2022 was the worst year for stocks since the financial crisis. The year started with the worst performers of 2022 posting some impressive results the first 5 weeks of the year. After, the inevitable bounceback reality set in. There were plenty of risks in play – a looming recession, on-going Fed interest rate hikes to fight stubbornly high inflation, the debt ceiling, along with continued geopolitical risks from Russia and China.

Last week, seemingly every one of those risks disappeared, or at least that is what you would think with stocks rocketing past the highs of February, closing the week all the way back at the highs from last August. Are there still risks in the market? Looking at our economic model, the answer is an overwhelming 'yes'.

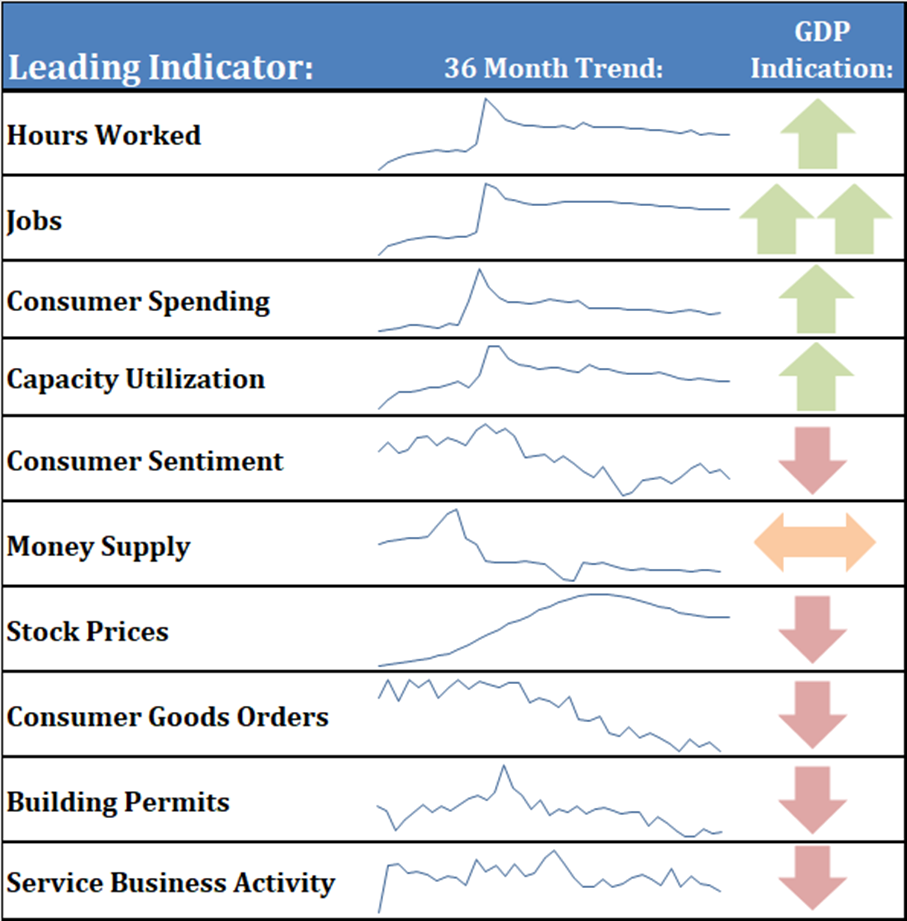

I won't go through every indicator this month as not much as changed since last month's update. You can get the full walk-through here:

The dashboard looks nearly the same as it has the last two months:

The labor market continues to hold the economy up. The "blowout" jobs report may be misleading, however. Economic shocks tend to skew the 'seasonal adjustment' factors, which could be causing misleading job numbers. The "headline" report which surveys employers the third week of the month showed strong job growth, yet the household survey showed a weakening labor market.

