The stock market continues to impress. Nothing seems to be able to stop it. This is bringing a false sense of security that the Federal Reserve is all-knowing and will not allow the economy or the stock market to ever falter again. Ignoring the Fed's inflation fight in 2022 the post-pandemic stock market has been one that is making seemingly everyone believe nothing can stop it.

We discussed the current economic environment last week:

Normally when I review the week I find some sort of theme to discuss in the blog. This week I struggled to find anything "new" that I haven't been discussing the past month or two. The only theme I came up with was this:

Valuations don't matter. Interest rates don't matter. Debt doesn't matter. Fundamentals don't matter.

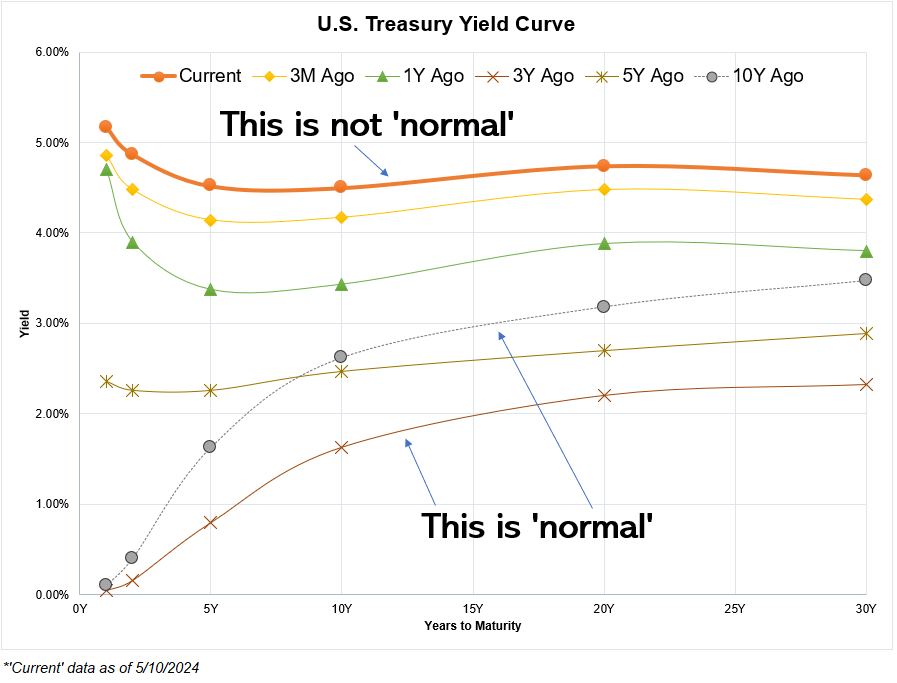

The one thing I kept thinking was "This is not normal". The best representation of this is the yield curve. The Fed's focus on controlling the economy has left us in an abnormal environment.

We cannot fight what is happening right now, but we have over 120 years of data telling us when the abnormal environment reverts back to normal things will break. All we can do is be prepared.

A few weeks ago I did a study for our advisors comparing CDs to Passive Management to Active Management since 2000. If you'd like a copy, drop us a message.

