The market's attention remains fixed on AI, energy prices, and the Federal Reserve. Yet beneath all the headlines is a much more simple factor that has historically driven economic growth: people going to work. The June employment report released last week suggests the labor market is neither booming nor collapsing. Job growth remains modest, hours worked are still expanding, and recession fears appear overdone. However, a less discussed trend is emerging beneath the surface. The U.S. labor force is no longer growing the way it has for most of the past two decades, and that could have important implications for economic growth, corporate earnings, and long-term investment returns.

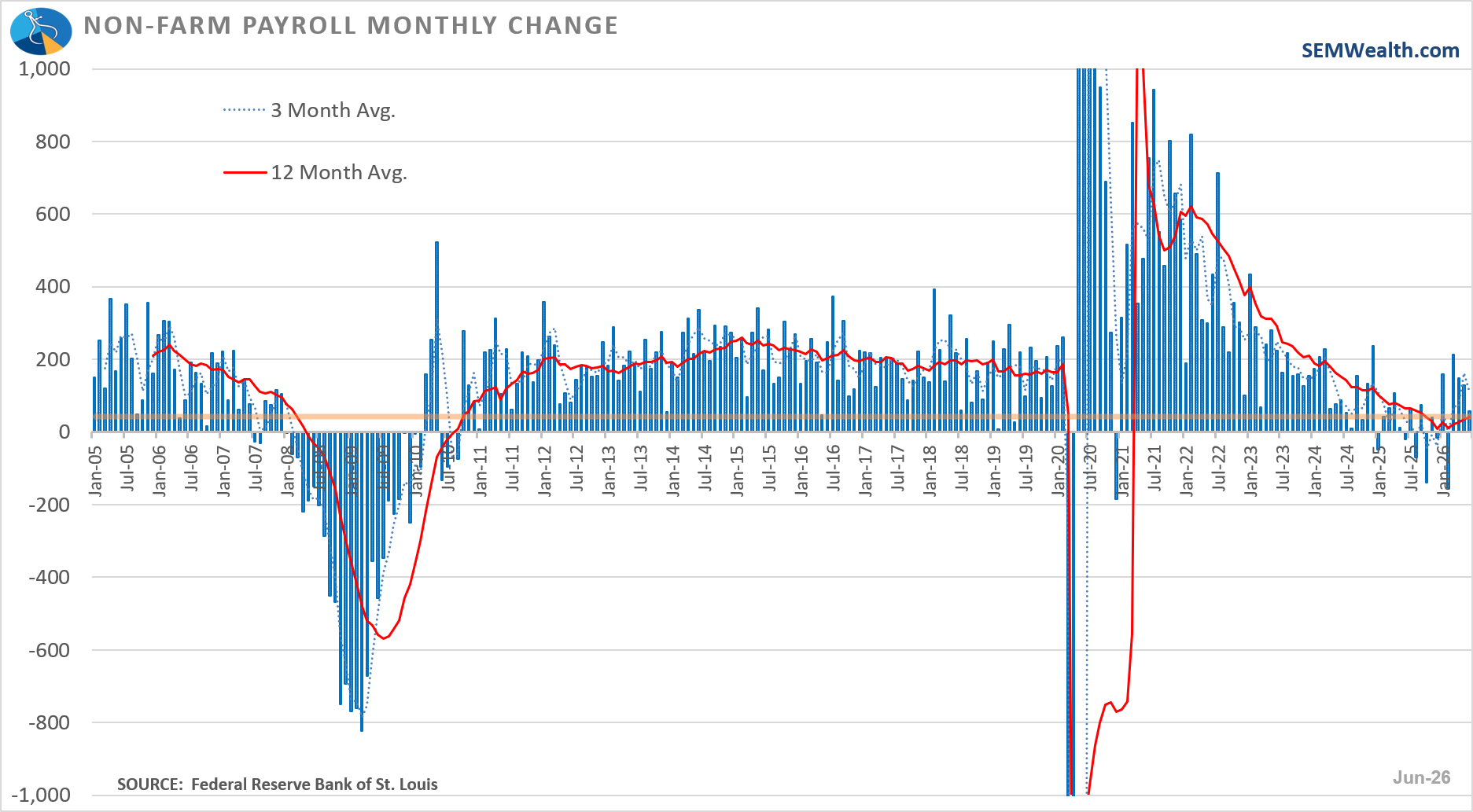

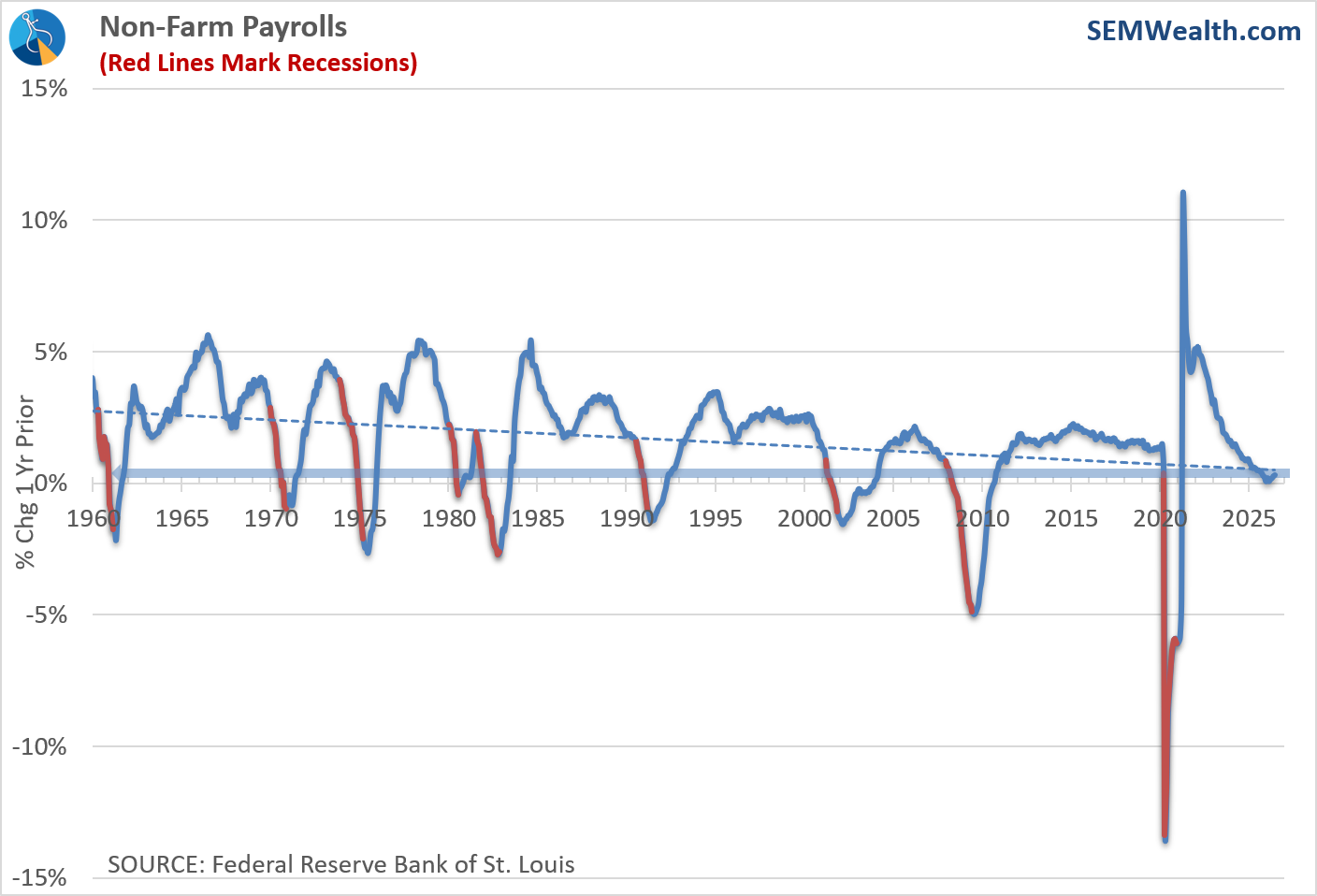

Let's first look at the June employment report. The overall labor market continues to be lackluster. The 12-month average has turned higher a bit, but we are still only seeing job growth of around 0.35% over the past year. The labor market is telling us things are "ok" – not great, but also not heading towards a recession.

