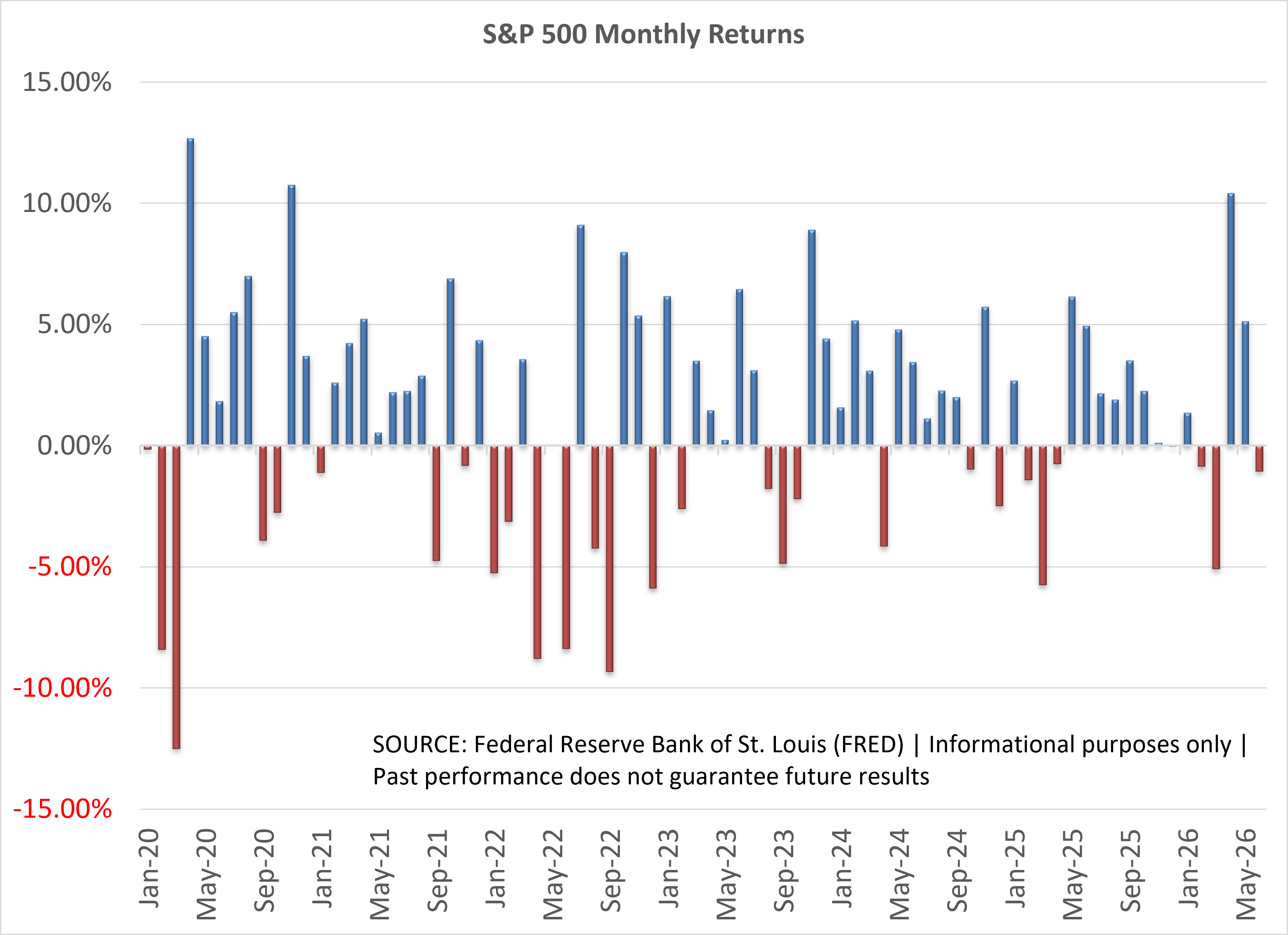

A Strong First Half

The first six months of 2026 rewarded investors who stayed disciplined through the volatility (or just flat out ignored all the frantic headlines). Despite concerns over inflation, interest rates, Middle East tensions, and whether AI-related spending could continue at its blistering pace, stocks pushed higher. Through June 30, the S&P 500 gained nearly 10%, the tech heavy Nasdaq Composite advanced 13%, with the Dow Jones Industrial Average trailing at “only” a 9% gain. Small-cap stocks were an even bigger surprise, with the Russell 2000 climbing nearly 22% in its best first-half performance since 1991.