Market Charts

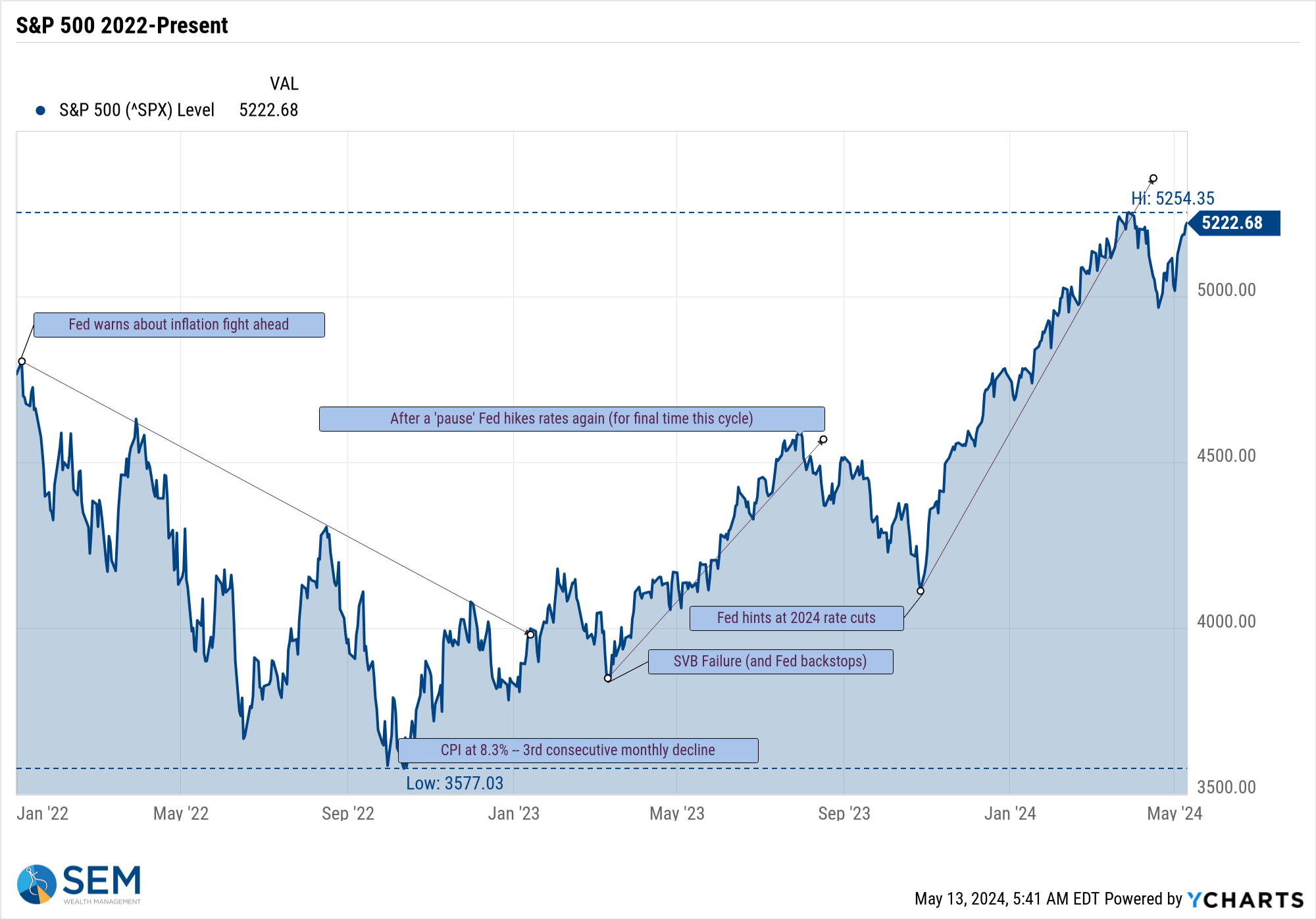

The S&P 500 is nearly back to its all-time high.

