SEM applies a Behavioral Approach to Investing. Our total portfolio approach is designed to overcome the most common behavioral biases. To understand the importance of this we need to first understand the biases. About two years ago I posted a video clip from one of our client seminars where I discussed some of these.

The list of biases is extensive, but there are some common ones that tend to occur during particular phases of the market cycle.

Belief Perseverance Biases

The first group of biases are Belief Perseverance. These are COGNITIVE errors, which is mental discomfort when dealing with new information that conflicts with past beliefs. To deal with the discomfort, our brains tend to use the following biases:

1. Conservatism Bias

Conservatism Bias is a bias where we maintain our prior beliefs by failing to properly incorporate new information. We see this in action every day with both individual companies and the markets. New economic data or financial reports could mean a serious change in the long-term outlook, yet we tend to highly overweight the previous information and underweight the new. Mentally it is far easier to maintain the current view than to try to incorporate the new, often highly complex information into our outlooks. The most glaring example of this in the current market is the shift in Fed policy from “stimulative” to “tightening”, something the market has not had to face since Allan Greenspan was in charge back in 2006.

2. Confirmation Bias

Confirmation Bias is one way we deal with the new, complex information — we ignore it. Confirmation Bias seeks only information that confirms our previous belief and ignores anything that may conflict with it. We see this quite often with our political affiliation, but it exists in all aspects of life. Investors & analysts alike tend to only pay attention to information that falls in line with their outlook. They often ignore or explain away anything that conflicts with this.

Looking at the Fed, we again see a glaring example of Confirmation Bias. I’ve heard nearly every Wall Street analyst (who all tend to have a very strong bullish slant) use data showing how the market usually rallies when the Fed raises interest rates. Overall this may be true, but they are ignoring one key aspect — nearly all of the increase has been due to increasing earnings (since the Fed usually raises rates during a rapid recovery). The P/E ratio tends to fall fairly significantly during the rate hiking cycle as investors lower their “risk premium” under the assumption the Fed will raise rates too much and cause a recession. With earnings already slowing dramatically, it may be difficult for the market to rise with the Fed raising rates.

3. Representativeness Bias

Representativeness Bias is where we assign “new” information into categories based on our own past experiences. We see this happen quite often during a bull market. Every dip in the market is relatively shallow, so investors classify a sell-off as a buying opportunity. We also see a constant classification of what “year” the market resembles. So many people were burned by 2008 they are looking for similarities. Most often I hear analysts say, “housing is not in a bubble, so any correction won’t be as bad as 2008.” We also hear, “tech stocks aren’t as overvalued as 2000, so any correction won’t be as bad as 2000-2002.” They are instead classifying any corrections into “2011” or even “1998” categories because those are ones most of us remember. (This also could be considered “Conservatism” as both 2011 & 1998 comparisons were quite bullish in the end.)

I rarely hear anybody use a 1936-37 comparison to the market even though fundamentally and technically we could be looking at something similar. Back then the Fed raised rates under the assumption the recovery was stable enough and they risked losing control of inflation. We of course know with hindsight the Fed did not have control of the situation (our final two Belief Perseverance Biases). The key takeaway from this bias is to look at ALL market history before classifying something into a particular category.

4. Illusion of Control Bias

This bias stems from people believing they have control of a situation or can influence the outcome, when in fact they cannot (study the history of the Federal Reserve for proof of this one). As investors, we tend to think we can control the direction of our investments, but we are truly at the mercy of the overall market. Sticking to longer-term, well researched strategies is critical to overcoming this bias as an investor. If you are a member of the Fed, I would encourage you to study this bias in much greater detail.

All of these biases tend to occur during a bull market, so it is something we all need to watch carefully for.

