Jerome Powell is a wizard. He has continuously been wrong yet whenever he says something the market (temporarily) believes he has the ability to predict our economic future. At the last Fed meeting in April, Chair Powell said the Fed was 'not far' from the first rate cut. At the conclusion of last week's meeting he said the Fed 'is not confident' inflation will reach their target. He couldn't give a timeline on rate cuts, but assured investors the next news is 'likely' not a rate hike. That apparently was enough to send the market higher and interest rates lower.

Now, don't get me wrong. Chair Powell has had some tremendously difficult situations thrown at him starting with the Trump tax cuts, then the pandemic, the solutions to the pandemic, and then 40 year highs in inflation. I don't know if any of the former Fed chairs could have done a better job than him. This doesn't mean he won't once again fail (as he did in 2021/2022 by waiting far too long to start hiking rates).

I'm not sure how much data the Fed had ahead of time, or what data they are even looking at, but some of the data inside our economic model is moving towards something Chair Powell is not a concern of theirs – stagflation (slow growth and high inflation). I'm not wanting to alarm anybody. This was the first month we've seen this happen and it could quickly revert back to where we were at the start of the year (strong growth and declining inflation). However, the data from last week is NOT a reason I would subjectively jump in and buy stocks.

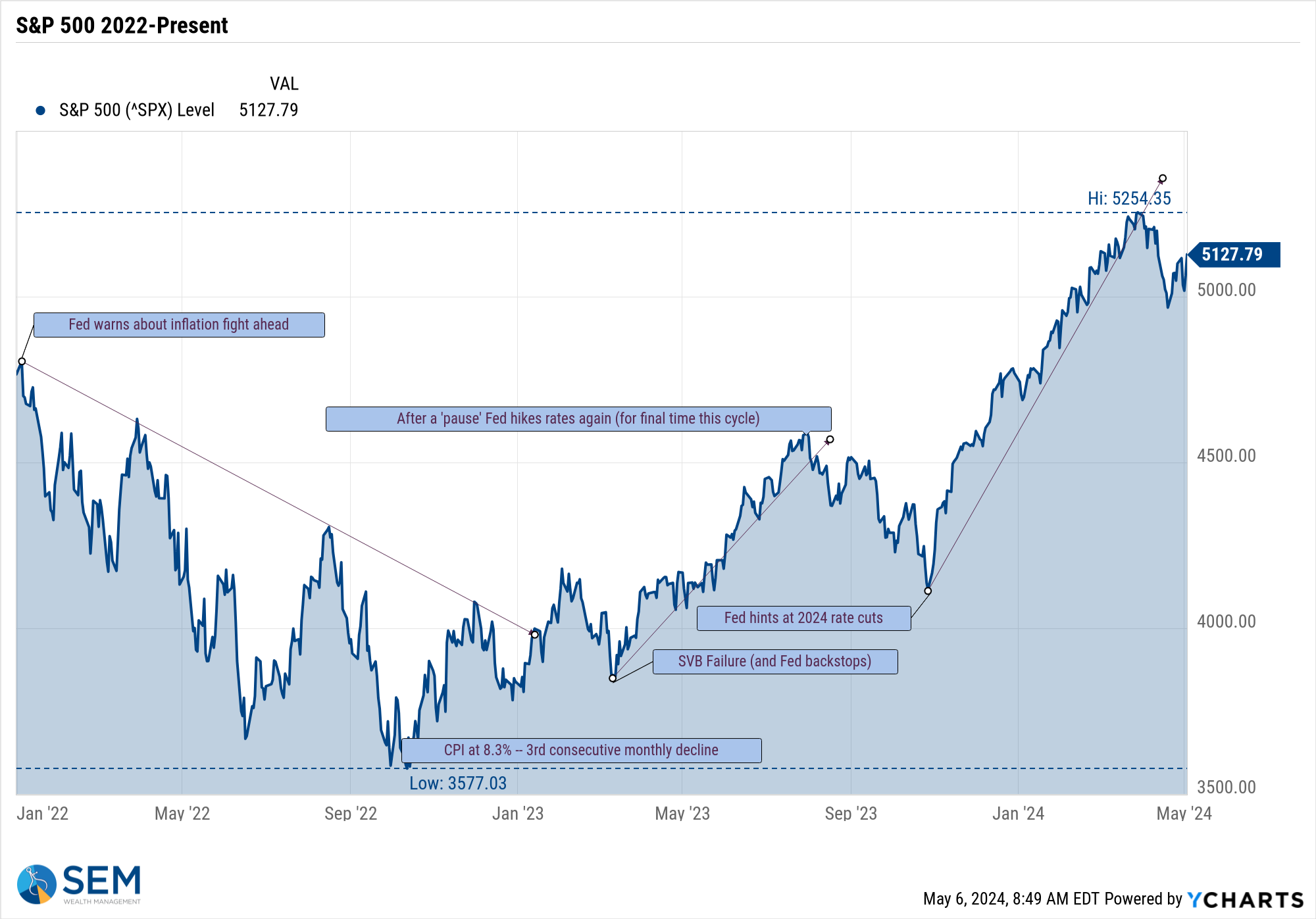

The news of the week was on Friday with the jobs report where a "disappointing" number sparked a rally for stocks (with the logic being this could encourage the Fed to cut rates).