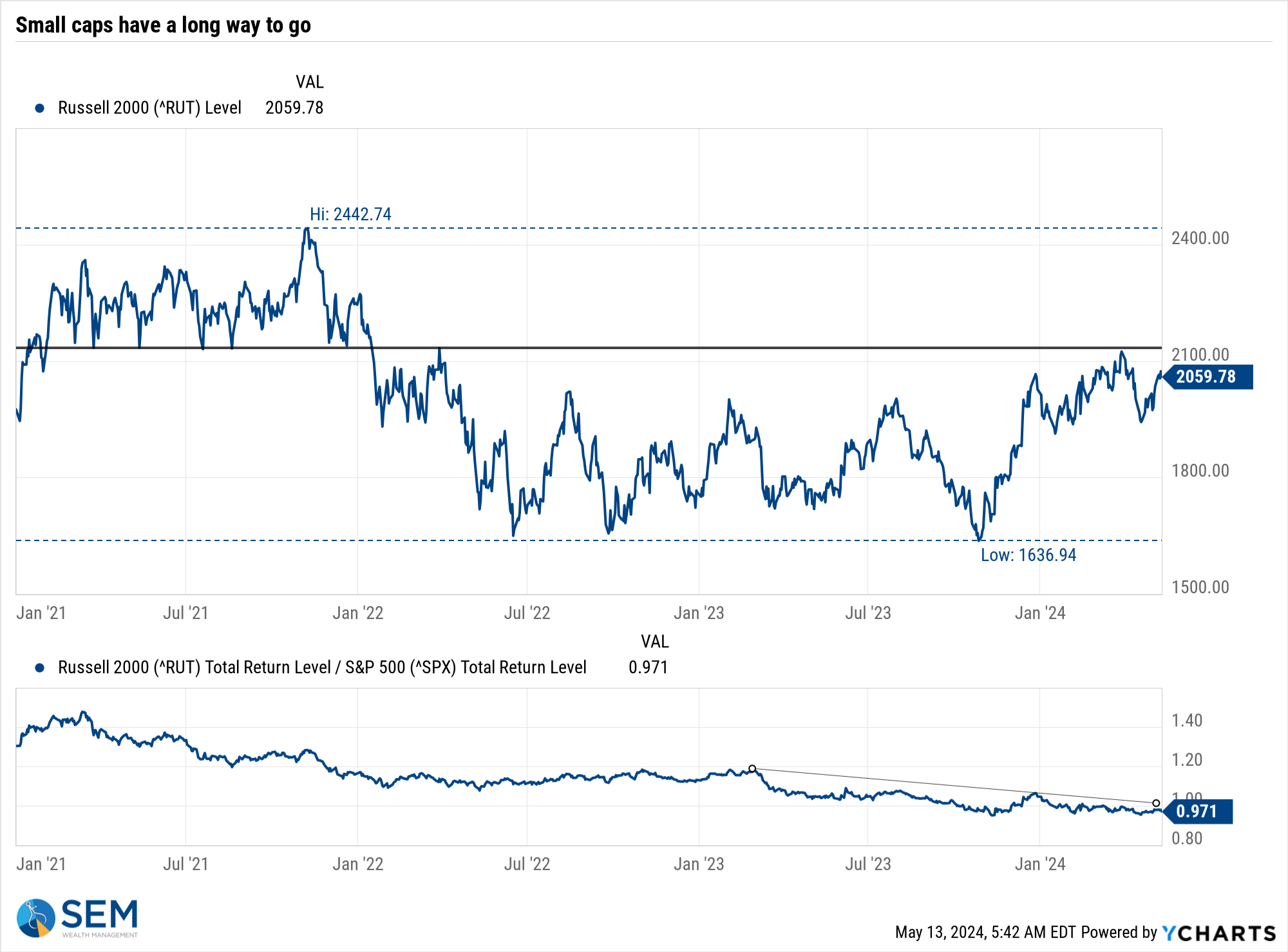

Small cap stocks still have a long way to go. The panel at the bottom of the chart below measures the Small Cap index versus the Large Cap index. In a healthy market you would expect that line to be increasing or at best to be level.

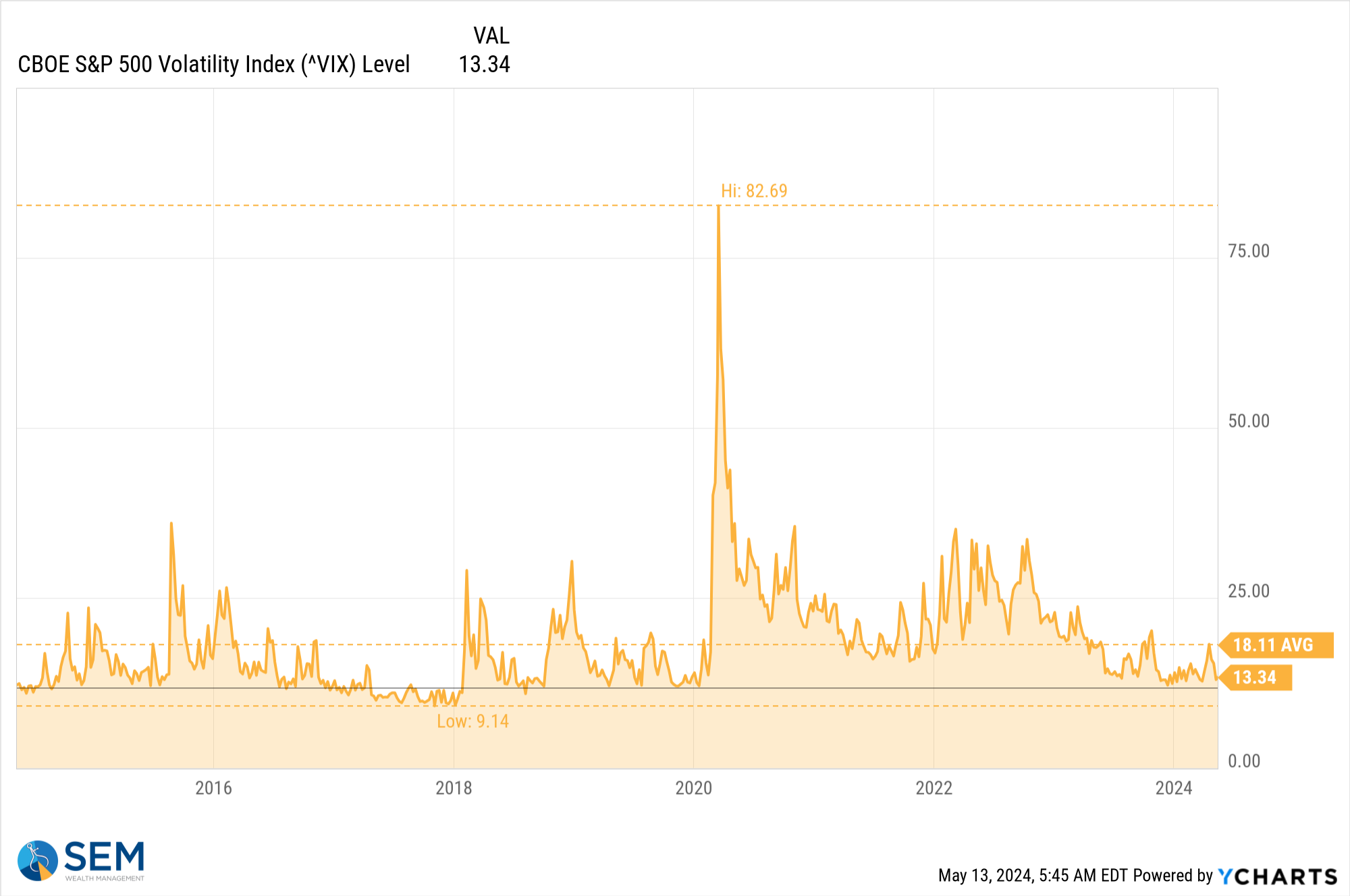

Volatility remains near the lows of the post-pandemic era.