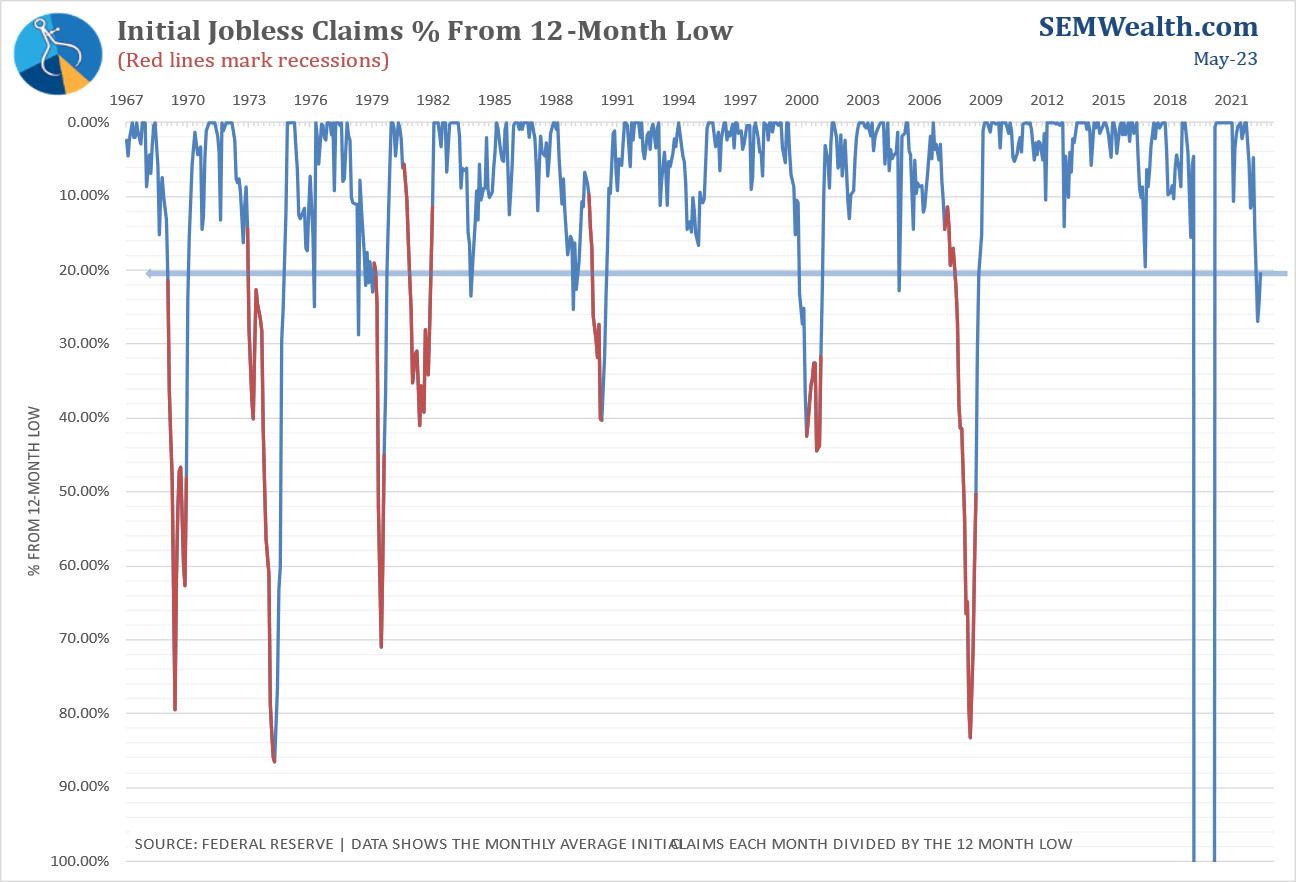

With those discrepancies, watching initial jobless claims will probably give us the best sign of which direction the labor market is heading. Claims are 20% up from the lows, which is typically a sign of a weakening labor market. I like this data because it comes from actual state unemployment office claims and is reported every week.

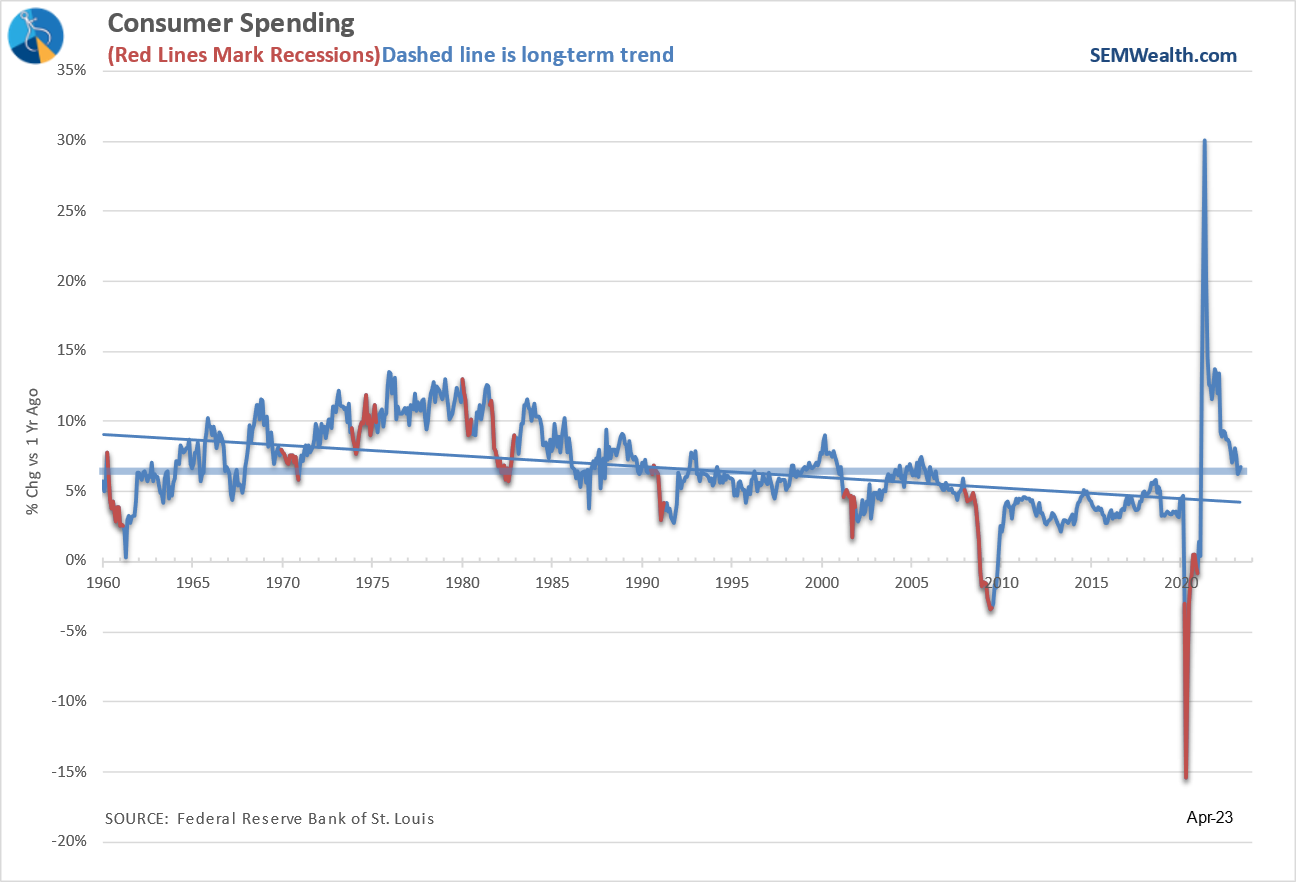

Consumer spending also remains quite strong. Clearly the Fed rate hikes have not put enough of a dent on spending overall to cause consumers to pull back.

