The stock market is back to its highest levels since early February. 10-year bond yields have climbed 1% since the start of the year and are at the highest level since early 2019. Last week we asked who was right – stock or bond traders. The stock market believes the Fed will not raise rates very quickly, inflation will not be a problem, and growth will rocket higher as soon as the war in the Ukraine is over. The bond market believes inflation is a major problem, the Fed has been far too slow in raising rates, and they will be forced to hike rates aggressively to stem inflation.

If we focus too closely on day-to-day or even week-to-week movements we can lose track of the big picture. Often times having patience to let the cycle progress without reading too much into short-term movements is the key to success.

Weekly Talking Points

- Even if the conflict in Ukraine ends quickly, we are back to where we were at to start the year – stocks are overvalued, economic growth is slowing, inflation is borderline out-of-control, and the Federal Reserve will be raising rates and pulling back stimulus.

- There are still more scenarios for additional risks than additional rosy scenarios for the stock market.

- The bond market is saying the Federal Reserve is way behind the inflation curve and is raising rates for them at a furious rate. Consumer sentiment is saying inflation is taking a huge bite out of future spending plans. Stocks are saying there is no risk in the market.

- If you were overweight stocks going into the year, any bounce should be looked at as a selling opportunity. We're well overdue for a real bear market.

- SEM's allocations are close to minimum exposure across the board. Unless your financial plan, cash flow strategy, or investment objectives have changed, there is no need for action on your part.

I don't really have a lot more to add other than some charts I've been watching. The frustration from the bond market over the Fed's lack of action in fighting inflation is jaw-dropping.

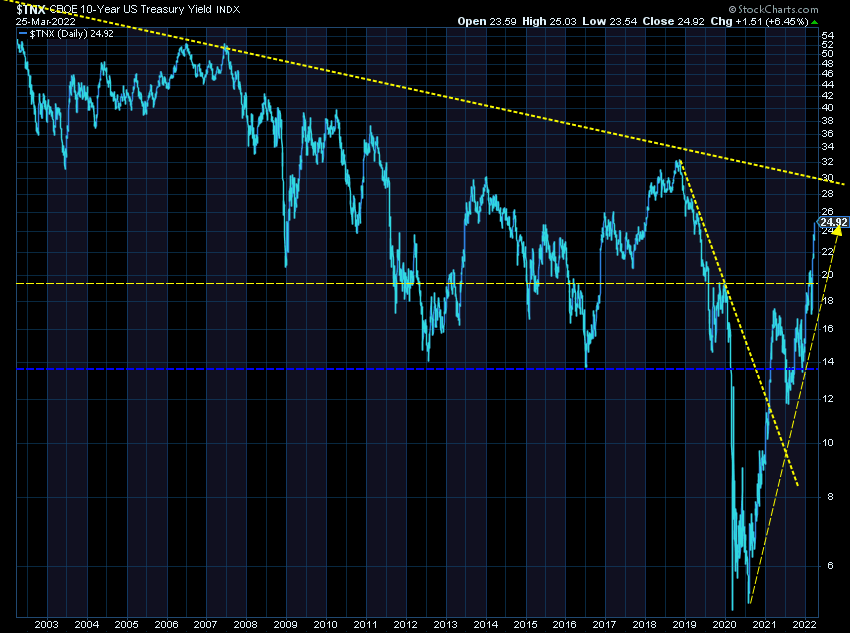

This daily chart of 10-year yields really highlights the sharp move.

It's tough to see on the long-term chart where the next level of resistance might be. Maybe the very long-term downtrend line around 2.8% or the 2013/2018 highs in the low 3% range.