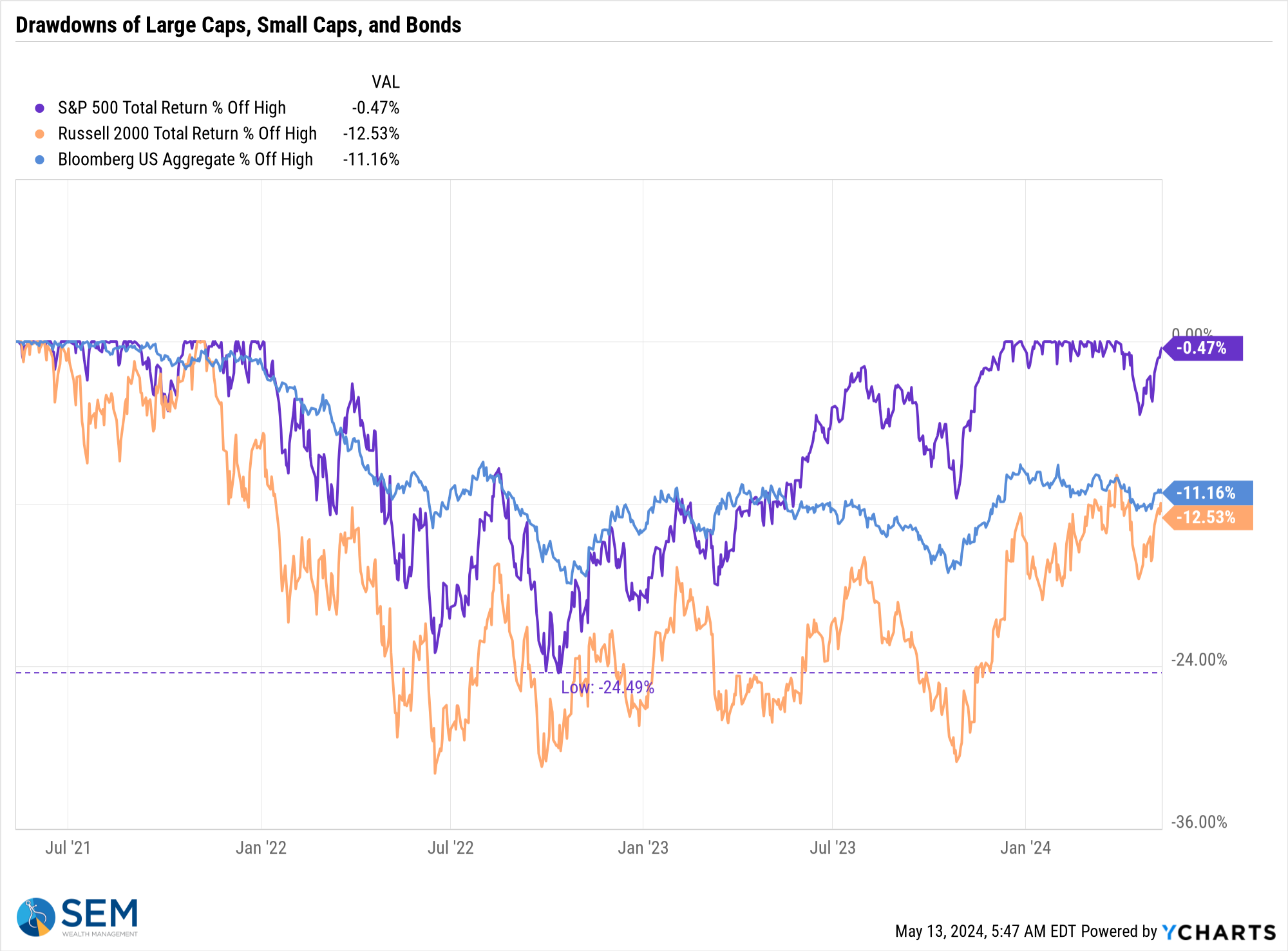

Looking at the drawdowns (% down from the high), you can see the difference between large (mega) caps, small caps and bonds. Diversification has hurt during the post-pandemic "boom".

Like stocks, bonds had a nice, steady week. The trend in yields is still higher, which should be a problem for stocks.