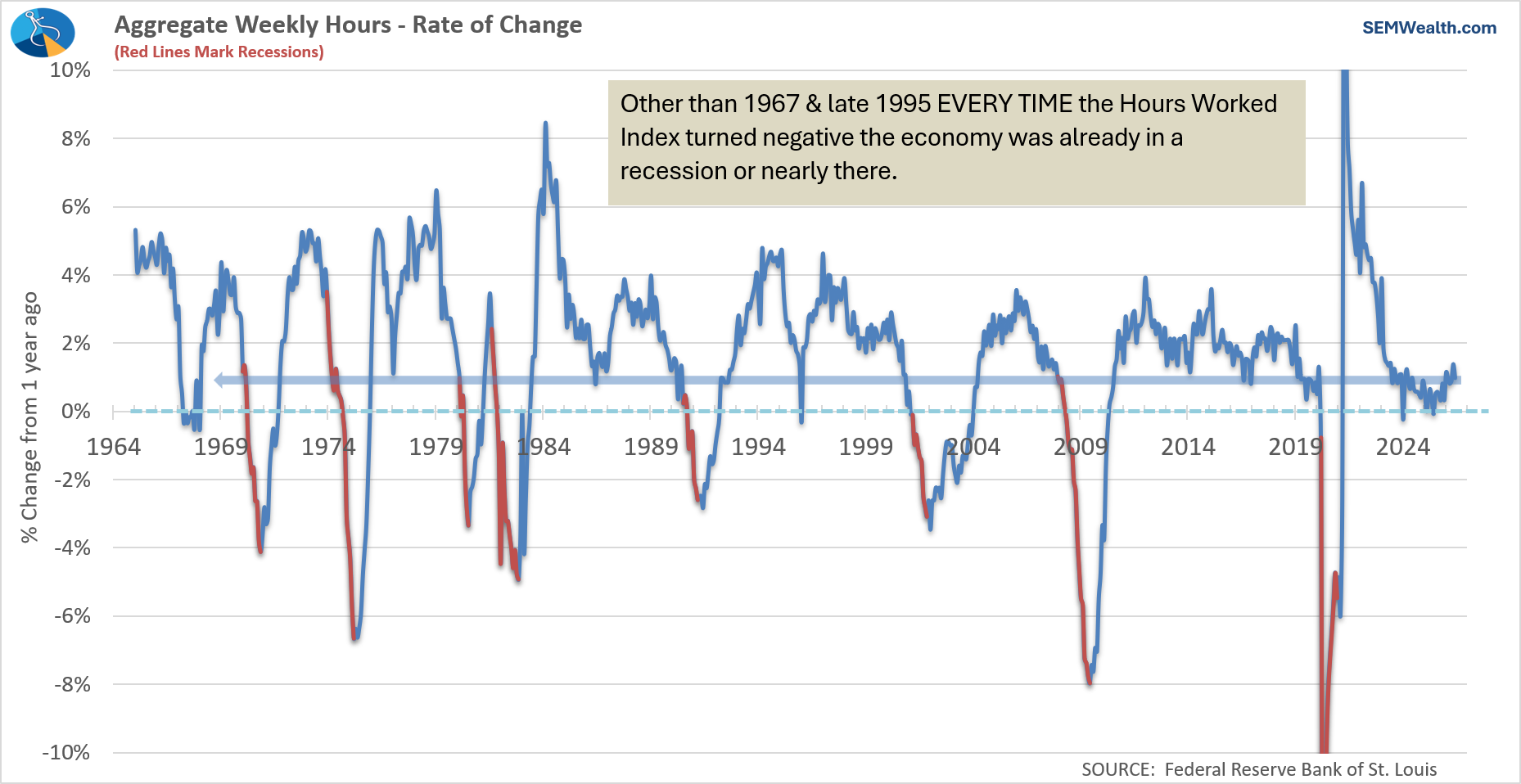

The Hours Worked Index has increased by about 1% over the last 12 months. Again, not blockbuster growth, but also not pointing to a slowdown.