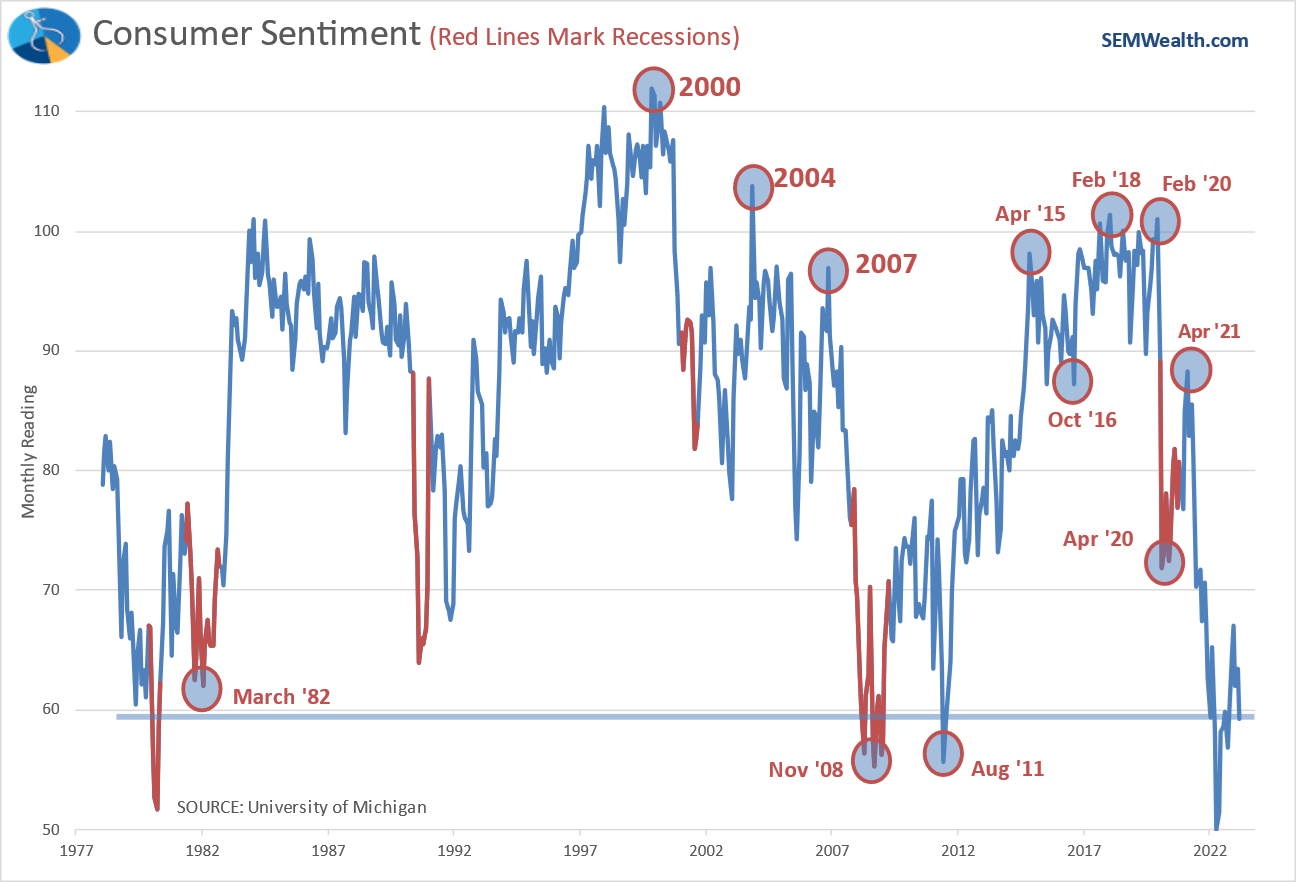

The consumer spending data is heavily skewed towards the top 20% of Americans, so there is sometimes a lag between when the 'average' American feels the strains of a weakening economy and when it shows up in the actual numbers. Sentiment remains quite weak and continues to point to less than optimistic consumer.