The gains were led by strong corporate earnings and continued economic resilience that overcame higher oil prices and dire consumer sentiment. The broader rally also benefited SEM’s growth-oriented models. The bond market was essentially flat for the first half as the tug-of-war between inflation, oil prices, and an improving economy led to little commitment on the direction of interest rates.

Should you adjust your financial plan?

When markets are making new highs, it is easy to think financial planning matters less. In reality, strong markets are often the best time to revisit your plan. A rising market likely pushed stock allocations above target levels, creating more risk than intended. Retirees may find this year's gains provide an opportunity to refill cash reserves or review withdrawal strategies. For investors still accumulating wealth, higher account balances are a reminder that consistent savings and long-term discipline often matter more than trying to predict market moves. Successful investing is not just about maximizing returns. It is about making sure those returns continue working toward your goals.

Remember: The growth in the stock market has already increased your stock allocations if you haven’t rebalanced. For more see our “Bonus Content" below.

If you would like a personalized review of your portfolio, go to Risk.SEMWealth.com

Look Ahead: Opportunities and Risk

The first half of 2026 reminded investors of an important lesson: markets rarely move in a straight line, but they often reward patience and a disciplined approach. Despite concerns surrounding inflation, interest rates, geopolitical tensions, and the sustainability of AI-driven spending, U.S. equities delivered strong gains. Corporate earnings remained healthy, economic growth proved more resilient than expected, and market leadership broadened beyond a handful of mega-cap technology companies.

As we look toward the second half of the year, there are reasons for optimism. Businesses continue to invest heavily in productivity-enhancing technologies, consumer spending remains relatively healthy, and many companies are finding ways to grow profits even in an environment of higher financing costs. Small-cap and value-oriented stocks have also shown renewed strength, suggesting investors may be finding opportunities beyond the areas that captured most of the attention over the past few years.

That said, risks remain. Stock valuations are no longer cheap, particularly in segments tied to artificial intelligence and technology infrastructure. Interest rates are still well above the levels investors became accustomed to during the decade following the financial crisis, and any unexpected resurgence in inflation could influence Federal Reserve policy. Geopolitical developments also have the potential to create periods of market volatility with little warning. While these concerns may generate unsettling headlines, they are not unusual. Markets have always faced a wall of worry.

Rather than trying to predict the next correction or identify the next hot investment theme, we continue to believe the best approach is maintaining a disciplined process built around diversification, risk management, and long-term objectives. Opportunities will undoubtedly emerge over the coming months, but so will uncertainty. The longer the stock market hits record highs, the more risks we will see. Successful investing is rarely about making perfect predictions. More often, it is about staying committed to a sound plan while others are reacting emotionally to the latest news cycle.

The second half of 2026 may bring both surprises and opportunities. Our focus remains the same as always: protecting capital when necessary, participating in growth when available, and helping clients remain aligned with their long-term financial goals.

Bonus Content

What happens if you don't rebalance?

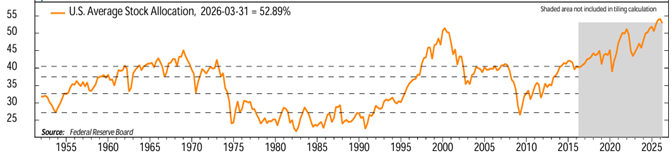

Earlier we posted a graphic of the household stock allocation, which has now exceeded the all-time high set in early 2000 (just before the tech bubble burst). While extended bull markets have always led to individual and professional investors to chase the returns higher, pushing more and more money into the stock market until it bursts, there is another simple reason we see so much money invested in stocks – - investors are not rebalancing their portfolios.

There are many benefits to rebalancing a portfolio, primarily it can lead to buying low and selling high (because you are selling your 'winners' to allocate to the 'losers'.) Since the stock market for 100 years has proven to be a "mean reverting mechanism", where extended periods of above average returns are followed by sharp losses (and sometimes 'lost decades' where stock investments are underwater for prolonged periods of time), a periodic rebalance leads to selling the assets that went up the most.

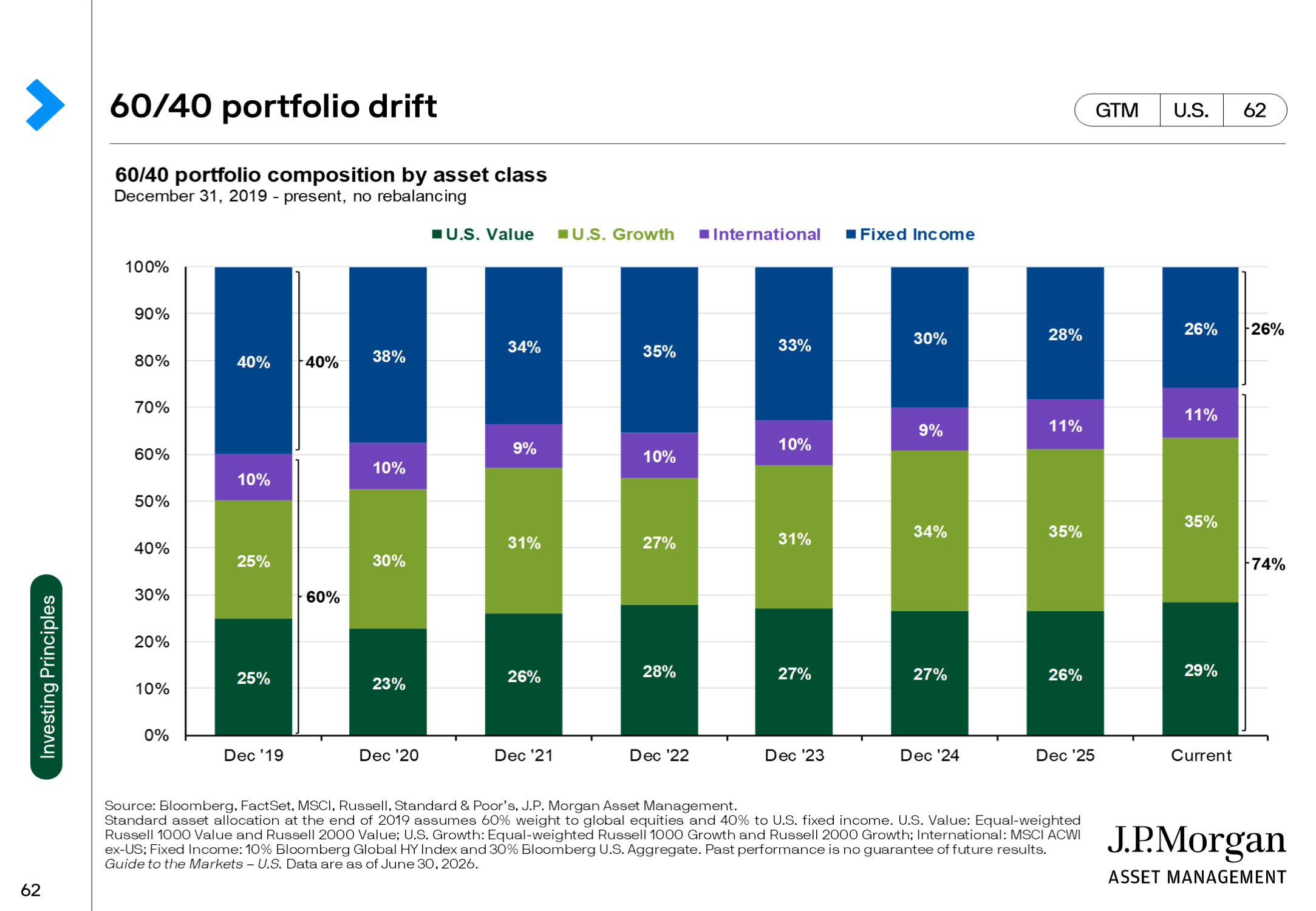

While every client is different, our own data has found the "average" investor prefers the risk-reward balance of a 60% stock, 40% bond portfolio. This is often referred to as a "balanced" portfolio. Below is a simple example of what would have happened to a 60/40 portfolio that started at the beginning of 2023 (the beginning of the AI mania) if you just "let it ride".

Not rebalancing means you are now in a 70/30 portfolio and no longer balanced. Your potential downside risk jumped by 6%, meaning your portfolio may be out of your risk objective bands. (Note, SEM has rebalance mechanisms for our clients already in place based on the financial plan, cash flow strategy, account type, and risk objectives, so if you are an SEM client you likely do not need to ask for a rebalance.)

JP Morgan took our exercise even further, diagraming what happened to a 60/40 portfolio started just before COVID in 2019 that was not rebalanced. The end result would be a 74/26 portfolio.

One of the biggest concerns we have when we see these numbers is the simple fact that we are now that many years older than when the AI mania started in 2023 or whenever it was the last time a portfolio was rebalanced.

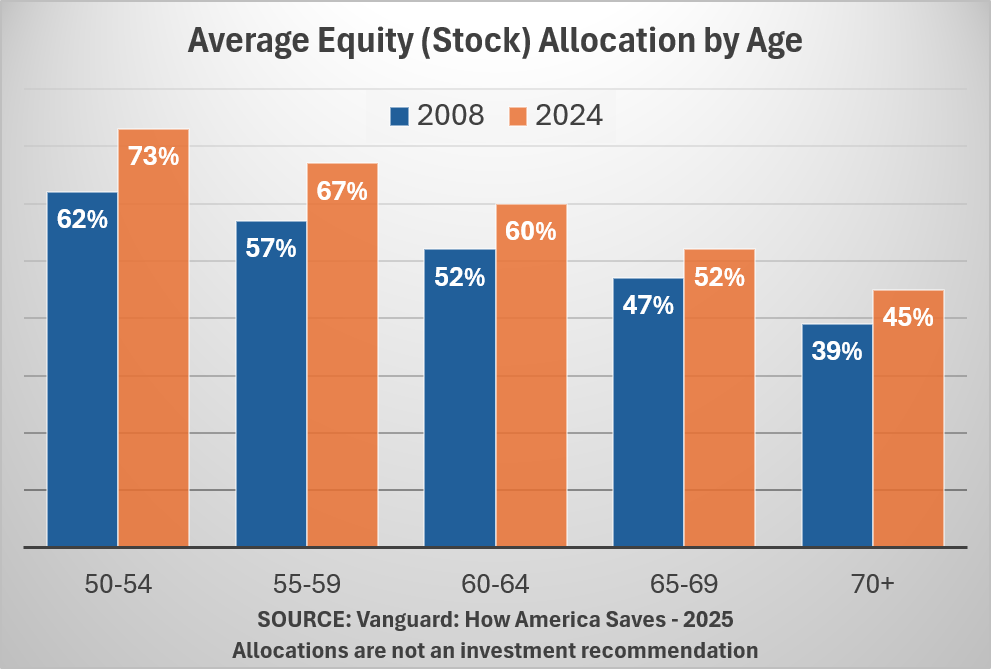

We talked about this in our newsletter last summer following the Vanguard "How America Saves" report which showed across the board, all age groups have significantly more money allocated to stocks than they did just ahead of the financial crisis.

The simple fact you are older does not always mean you should reduce your allocation. However, the strong performance of the stock market the last few years has led to all investments with stock exposure to post returns well above average (including the SEM models). This means it is likely your financial plan needs updated. The updated plan will likely tell a different story than it did just a few years ago.

The strong stock performance gives you FLEXIBILITY to (possibly) adjust your plan. As always, if you would like a personalized review of your portfolio, go to Risk.SEMWealth.com. This will kick off a review of your allocation by our team as well as a discussion with this allocation with your SEM financial advisor.

Is SpaceX in Your Index Fund?

On July 6, SpaceX entered the NASDAQ 100 index, which means owners of the popular QQQ ETF and any index fund tracking that index will automatically have a position after that day.

NASDAQ twice changed their rules to win the SpaceX IPO and to get it into their index. First they removed their "seasoning" rule (waiting a certain amount of time for trading to settle down) for "hot" IPO issues. They then added a "float multiplier" in an attempt to get a company like SpaceX which has only 4% of its shares currently trading to be a bigger portion of the index. Even with that, SpaceX will be a little less than 1% of the NASDAQ 100 or somewhere in the mid-teens in the holdings ranks.

Russell also changed its rules to allow SpaceX into their indices (in this case the Russell 1000 Blend and Growth indexes). Even though the "float" does not yet exceed their 5% threshold, Russell added them to those to indices at the close on Friday. Unlike NASDAQ, Russell did not add a float multiplier to boost SpaceX's allocation, so with just 4% of the shares outstanding available, SpaceX is a mere 0.1% of the Russell 1000 index (the largest 1000 US based companies in terms of market capitalization.)

In the months ahead, the "float" for SpaceX will increase significantly as employees and early investors have their restrictions lifted. SpaceX has a planned rolling release of the lock-up, mostly timed around earnings releases and specific calendar triggers. Elon's 42% of the shares (and his 80% of the voting rights) are locked for the first year of trading, which impacts the float adjustments used by the index providers. As it is currently scheduled, here is the changes to the float for SpaceX.

| Time | Float % (approx) |

|---|---|

| Today (July 2026) | ~4–5% |

| Aug 2026 | ~8–10% |

| Sep 2026 | ~20–25% |

| Nov 2026 | ~40–50% |

| Dec 2026 | ~60–70% |

| Mid-2027 (full unlock) | ~100% |

What this means for Russell and NASDAQ 100 index holders is you will see a greater and greater percentage of your index fund going to SpaceX. The 60-70% float by the end of the year would make SpaceX just inside the top 10 with a 2% position (assuming the price stays around the same level it is at today.) SpaceX would become a 3-5% position in the QQQ ETF, right around where Broadcom, Meta, and Tesla are currently.

The one index provider that refused to change their rules was S&P. S&P stuck to their "seasoning", "float", and "profitability" rules. SpaceX will surpass the "float" rules by September. S&P does not have a "fast-track" for IPOs, so the "seasoning" won't happen until June 2027. One of the biggest obstacles, however for SpaceX, is S&P's profitability rules. In order to be included in the S&P 500 index, a company must both post POSITIVE net income for the most recent quarter AND have POSITVE net income for the trailing 12 months.

During the most recent quarter SpaceX generated around $4.6B in revenue, but lost $4B overall. In 2025 they lost nearly $5B on $18B in revenue. They did make $0.7B in 2024 according to their filings. Starlink is generating lots of cash for SpaceX, but not enough for Elon's Starship division, and especially the xAI segment (which conveniently absorbed the money losing Twitter division and then was conveniently merged into SpaceX prior to the IPO.) Based on the fact SpaceX announced a $25B bond offering shortly after it raised $75B in its IPO, I'd venture to guess SpaceX is still burning through cash faster than Starlink can generate it.

Maybe it's good, or maybe it's bad to bend the rules to get "hot" IPOs into an index. This has actually led us to have a greater understanding of the differences between the Russell and S&P rules and why those indexes may deviate at various points in the market cycle (since Russell does not require profitability to enter its indexes and S&P does).

Note: This is not a recommendation to buy or sell SpaceX or any ETFs or index funds that may include them. It is simply information you might use to better understand the difference in index funds. Most of SEM's models include low-cost index ETFs or funds. They mostly are based on the S&P, but some do follow the Russell indexes. SEM does not take ownership of a specific stock into our allocation decisions.

Free Financial Literacy Tools

If you're reading this, you most likely have done a good job setting yourself up for financial success (since the bulk of our readers are SEM clients). One of our missions at SEM is to help increase financial literacy for younger generations to help kick-start their path to financial success. If you know somebody who could use some (free) help, we have a few resources available.

The first is our "Money Talks with Dad" series. We have a wide range of topics. This summer, we're posting 10 minute "clip" shows which consolidate various topics to make it easy to digest. The first was on starting out the budgeting journey by identifying "needs" versus "wants.

All of our episodes are available on YouTube as a Podcast. You can find that here:

The other resource is our Free Financial Assessment at WhatsMyScore.net

The quick, 5-minute assessment gives the user a score and a brief gameplan of the first things to work on. Included in the assessment is a free coaching session to answer any questions the user might have. If you know somebody who could use the assistance, we encourage you to forward these resources to them.

Download/Print version of the Newsletter

What is ENCORE?

ENCORE is a Quarterly Newsletter provided by SEM Wealth Management. ENCORE stands for: Engineered, Non-Correlated, Optimized & Risk Efficient. By utilizing these elements in our management style, SEM’s goal is to provide risk management and capital appreciation for our clients. Each issue of ENCORE will provide insight into investments and how we managed money.

The information provided is for informational purposes only and should not be considered investment advice. Information gathered from third party sources are believed to be reliable, but whose accuracy we do not guarantee. Past performance is no guarantee of future results. Please see the individual Model Factsheets for more information. There is potential for loss as well as gain in security investments of any type, including those managed by SEM. SEM’s firm brochure (ADV part 2) is available upon request and must be delivered prior to entering into an advisory agreement.