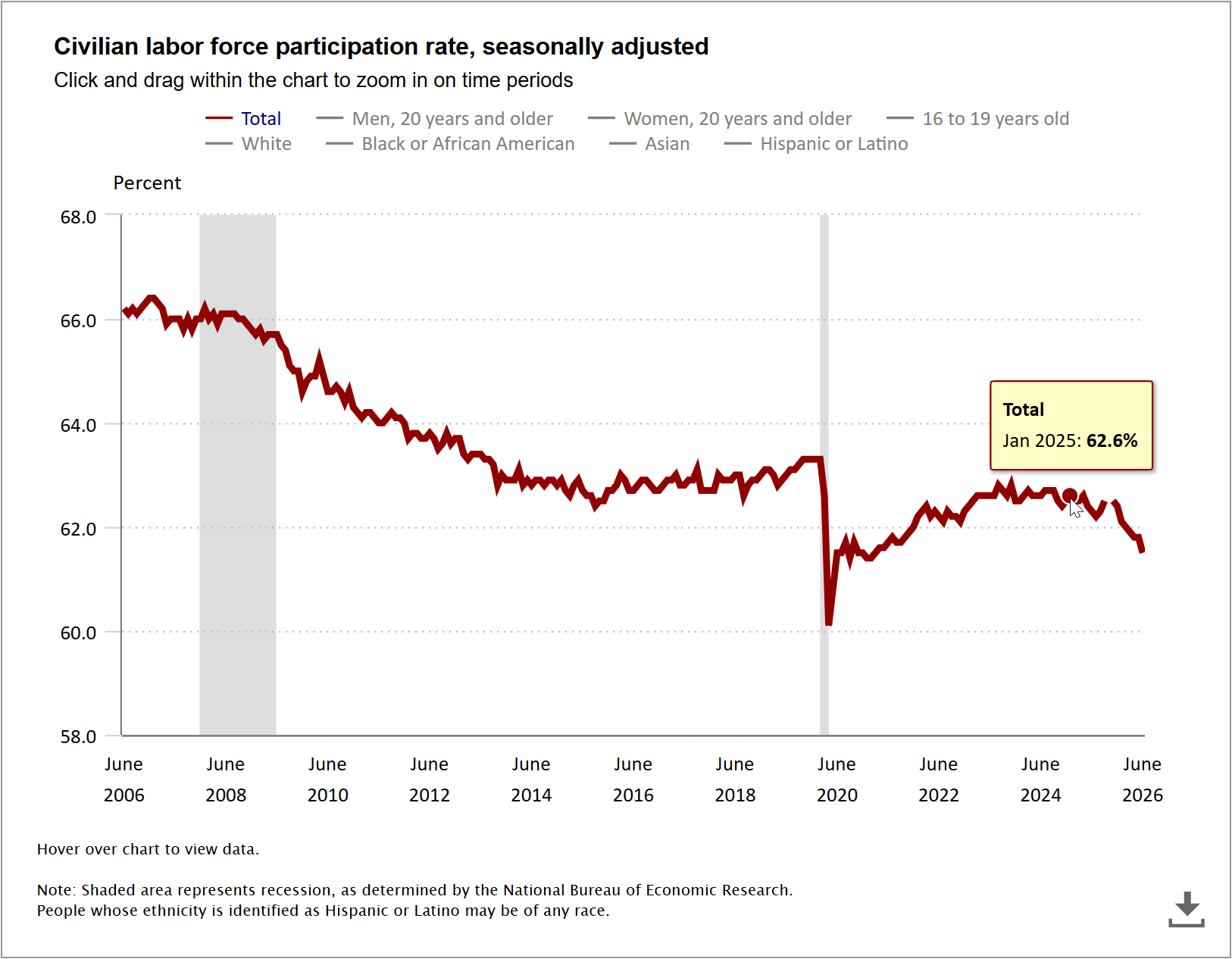

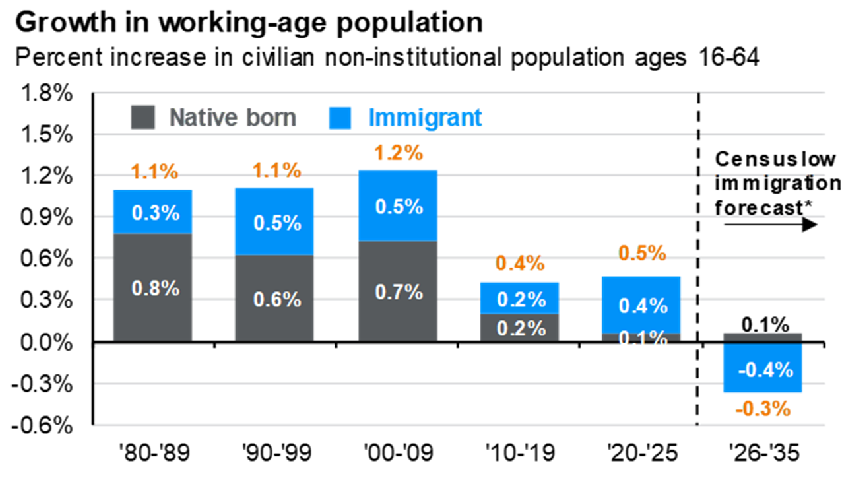

The unemployment rate declined slightly as the labor force participation rate again shrunk. Earlier this century we endured a decline in the labor force due to the retirement of the Boomer generation. That had stabilized by 2015 since the Millennial generation is bigger than the Boomers and they were entering the workforce in size. We then saw a steep drop during COVID, but saw it climb back to the same levels it had bottomed at in 2015. However, since early 2025 the participation rate has been plummeting.

What's going on? The answer is a significant drop off in LEGAL immigrants working in the country. Remember, the official payroll numbers, which includes the "working age population" only counts those in the country legally. Since 2025 we've seen a significant drop-off in work-visa renewals and new work-visas being issued. This is not a political statement, but an economic one. We should enforce our immigration laws and keep people out of the US from entering illegally. However, our diverse economy needs LEGAL immigrants to work here. We simply do not have enough people born here who are willing to fill the jobs that our economy needs to continue growing at a pace we've all been accustomed to.

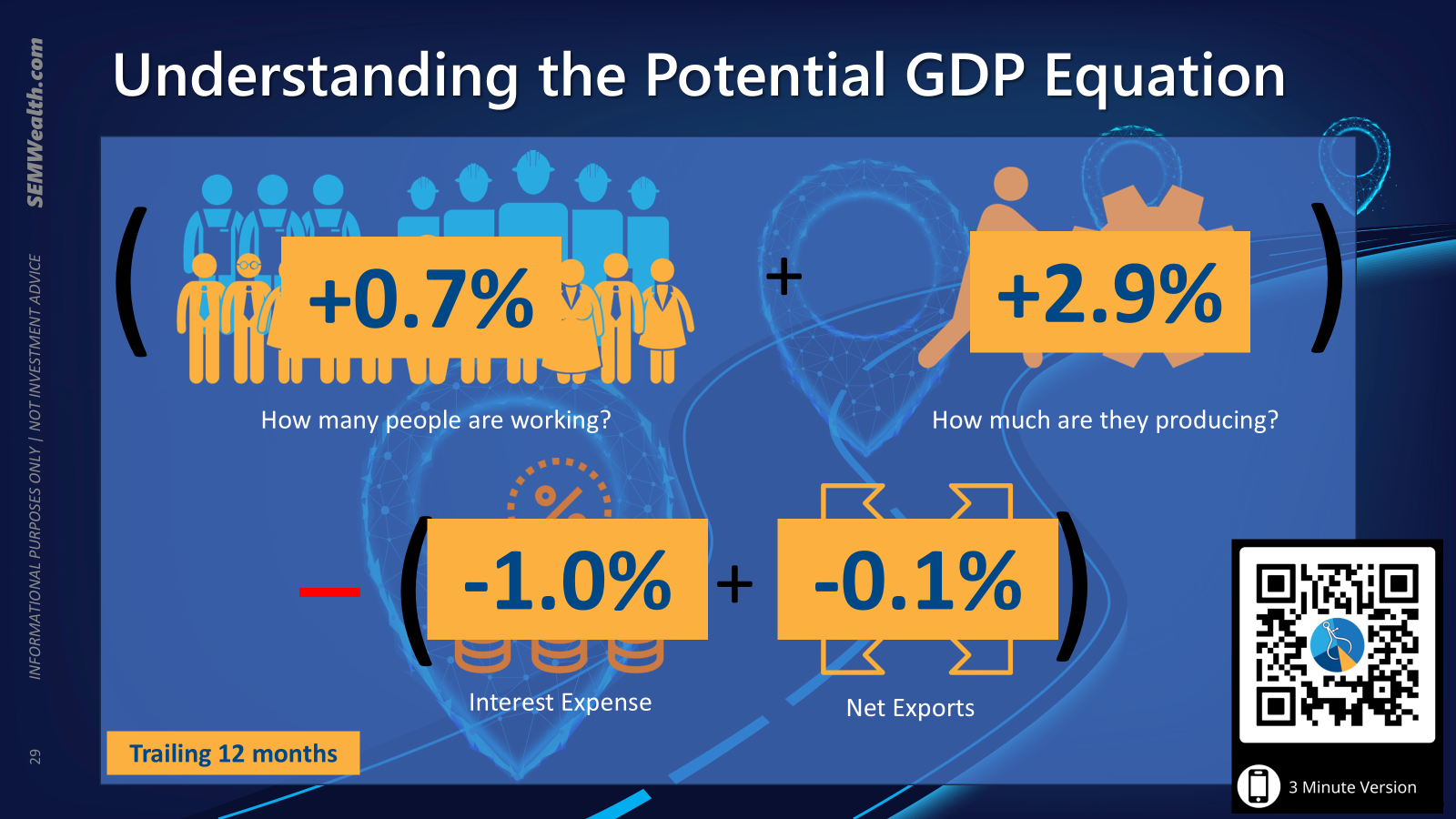

Why does this matter? Our economy grows based on a simple function – how many people are working plus how much are they producing (Labor Force Growth + Productivity Growth). We then have to subtract out interest paid on our debt (which is growing substantially) and our trade deficit (which is still increasing, despite the trade war).

Put more simply – in order to pay for our deficit spending the past 40 years, we need more workers producing more, just to maintain a certain standard of living. If we don't, our economy will not grow at a rate enough to sustain it. We cannot rely on "AI" to magically increase productivity to cover what is expected to be a SHRINKING labor force. In fact, the lack of LEGAL immigrant workers is holding back the potential growth of AI as we simply do not have enough workers to build out all of the infrastructure necessary to meet the expected demand for AI. This means productivity growth may not hit the levels most are expecting.

This has major ramifications, especially with the massive amounts of capital expenditures expected over the next 2-3 years, which is driving earnings and stock prices to records.

Again, this is NOT POLITICAL. It is basic economics. It is something all Americans should be aware of as we choose the next Congress in November.