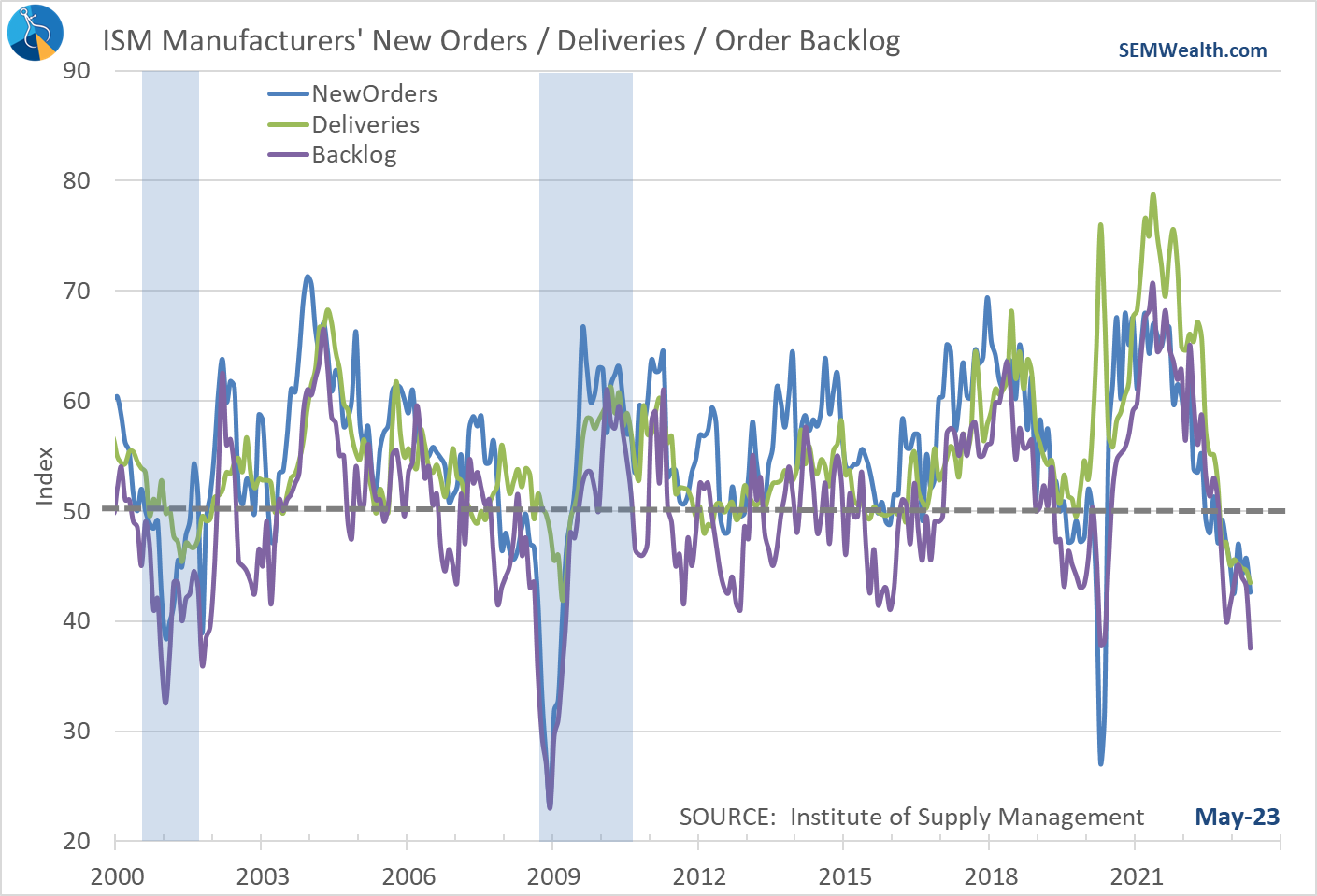

On the negative side, manufacturing continues to be pointing to a sharp recession. "AI" may be causing ridiculous rallies for technology stocks (and thus driving the S&P 500 higher), but it is not helping actual manufacturing in the US. Things were already bleak, but they became much worse in May.