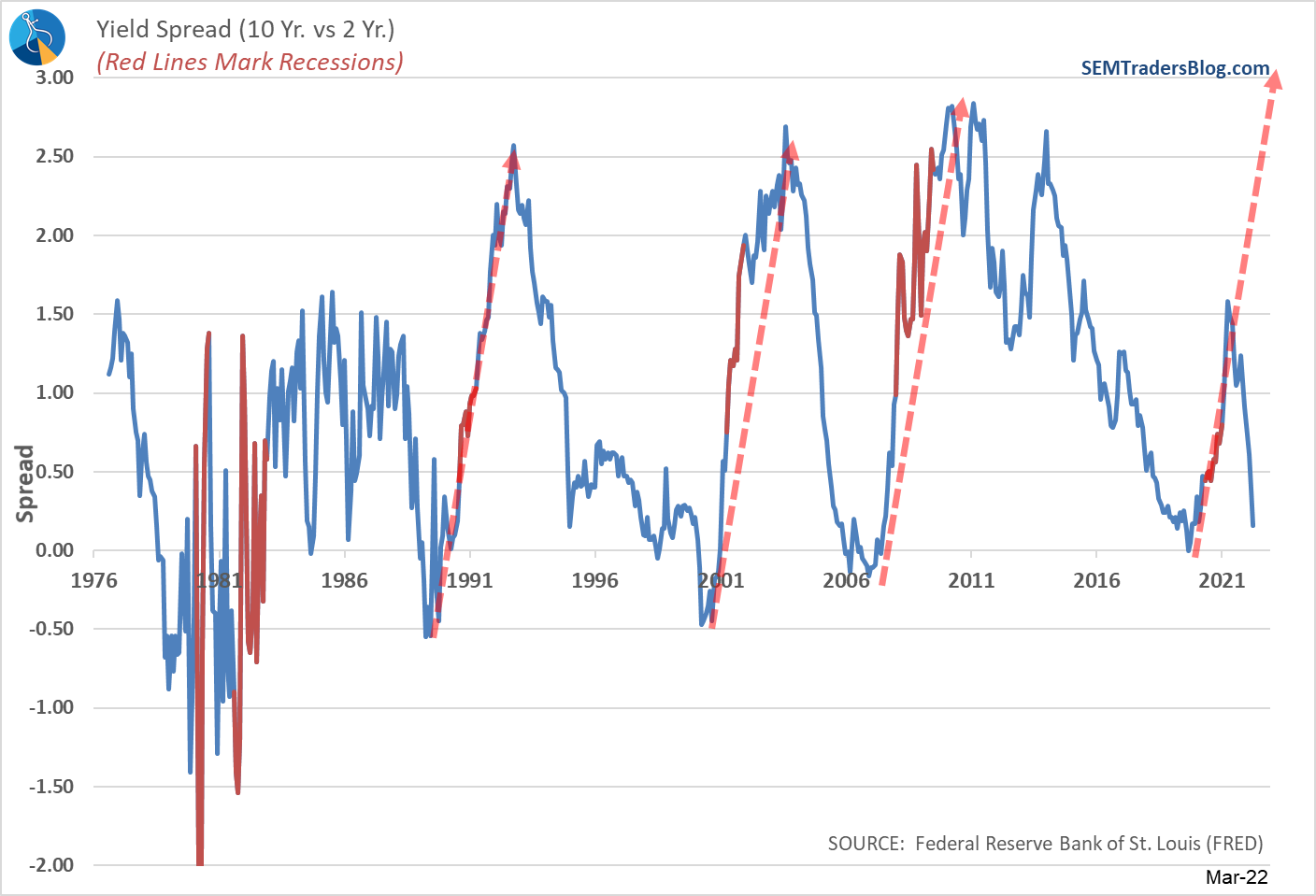

The 10-year to 2-year Treasury yield spread has been discussed a lot lately. It has historically been a very good indicator of a recession. What's been interesting this time is the fact 10-year yields are rising, just not as fast as 2-year yields. Normally, you see 10-year yields falling ahead of a recession. The other interesting thing is how short the yield cycle has been during the economic recovery. In early 2021 I showed this chart using duplicate lines during past expansion cycles.

We should have seen the yield spread move significantly higher. Instead, the Fed artificially kept rates too low and now we are dealing with inflation that could be running out of control.