Economic Update

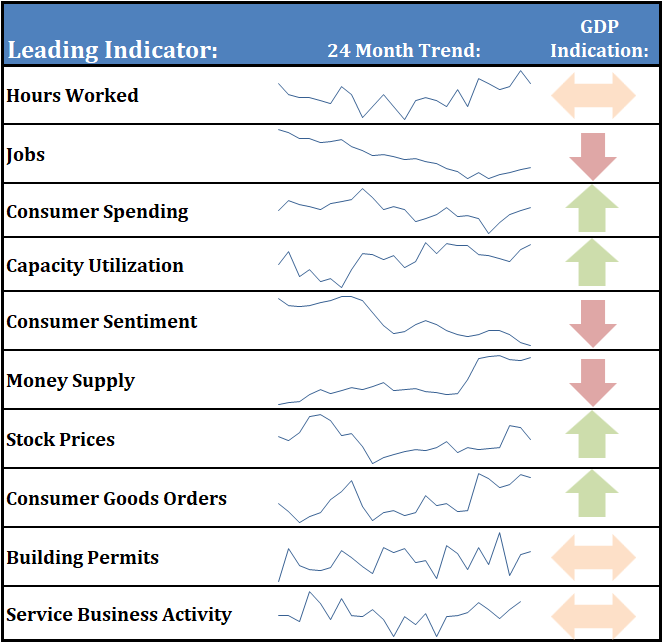

Overall, our dashboard of leading economic indicators slightly improved last month, despite disappointing jobs numbers and a decline in the hours worked index. If we have a decently steady month for economic data, we should see our model adjust from 'neutral' to bullish.

At SEM, we spend a great deal of time looking beyond the headlines and focusing on the underlying drivers of economic growth. While markets often react to the latest policy announcement or earnings report, long-term trends such as labor force growth, productivity, debt costs, and trade flows ultimately matter far more. The challenge for investors is that these structural shifts unfold slowly and are easy to overlook until they begin affecting corporate profits and market expectations.

For now, the economy continues to grow and the labor market remains stable. However, if labor force growth continues to weaken, investors may need to temper expectations for future growth and be more selective about where they invest. As always, our goal is to monitor these trends objectively, adapt when conditions change, and position portfolios based on evidence rather than headlines. The labor force may not be the most exciting topic on Wall Street, but it remains one of the most important variables shaping the market's future.