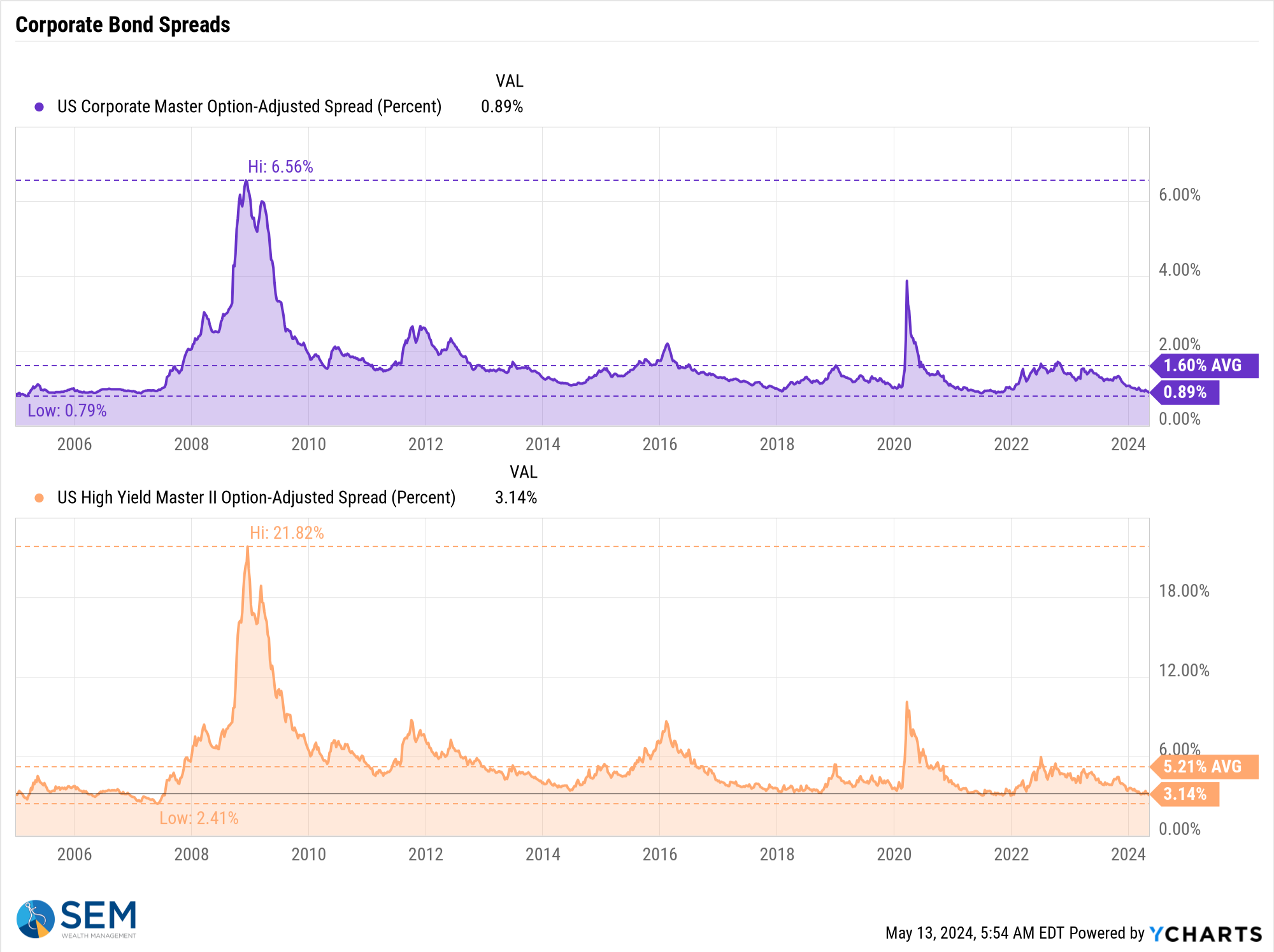

However, like stocks the corporate bond market currently sees little risk of stress in the financial system. The spreads between both investment grade corporate bonds and high yields to treasury bonds are at post-pandemic lows and very close to ALL-TIME lows. There is still inflation risk, which could turn into credit risk, but for now the bond market is predicting smooth sailing.