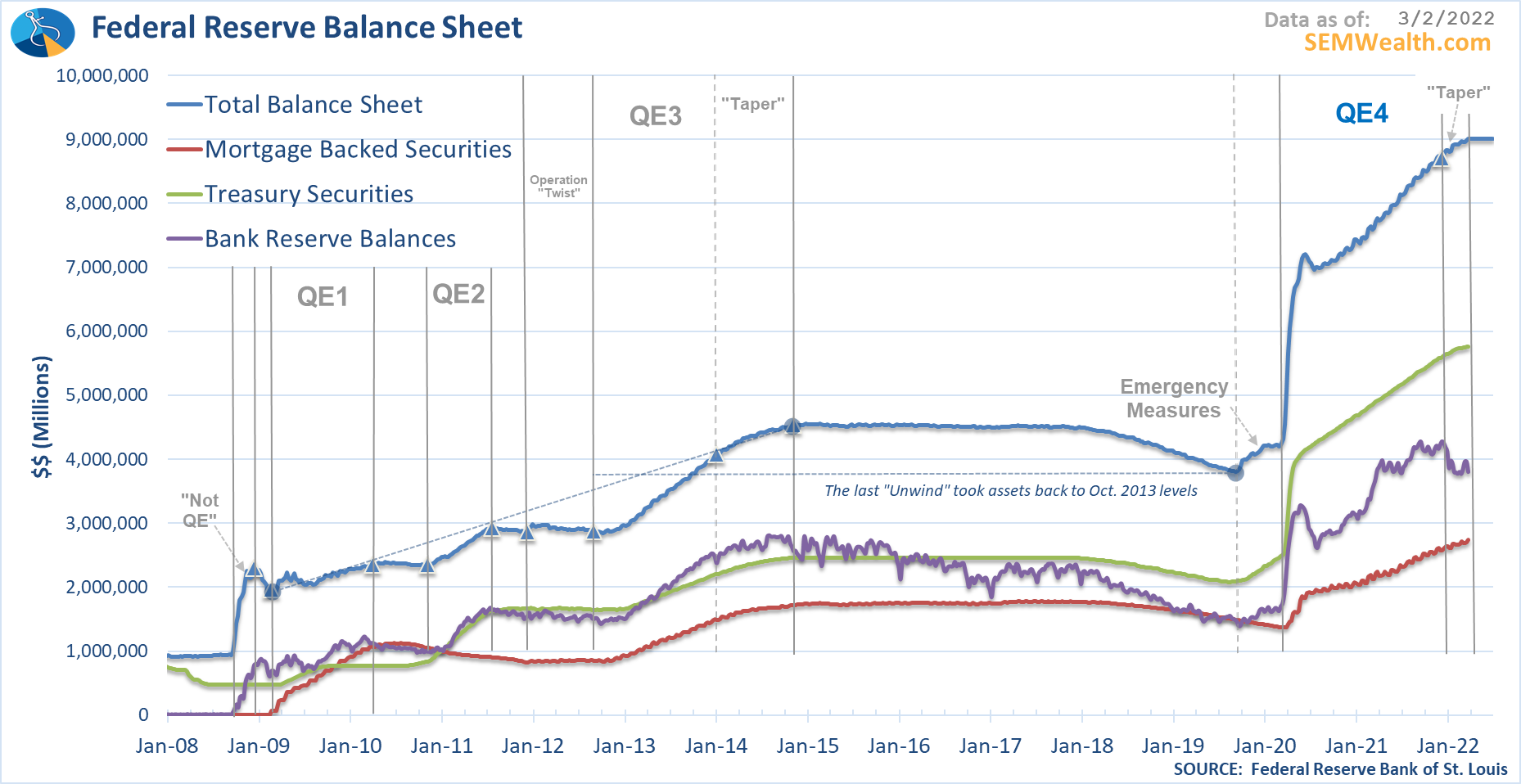

The Fed Balance sheet chart highlights the problem. The Fed has 3 mandates:

1.) Financial Stability

2.) Maximize Employment

3.) Price Stability

Consider:

1.) Banks posted record profits in 2021 and are expected to exceed those profits in 2022. I'd consider banks "stable".

2.) Unemployment claims last week were the lowest since the early 1960s. If you want a job you can get a job. I'd consider that "maximized".

3.) Inflation has been hitting 40 year highs each of the past 6 months. I'd consider prices NOT stable.

Why in the world has the Fed continued to print money to boost the balance sheets of the Wall Street banks? What do they know that we don't? What are they afraid of? I guess time will tell.