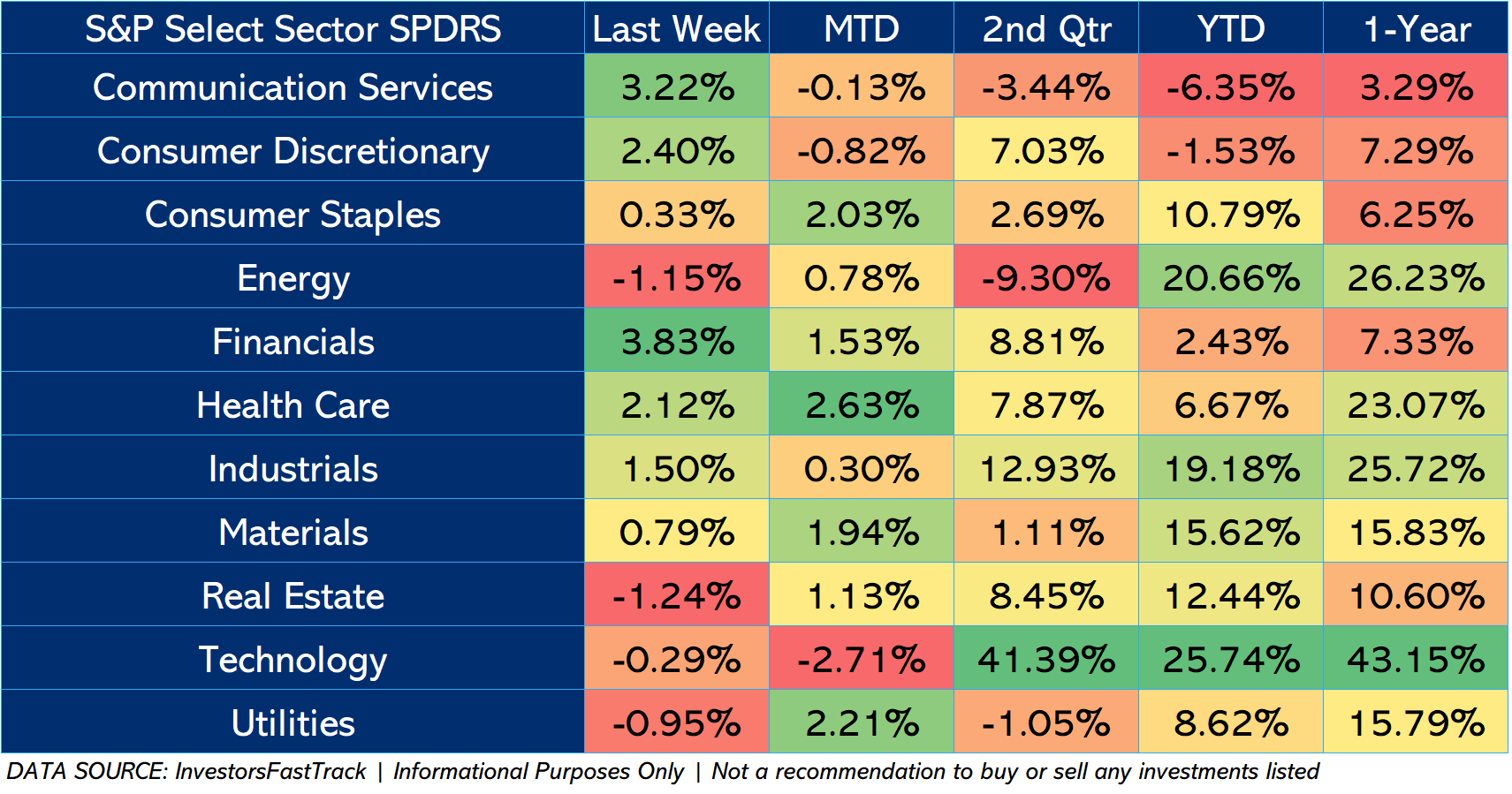

Market Update

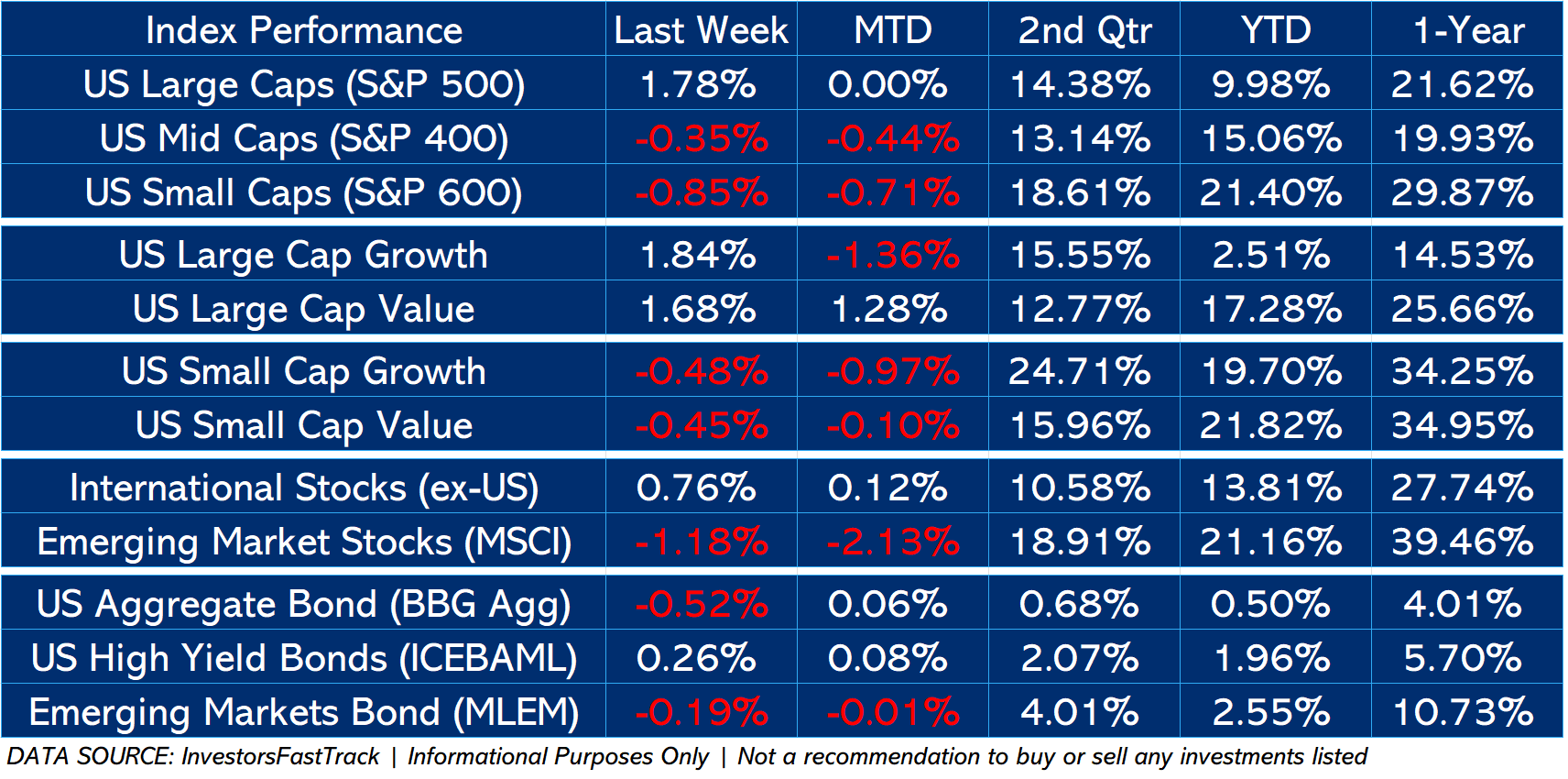

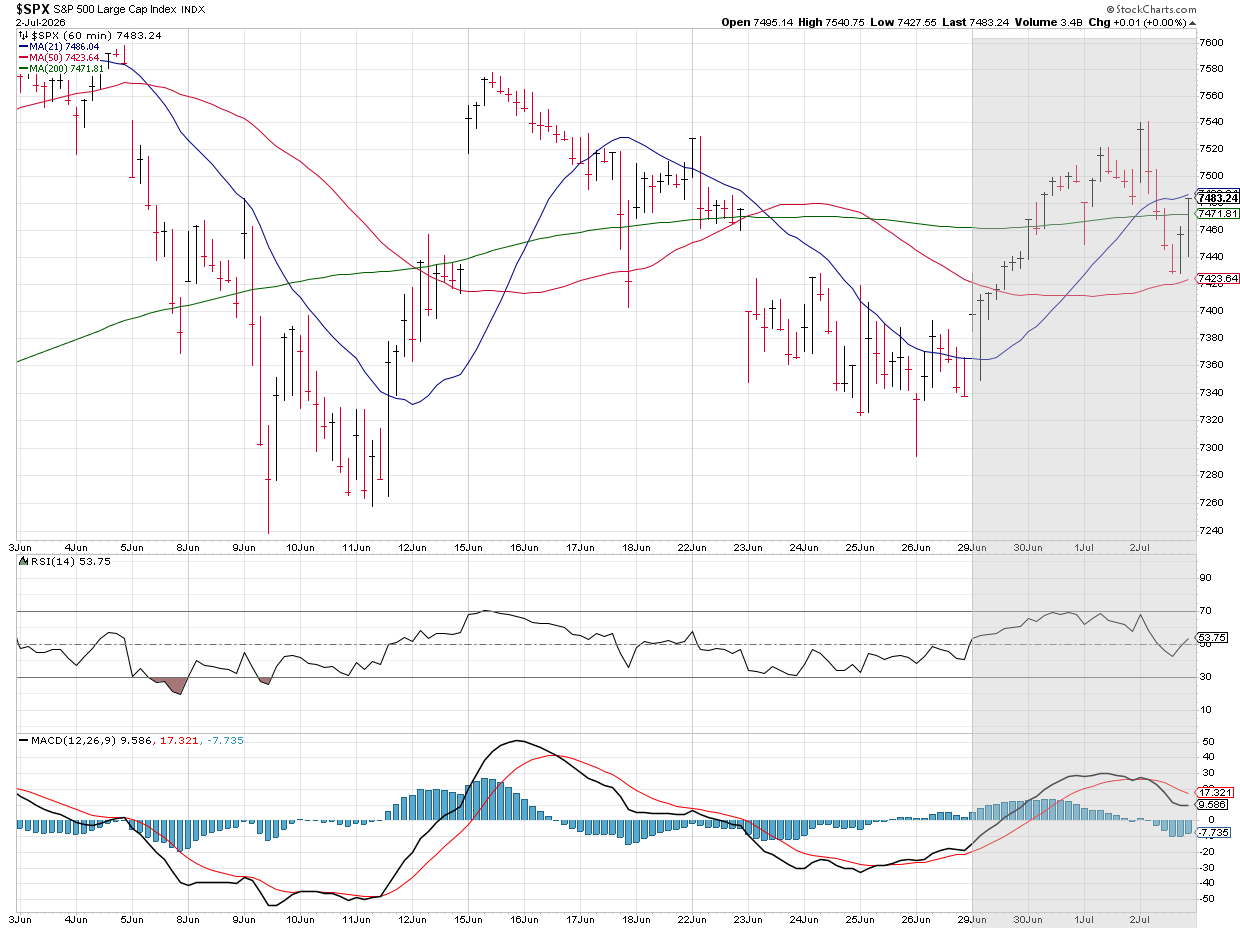

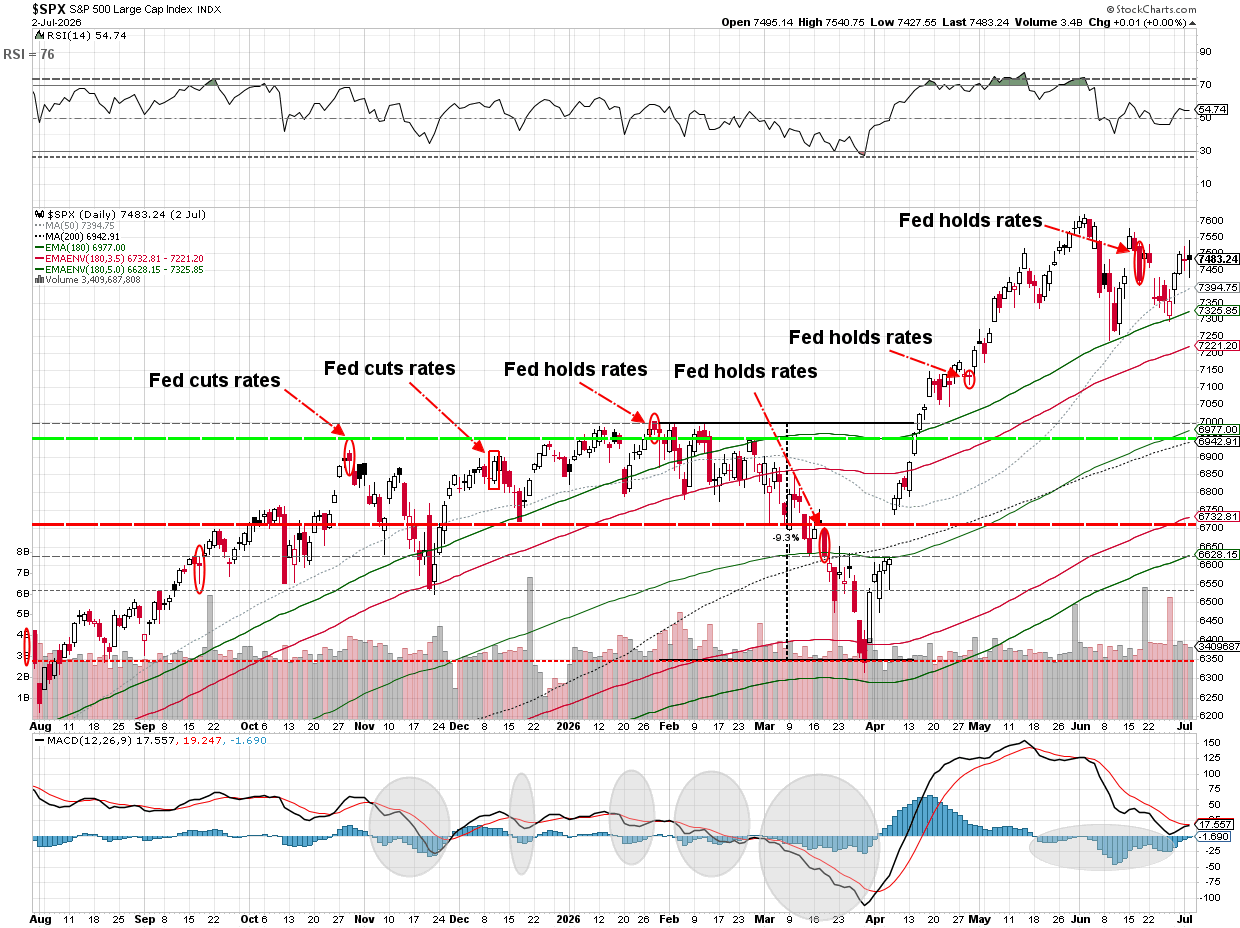

It was a generally positive week for the S&P 500.

The S&P did manage to climb back to where it was ahead of the Fed meeting, so perhaps stocks