SEM Model Positioning

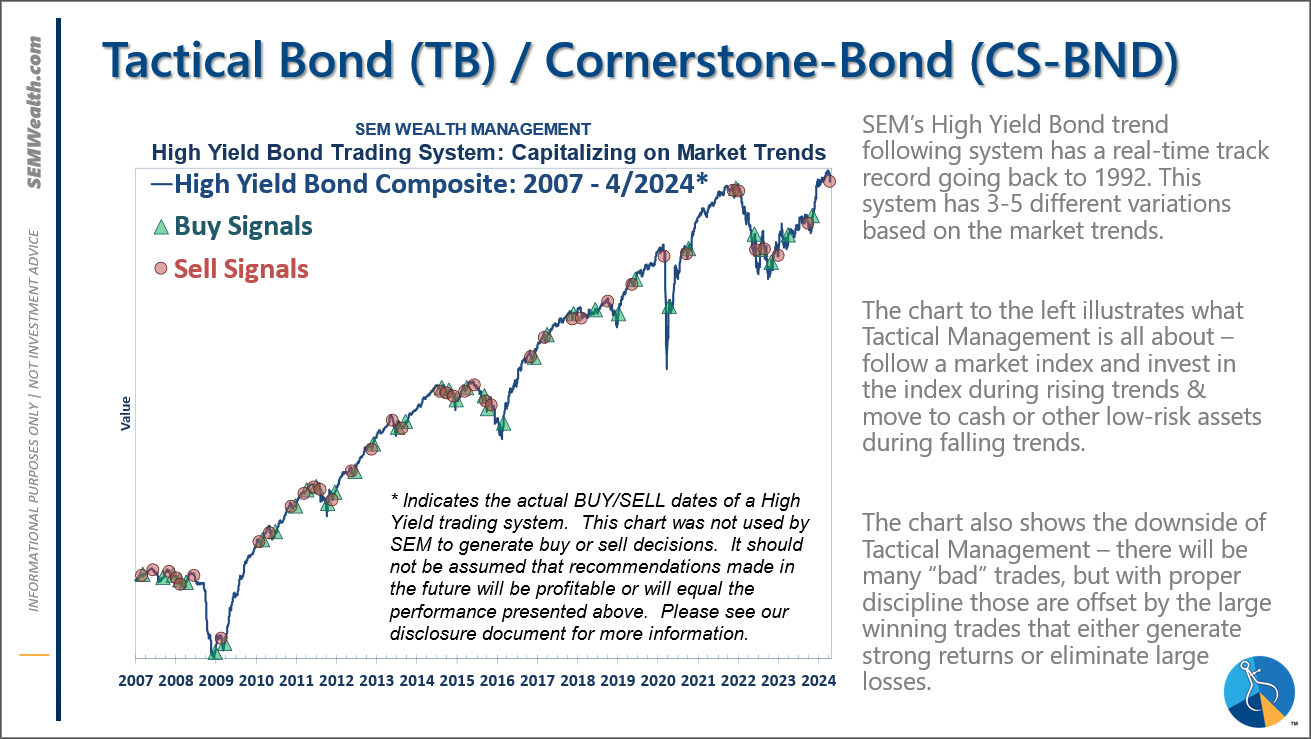

-**NEW** Tactical High Yield had a partial buy signal on 5/6/24, reversing some of the sells on 4/16 & 17/2024