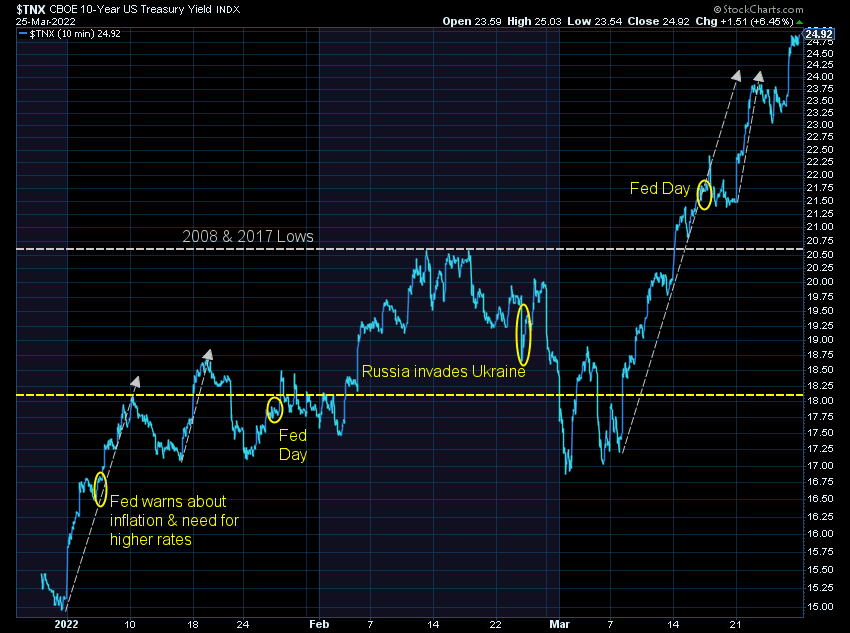

Turning to stocks, the move off the lows has been impressive. I added some notations to this chart to put the move in perspective. The market is well above where it was at following the January & March meetings as well as the Russian invasion. However, we still are a long way off from returning to where stocks were when the Fed first warned about inflation and the need for higher rates.

I continue to hear the perma-bulls say stocks are "undervalued". Their thought is given the high inflation levels bonds are a bigger risk than stocks. What they are missing is the fact once bond traders feel confident the Fed is taking inflation seriously, we could see a MAJOR rally in longer-term bonds. At the same time, we could see stocks hit hard.

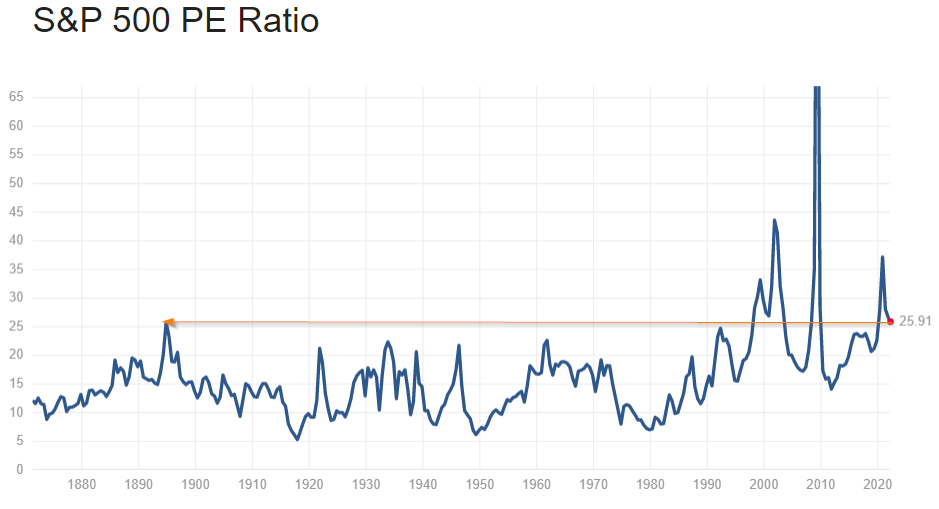

The P/E ratio has barely come down. It still remains at "bubble" levels.

From a fundamental perspective, high P/E ratios are acceptable if we have:

- High growth rates

- Low interest rates

My data and experience says the Fed is going to be forced to raise rates too quickly, which will cause growth rates to slow (likely to the point they cause a recession). Even without that, after dumping 25% of GDP into the economy in 2020 & 2021, it is highly unlikely we will see Congress send Americans any more stimulus. The growth we saw in 2021 is gone. We'll be lucky to resume the 2.5% growth we saw in 2019.

This means stock valuations MUST come down. Our systems will focus on the data and adjust accordingly. However, over the last 6 months of 2021 we saw too many people moving from conservative investments to more aggressive ones simply because they wanted to make more money. This rally should be looked at as a gift to "right-size" the risk in your portfolio back to where it should be.

For the rest of you, let this cycle play out. Stay patient and focus on making sure your investment allocations align with the financial plan, cash flow strategy, investment objectives, and your investment personality. If you want a quick check-up, start the process with our Risk Questionnaire.

This week will be busy on the economic data front, especially on Thursday and Friday. We also will begin to see quarter end rebalancing trades taking place which always cause volatility (and often counter-trend moves that could be reversed the following week). Stay patient and focus on making sure your investment allocations align with the financial plan, cash flow strategy, investment objectives, and your investment personality.