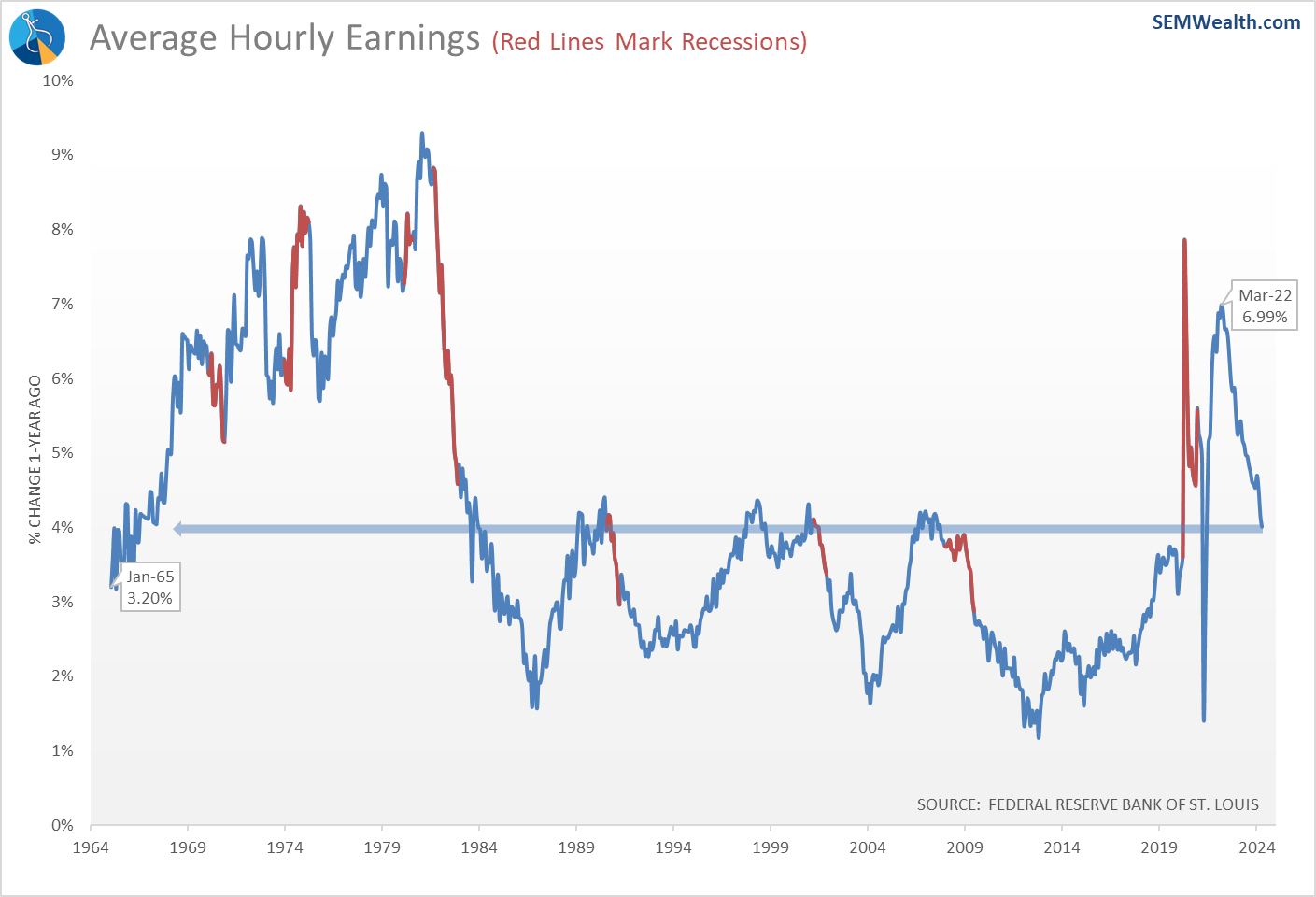

While the trend in average hourly earnings growth is DOWN, the problem is they are still growing at a 4% annual rate (which is inflationary).

