We're starting the 7th week since the country began to shutdown due to the Coronavirus. We continue to see so much confidence in the forecasts from the big name Wall Street investment firms. The consensus is this is just a small bump in a bull market and you should both stay the course and put more money into the market. I hope they are right, but as I like to say hope is not a startegy. Hope for the best, plan for the worst is my motto.

I'm rarely bored. I always have plenty of ideas on my mind and they make it onto my whiteboard with the best ideas making it to a project in Microsoft Planner. This crisis has been a great opportunity for our systems to be stress tested and has generated new ideas. We haven't come up with anything as world-changing as calculus, but we do believe we've made some significant improvements that have us ready to handle whatever direction the market decides to follow from here. I still need to write-up all the improvements/tests. Hopefully when things slowdown.

I receive over 200 emails a day. Most get filtered out either to a junk folder or a reading folder. The first hour of each morning is spent reading those that make it to my reading folder. I also spend 2-3 hours Saturday and Sunday mornings reading some bigger picture thought pieces. I've been managing money for 25 years, 21 of them for SEM. I believe I've developed a pretty good filter for what matters, what doesn't, and what is complete BS. Here are some of my random thoughts as we start week 7:

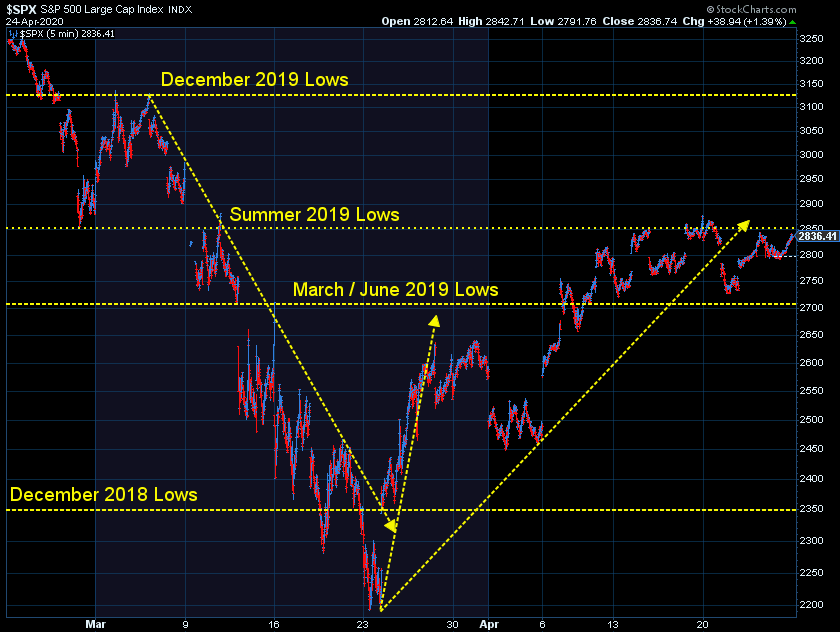

-Finally Consolidating: While CNBC pointed out last week was the "1st down week in 3 weeks", it was actually a postive week in that the market seems to be trying to take a breath and consolidate the huge move off the bottom. I don't know if it means much, but the bands for the consolidation were the spring and summer lows from 2019. For the short-term, you can consider a sustained move above 2850 a positive sign and a drop below 2700 a bad sign. (Not investment advice, with a market this volatile even technical analysis over short time horizons is not as reliable as it usually is.)