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

6. “Recency” (Availability)

Out of all the behavioral biases, “recency bias” is probably the most prevalent. I first heard our founder, Rick Gage, use the term Recency Bias back in 1999. He told me something that has always stuck with me. The human brain is conditioned to take the most recent situation and project it out indefinitely into the future. This causes investors in bull markets to take on far more risk than they can handle, but then in bear markets to become far too conservative to ever meet their investment objectives. Recency bias applies throughout our lives, from our assessment of our favorite sports team, to our outlook on our children’s future, to the weather, to the direction of our country, etc. It’s just how our brains work.

As I was studying the Emotional Biases of investors I was excited to see psychologists actually defining the technical term for “recency bias” — Availability Bias. Availability Bias is an Information-Processing Bias where individuals take a mental short-cut (heuristic) to estimate the probability using the information that comes most easily to mind. The way the human brain is programmed, the most recent information is easiest to recall. There are 4 sources of Availability Bias that apply to investing.

Retrievability: When an answer comes quickly to mind, more often than not we will assume that is the correct answer. This happens quite often in the investing world. The Wall Street firms have spent so much money advertising that investors tend to choose the “best” mutual funds based on how well known their brand is rather than the actual performance. We also see this when it comes to annuities, management fees, and active investing. With all the marketing dollars spent criticizing these things, investors have been programmed to look down on them regardless of what the long-term results say.

Categorization: This form of Availability Bias is closely linked to the Belief Perseverance Bias, Representativeness. When solving complex problems, individuals will group the data into simple categories that are familiar to them. We tend to assign markets to simple categories (bull or bear) or break them down into similar years for comparison (is it 1998 or 2011?). We also tend to limit our investment options to categories we understand, which will limit our available investment options or cause us to be heavily invested in one category. For US investors that means a disproportionate weighting in Large Cap, US based stocks due to the belief the S&P 500 represents the “market”.

Narrow Range of Experience: We are all prone to taking our own experiences and believe that is how the world works. Over the past 8 years this has often been the case when we see nearly every asset class rally on economic data that was highly disappointing. This is because during this bull market bad economic news has actually been “good” news for the markets as it meant the Federal Reserve would be prone to creating more “stimulus”. We also have witnessed a large number of people that believe the Fed will not allow a bear market or recession to happen since they have done “whatever it takes” to prevent this from happening the last 8+ years. This belief also falls under many of the Belief Perseverance Biases above.

Resonance: We all tend to believe the “world” shares our own interests and experiences. If we are struggling financially, we believe the rest of the economy is also struggling. If we have a strong interest in market behavior, we believe everyone shares this interest (which leads to writing 3000 words and counting in 2 1/2 days in a blog article). With our investments we have clearly seen how an individual’s interest or experiences can slant both their risk tolerance and their choice of investments. This leads to over weighting (or under depending on the current trend) their own industry and shifting their asset allocation depending on how well the company they work for is doing. As the economy has improved and more people found work, we’ve seen a stark shift in investors’ risk tolerance even though the economic cycle tells us we are probably near the end of the expansion cycle.