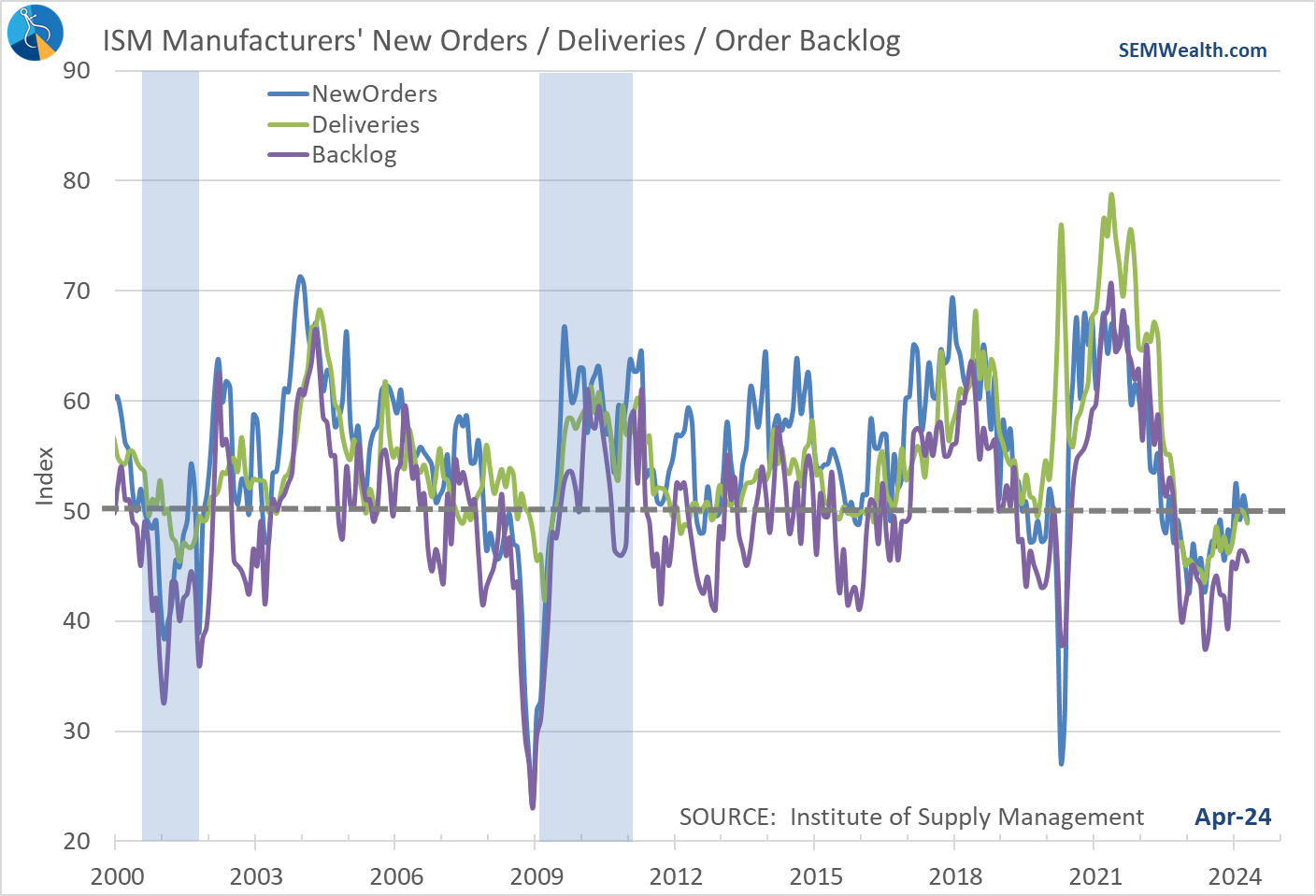

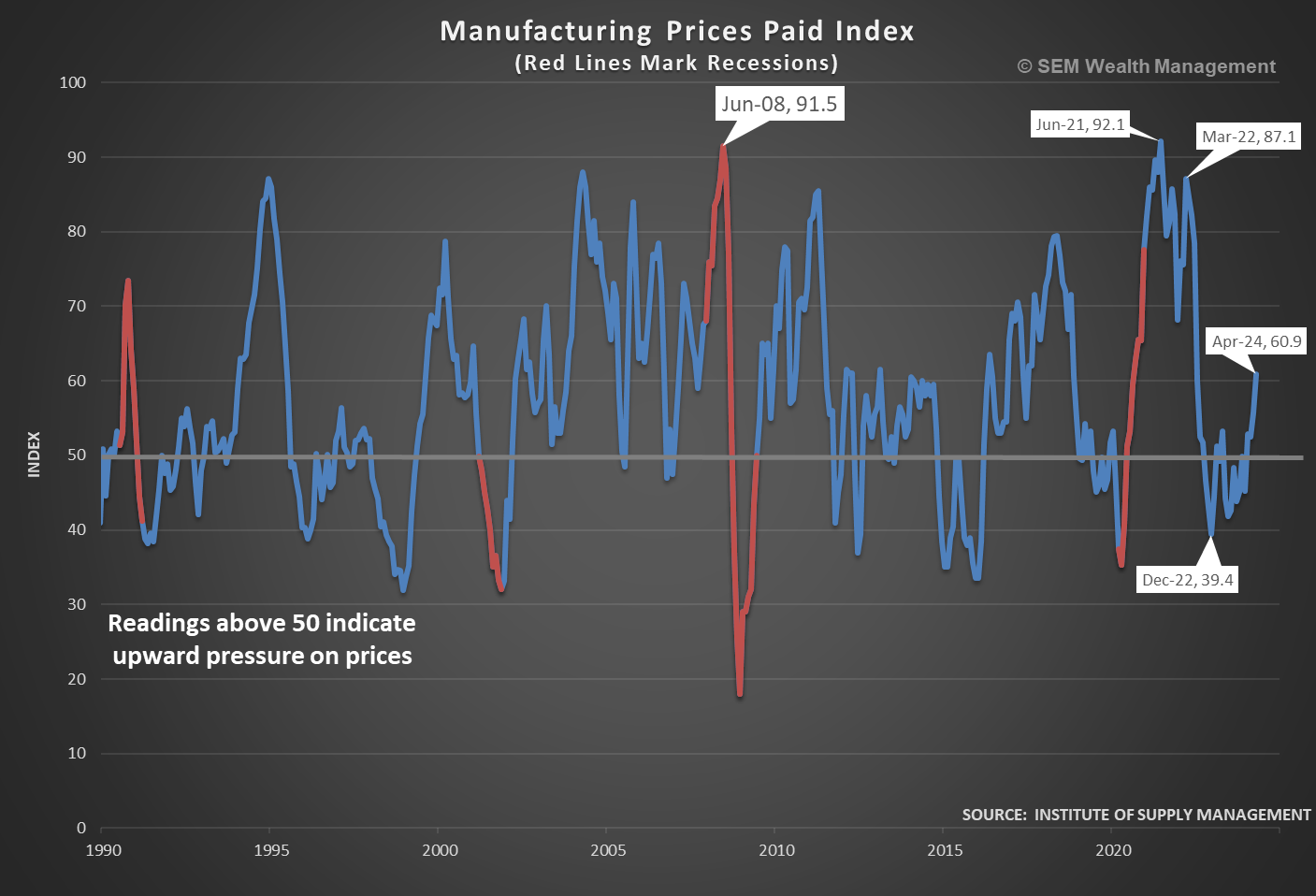

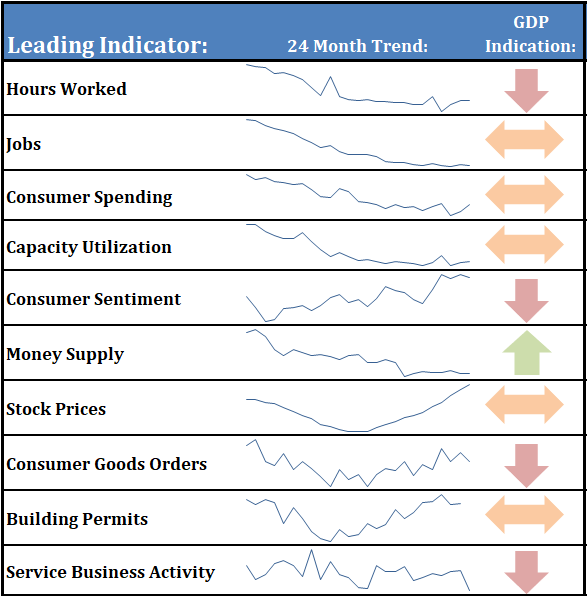

The bigger concern came from the ISM surveys. The manufacturing index dipped back into "contractionary" territory (below 50). All 3 of our leading index components are also pointing towards a contraction.

Despite the contraction, manufacturing prices paid skyrocketed in April

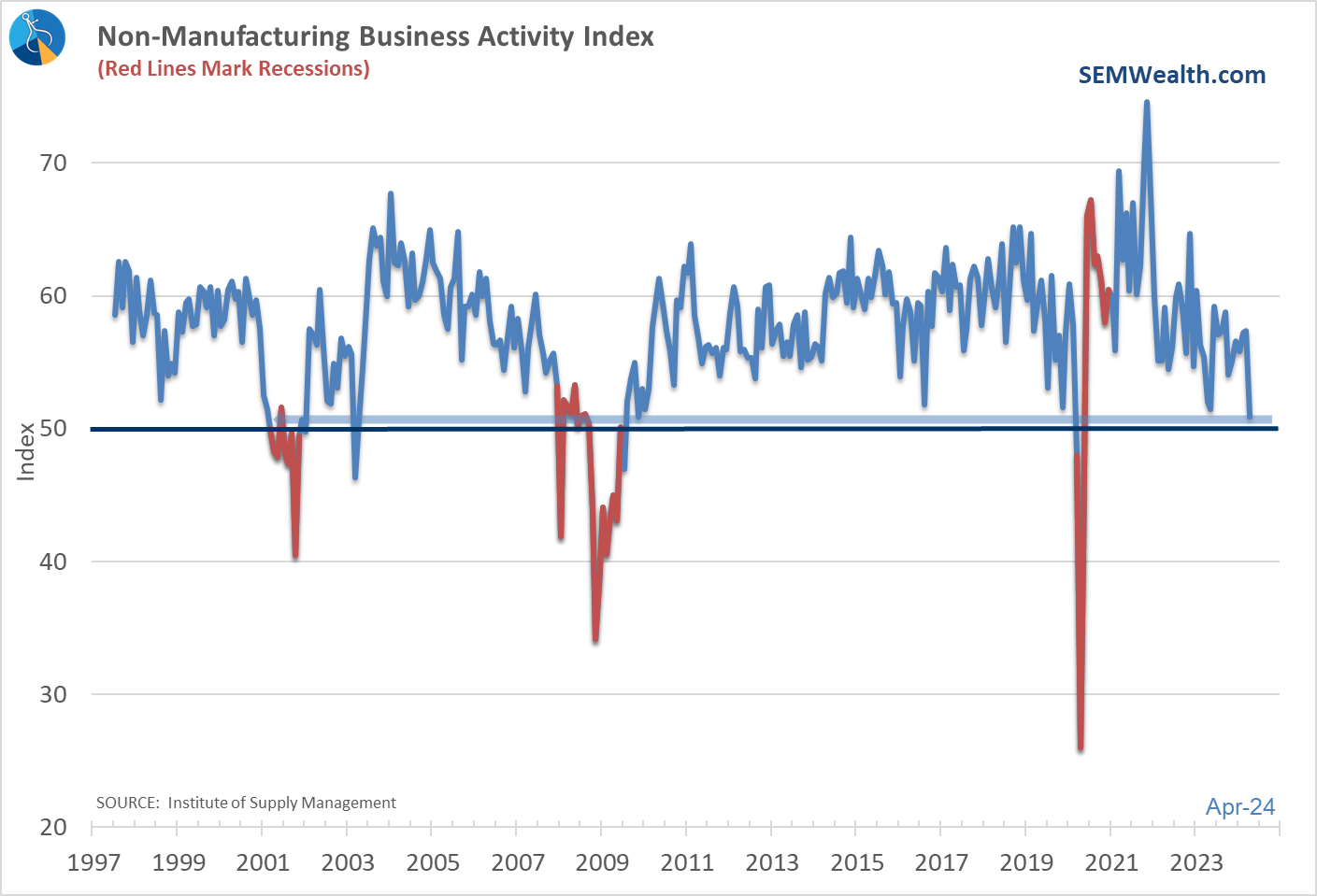

The services sector also showed a sharp drop in April. It is a whisker from being in contraction territory.