-Dynamic Models went half 'bearish' 5/3/2024

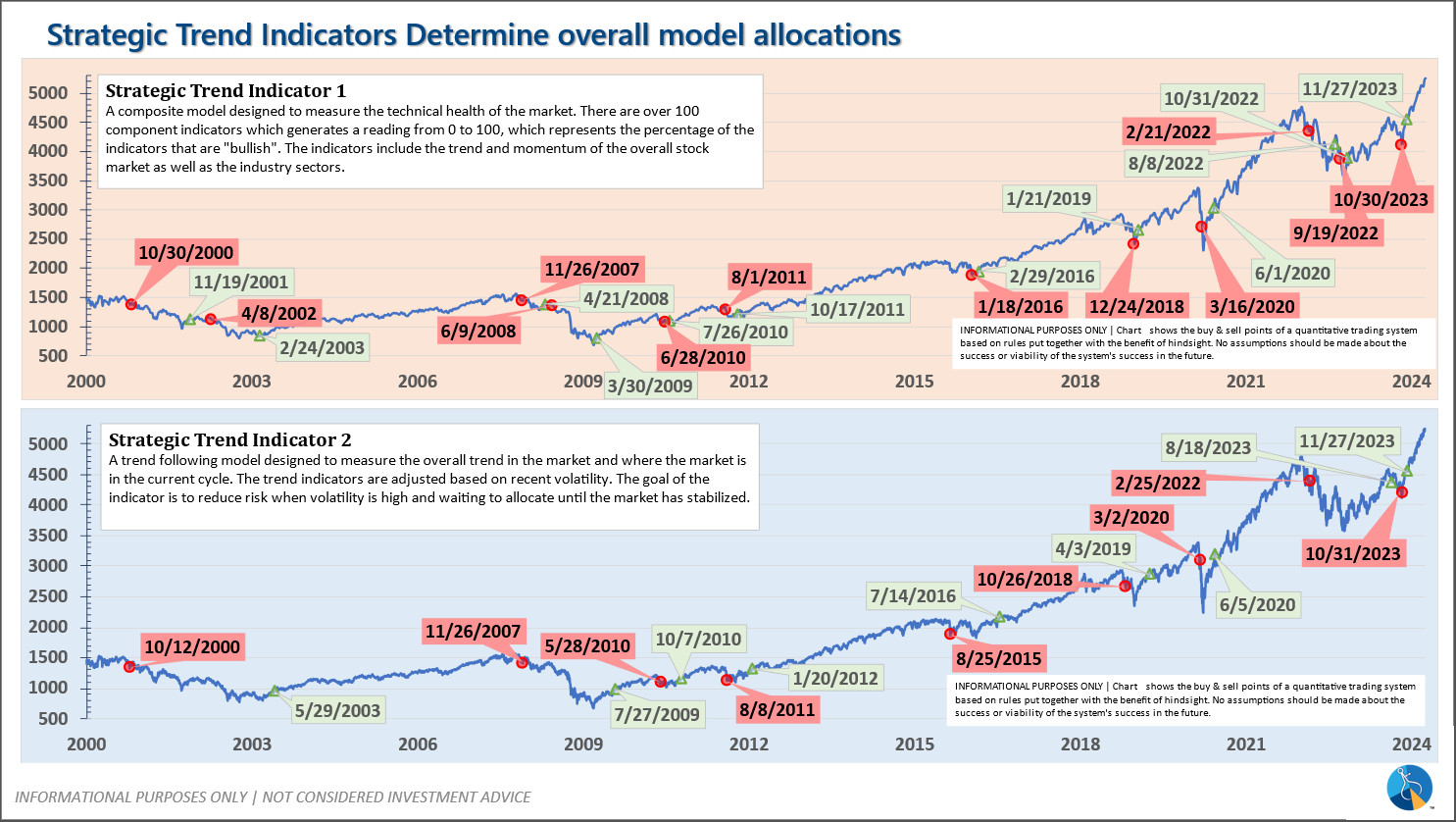

-Strategic Trend Models went on a buy 11/27/2023

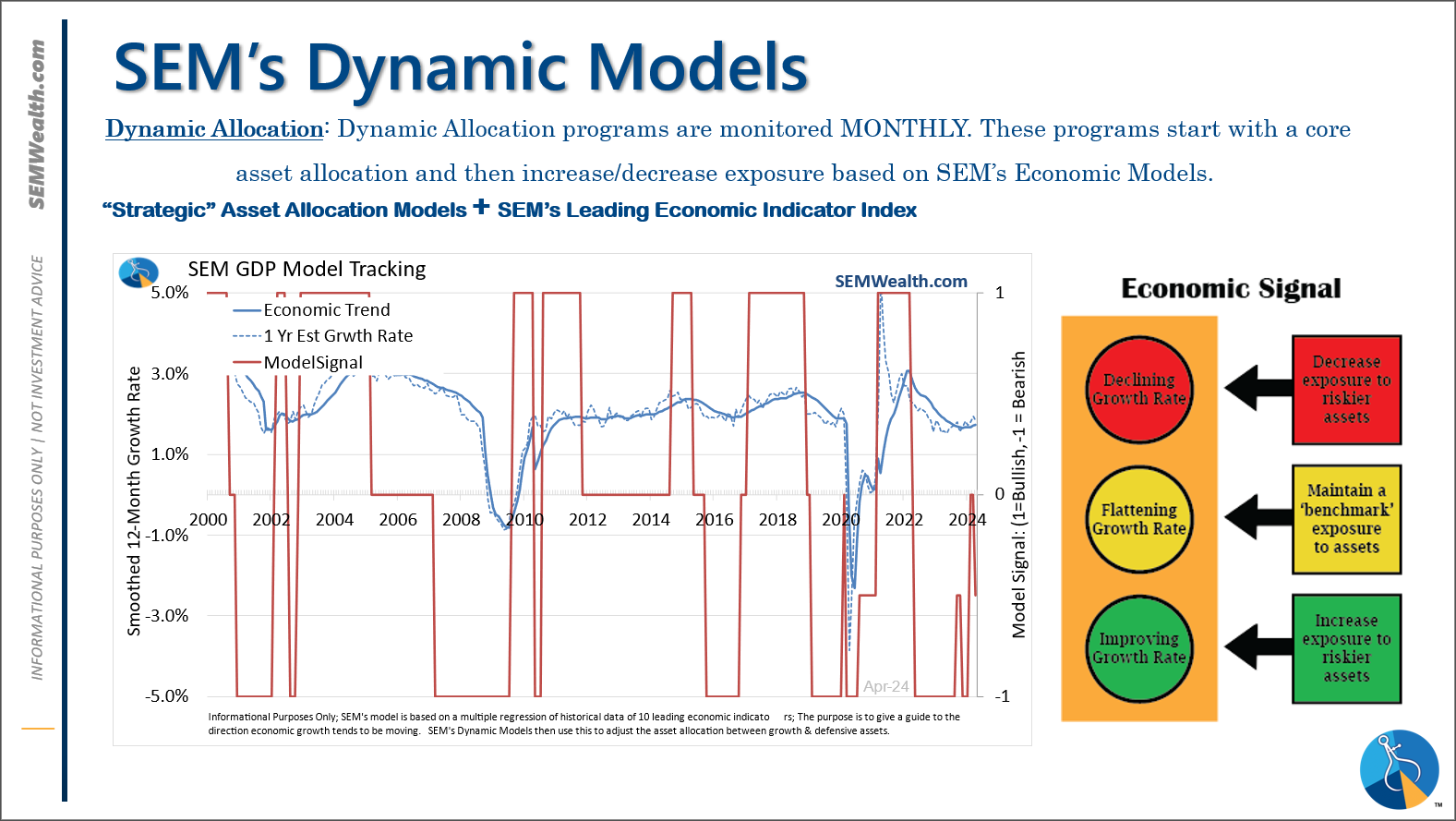

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

Tactical (daily): On 5/6/24 about half of the signals in our high yield models switched to a buy. The other half remains in money market funds. The money market funds we are currently invested in are yielding between 4.8-5.3% annually.