6. Hindsight Bias

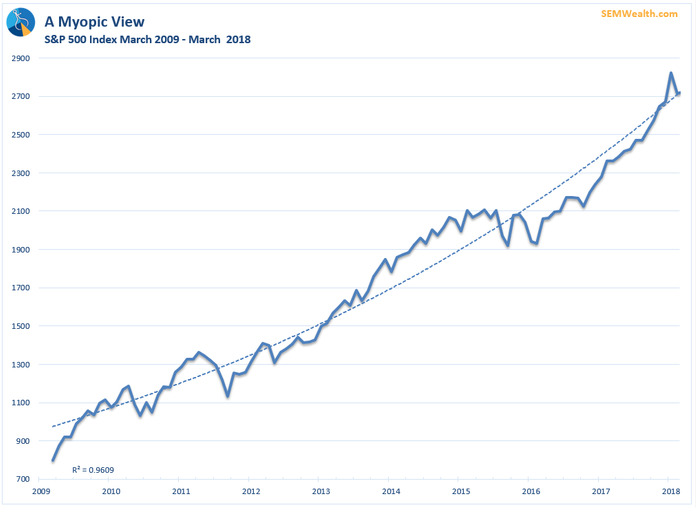

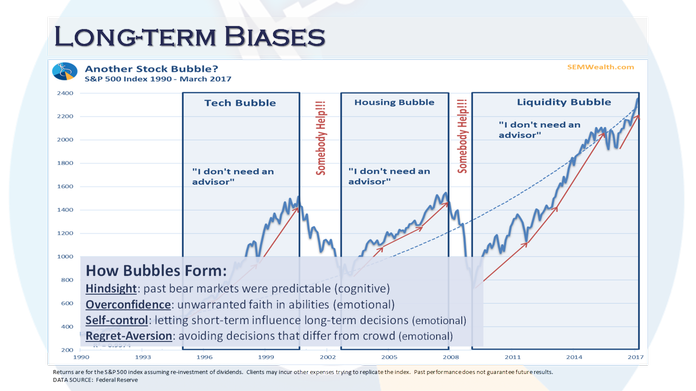

Unlike the other cognitive errors, hindsight bias tends to play out over longer periods of time and is one of the key reasons we see bubbles form.This is probably the most difficult bias for us to overcome as investors. With hindsight we see past events as being predictable, which means it is reasonable that we “should have seen it coming”. This leads us to believe we will see the next one coming and be able to avoid it (see the other biases above). This is the reason so many people are looking for comparisons of past market drops. The problem is the NEXT financial crisis and/or bear market is unlikely to be caused by the same thing that created the past two bear markets. As we are now working with our third teenage driver on getting his license we see an important lesson for investors — if you spend too much time focusing on the rear view mirror you will not see the danger IN FRONT OF YOU.

Emotional Biases

All of the previously discussed biases were COGNITIVE ERRORS. Simply put, Cognitive Errors are mistakes our brains tend to make using “heuristics”, or mental short-cuts. They can be categorized as information processing errors or belief perseverance errors.

7. Overconfidence

This is the 3rd stock market bubble I’ve been involved in during my career. By far the Emotional Bias that appears most often in a bubble is Overconfidence Bias. This is also the easiest bias to understand when assessing others, but not as easy to diagnose on ourselves. Overconfidence Bias is an unwarranted trust in our own ability to assess situations, predict outcomes, & analyze complex situations. Overconfidence Bias can take two forms: prediction overconfidence & certainty overconfidence. While both have some Cognitive characteristics, it is our own emotions that place this in the Emotional category, which makes it particularly difficult to overcome completely.

Prediction overconfidence has some roots in the Cognitive Error, Anchoring & Adjustment as well as Representativeness in that our predicted outcomes all tend to stem from a certain starting point, average, or other base value and then we assign probable outcomes based on what we believe the current environment most closely represents. The problem with Overconfidence Bias is the distribution of likely outcomes tends to be both too narrow and skewed too heavily to the positive side. Remember, in 25 years of following the market I’ve never seen a major Wall Street firm predict either a Bear Market or a Recession. The “worst” they will predict is a “below average” year.

Certainty overconfidence is where investors really get into trouble. We tend to assign unreasonably high probabilities of positive outcomes. We believe we have more knowledge than other market participants. The certainty can actually be made much worse if we perform research that is tainted by such Cognitive Errors as Confirmation Bias, Conservatism, Anchoring, Framing & Representativeness. Many studies have been performed and my own experience confirms that the longer a market rises, the more overconfidence bias prevails in our assessment of the financial markets. I will never forget what one of my college professors told me (remember I went to college in the 1990s) — “Don’t confuse brains with a bull market“.