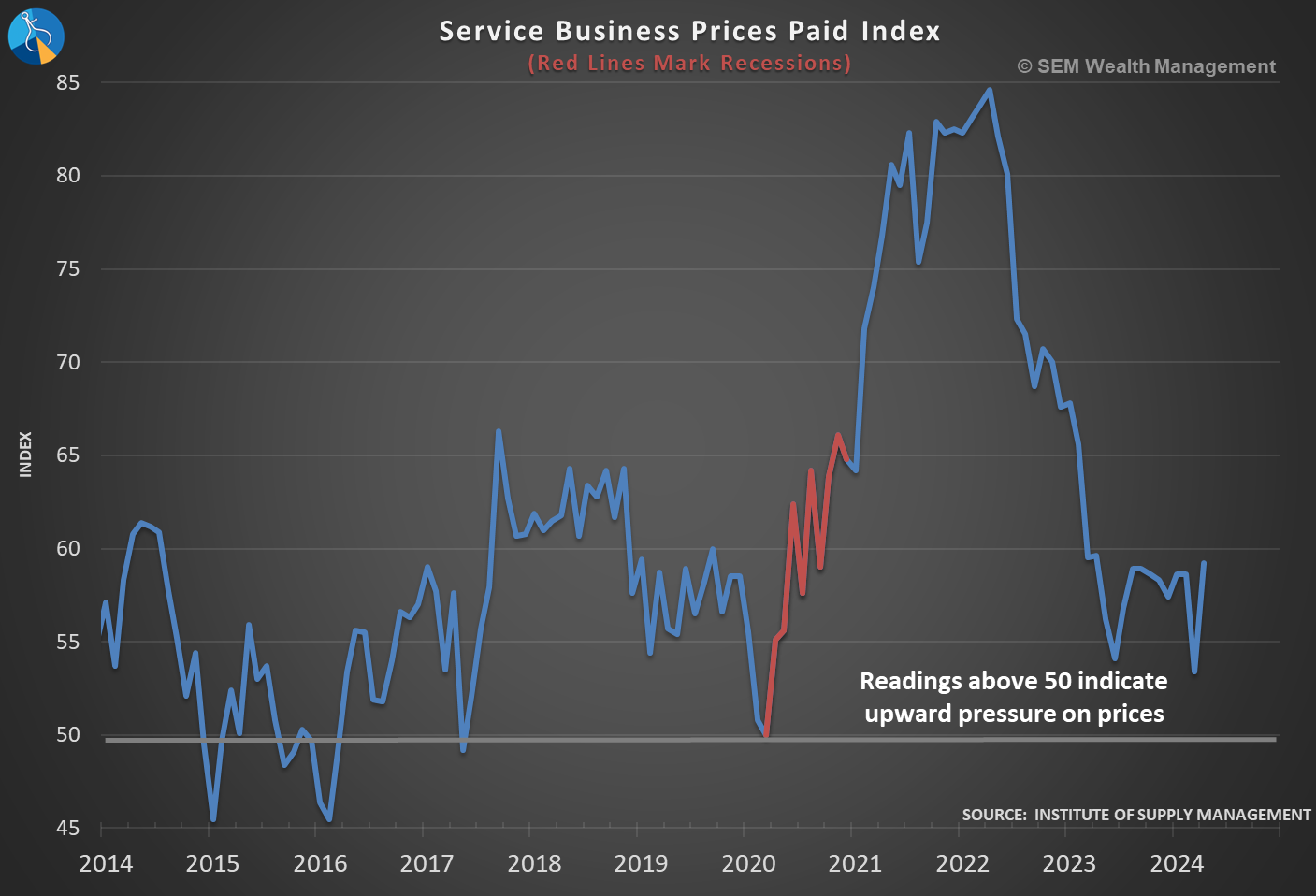

Like the manufacturing segment, service prices also jumped quite a bit.

Several other of our leading indicators went into "contractionary" territory last month, which combined with the "stress" we highlighted last week is a longer-term problem.

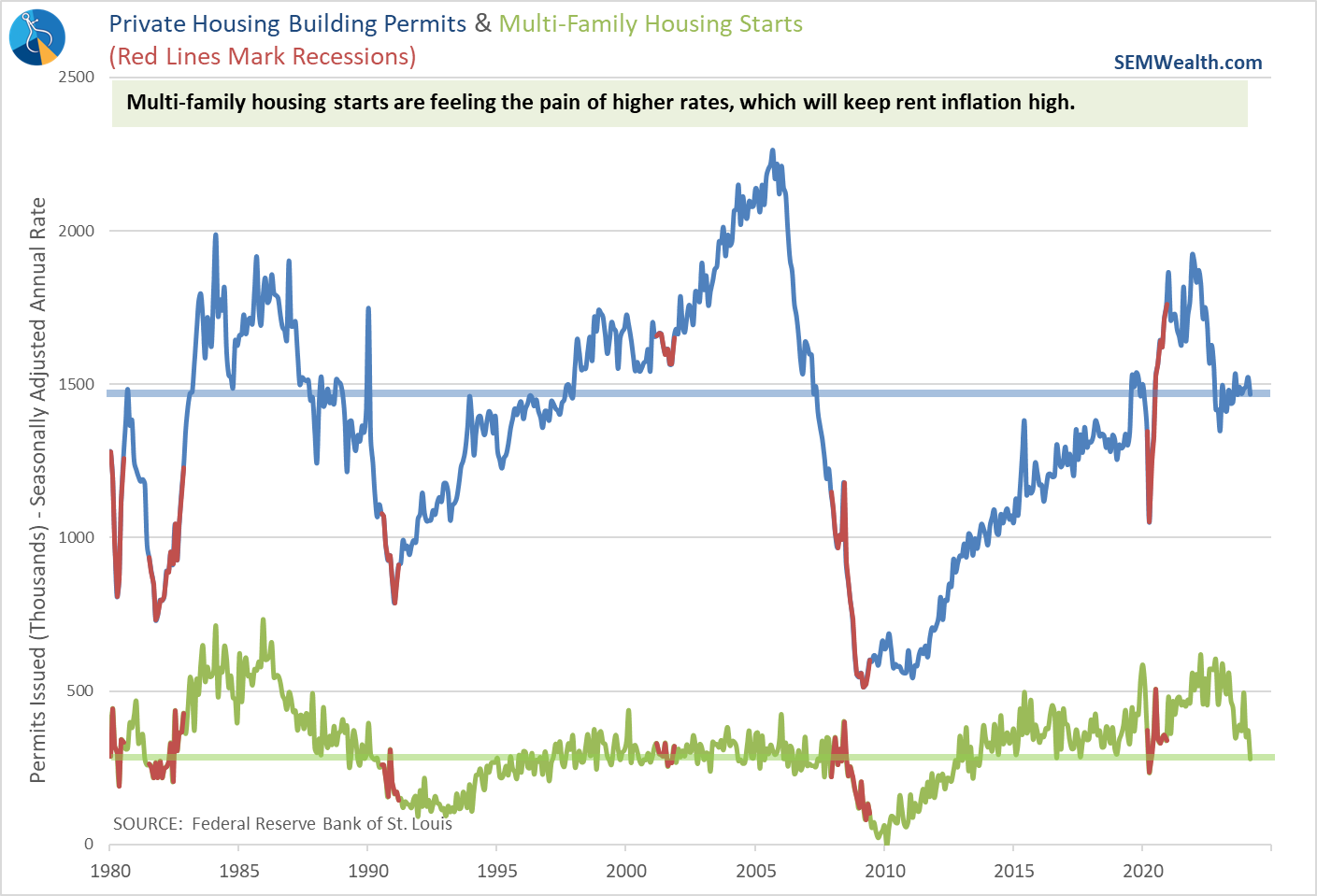

The other indicator that stood out to me was building permits. This indicator is feeling the pain of higher rates, but more importantly so are multi-family housing starts. This of course is a problem because there is a shortage of rental properties which will keep inflationary pressures high.

Overall our dashboard shows the stress in the economy.