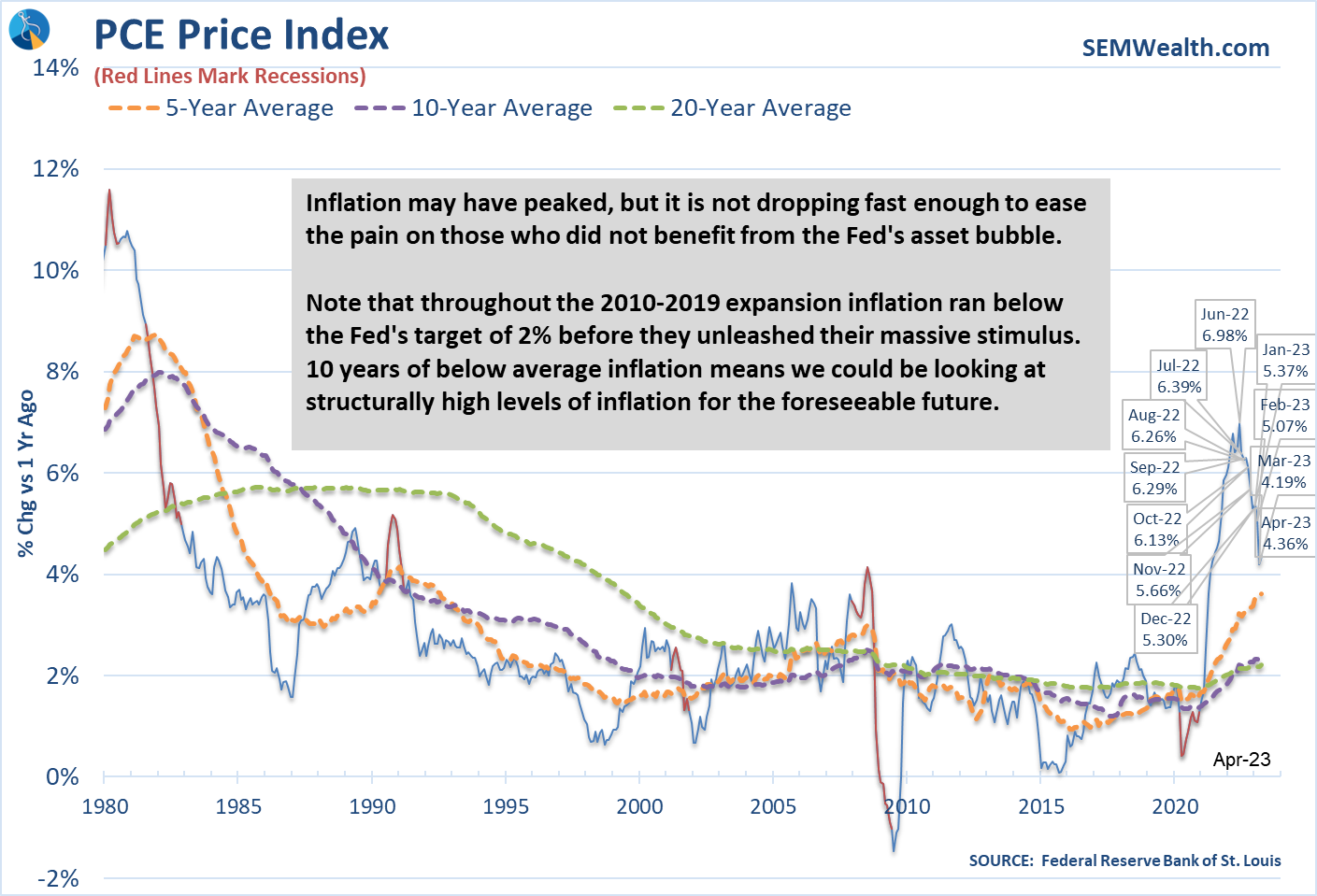

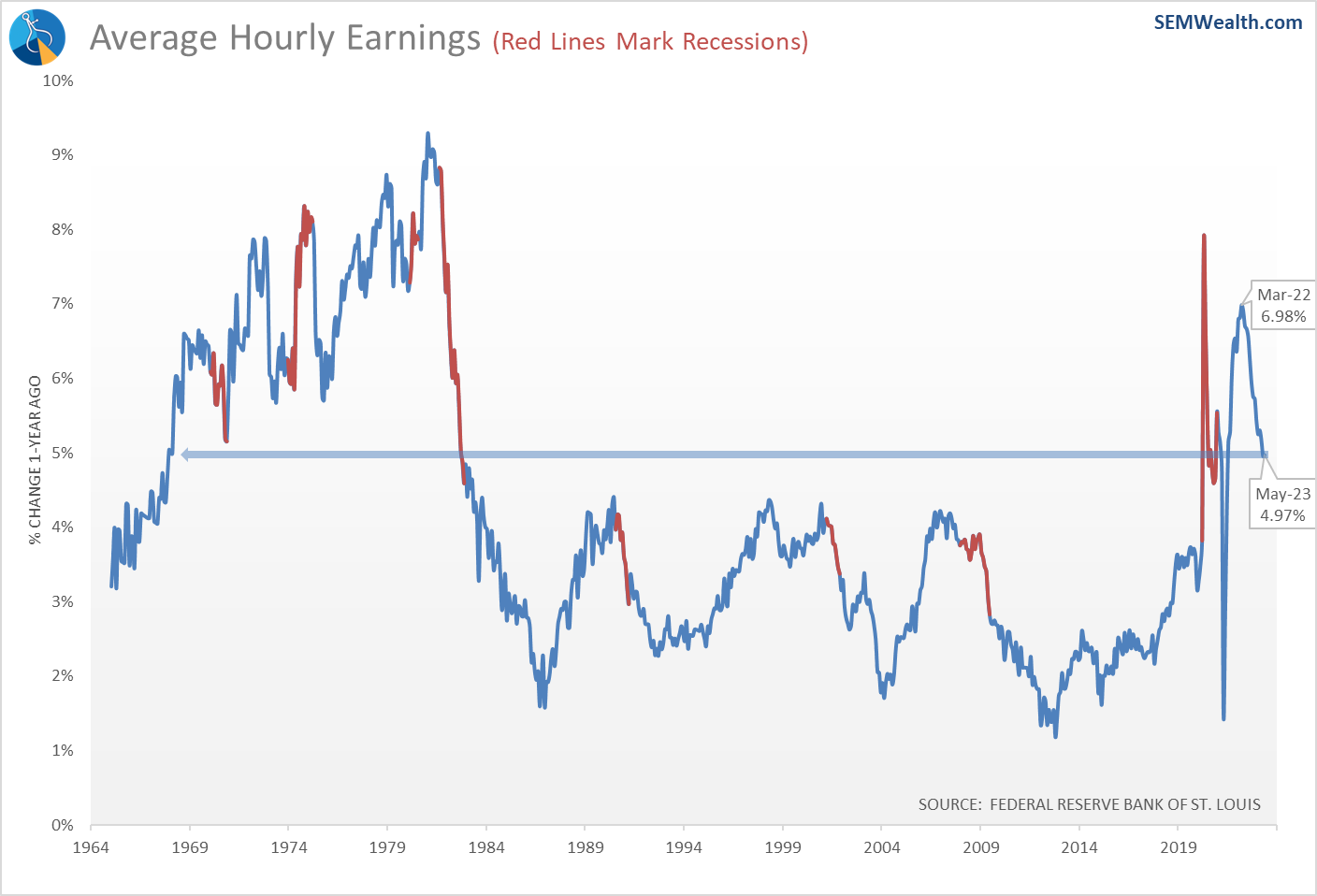

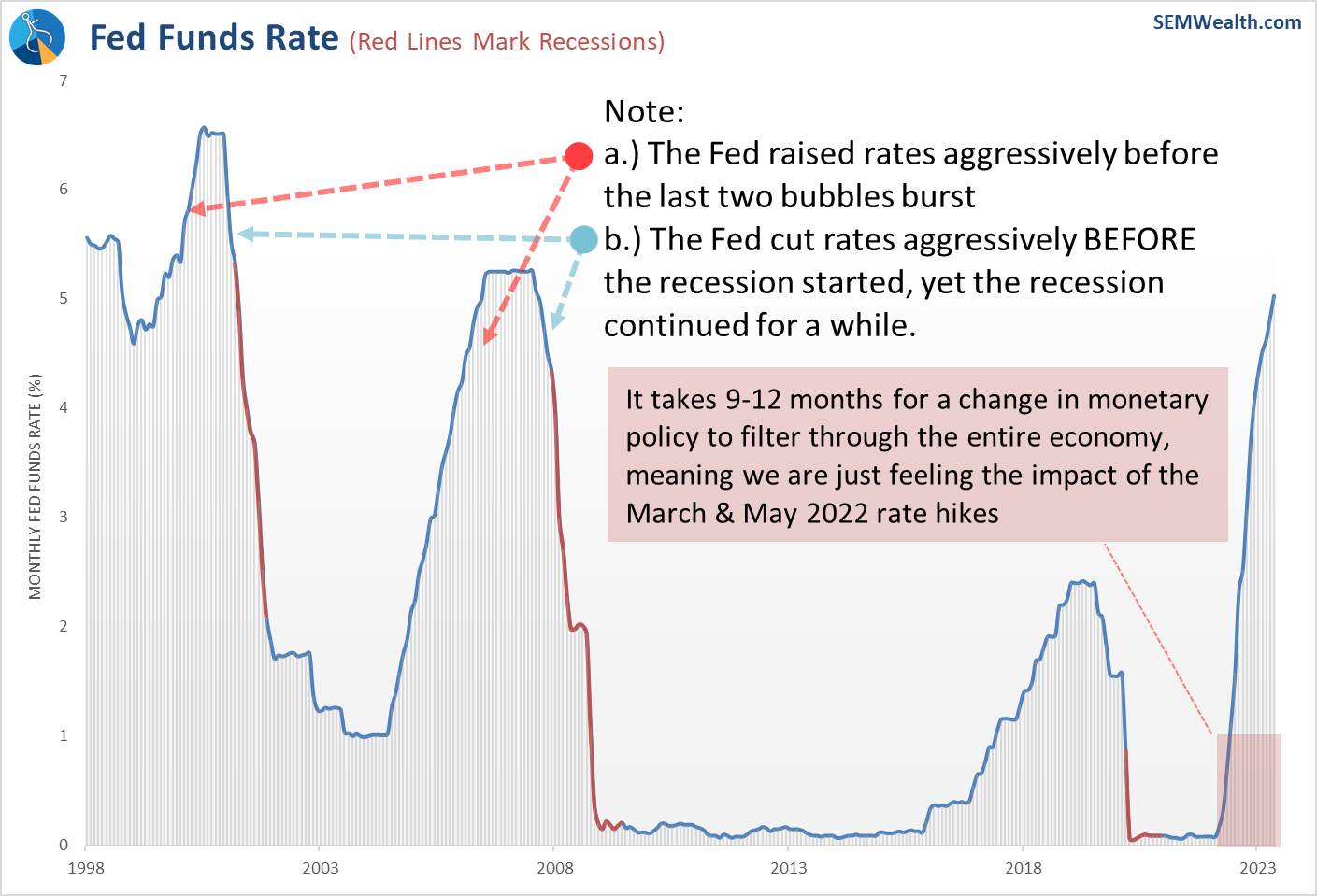

Many people seem to believe the Fed is done raising interest rates. They may pause, but two of the Fed's key measures of inflation, the PCE Price Index and the Average Earnings both ticked up in the last month. While one month does not make a trend, it does bring into play the chances of "stubbornly high" inflation becoming a story much sooner than most people thought.

The economy is just now feeling the impact of the beginning of the Fed's rate hiking cycle. We have a lot more hikes that still will be filtering through the economy.