have digested the "new" environment where the Fed is more focused on inflation than boosting employment.

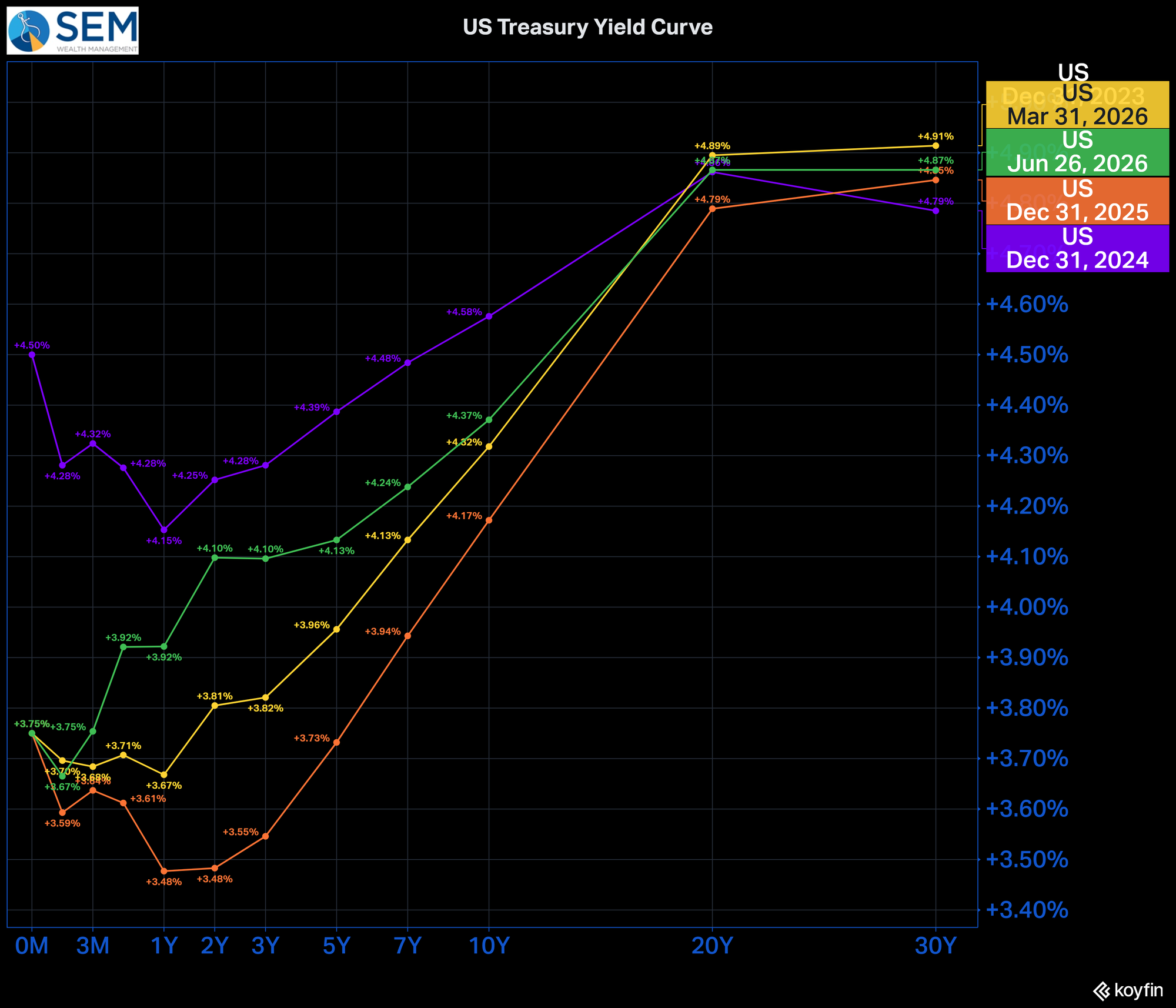

Yields actually came down a bit on Thursday with the lackluster jobs report (less inflation pressure?), but remain significantly higher than they were at the start of the year.