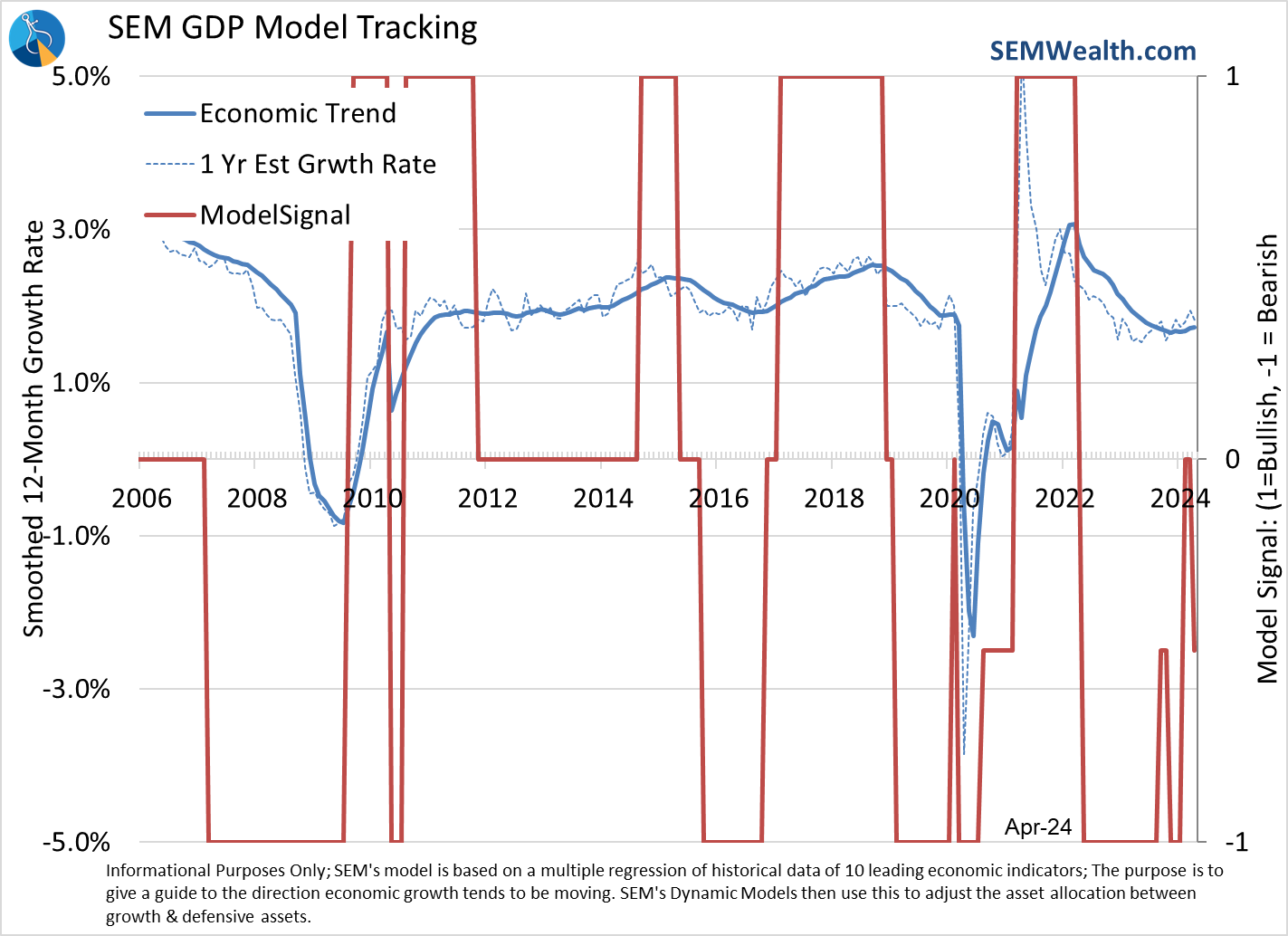

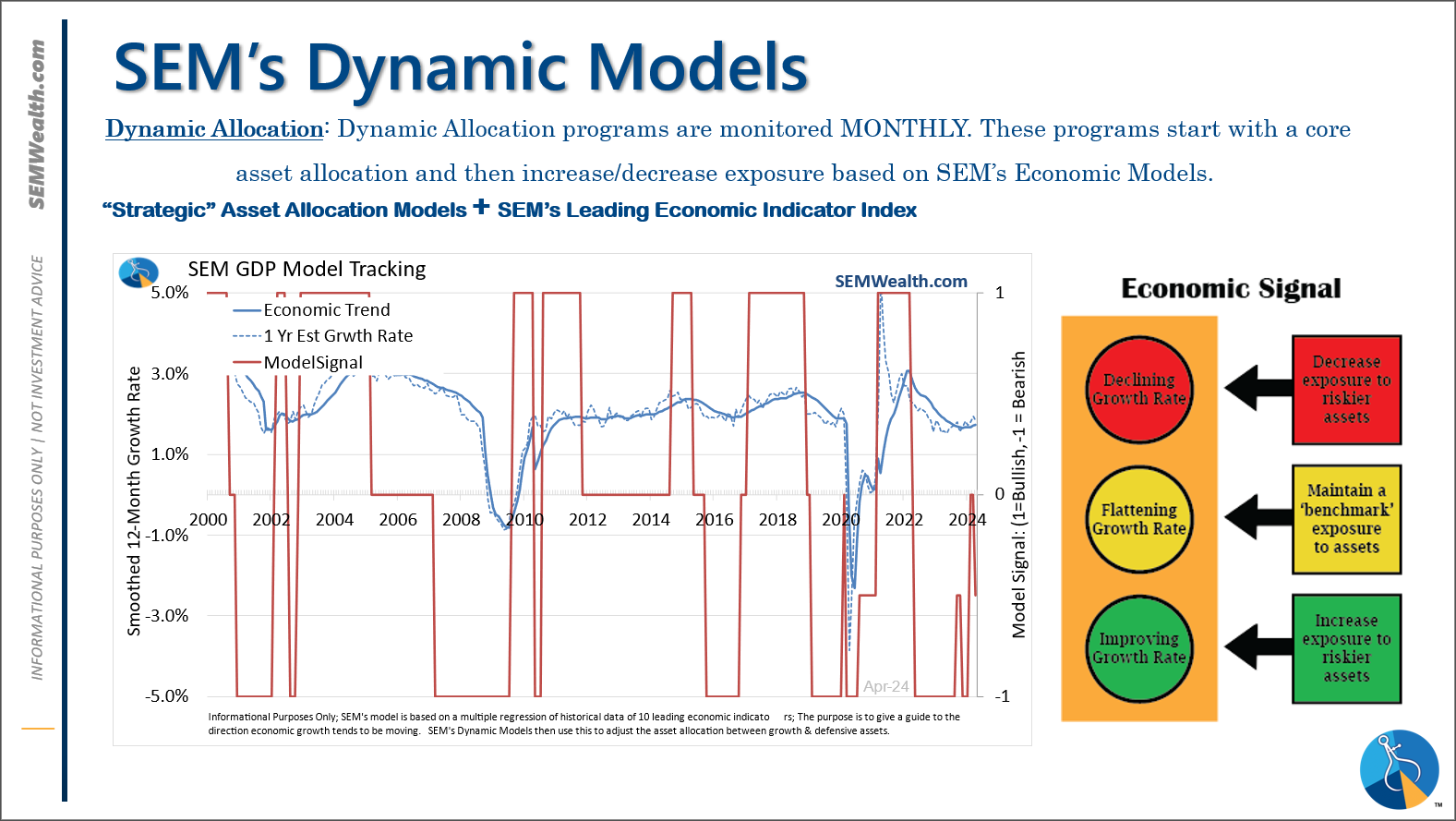

With so many of the indicators either flat or down it should be no surprise our economic model has swung a little bit bearish. (Note it's a smoothed trend model that moves in phases so it takes more than just one negative month of data to make a big change.)

This means cutting our dividend stock and small cap stock positions in half for our Dynamic Income models and Dynamic Aggressive models respectively. On the other side of things, the Tactical Fixed Income models are within a hair of triggering a buy. This is why I love SEM's combination of 3 different management styles. When things are uncertain you can see one model saying one thing and the other saying the opposite. It prevents one single idea from swinging the allocation in the wrong direction.

Which one is right? Time will tell.

Market Charts

The post-Fed rally helped moved the S&P 500 higher for the week. As mentioned above, the overall outlook for stocks on a fundamental basis worsened (slower growth, higher inflation levels) which should hurt valuations at some point. Note the September/October sell-off last year had several big rallies so we shouldn't take this rally as the end of the sell-off.

