/E, and the long-term trend (all the alternative metrics I hear analysts using). Using these metrics, stocks are 22% overvalued (again assuming NO IMPACT from COVID-19)

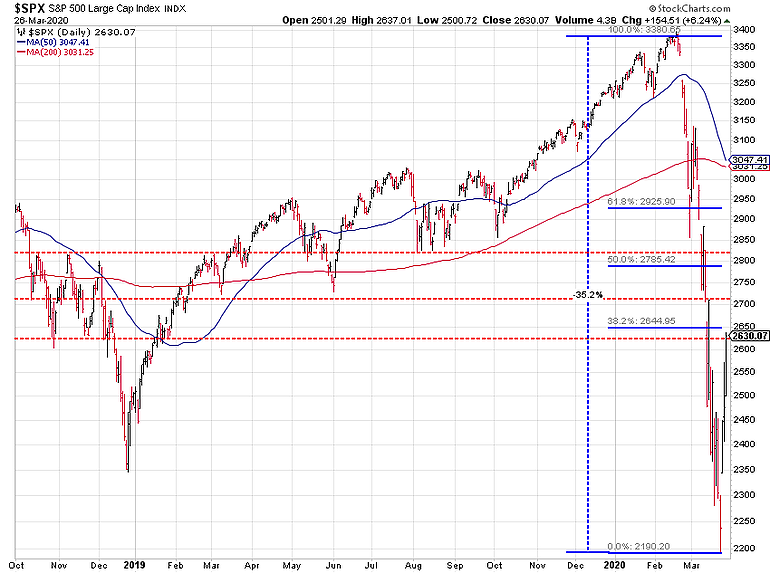

Fifth, stocks are back to February 2019 levels -- well off the lows of December 2018. They've bounced to the first logical rallying point. This is nothing more than a technical bounce. They can continue moving higher, especially into quarter end (there are hundreds of billions of "strategic" portfolios that need to sell bonds and buy stocks), but we EXPECTED a big snapback rally. They always happen after a big sell-off.

Where we Stand Now

So let's take a look at where we stand now:

- Valuations are high even if we have NO RECESSION. They are absurd if we do have a recession.

- Even with no earnings slowdown, valuations are high. Looking at the track record of analysts, earnings estimates are going to come down, which makes stocks even more overvalued.

- Prices and earnings in the market assume NO IMPACT by the end of the year from COVID-19. If that is true, great. If not, stock prices need some serious adjustments.

Let's Go Back to February 20

Let's assume NO IMPACT from COVID-19 and review where we were on February 20 (the day the market peaked):

- Stocks were overvalued

- Revenue growth was slowing

- Profit margins had peaked in 2016

- Economic growth was slowing despite a $1 Trillion budget deficit

- Business & state, local, and federal governments were all over-leveraged

Where is the Opportunity?

All of the above tells me this is a SELLING OPPORTUNITY, not a buying opportunity. Logic tells us:

- Even with no impact from COVID-19, all of the factors listed above are still in place.

- It is very possible COVID-19 will cause a major STRUCTURAL shift in our economy -- slower economic growth, lower margins, and slower revenue growth.

- The 'solutions' (which I think were necessary and welcome) from both the Federal Reserve and the government will only make all of our problems worse over the long-term. Remember debt, is future spending brought forward. This makes buy & hold investing far less attractive.

Just because stocks went down it doesn't mean they are now "on sale". If you believe they are on sale, you must also believe prices were reasonable DESPITE the items listed in "Let's Go Back to February 20" above. I look at it like the furniture sales. If stores are open in your region, you're about to have the pre-Easter sale, followed by the Easter sale, followed by the pre-Memorial Day sale, etc, etc, etc.

Their goal is to get you to believe this is a great opportunity. All the people saying this is a "buying opportunity" were also the ones telling you at the peak of the market that stocks were fairly valued and set to go up. They only make money if you stay invested in the stock market, so they always want you to believe this is a buying opportunity.

What if I'm Wrong?

Now here's what's important:

- All of the above is my opinion and plays ZERO impact on SEM's model allocations.

- We have TREMENDOUS opportunities in our fixed income portfolios (will hopefully have the data gathered next week)

- The Dynamic models have a large chunk of money ready to go to work WHEN the economy bottoms.

- AmeriGuard will be able to adjust allocations next week, but we've also been able to add daily oversight to the models which will be deployed going forward.

I'm humble enough to know I could be wrong, but the key is it doesn't matter. Our portfolios will adjust to whatever the ultimate impact is.

What if You're Wrong?

I don't see how anybody can with confidence declare the worst is over, which means stocks are not on sale, but significantly overvalued. If you do, based on history you better be right because the "shock" of seeing the economy still falter and earnings plummet is what always happens during a bear market. We had all kinds of stimulus packages from 2000-2003 before they finally worked. Remember the Fed started "extraordinary" measures in early 2008 and TARP passed in early October 2008. Passing these deals and getting the money into our system is the problem.

Do you really want to guess about the outcome of something that has never occurred in our country?

Who do you want to trust, the company that told you stocks were a good value at the beginning of the year and continue to argue that or the company who has time and time again proven the ability to navigate all types of markets?

SEM has proven our value throughout March and I'm confident regardless of the outcome we will again prove our value as we go from "hope" this is over to the reality of facing the damage this virus has done to our economy.

Read More Data-Based Analysis

The purpose of this blog is to give our readers the research and data behind what is actually happening in the market. When we see panic we will be trying to offset that by looking at the bigger picture. When we see euphoria we will do the same. In a week we've gone from panic to euphoria. Here is some of the big picture stuff you should be focusing on:

No Quick Fixes: A look at past large drops in the market along with a road-map of what we should expect based on history.

Monday Morning Musings: All the random thoughts that came across my mind over the weekend.

Not another COVID-19 Update: A short video (and written summary for those of you like me who would rather read than watch) discussing the BIG PICTURE outlook and where we should be focusing.

There are additional links inside each article that look at some of the structure things the market and economy are facing.