SEM Market Positioning

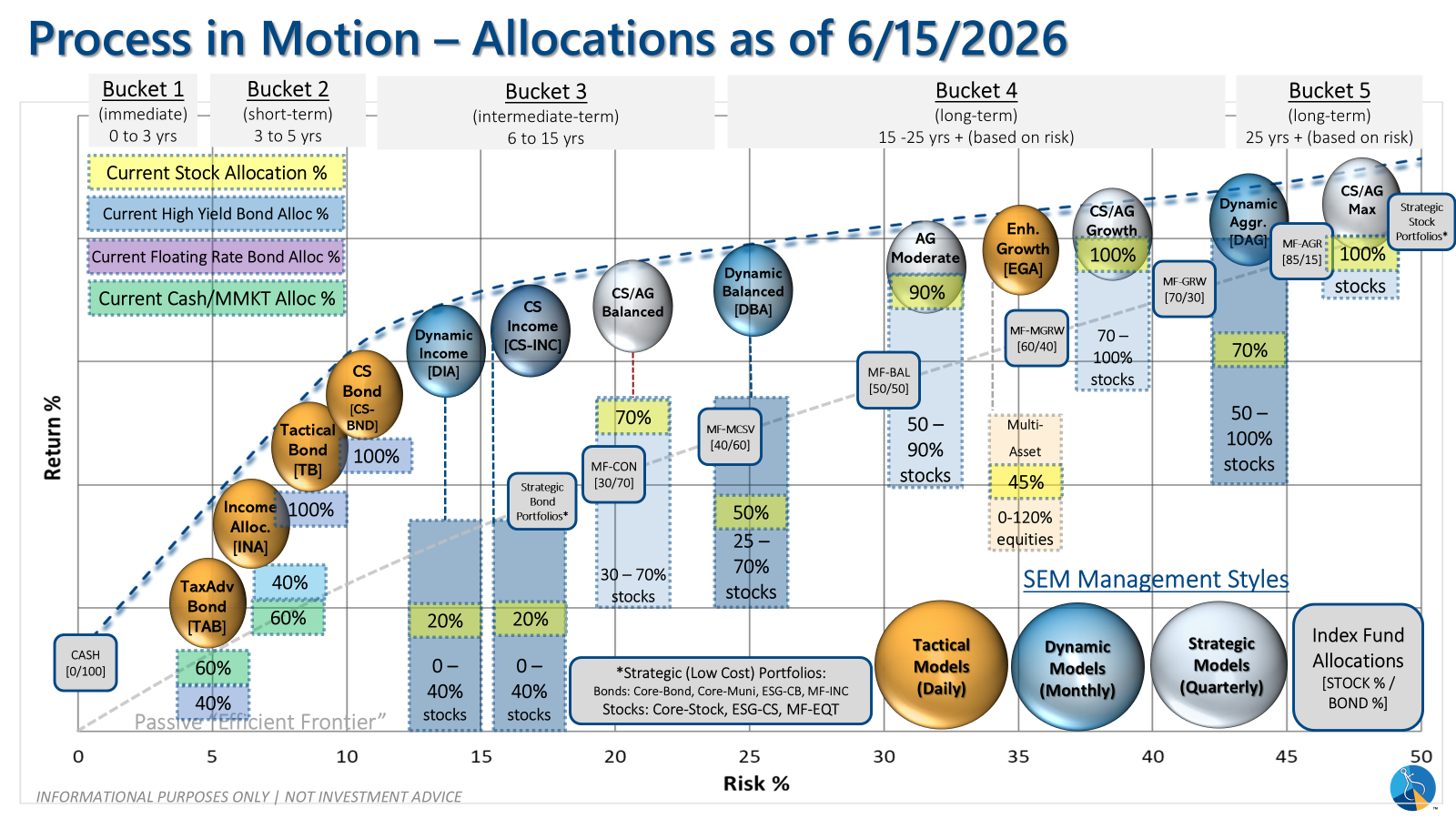

SEM deploys 3 distinct approaches – Tactical, Dynamic, and Strategic. These systems have been described as 'daily, monthly, quarterly' given how often they may make adjustments. Here is where they each stand.

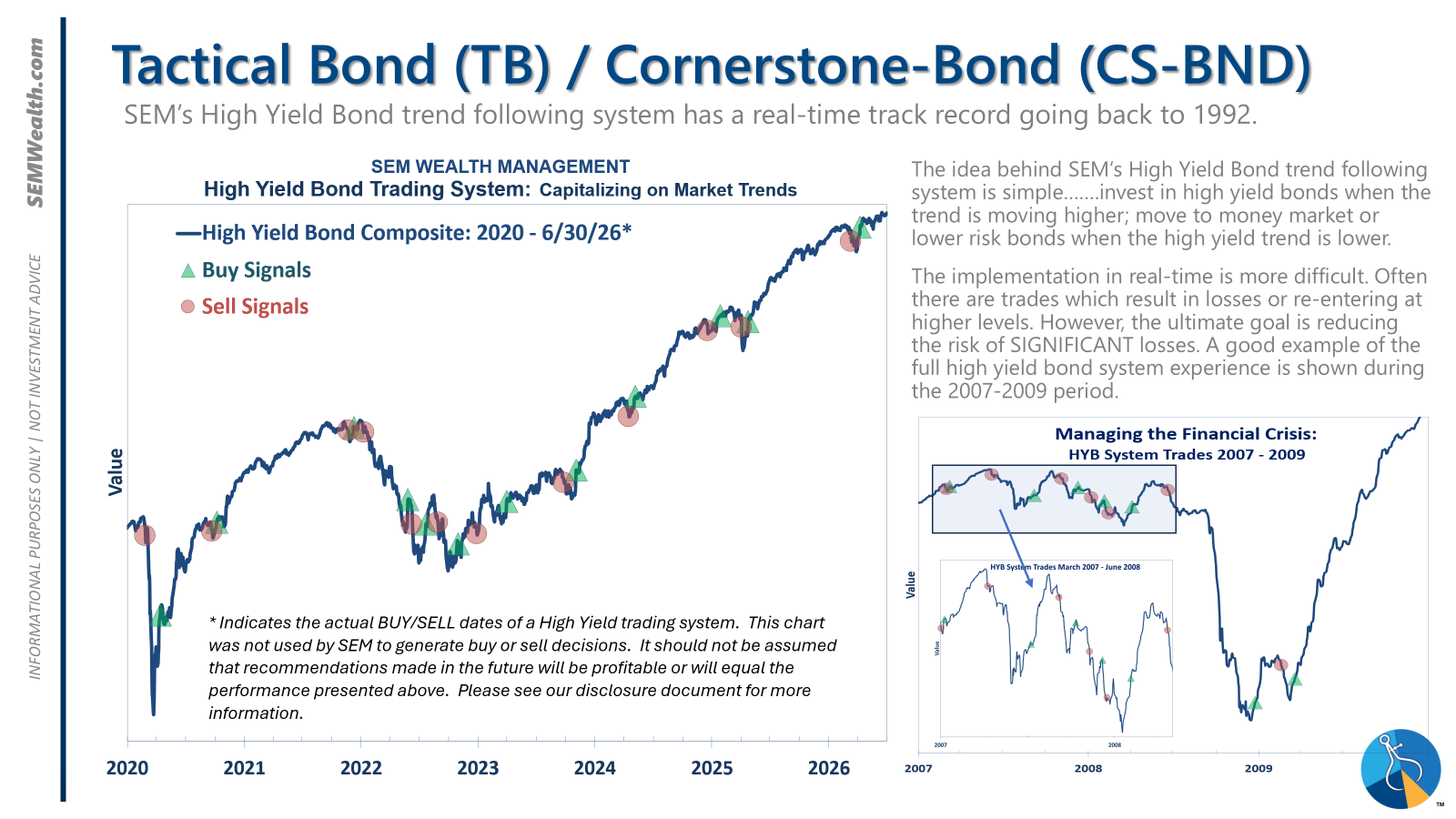

- Tactical = BULLISH | 100% High Yield Bond (4/8/2026) | High-yield spreads remain narrow but trend is slightly higher