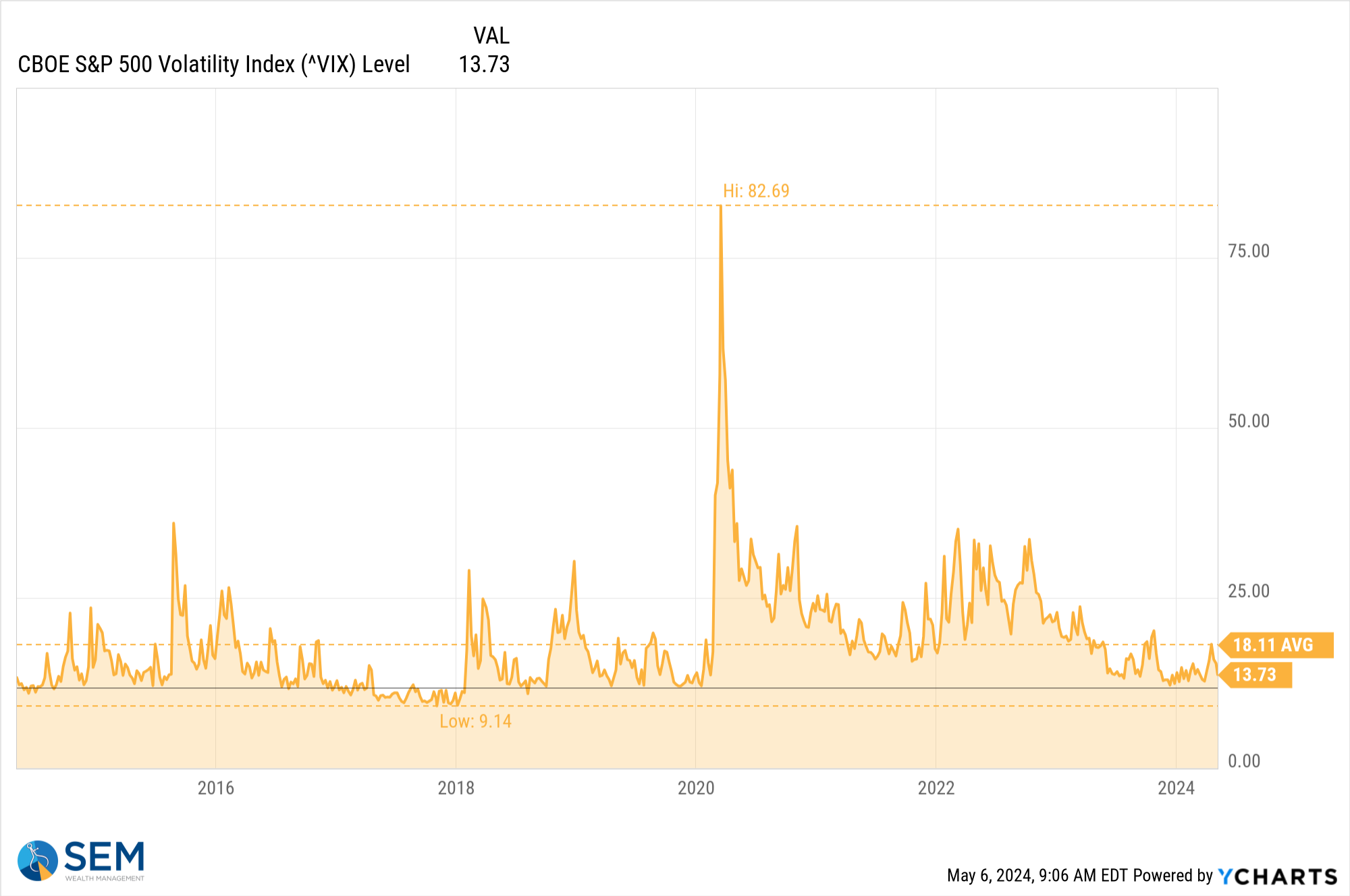

Volatility, which is a measure of sentiment remains low. This could be fuel for additional selling.

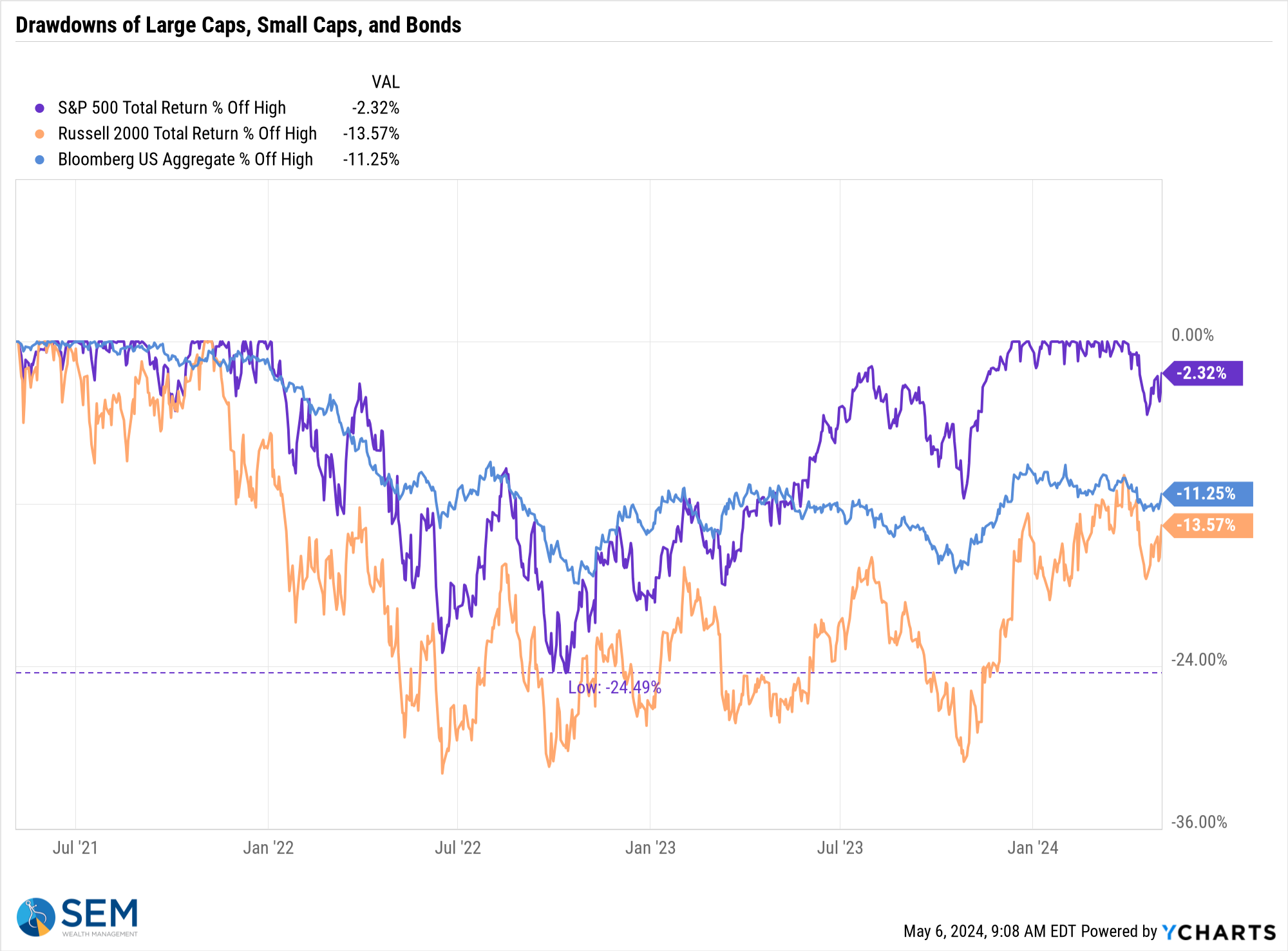

As we've been saying for nearly a year, a portfolio diversified away from the 'Magnificent 7' mega-cap stocks continues to be hurt with both bonds and small caps still over 10% off their highs.

