The bear market of 2020 is unprecedented. The pace of the decline has exceeded all records, including the steep fall in 1929. While the move is unprecedented, the reason we only use quantitative models at SEM is this allows us to not guess about the next move and how to adjust our portfolios. This is CRITICAL in our ability to navigate uncertain times.

Remember, the 9/11 attacks were unprecedented. Real Estate prices collapsing across the entire nation were unprecedented. The emergency stimulus measures we saw in 2000-2003 and again in 2008-2009 were unprecedented. SEM thrives in "unprecedented" times.

History doesn't repeat, but it most certainly rhymes. The reason is simple -- while technological advancements, information dissemination, education, and our own study of history should make all of us better at not repeating the same mistakes, there is one common denominator. We are humans. Humans have natural behavioral biases.

Last year we did a series of tests on our advisors and clients to show how both groups are prone to specific biases. If you find yourself feeling certain about how this will play out, I'd encourage you to take some time to check out our BEHAVIORAL BIASES page. Make sure you click on the links at the bottom of the page to review the tests we ran last year.

Anybody who has listened to me the past few years know how how dangerous a RECESSIONARY BEAR MARKET is for both advisors and investors. You have a combination of shock (we were clearly in the "euphoria" stage of the bull market at the end of 2019), huge dollar losses -- significantly higher than the last bear market, job losses, and overall economic uncertainty. You cannot fix a $22 Trillion economy in just a few months (or by passing a $2 Trillion stimulus bill).

The stimulus is welcome and needed. The Fed's long list of emergency measures is welcome and needed. That said, the implementation, timing, delivery, and effectiveness of the stimulus measures will take time. Bankers are working from home. The handful of small business owners I talked to didn't even know if their banker does SBA loans. The Treasury Department says the money will go out in days, the IRS says it could take weeks or months. Unemployment offices were overwhelmed last week.

Maybe I'm wrong. I hope I'm wrong. I see too much pain in our community and around the country.

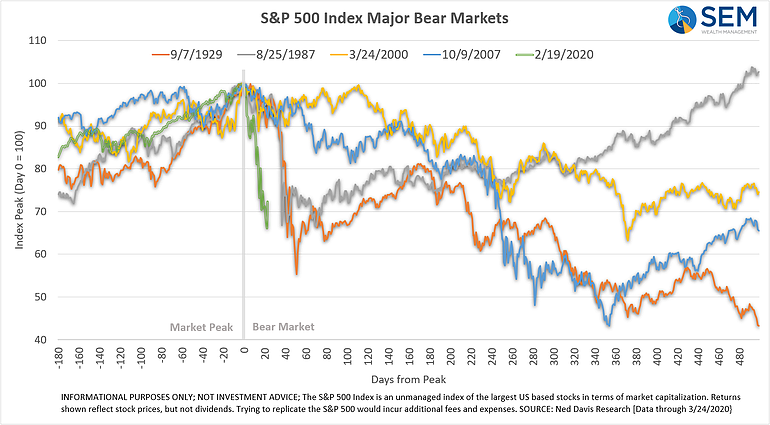

Going back to the DATA, let's look at what we should expect. Remember, history doesn't repeat, but it most certainly rhymes. Let's take a look at some past bear markets. Day 0 is the top of the market. I went back 180 trading days (about 9 months) and then forward 500 trading days (about 2 years). This allows you to see both the last phase of the bull market and then how the bear market played out.

Looking at these I think it is clear -- there are no quick fixes. There were all kinds of emergency stimulus measures from Congress and the Federal Reserve -- multiple packages had to be passed. 1987 is actually an outlier -- it was the only bear market on the list that didn't have a recession. Even it took a very long time to recover.

The other thing that is clear is how many big rallies we should expect. Last November I posted an article about "missing the best days". The data shows us that nearly all of the best days in the market come inside of a bear market. Having investment models such as Tactical Bond, Income Allocator, Dynamic Income, Dynamic Balanced Allocation and even Dynamic Aggressive Growth do not fully participate in the "best days" because they are designed to not be fully invested during bear markets. We've seen that play out in March.

You should expect big rallies. History tells us this. History also tells us this could be a very long bear market. This means having a plan to adjust portfolio allocations to better fit the financial plan, cash flow strategy, and investment personality of your clients (or your own portfolios). I've been asked more times than I can count if it's "too late" to make adjustments. Without knowing the full situation, generally speaking, rallies should be used to reduce risk exposure (if necessary/desired) and sell-offs should be used to add risk exposure (if you've been waiting for better prices, we finally have some.)

In both cases, dollar cost averaging is typically the safest strategy. This means selling in chunks as it goes up and adding money in chunks as it goes down. After yesterday's rally, stocks are back to December 2018 levels -- we haven't given up that much, just the insane rally from December 24, 2018 through February 20, 2020. Remember earnings grew by 3% last year. Those prices were beyond unreasonable.

Again, going back to the data, we should expect some basic snap-back rallies inside a bear market. It's never exact, but generally it follows some basic patterns.