The problem is as the market goes higher and the confidence investors have that there will not be a bear market, portfolios tend to shift far too heavily to risky assets. Few people understand that regardless of the current market environment, simple statistical theory tells us in any given year the S&P 500 can lose 35-40% (at a 95% confidence level). Overconfidence bias ignores this fact as we believe (fill in the blank) means we will not have a bear market any time soon. It is CRITICAL we all understand the consequences of Overconfidence and go back through both our own abilities to identify market trends (keeping in mind all of the Cognitive Errors, especially Availability (Recency) Bias & Hindsight Bias). Markets can & will lose money and those losses are likely to be far higher than what we predicted and most of the time more than we are comfortable with. Again, don’t confuse brains with a bull market.

8. Self-Control

This bias is just what it sounds like. I’m sure many of us have looked back with regret at the times we’ve lost self-control and made bad decisions. Essentially self-control is the combination of what happens when we do not offset our behavioral biases with a well thought out plan. SEM’s focus is on structuring portfolios that help overcome each client’s personal behavioral biases.

9. Regret-Aversion

Nobody likes to be wrong, which is at the core of Regret-Aversion bias. This is probably the most commonly observed bias in my experience the last 20+ years. Along with Hindsight & Availability (Recency) Bias, both Cognitive Errors, Regret-Aversion Bias causes the most damage to long-term investment results. Regret-Aversion Bias is the fear of making a decision that turns out poorly. It is human nature to feel pain when we make wrong decisions. This fear can be paralyzing and can take on a few forms when it comes to investing.

The first is based on actions we COULD have taken. Closely related to Hindsight Bias the longer we see a decision we didn’t make (not buying or not selling) go against us the more painful it becomes. The more painful it is to us, the more memorable this “error of omission” is, which means the more we are sensitive to not making the same mistake again. This often leads to staying out of the market far too long if an investor didn’t sell ahead of large losses or staying invested in risky investments far too long if an investor previously missed a “buying opportunity”.

The second form of Regret-Aversion Bias is based on actions we actually took. This “error of commission” has been found to be much more painful to us than an “error of omission” which can lead to being mentally paralyzed in making investment decisions. Investors that sold too early often will refuse to sell regardless of riskiness in the future. Conversely investors that bought into a market at a top are likely to refuse to invest in that market for a significantly long period of time. Regret-Aversion causes us to vow to “never make that mistake again.”

There are two consequences of Regret-Aversion Bias:

1.) Overly conservative investments that do not meet long-term investment objectives. This is the result of the pain of past losses due to our decisions (buying near the top and/or riding the market all the way to the bottom.)

2.) Herding behavior. One way humans deal with Regret-Aversion is to simply do what everybody else is doing. We are under the assumption that if a lot of other people are investing in a certain asset class they must know more than we do. This is also a psychological way to prevent being “wrong” or at least being perceived as being wrong. Without endorsing Keynesian Economics, this quote from John Maynard Keynes comes to mind:

“Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

We see Regret Aversion Bias most often during a bull market run. A majority of our clients joined SEM following the collapse of the stock market in 2008-2009. The pain of realizing those losses led most to choose allocations that are far too conservative to meet their overall return objectives. After the market has been going up for 5-7 years we see the other side of Regret-Aversion — Herding Behavior. In the late days of a bull market, lackluster fundamentals drive the market higher. The longer the market continues to go up, the more other biases combine with the regret of selling at the bottom or not getting back in to the market during recent corrections.

ILLUSTRATIVE PURPOSES ONLY — PLEASE SEE DISCLAIMER AT BOTTOM OF PAGE

In the later years of a bull market it is dangerous to follow the herd. A long-term approach is CRITICAL to success. Much better opportunities for gains will appear on the other side of the bear market. To take advantage of these opportunities we must be PATIENT. The best way to deal with Regret-Aversion and many of the other biases is to look at the long-term data. By studying the data we can see how different investments perform in different parts of the market cycle. Studying the data tells us our income programs (Income Allocator, Tactical Bond, and Dynamic Income Allocation) typically have relatively low returns for several years at the end of the market cycle. However, those same strategies typically lose significantly less than most other investments during the subsequent bear market. Unfortunately too often we see people letting their behavioral biases take over which leads to unfortunate outcomes. The circumstances in each of the market cycles have been different, but the dynamics have not.