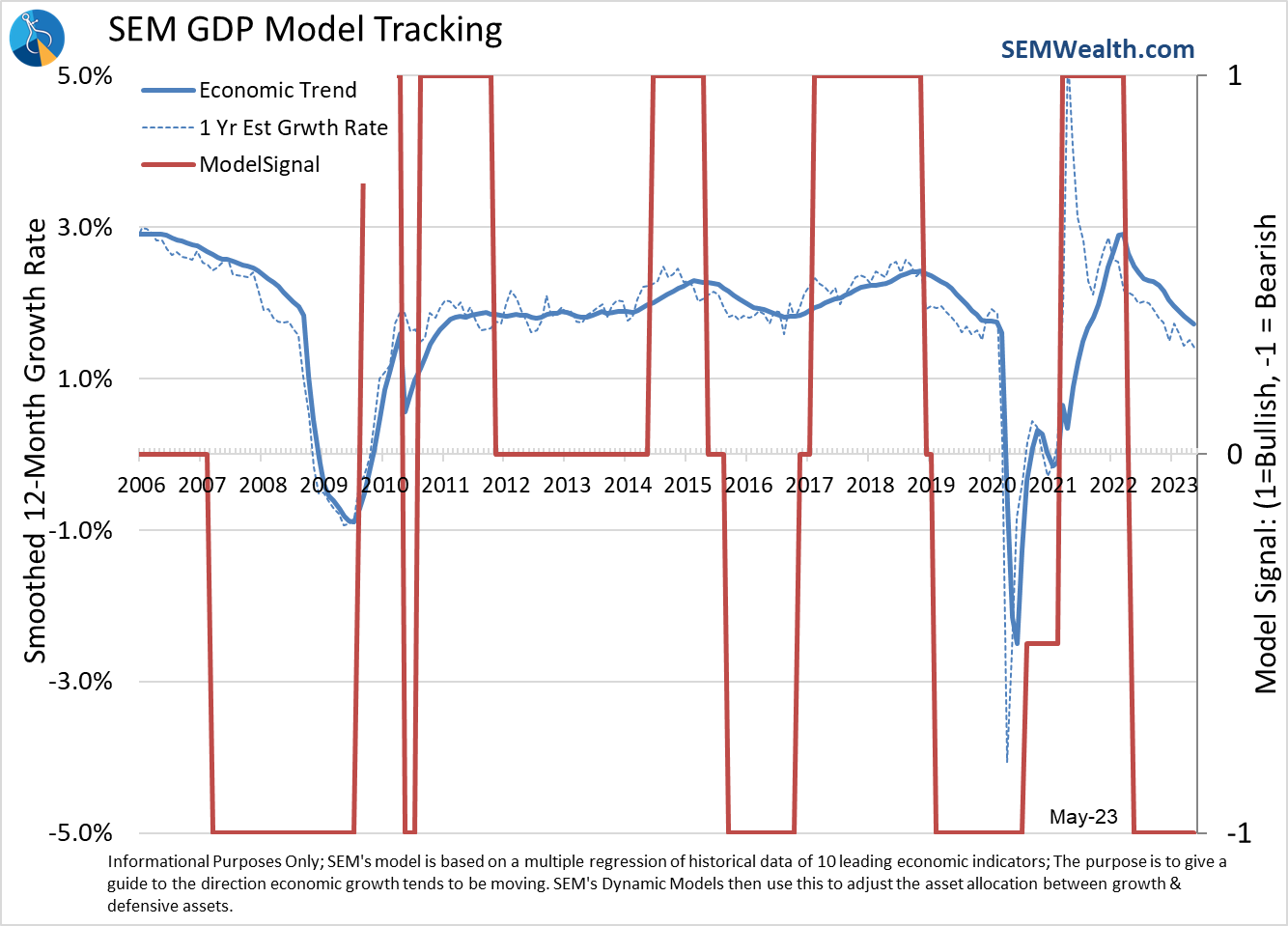

Overall, our model continues to show a steady decline in economic growth. It's not screaming for a devastating recession, but it most certainly is not signaling an easy environment for corporate earnings.

While earnings do not track economic growth perfectly every single year, over the long-run they do. Right now, the data is saying the economy is growing at BELOW AVERAGE rates (and heading to negative growth), yet the stock market is pricing in ABOVE AVERAGE earnings growth (with no drop in earnings). One of them is right and based on the track record of Wall Street analysts, I would bet our economic model is the one that is correct.

That means stocks are SIGNFICANTLY overvalued.

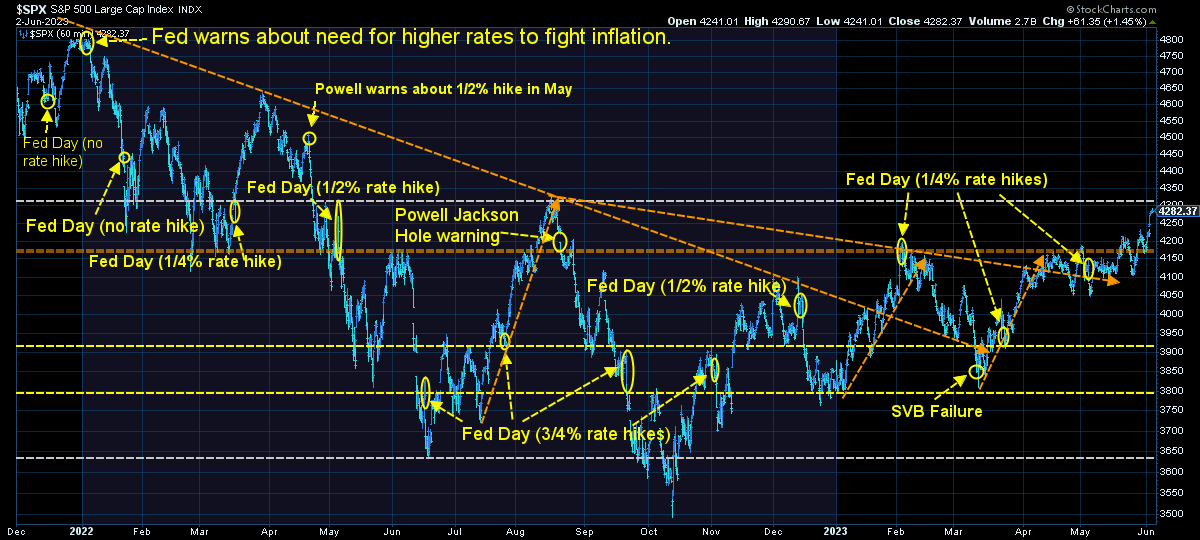

This doesn't mean they cannot continue higher for longer than we think is rational. After moving through the resistance level at 4200, the S&P 500 is up to the next level of resistance at the highs from last August.