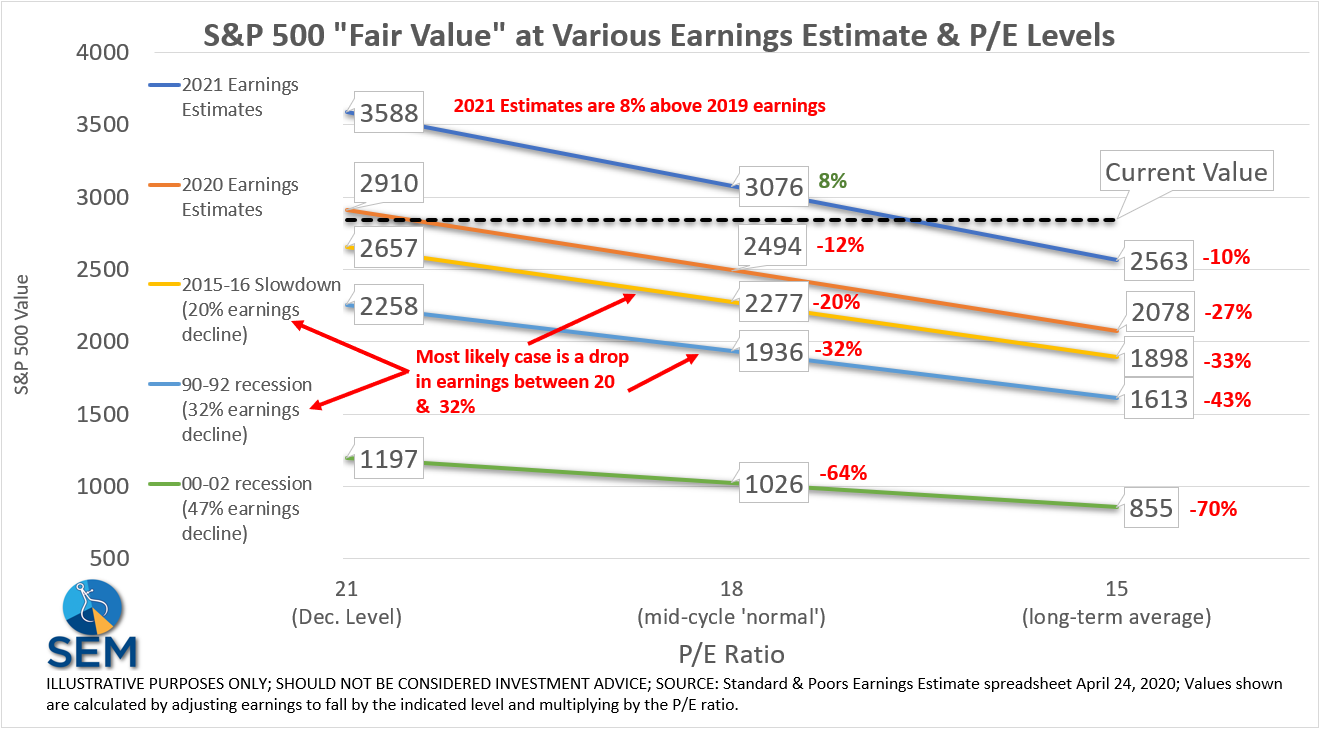

-Still Overvalued with Plenty of Downside Risk: Over the long-term, stocks maybe were a bargain for about a day back in March when they hit 2200. When you buy stocks you are buying all future streams of income. You have to determine what you think the stocks will earn and then what multiple of those earnings you should pay. The most simple valuation formula is to take the earnings times the P/E ratio. Of course with nobody having any idea what earnings will be, we see people ignoring the impact on earnings in 2020 and looking towards 2021.

I've been using this chart since 2018 to illustrate the different valuation numbers you can use. I argued at the beginning of 2020 that a P/E of 21 was way too high. The best values come when the P/E reverts back down to the average. Let's give the market the benefit of the doubt and say this is a "mid-cycle" slowdown, not a prolonged recession. You then can see what the "fair value" of the market is under different scenarios.

Right now, estimates call for 2021 earnings to jump all the way back ABOVE 2019 earnings by 8% (after falling by 12% in 2020). Even with that spectactular recovery (22% jump from their 2020 estimate), stocks are only 8% undervalued. So a reasonable upside right now is about 8%. Your downside is somewhere between 20 to 32%. I don't know about you, but that's not too attracive to me, especially when you consider even during good times the FORWARD P/E (Price times FUTURE earnings) is around 15, which means stocks are 10% overvalued based on the current 2021 earnings estimates.

