A necessary war?

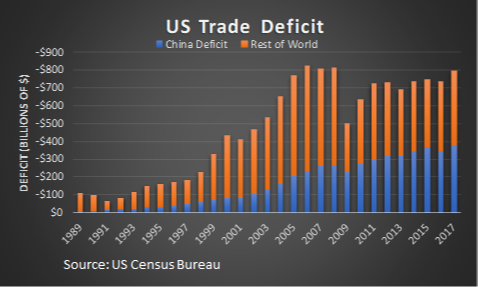

The stock market has been on shaky ground lately as the United States is escalating the potential for a heated trade war with China. China represents 47% of our total trade deficit. The US announced the initial shots in March, which was matched by China with their own tariffs (even though China already charges heavy tariffs on US goods). Wall Street has been hitting the airwaves to warn about the dire consequences of a trade war. While short-term they are correct, the more important issue is if this is a necessary change in our trade polices.

For years we’ve talked about why the Fed’s models and other economic theories have seemingly stopped working. We’ve gone through the worst economic recovery in the history of our country where GDP growth only surpassed the long-term average a couple of quarters. The reason is simple — the US economy is not a closed system. We are spending far more than we make and we are importing far more than we export. We have essentially borrowed money from others to finance our lifestyle and willingly allowed cheap foreign products to be sold in our country.

Nobody knows what the ultimate outcome of the heated trade discussions will be. What we do know is something needs to change and while that can cause some short-term losses in the market, shifting towards a closer balance of trade would be quite healthy for the US over the long-term. That said, a lot of the rhetoric back and forth could just be negotiating tactics, so making investment decisions based on these headlines can be detrimental to your long-term financial health.

Markets move in cycles

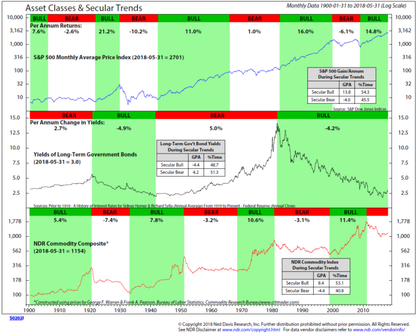

Our brains are programmed to assume recent experiences will continue into the foreseeable future. (The psychological term is Availability Bias, which we’ve always called “recency” bias). When evaluating the investment markets this can have serious implications on your long-term success.

This chart from Ned Davis research highlights bull & bear markets in stocks, bonds, and commodities. All markets move in cycles. The end of the cycle will not be known until we have the benefit of hindsight, which makes using a scientific approach to investing that much more important.

Trade impact on economy

With the escalating trade tensions, many people have been lamenting about the retaliatory tariffs being threatened by our trading partners. While this may have a short-term impact on the economy, the chart to the left shows the impact exports & imports have on our overall economic growth.

Imports from other countries SUBTRACTS from our growth (because we are paying somebody outside the US). The Exports we have do not offset the cost of the imports, which is why the US is attempting to level the playing field. Over the long-term this needs to be more balanced, even if it hurts in the short-term as the economy adjusts.

Are you willing to gamble?

“Buy low, sell high” is the advice we all have heard. Few people understand how to define “low” or “high” and often end up buying high & selling low as our natural human emotions get involved. The easiest way to measure the level of the market is to divide the value of the stock market by the underlying earnings. (How much you pay for the profits of the companies in the index?) Due to the volatility in corporate profits, Professor Robert Shiller, a Nobel Prize winning economist proposed a way to “normalize” earnings. This has become known as the “Shiller P/E”.

This chart from Credit Suisse supports the “buy low, sell high” advice. Whenever the Shiller P/E was at a low starting point, the returns tended to be higher for the next 3 years. The higher the Shiller P/E was at the point of purchase, the more random the returns were. All of the large losses (above 20%) occurred with the Shiller P/E starting point above 20. It is currently above 30.

Anyone jumping into the market now are essentially buying high and hoping to sell even higher. I’d much rather remain patient and wait for the much easier opportunities that will come when valuations cycle back to more normal levels.

Download / Print version of the newsletter

What is ENCORE?

ENCORE is a Quarterly Newsletter provided by SEM Wealth Management. ENCORE stands for: Engineered, Non-Correlated, Optimized & Risk Efficient. By utilizing these elements in our management style, SEM’s goal is to provide risk management and capital appreciation for our clients. Each issue of ENCORE will provide insight into investments and how we managed money. To learn more about ENCORE Portfolios, please contact your financial advisor.

The information provided is for informational purposes only and should not be considered investment advice. Information gathered from third party sources are believed to be reliable, but whose accuracy we do not guarantee. Past performance is no guarantee of future results. Please see the individual Program Reports for more information. There is potential for loss as well as gain in security investments of any type, including those managed by SEM. SEM’s firm brochure (ADV part 2) is available upon request and must be delivered prior to entering into an advisory agreement.