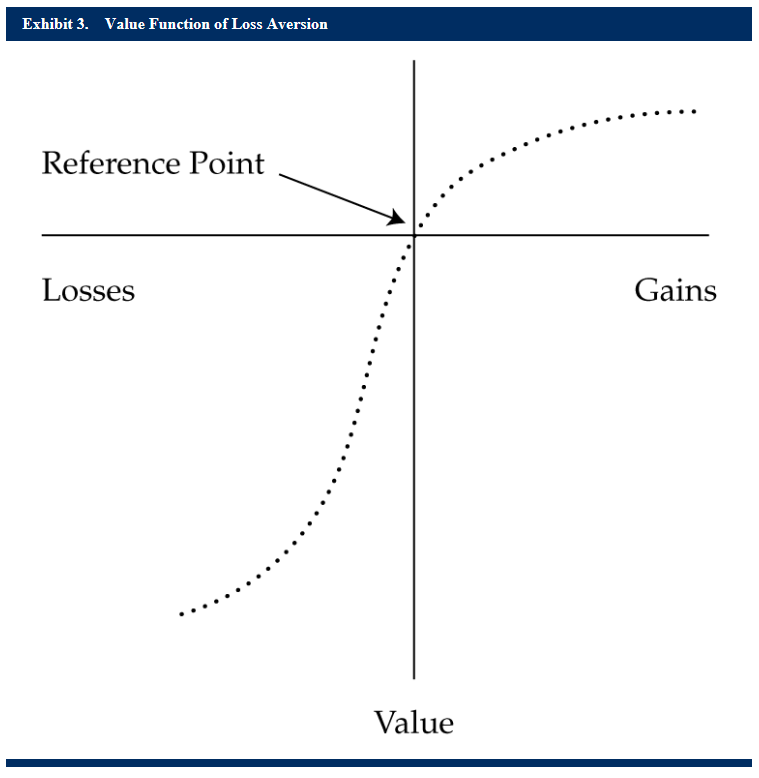

10. Loss-Aversion Bias

Loss-Aversion Bias was first identified in 1979 by two psychologists studying prospect theory. It is something we have mentioned quite often as numerous other studies have also identified this bias. Essentially Loss-Aversion Bias tells us losses are far more powerful than gain psychologically. This chart from the CFA Level III Chapter on Emotional Biases illustrates the “utility” of gains and losses.

This aversion causes investors to behave in ways that can have serious consequences on their portfolios. In a buy & hold stock & bond portfolio, studies have shown investors tend to hold on to their losers far too long under the belief their decision was not a “loss” until they “realize” actually sell the investment at a loss. On the other side, they tend to sell their winners far too quickly out of fear their profits may erode. This typically leads to undiversified, highly risky portfolios.

Loss-Aversion Bias also can tie in closely with the Cognitive Errors, Framing, Anchoring, & Mental Accounting which then creates Myopic Loss Aversion. Investors are often their own harshest critiques and also their own worst enemy. They often “evaluate” their decisions on short periods of time (often every time they receive a statement or at the end of a calendar year.) The “Framing” of the period often does not allow for a fair evaluation of the investment (unless it covered an entire market cycle). Some investments are designed to be “diversifyers” that help limit the downside, while others are designed to provide strong upside, but may have significant downside. The overall portfolio is designed to meet LONG-TERM risk/return characteristics but the time-frame may make either look unfavorable depending on when it is evaluated. In addition, investors tend to “Anchor” their account value to the last evaluation period (again often the last statement). With that value in mind, they mentally consider that money to be the new baseline for their account (mental accounting). If the account moves below that value the investor may panic and want to lock in the “gains” by moving to “safer” or “better” investments. Again, depending on the time-frame, this will likely lead to an undiversified portfolio that does not come close to meeting the investor’s overall risk-return objectives.

For more on our Behavioral Approach to portfolio construction, click here.