Market participants have focused so long on what the Fed will or won’t do they seem to have forgotten how to actually analyze investments. Bank of America Merrill Lynch (BAML) CEO Brian Moynihan summed up the current state of the market —

“Where else is the money going to go, with dividend [stock] yields exceeding sovereign [bond] yields? The money is going to go into the equity markets because they’re looking for return.”

That may work for a while, but sooner or later fundamentals end up catching up

to the market. They always do. Buying something just because it has a higher CURRENT yield or return is actually one of the things we see happening in a bubble. “Investors” focus on returns and disregard the underlying risk. Here’s how the CFA Institute described a bubble (CFA 2016 Level III Curriculum, Reading 7, How Behavioral Finance Influences Market Behavior):

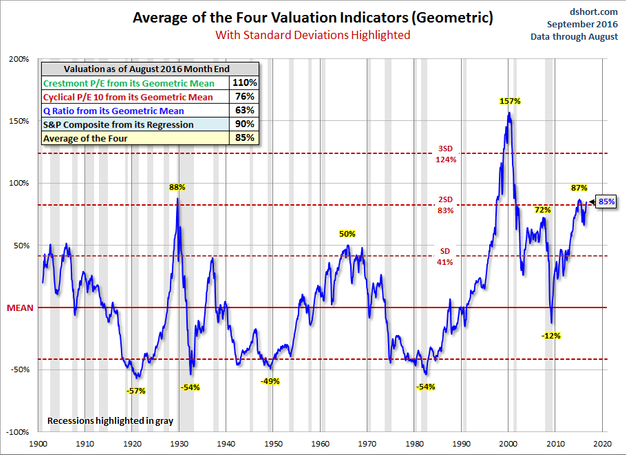

Bubbles and crashes appear to be panics of buying and selling. A continuous rise in an asset price is fueled by investors’ expectations of further increase; asset prices become decoupled from economic fundamentals. A more objective modern definition specifies periods when a price index for an asset class trades more than two standard deviations outside its historic trend.

Bubbles and crashes are, respectively, periods of unusual positive or negative asset returns because of prices varying considerably from or reverting to their intrinsic value. Typically during these periods, price changes are the main component of returns. Bubbles typically develop more slowly relative to crashes, which can be rapid. Some bubbles and crashes will reflect rapid changes in economic prospects that investors failed to anticipate.

First, it should be noted that there can also be rational explanations for some bubbles. Rational investors may expect a future crash but not know its exact timing. For periods of time, there may not be effective arbitrage because of the cost of selling short, unwillingness of investors to bear extended losses, or simply unavailability of suitable instruments. These were considerations in the technology and real estate bubbles. Investment managers incentivized on, or accountable for, short-term performance may even rationalize their participation in the bubble in terms of commercial or career risk.

The overconfidence and excessive trading that contribute to a bubble are linked to confirmation bias and self-attribution bias. In a rising market, investors can have faulty learning models that bias their understanding of this profit to take personal credit for success. This behavior is also related to hindsight bias, in which individuals can reconstruct prior beliefs and deceive themselves that they are correct more often than they truly are. This bias creates the feeling of “I knew it all along.” Selling for a gain appears to validate a good decision in an original purchase and may confer a sense of pride in locking in the profit. This generates overconfidence that can lead to poor decisions. Regret aversion can also encourage investors to participate in a bubble, believing they are “missing out” on profit opportunities as stocks continue to appreciate.

There is a lot of significant information in that passage that ALL of us need to understand. Let’s stop arguing whether or not we are in a market bubble — while my subjective observations are we are indeed in a bubble, the data confirms this. We are back to the objective two standard deviations above the mean that is used to identify a bubble.

As the passage from the CFA Institute suggested, investors may know we are in a bubble, but they have either rationalized their participation in it or believe they will have the ability to identify when the bubble is bursting and will be able to avoid any losses. Let’s go back to the reading to see how it REALLY ends.

As a bubble unwinds, there can be underreaction that can be caused by anchoring when investors do not update their beliefs sufficiently. The early stages of unwinding a bubble can involve investors in cognitive dissonance, ignoring losses and attempting to rationalize flawed decisions. As a bubble unwinds, investors may initially be unwilling to accept losses. In crashes, the disposition effect encourages investors to hold on to losers and postpone regret. This response can initially cause an underreaction to bad news, but a later capitulation and acceleration of share price decline.

Look I get what advisors and investors are going through. The passage even discussed needing to participate in a bubble for “career success”. What is beyond frustrating to me is seeing a steady flow of clients that had a low willingness and ability to take risk leaving to find “higher returns”. I constantly scan the investment universe for available investments and finding a low risk investment that has better 3, 5, & 10 year returns than our Tactical Bond or Income Allocator is quite difficult. Even better, both have posted a strong 2016 and looking at current yields and spreads the trend should continue (so long as the Fed does not mess things up).

That does not seem to matter at this point. Investors are irrationally demanding even higher returns and either their current advisor will give it to them or they will find one that will (or simply start investing for themselves.)

If a client wants “lower fees and higher returns” they can get them right here with SEM. This is one of the primary reason we launched our Dynamic Programs. The difference between what SEM has to offer and most other places we are seeing the assets flow to is we still have a plan to handle the inevitable market crash.

To learn more about our Dynamic Portfolios, check out this Presentation.

Be sure to check out our Current Allocations page for a summary of our positions and the latest signals from our trading systems.