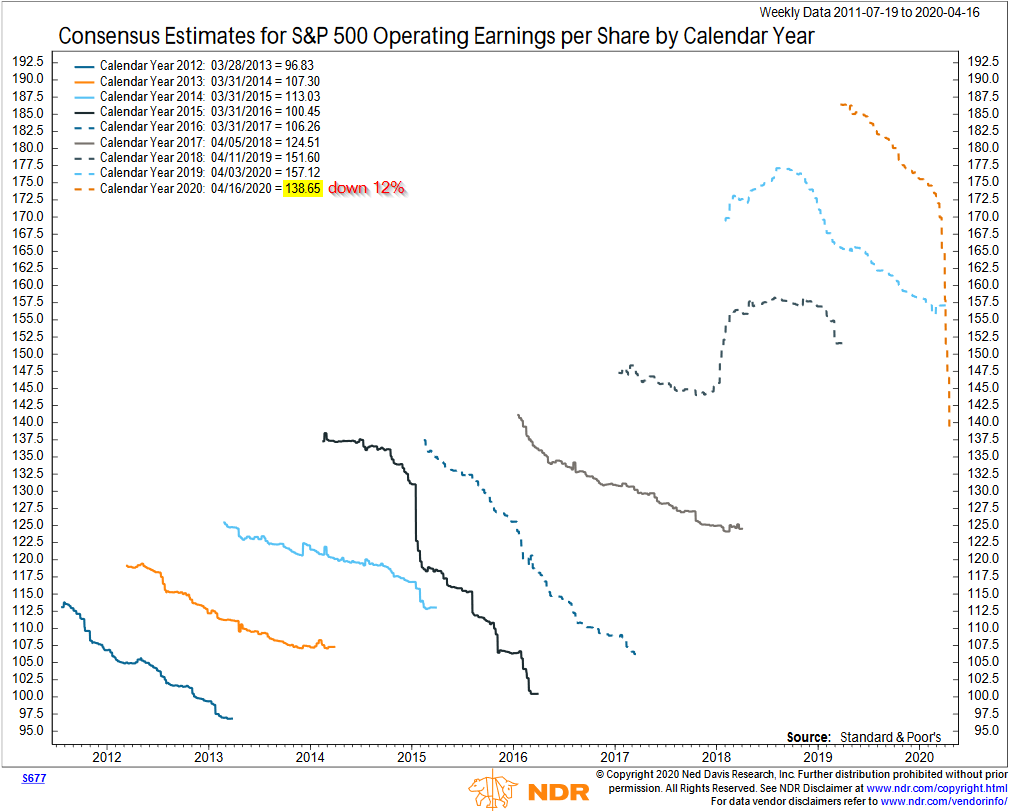

-Anlaysts are Terrible at Forecasting Earnings: Garbage In-Garbage Out. This chart from Ned Davis really illustrates how wrong analysts are with their estimates. They also are almost always way too optimistic with their expectations. This puts an underlying bias to the upside in stock prices........until earnings are so bad people wake up and adjust their valuations accordingly.

-Do you really think the damage done to the economy is only 13%? If so, you should buy stocks right now. If not, your stock portfolio is overvalued. Stocks are only down 13% from their highs. As Howard Marks put it, "the world is more screwed up than 15%". This isn't (yet) a bear market. There are far too many people who want to buy stocks simply because they are down a little bit. A real bear market leads to people thinking you're crazy for owning stocks. Any rallies from here will only make the sell-off that much worse when the reality of the economic damage of this crisis becomes apparant. I hope I'm wrong, but again, hope is not a strategy.

-The Market is Not Efficient: One of the things I enjoy about Facebook Memories is looking back at things I posted in the past. Over the weekend I saw this post from 2 years ago. As you might recall the Fed had been raising interest rates and winding down their balance sheet (finally reducing the stimulus from 2009). 10-Year Treasury yields had moved up to 3% (remember that?). Here's something I said then that remains relevant today:

Here’s the problem with the efficient market theory passive proponents have pushed on everyone the last 3-4 years — NOBODY knows what the future may hold. This means the valuation models used by the “market” have inputs that are unreliable. The key variables in all market valuation models are expected earnings, future growth rates (both near-term and perpetuity), the market risk premium (how much you need to be paid for taking on stock market risk), and interest rates.

I also included this comment on LinkedIn:

From the beginning of markets, prices have always been about supply and demand. If more people buy than sell, markets go up and they go down when the opposite happens. Despite all the technology, information, and education, buy/sell decisions are still driven by emotions. Think of the “fundamental” value managers. The key drivers to a valuation estimate are how much you think a company will make in the future and what is the proper risk premium. If you are overly optimistic both your estimates and your risk premium will lead to extremely high valuations. If you are overly pessimistic you see the opposite. So in other words, markets behave as they always have because they have always been driven by human emotions.