This is not 'normal' and we should expect large cap stocks to underperform small cap stocks as our economy is fueled by innovation and new ideas. An economy dominated by just a few companies becomes stagnant and unproductive, which drives down growth and leads to losses in the stock market as valuations adjust to the slower growth.

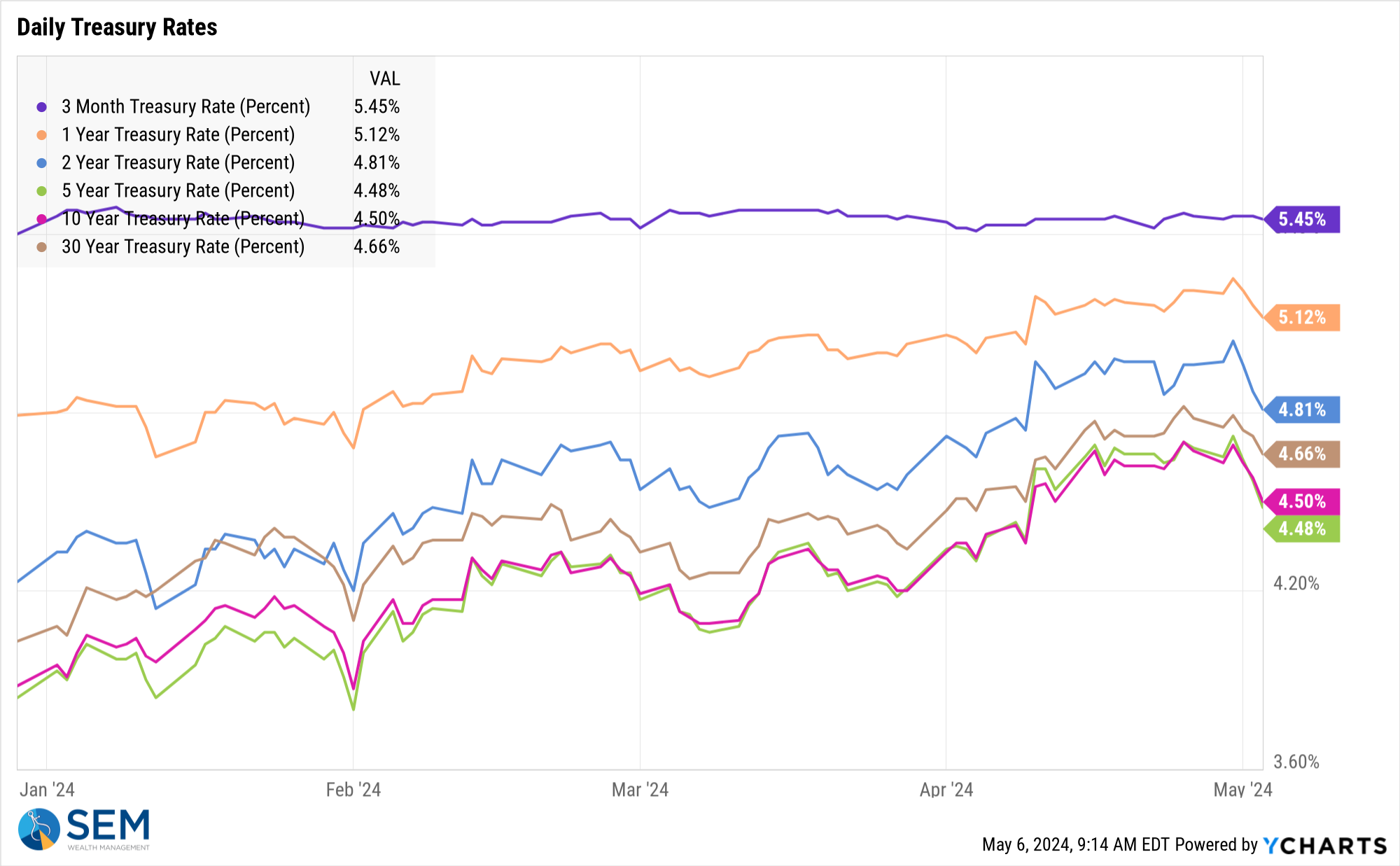

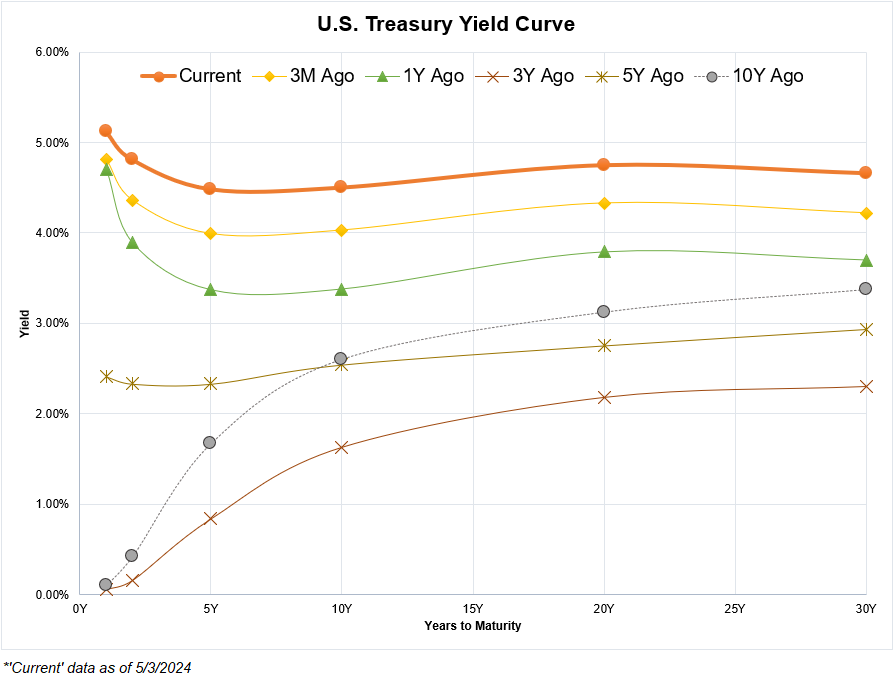

Bonds also should (at some point) revert to being a risk reducer. We are still in 'abnormal' territory as the yield curve is inverted (short-term rates higher than long-term rates.) The inversion actually got worse last week as the bond market saw the slowing economy as a positive.

The yield curve chart illustrates where the disconnect is. In a normally functioning economy we would see short-term rates much lower than long-term rates (similar to the 3 Years ago or 10 Years ago lines below.

The chart above also shows the shift higher in rates over the past 3 months and 1 year. As we 'normalize' rates either short-term rates need to go down or long-term rates need to go higher.

A few weeks ago I did a study for our advisors comparing CDs to Passive Management to Active Management since 2000. If you'd like a copy, drop us a message.