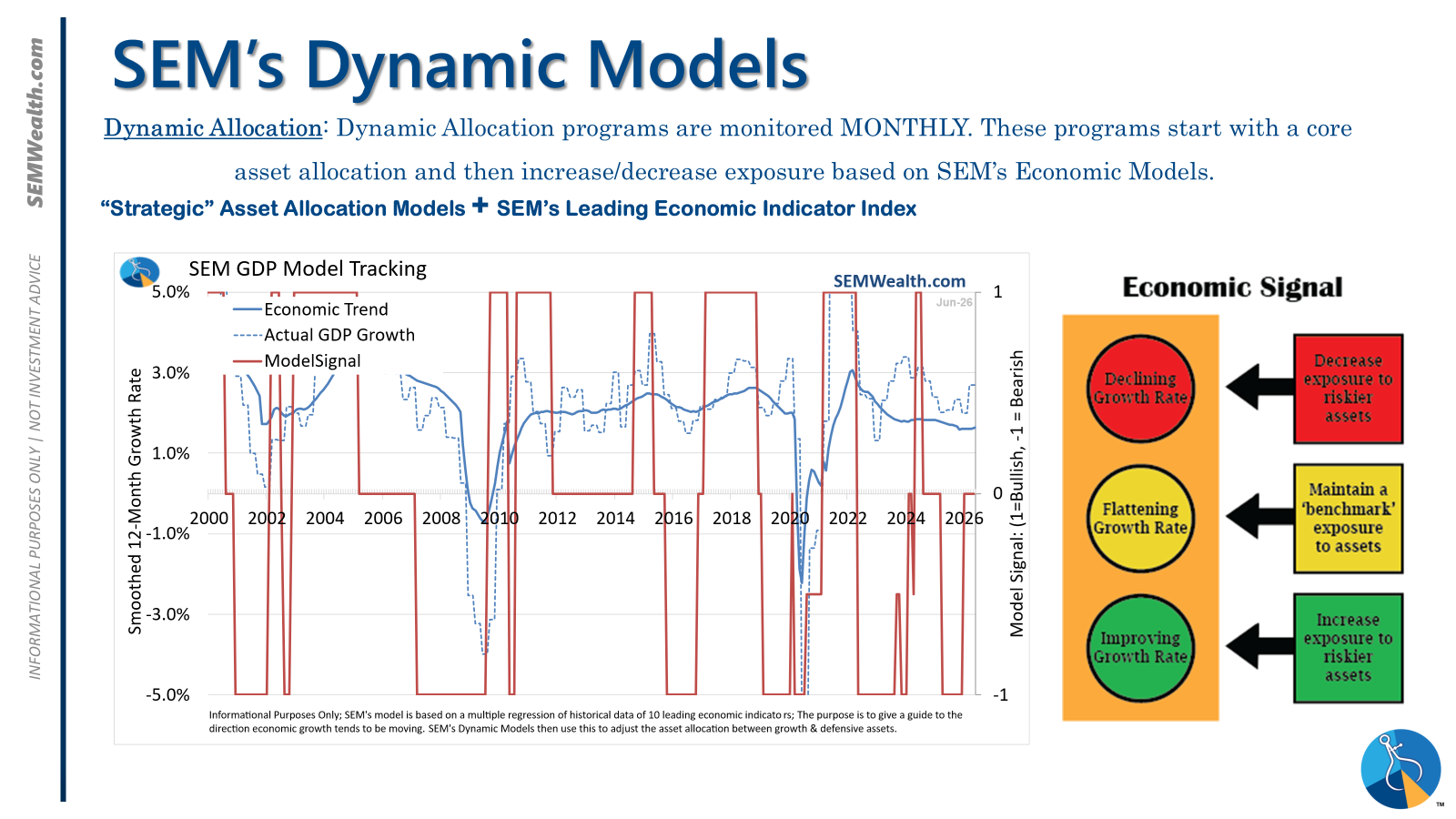

- Dynamic = NEUTRAL (2/15/2026) | "Benchmark" Allocation | Economic model inconclusive

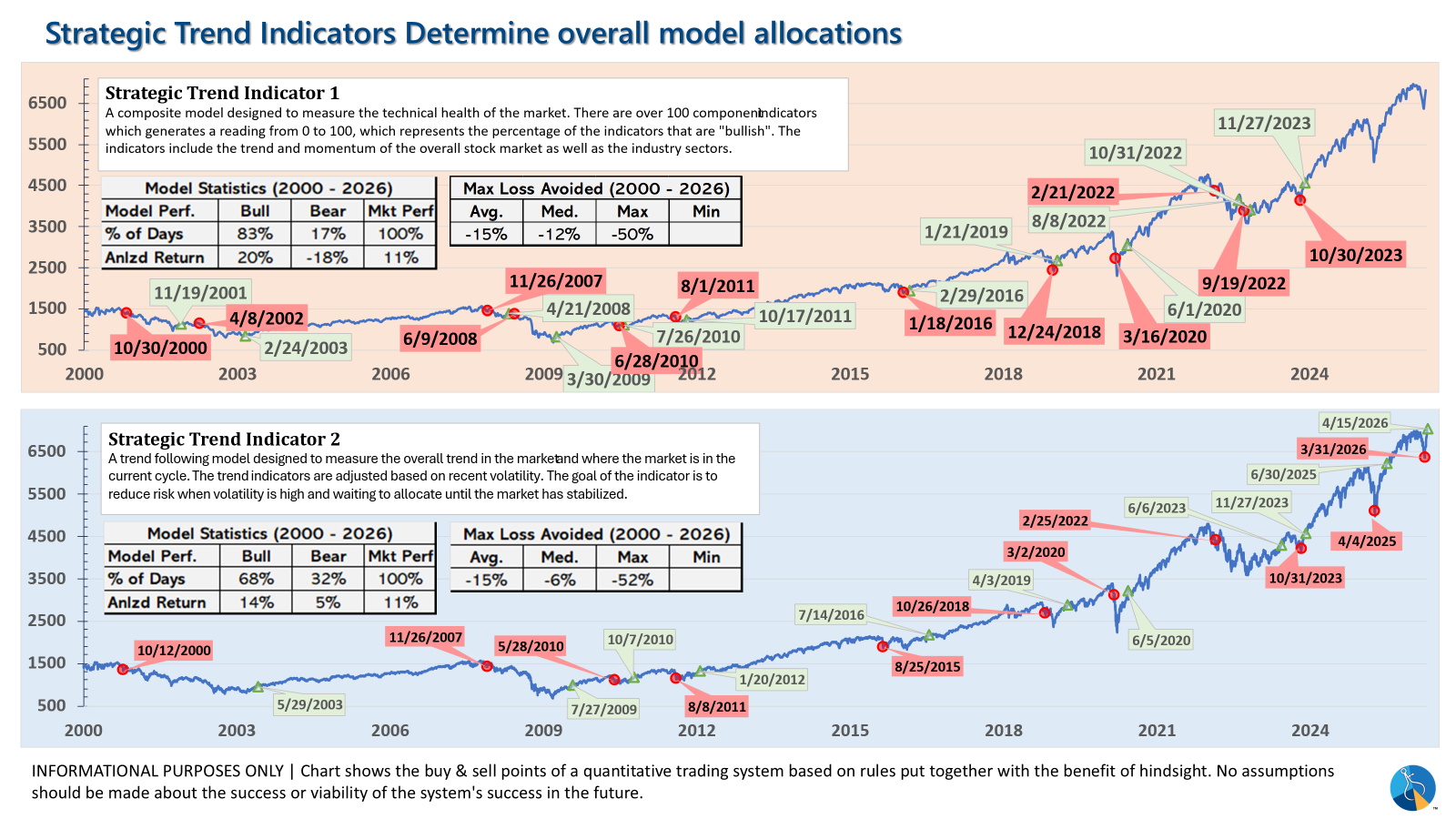

- Strategic = BULLISH (4/15/2026) | V-Bottom projecting "end" of Iran War

Tactical (daily):

- Monitored DAILY

- Models: Tactical Bond, Cornerstone Bond, Income Allocator, Tax Advantaged Bond

- Designed to follow the trends for use in our lower risk models

- BUY Signal issued April 8, 2026 (exiting the sell from March 13)

Dynamic (monthly):

- Monitored MONTHLY

- Models: All "Dynamic" Models (Income, Balanced, Growth, and Asset Allocator)

- Uses SEM's Quantitative Economic Model

- Designed to overweight riskier assets if economic trend is higher & underweight those assets if economic trend is lower.

- NEUTRAL signal issued February 15, 2026 (following BEARISH signal from July 2025)

Strategic (quarterly)*:

- Monitored QUARTERLY

- Models: AmeriGuard (Balanced, Moderate, & Growth) and Cornerstone (Balanced & Growth)

- Core Component: Quantitative Filter using 4 different time horizons across universe of asset classes

- Trend Indicator: Two different Quantitative Systems monitoring the intermediate-term trend, health of the market, and volatility

- CORE has been overweight small cap and international since October 2025 – overweight increased slightly in January

- Both TREND INDICATORS are BULLISH following 10% drop and "V-Bottom" reversal in early April

- AmeriGuard & Cornerstone Max DO NOT use the Trend indicator and are always 100% invested in stocks using our CORE rotation model.

The core rotation is adjusted quarterly. This quarter we saw half of our international positions reduced (we sold developed markets and kept our emerging markets exposure). We also saw the remaining share of mid-cap reduced in favor of more small cap exposure. We remain with a "barbell" core portfolio – about half in large cap and half in small cap as the models expect the market to "broaden".

The * in quarterly is for the trend models. These models are watched daily but they trade infrequently based on readings of where each believe we are in the cycle. The trend systems can be susceptible to "whipsaws" as we saw with the recent sell and buy signals at the end of October and November. The goal of the systems is to miss major downturns in the market. Risks are high when the market has been stampeding higher as it has for most of 2023. This means sometimes selling too soon. As we saw with the recent trade, the systems can quickly reverse if they are wrong.

Overall, this is how our various models stack up based on the last allocation change:

Curious if your current investment allocation aligns with your overall objectives and risk tolerance?