Don't fall into the trap the market is "all-knowing." I heard the market strategist from a big name Broker/Dealer on CNBC say late last week, "clearly the market knows something that we don't. We should trust what the market is saying because it always knows more than we do." I was dumbfounded. What's sad is this "independent" Broker/Dealer won't allow their advisors to work with us because we are "too small" at $500 Million under management.

-Capitalism as we Know it Has Changed Forever: Famed investor Leon Cooperman's CNBC interview last week was recapped in Market Watch (thanks John S. for sharing) listing the 10 things changed by Coronavirus. As you can see the list contains many of the things I've been discussing the last 7 weeks:

1. Capitalism is altered due to the impacts on economies from the viral outbreak

2. Politics in the U.S. are moving more to the left: “Taxes will have to go up.”

3. Low interest rates may be lasting and are indicative of ‘a troubled economy.’

4. Consumer demand will come back slowly unless there is a vaccine for the coronavirus

5. Businesses will face compliance costs related to the virus

6. Lots of equity issuance will be required to “replace lost capital.”

7. Stock buybacks, one of the markets biggest drivers, will fade away

8. Profit margins at corporations will revert to the mean

9. Credit is cheaper than equities

10. A quiet Warren Buffett, a white knight in the last crisis, is a bad sign for the long term

I've mentioned #10 many times. Those of you who believe stocks are a good value right here should pay attention.

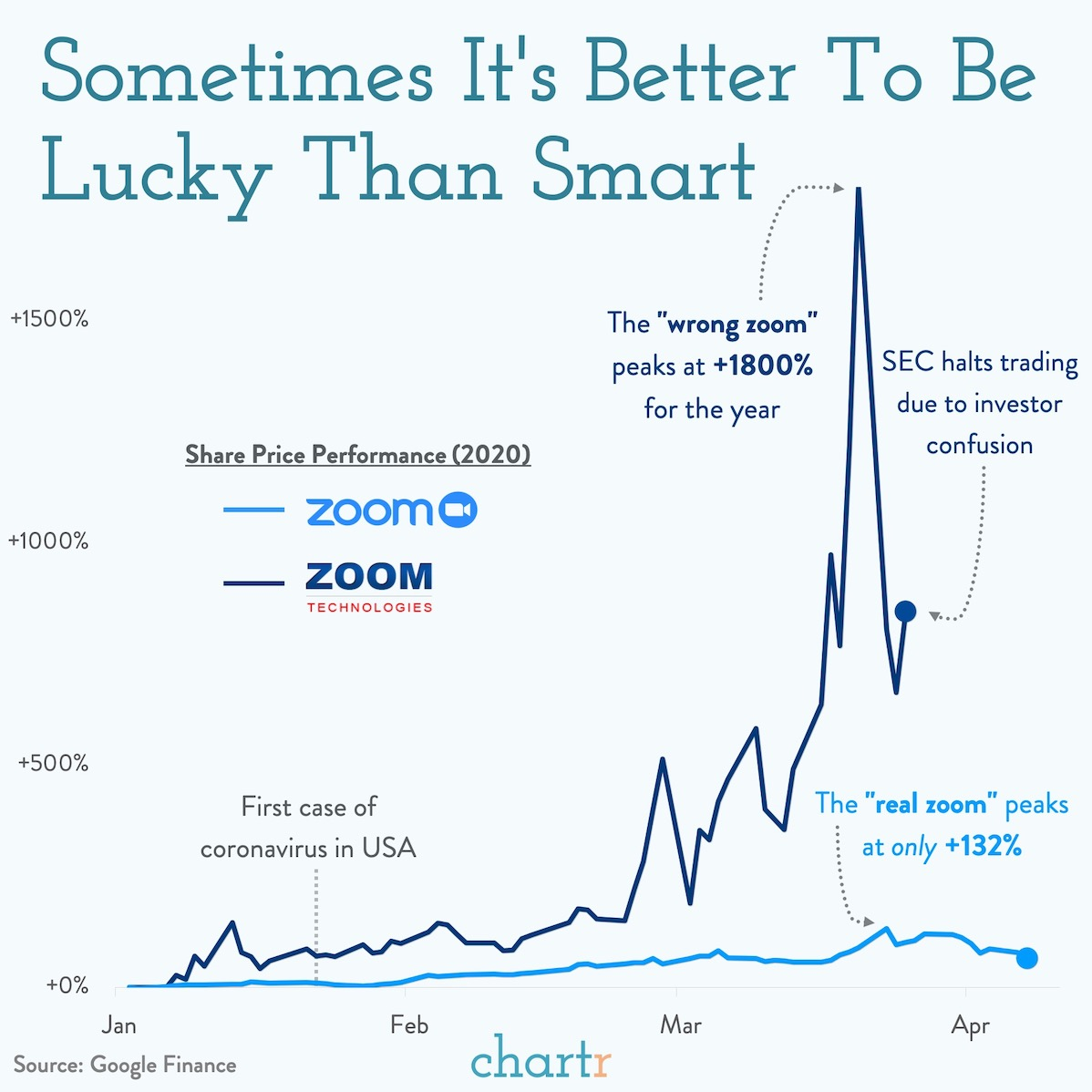

-Zoom Boom: The boom in the use of Zoom Communications (ticker symbol ZM), also helped Zoom Technologies (ticker symbol ZOOM). (Source) This reminds me of the 1990s when the wholesale food company Sysco would see a jump in their stock when tech company Cisco would report earnings.

-How Did They All Miss This Opportunity? Zoom has become the Kleenex of online meetings. Despite the security concerns, everyone seems to be using Zoom. We used to use WebEx, one of the first movers in the industry, but the lag in calls was so aggravating (plus the cost). We then moved to Join.Me and liked it better than WebEx. As we migrated to a Microsoft "ecosystem" we've been using Microsoft Teams. We kept our Join.Me account because Teams was harder for a non-Teams user to figure out how to navigate. This year Microsoft has stepped up their game and fixed a lot of the usability issues. As far as we can tell they are the only online meeting service that doesn't require the other user to download software on their computer to use their camera and share their screen. The NFL Teams all used Teams for the draft last week and by all reports the software worked well. We won't use Zoom even though it is still slighlty easier for the end user to utilize. We just can't trust their security. If you are a Microsoft 365 subscriber it is easy and cost effective to add Teams to your subscription.

-Huge Impact on Commercial Real Estate: Whatever technology ends up gaining the most marketshare, I think many managers have learned you don't necessarily have to have everyone in the office to be productive. I'd be especially cautious with any commerical real estate related investments. Prime office space is prohibitively expensive. We ended up opening our Virginia office in a quiet, rural office complex where the rent is 1/3 as much as in the city. The building we were supposed to be in when we first relocated here was near capacity and offered little room for growth.

-Not All Changes will be Bad: Our 13-year olds participated in their first "game night" with their teen youth group at church. The prior weeks they said, "this sounds dumb." We encouraged them to try it. It started at 8 Friday night and they were still going at midnight when their "screen time" apps shut them down. The next morning they said, "that was so fun. I can't wait until next week." For us it was great to have them doing some supervised online games from the safety of our basement while interacting with their friends from church.

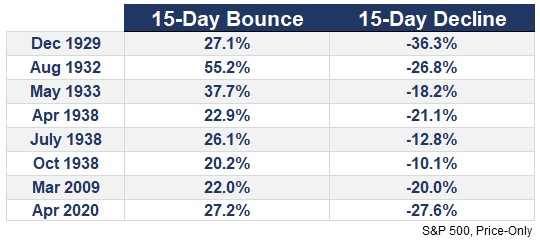

-As Volatile as the Great Depression: Too many people are getting excited about the bounce in stocks (like the guy from the B/D who thinks stocks know something we don't). This table from Ben Carlson over at 'A Wealth of Common Sense' shows that each time we've had a huge 15-day bounce it was on the heels of a large 15-day decline.

Other than the March 2009 bounce, there was still a lot more downside to come based on this data. Keep in mind the March 2009 bottom came after an 18 month bear market and deep recession.

-Oil Shocker: Last week we saw oil prices temporarily go negative. It seems we have so much oil, there's not much room for storing it. It's prohibitively expensive to shut a well all the way down so the price indicated producers being willing to pay to have somebody take the oil off their hands.

It also turns out that once again contracts which are designed to be used for actual hedging of prices are hurting speculators. In a world where there's an ETF for everything, the USO ETF, which is supposed to track oil prices has been hammered. The USO ETF issuers are not producers or users of oil, but are constantly buying oil futures contracts and then rolling them to a later month as they expire. That works fine unless they have a bunch of redemptions and have to sell their futures contracts prematurely. Warren Buffett called derivatives "financial weapons of mass destruction". Once again, here is a perfect example of how quickly you can lose money if you are speculating in something you shouldn't be. Clearly no regulator will protect people from idiotic products like this, so it's up to us to educate people from the danger of these types of investments. It's hard to see on the chart, but this is an 83% drop in the price of the ETF since September.

Not to be outdone, it's being reported The Bank of China's clients are on the hook for at least $1 Billion of losses from the drop in oil prices. These aren't Chinese oil companies, but individual Chinese investors the Bank of China recommended these investments to.

-A Bailout Isn't Always the Answer: In the midst of the drop in oil prices, the President and other Administration Officials promised they would be working on a bailout for the oil companies. I understand needing to save these jobs, but giving these companies more money to continue producing oil will only make the problems worse. All the infrastructure projects promised during the election never happened. This included expanding our oil storage and transportation capacity. If we can't store the oil and move it efficiently, what's the point of a bailout? Seems we could find a smarter way to spend the money.

(Note: I'm not calling the president stupid, just the idea that bailouts are the answer.)

-A Deflationary Spiral: In addition to oil prices, we are in danger of going into a deflationary death spiral as consumers realize all the things they thought were important to spend money on three months ago are not as important when your job can be wiped out immediately. This is why the Fed has reacted so aggressively. They'd love to have their emergency actions cause inflation. Deflation is so scary because it encourages consumers to delay spending. If you see car prices (or any other big ticket items) moving lower every month you have no urgency to spend.

-Social Cycle Predicted This: CNBC interviewed Neil Howe on Friday. He's the author of many books and one of the country's top demographic experts. Long-time readers will recognize his name. I've mentioned the social cycle many times and the consequences it will have for our country in the coming years. We are in the midst of the crisis. I last wrote about this a few years ago in "The Consequences of Political Polarization". I'd recommend you bookmark it and digest what it means as this will play a key role as we move through this current crisis.

I still have down on my list to attempt to put this critical concept into a short, easily digestable seminar/webinar. It's such a broad topic I'm having a tough time. Neil obviously does a better job than I can. Here's his interview from last week:

-Social Security Even Closer to Insolvency: A year ago I posted an article walking through the report from the trustees of the Social Security and Medicare programs which discussed the solvency of those key "entitlements". In the article I specifically mention how the projections do not include the impacts of any recessions. Their growth rate was not realistic and this crisis will make it even worse. I'd encourage you to take a look at "One year closer to insolvency" before you invest in a manager who follows a buy and hold strategy.

-Lots of Experiments: With several states already releasing their restrictions on most businesses and many more ready to do so soon, we'll start getting plenty of data on a lot of the hypothesises on the Coronavirus in about 2-3 weeks.

For now, the curves still look favorable.

-We'll Never Be the Same: Our twins never got to take me to the airport and sit with me while I waited for my plane like their older siblings did. They've never gone to a sporting event where your bag wasn't checked and you had to walk through a metal detector. We don't know how many things will change, but we do know our world won't go back to what it was like in January. I'm not sure if the market is pricing that in yet. We were blessed to have our 2-year old granddaughter stay with us over the weekend so her mommy and daddy could have some much needed peace and relaxation. Brandi and I got a good laugh when she got a wipe to clean her slide before using it.

I hope this brought a smile to your face. We are facing a very scary, uncertain future, but I am a big believer in America. I'm just not a big believer in the "efficiency" of the market. Stay tuned to the blog. There's so much more to cover as we work through this. As we've done for the past 28 years we'll be there for you and ready to adapt to whatever comes next.

Have a great week!