I think this chart is telling as it highlights the key news surrounding the Fed. Note several times in 2022 – February, March, June, and then August we saw some furious rallies abruptly end with no real news. That is the risk we have right now. When investors believe there are no risks, simply things can cause the market prices to reset. Because there is no real fundamental support behind the current valuation levels, the reset can happen quickly and without warning.

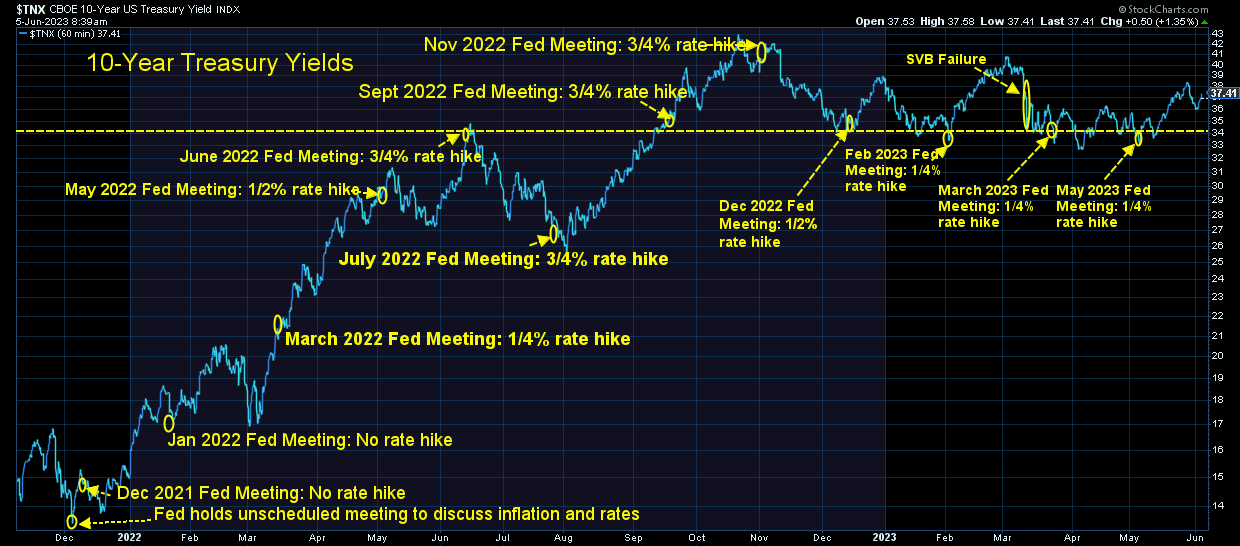

Interest rates have moved up throughout the current rally and will remain a headwind for corporate earnings. Unlike the stock market, the bond market saw the payroll report as a net negative and pushed rates higher once again.

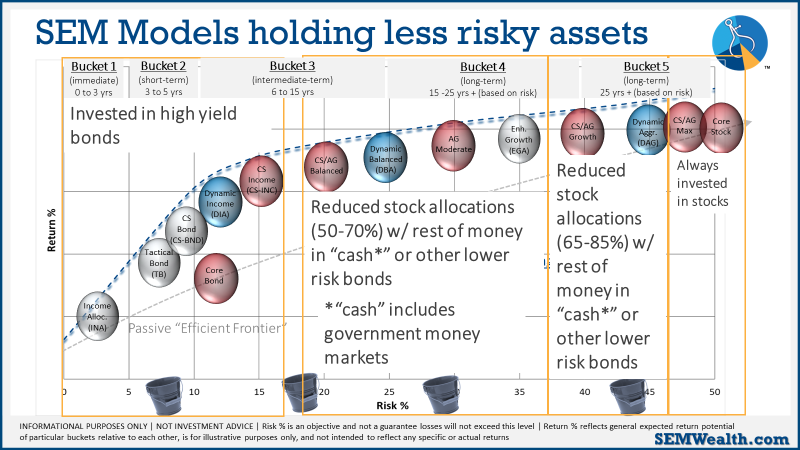

SEM Market Positioning

While those things above are certainly on our radar, we remain heavily invested. There were no changes (again) last week in any of our models. We remain mostly invested in high yield bonds in Tactical Bond, Income Allocator, and Cornerstone Bond. We remain "bearish" in the Dynamic models (reduced risk exposure based on our economic model), and right in between minimum and maximum exposure in our 'strategic' models.

Last week we were within a day of seeing several sell signals in our high yield bond models inside Tactical Bond, Cornerstone Bond, and Income Allocator. The rally on Friday gave us a little more wiggle room before the sell, but we will continue watching this closely.

This chart summarizes where we are as we enter the week:

As always, our models will change if the environment changes. For now, calculated, short-term risks are acceptable with the knowledge things could change quickly.

No matter what happens as we wrap up Part II of our Debt Ceiling Circus, our models are designed to monitor the overall TRENDS. If Wall Street gets concerned, they will tell their largest clients and we will see trends change in the market. Regardless of the reason, we only care about where the money is flowing (both in and out).

That said, we will be watching more closely than usual the underlying holdings in our funds to make sure they are not taking on abnormal risks. We will keep you posted if anything changes in our positions.

We are already in the heat of the election and it's only going to get more heated. With that I will continue to close with my primary piece of advice during times like this:

Do not let your political beliefs influence your investment decisions. The markets (and economy) do not always react the way you think they will based on the ideological talking points showing up in your media feeds.