SEM Model Positioning

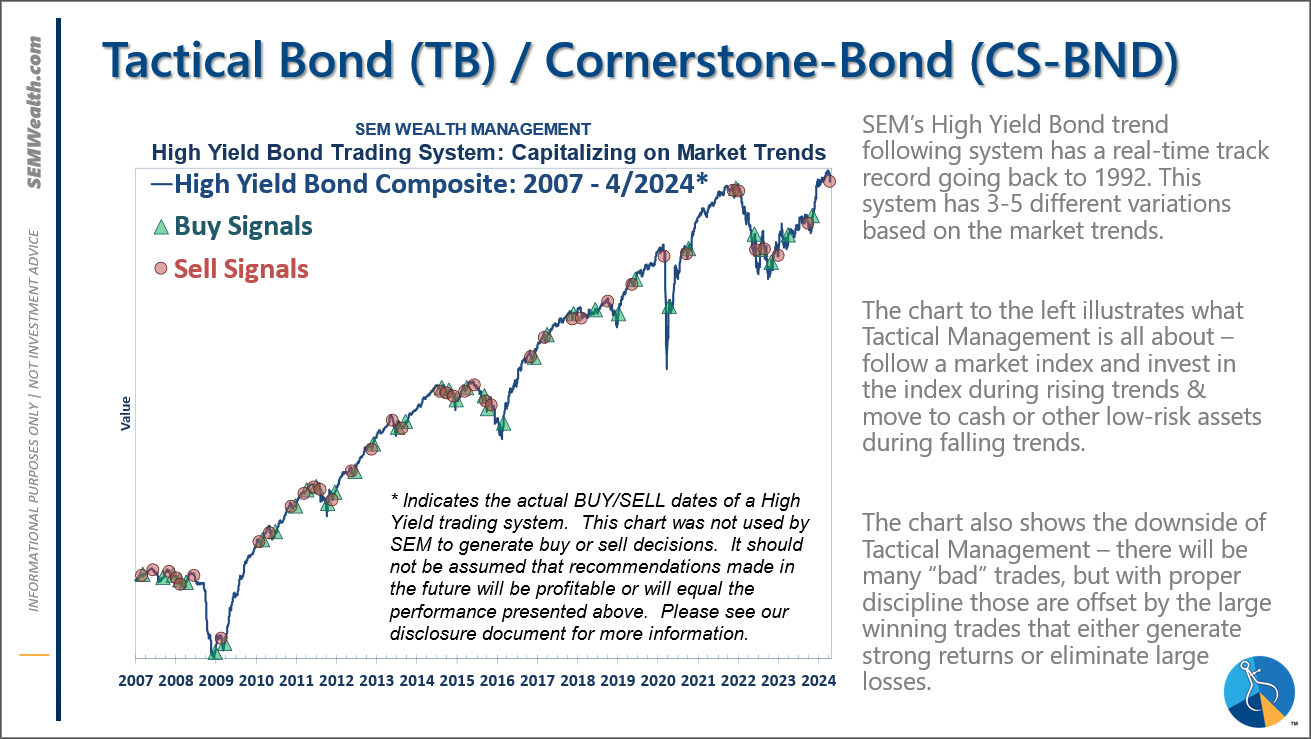

-**NEW** Tactical High Yield is very close to seeing buy signals following the sells on 4/16 & 17/2024

-**NEW** Dynamic Models went half 'bearish' 5/3/2024

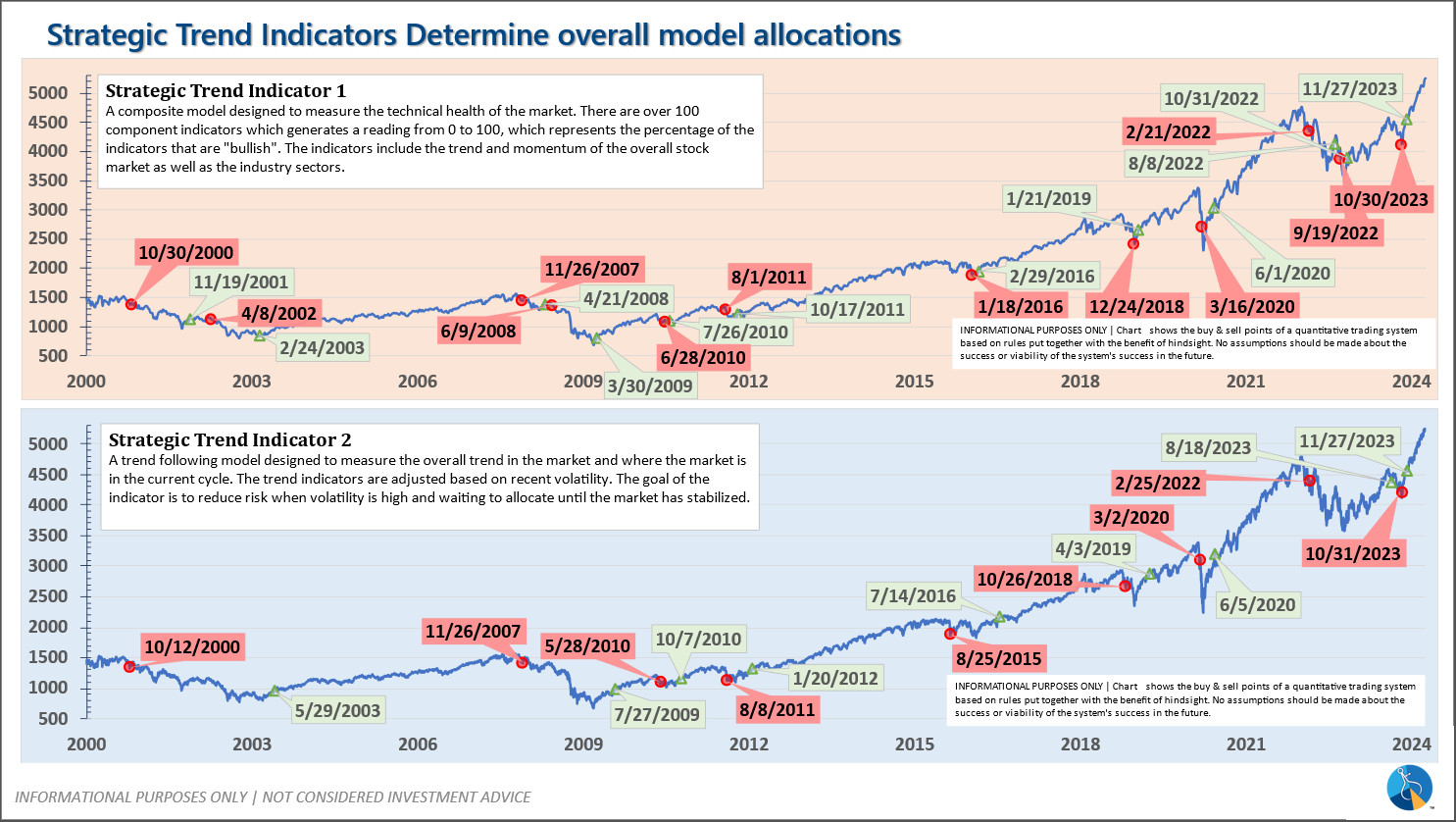

-Strategic Trend Models went on a buy 11/27/2023

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

Tactical (daily): On 4/15 & 16, 2024 the High Yield Bond systems sold the positions bought on 11/3/2023. The money market funds we are currently invested in are yielding between 4.8-5.3% annually.

Dynamic (monthly): The economic model was 'neutral' since February. In early May the model moved slightly negative. This means slightly less than benchmark positions – 10% dividend stocks in Dynamic Income and 10% small cap stocks in Dynamic Aggressive Growth.

Strategic (quarterly)*:

BOTH Trend Systems reversed back to a buy on 11/27/2023

The core rotation is adjusted quarterly. On August 17 it rotated out of mid-cap growth and into small cap value. It also sold some large cap value to buy some large cap blend and growth. The large cap purchases were in actively managed funds with more diversification than the S&P 500 (banking on the market broadening out beyond the top 5-10 stocks.) On January 8 it rotated completely out of small cap value and mid-cap growth to purchase another broad (more diversified) large cap blend fund along with a Dividend Growth fund.

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

Overall, this is how our various models stack up based on the last allocation change: