Throughout this entire series, we start with where our heart (or attitude) should be on the specific topic. Last month we looked at what our attitude towards saving should be. Take a look at it here if you missed it. Now that we have our attitude right, let's talk about three different types of saving funds.

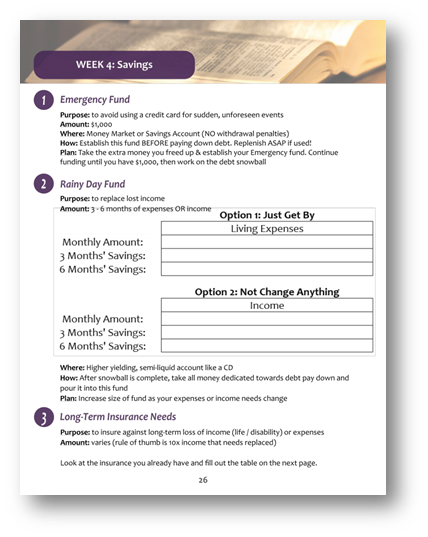

Emergency Fund

The emergency fund is designed to prepare for sudden, unforeseen events. Some of these events include an ER visit or other medical emergency, unforeseen car repairs, unforeseen and necessary home repairs (plumbing, HVAC, etc.) These sorts of things tend to be expensive and oftentimes people don't have the money to pay for them.

The goal should be to not have to put these expenses on a credit card. We discussed the dangers of credit card debt in this blog:

Here are two steps to create an emergency fund:

-

Save $1000 and put it in a money market account.

- A money market account is an interest-bearing account at a bank or credit union. You will slowly earn more from interest without having to do anything!

- Remember, this money is for emergencies only!

- If you do have to spend it, shift your focus to immediately funding it again.

-

Once you have the money in the account, shift your focus to eliminating your debt.

The next type of savings can honestly be tied into your emergency fund – the rainy day fund.

Rainy Day Fund

This savings fund is to plan for a loss of income. If someone loses their job or is out of work, it's typically for 3-6 months. Therefore, you need to have money saved to prepare for a loss like this. There are two options for this savings fund:

-

Just wanting to get by = 6 months of EXPENSES

- When looking at your budget, this is only the total cost of your necessary expenses. This will only meet your minimum needs.

- Choosing this route, you are required to shift your lifestyle because you won't have extra "fun" money for things like going out to eat, etc.

-

Don't want to change anything = 6 months of INCOME

- This route would allow you to continue the same lifestyle until you find another job (for 6 months).

Obviously you will need a lot more than $1000 put aside in savings if you were out of your job for months. This also isn't something that you'll be able to fund right away, it's going to take a lot of time. It is recommended to set aside 10% of your salary towards emergency savings. This money needs to be set aside as soon as you receive your paycheck so you don't spend it. As mentioned above, you should put this money in a money market account so you can earn more in interest over time. If you have extra income in your budget and have your debt paid off, you should try and put more money into savings until you build up to the 6 months of expenses or income.

These are both savings related to unforeseen circumstances. Having this money ready for these moments is important so you don't have to rack up debt when they come up. The last type of savings are more planning – long-term funds.

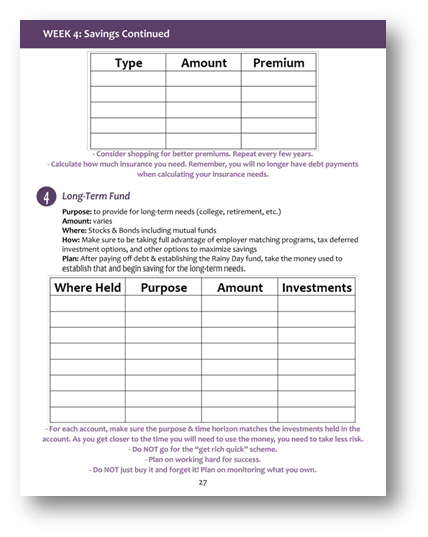

Long-Term Funds

There are three types of long-term funds I'm going to discuss this month: life insurance, college, and long-term investing. For all of these, I'm just going to give a brief overview. If you would like more information on any of them, please reach out to me and I can get you help.

Life Insurance

There is whole life and term life options. Take some time to look at the best option for your situation. The rule of thumb is that life insurance should provide ten times the income that needs to be replaced.

College

If you are planning on helping pay for your children's college, it's important to start early and look at all available options. Keep in mind all the different expenses that come with college outside of tuition if you are planning on paying for their whole college.

While it is nice to pay for your child's college, if you are in debt and don't have money aside for your retirement, then you should not put a focus on saving for their college!

Long-Term Investing

We will discuss investing more in a later blog, but here are some of the basics to keep in mind.

- Don't go for the "get rich quick" scheme because those don't work out.

- Money will grow little by little as it accumulates – be patient!

- You must understand risk vs. reward. I will talk about this more next time.

- If possible, max out your 401k or other company match programs. This is the only "guaranteed" way to make money with your investments.

Hopefully in the previous blogs, you've been able to work on your budget, or at least learn more about your spending habits. While saving isn't a fun thing to do, it's really important for your financial success! Take a look at the worksheets below and work though them over the next month.