Dynamic (monthly): The economic model was 'neutral' since February. In early May the model moved slightly negative. This means slightly less than benchmark positions – 10% dividend stocks in Dynamic Income and 10% small cap stocks in Dynamic Aggressive Growth.

Strategic (quarterly)*:

BOTH Trend Systems reversed back to a buy on 11/27/2023

The core rotation is adjusted quarterly. On August 17 it rotated out of mid-cap growth and into small cap value. It also sold some large cap value to buy some large cap blend and growth. The large cap purchases were in actively managed funds with more diversification than the S&P 500 (banking on the market broadening out beyond the top 5-10 stocks.) On January 8 it rotated completely out of small cap value and mid-cap growth to purchase another broad (more diversified) large cap blend fund along with a Dividend Growth fund.

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

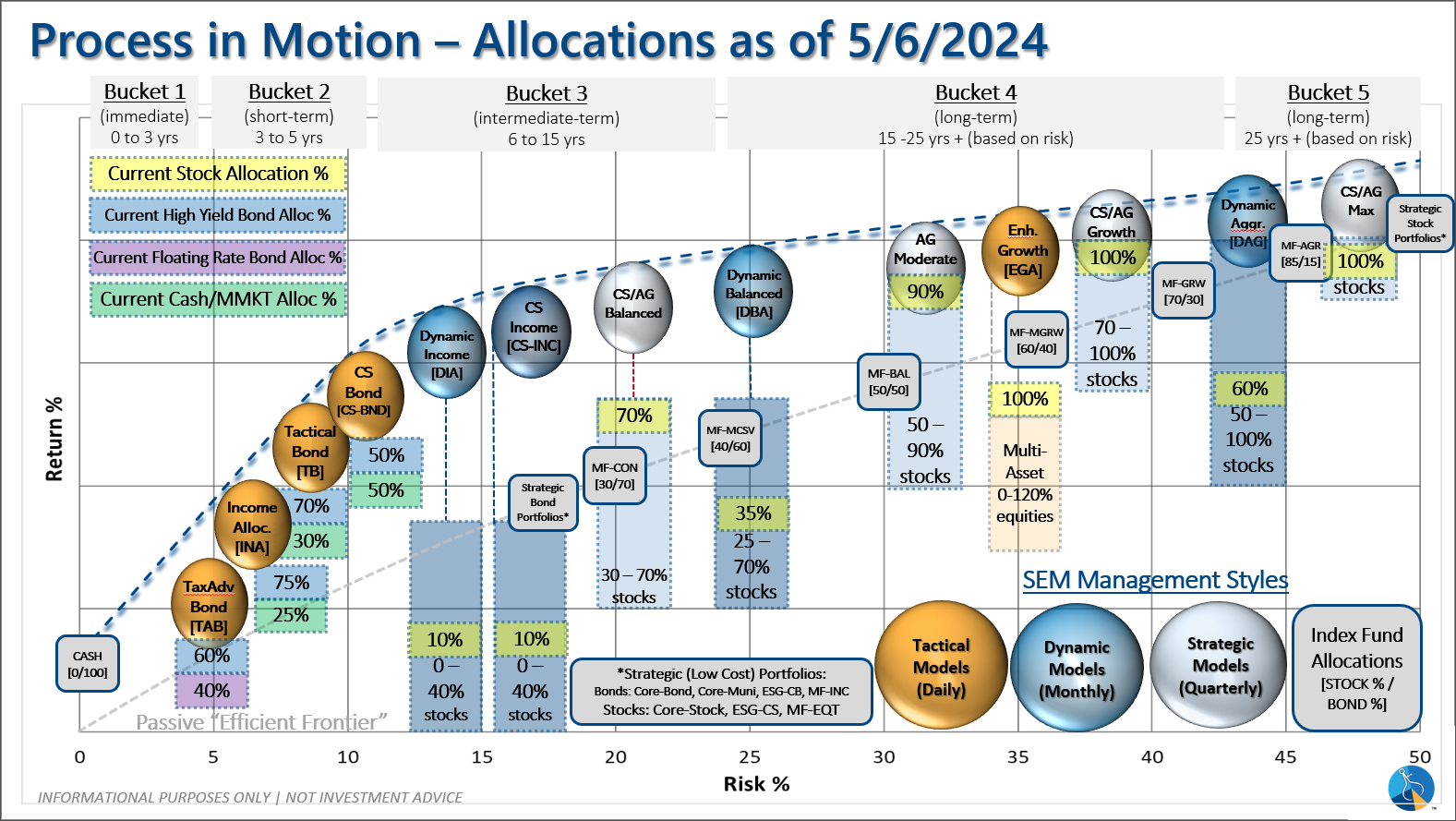

Overall, this is how our various models stack up based on the last allocation change: