"It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done." - Federal Reserve Chairman Jerome Powell, November 30, 2022

The above statement is the only thing that should matter if you are assessing the market prospects for the first part of 2023. However, this is the only statement market participants heard:

"It makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting."

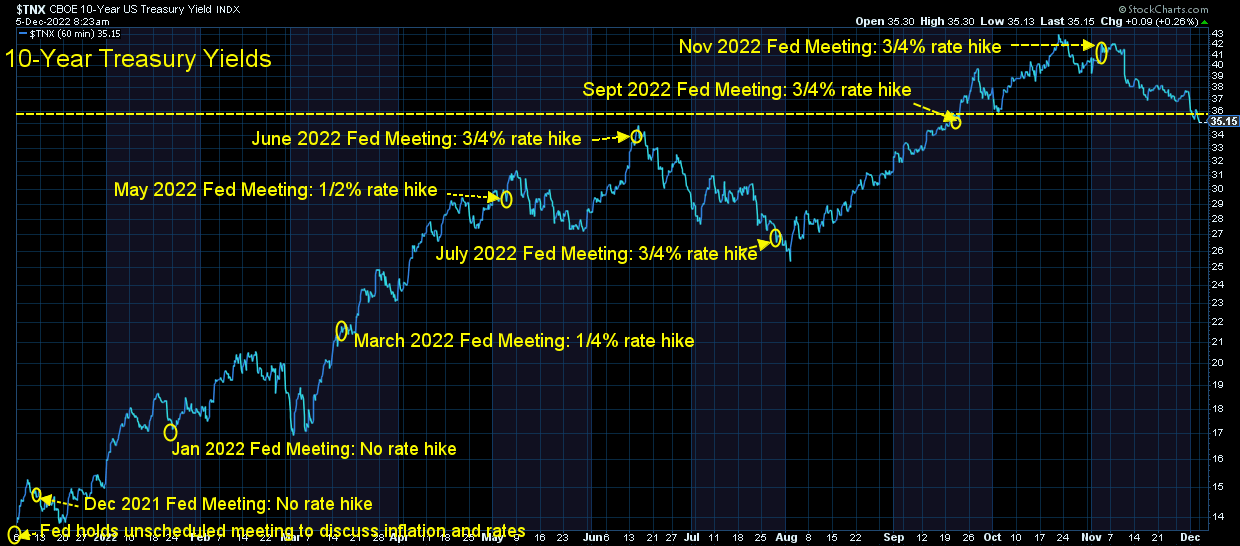

In other words, instead of raising rates by 0.75% in December, they are likely to raise rates by 0.50%, which by the way is exactly what everyone already expected following the last Fed meeting. This laser focus on the pace of interest rate hikes is dangerous. It takes 9-12 months for one change in monetary policy to filter all the way through the economy. That means we are just now feeling the full impact of the first 0.25% hike back in March.

If the Fed follows through with a 0.50% hike in December that will bring the total increases to 4.25% for 2022. Think about this – a year ago short-term interest rates were 0% and long-term rates were around 1.3%. Now short-term rates will be above 4% with long-term rates around 3.7%. This is a MAJOR drag on the economy (and should cause inflation to return to 'normal' levels). In my opinion the focus shouldn't be on inflation and what it means for Fed policy but instead what this hike in borrowing costs is doing to the economy.

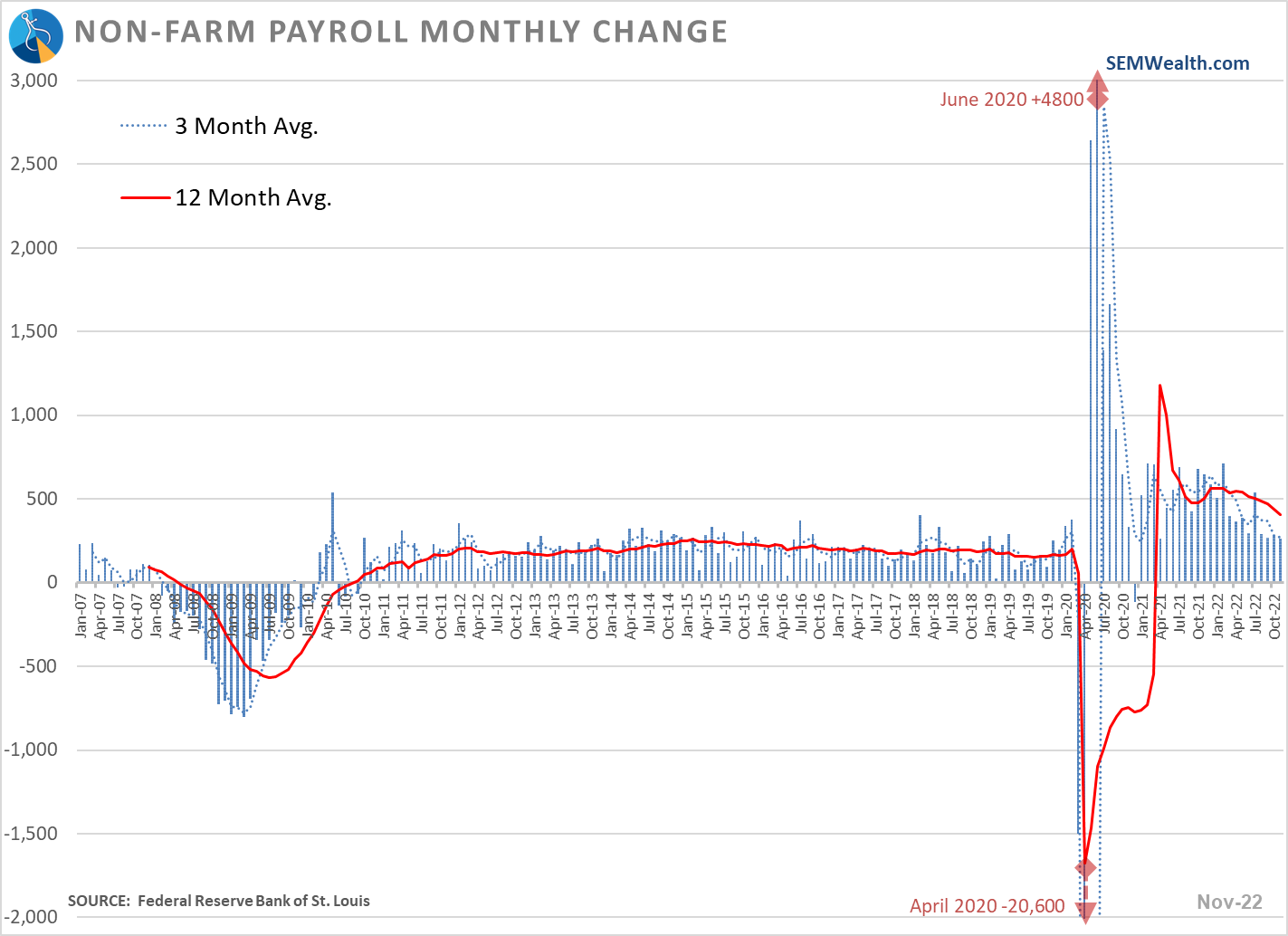

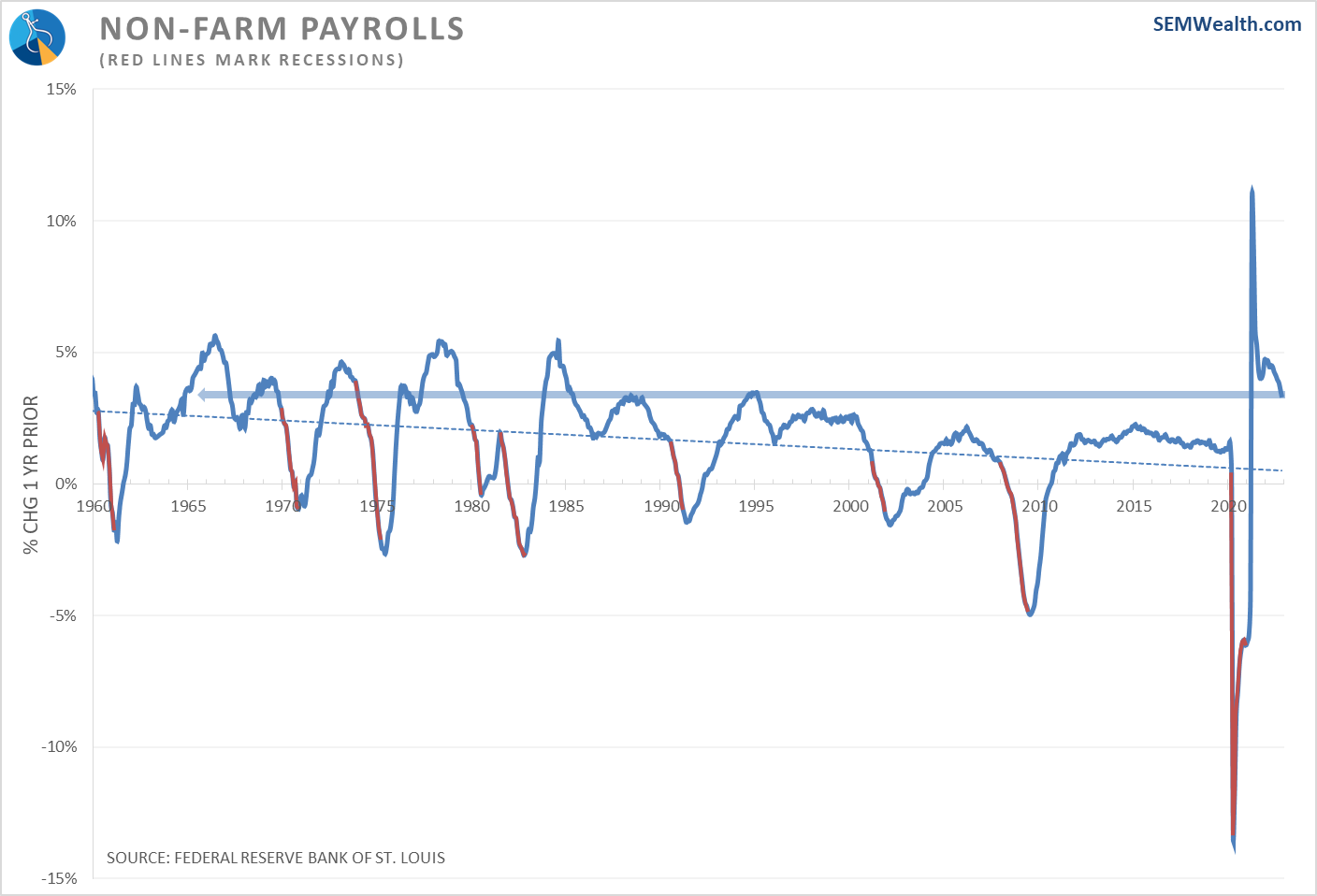

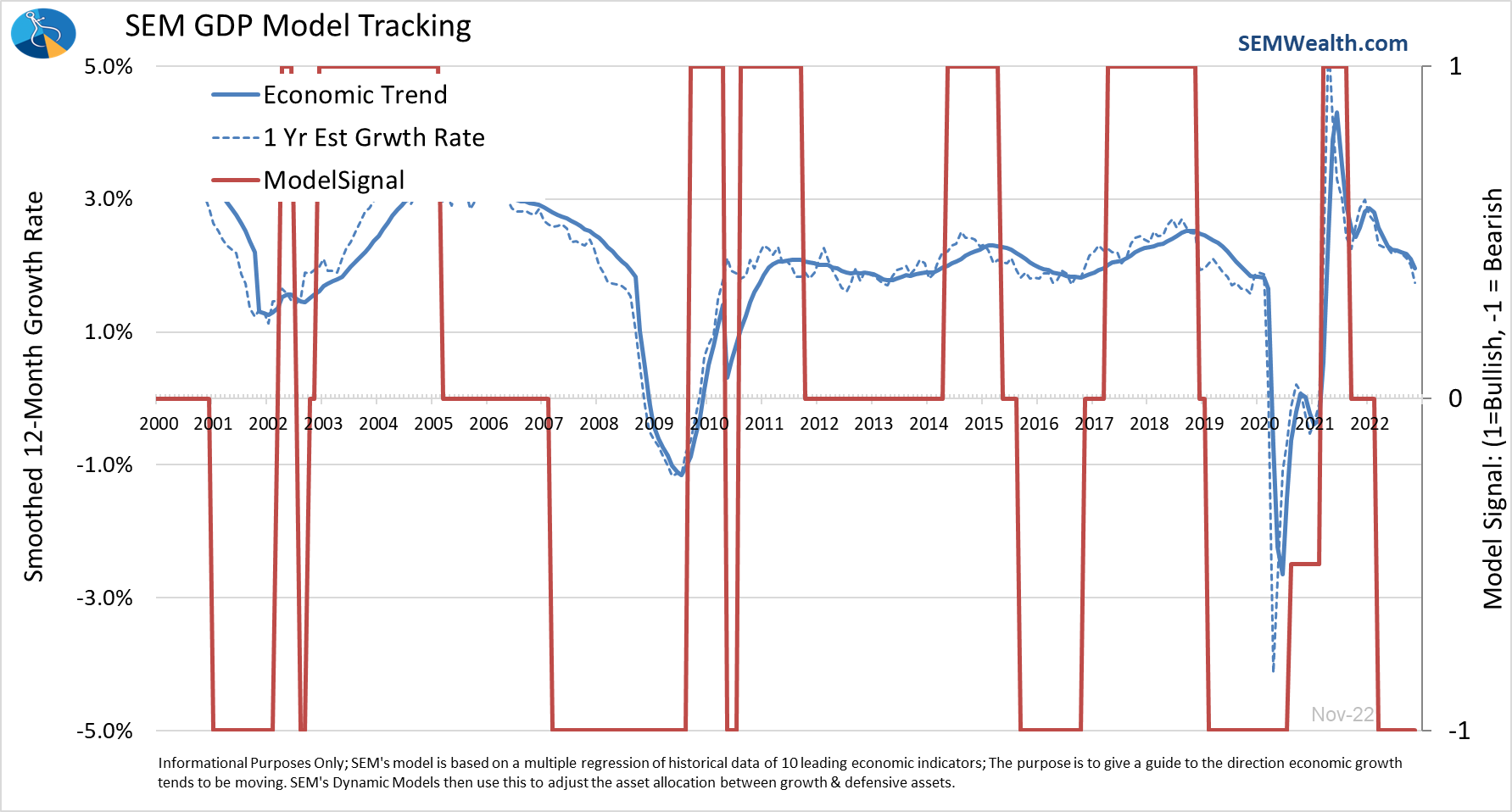

Our quantitative economic model, which was developed in 1995 and systematized in 2001 has been warning about an economic slowdown since April. This month's update shows an economy that appears to be rolling over. Since April, the one bright spot has been the labor market. Despite a headline number on Friday stating the labor market was "hotter" than expected, our data shows both the number of jobs and the hours worked index are slowing. What matters most for economic growth is whether or not the various components are better or worse than a year ago.

While the growth in jobs continues to be far better than any other recovery this century, it is contributing LESS to economic growth than it was last year (or even a few months back).

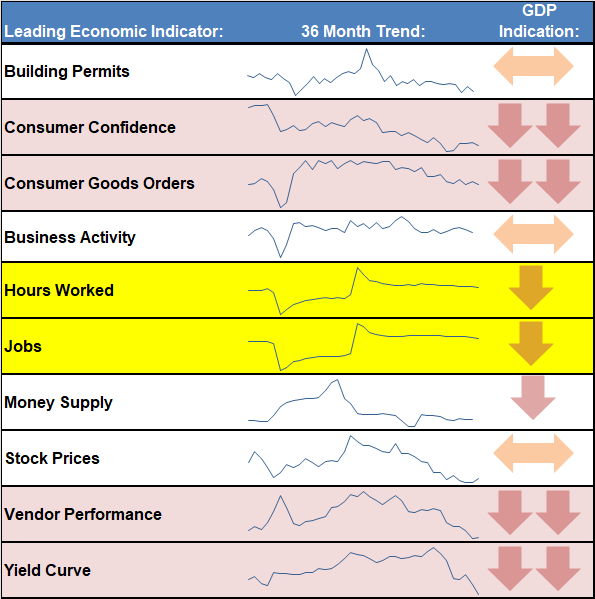

Looking at our dashboard, we no longer have any positive indicators. The fall-off in October and November was so stark in a few of the components (in terms of a drag on economic growth) I added a double down arrow.

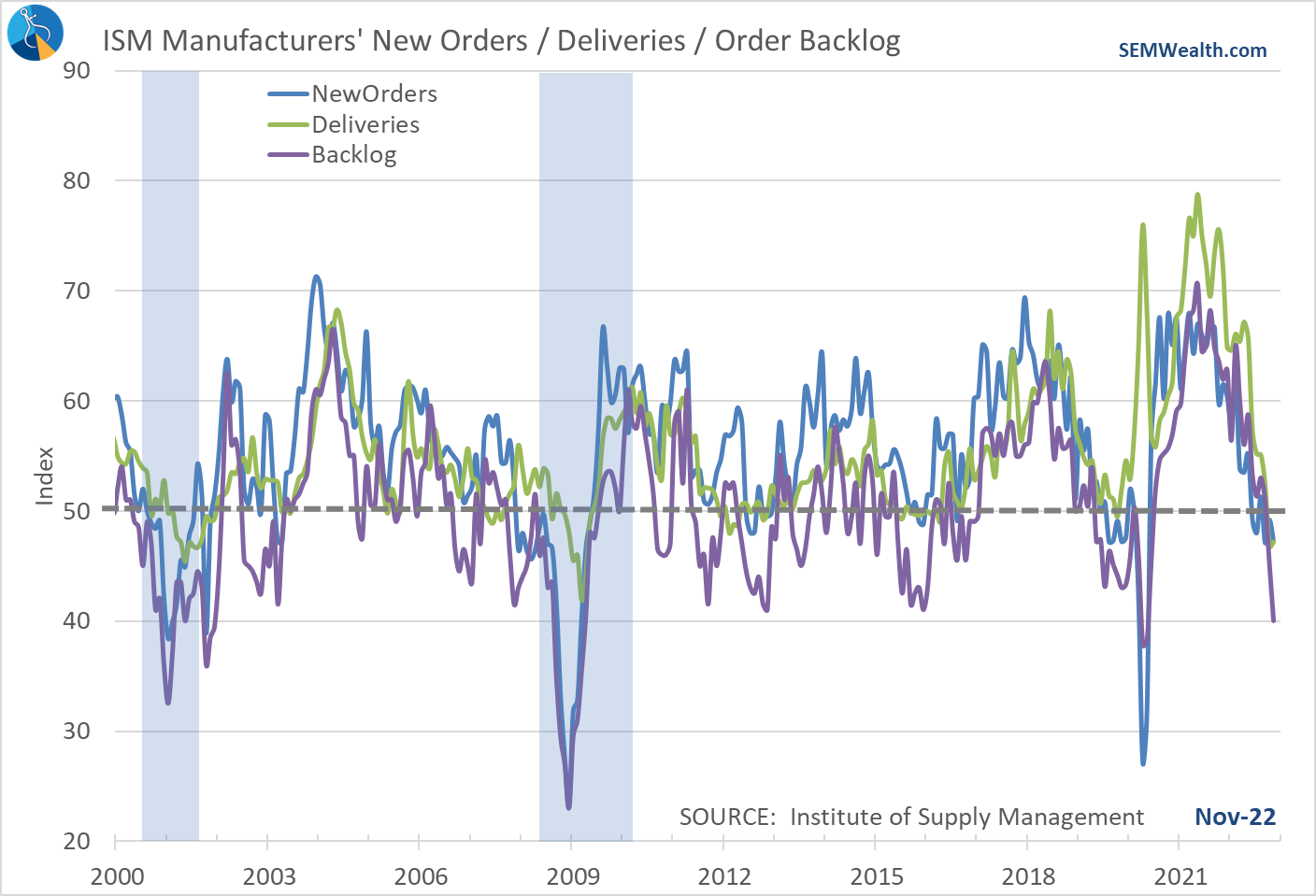

The ISM Manufacturing report continues to be one of the best leading indicators. There are sub-components which help illustrate weakness far earlier than most leading indicators. This chart looks at some of them. All of them are clearly in "recessionary" territory (below 50).

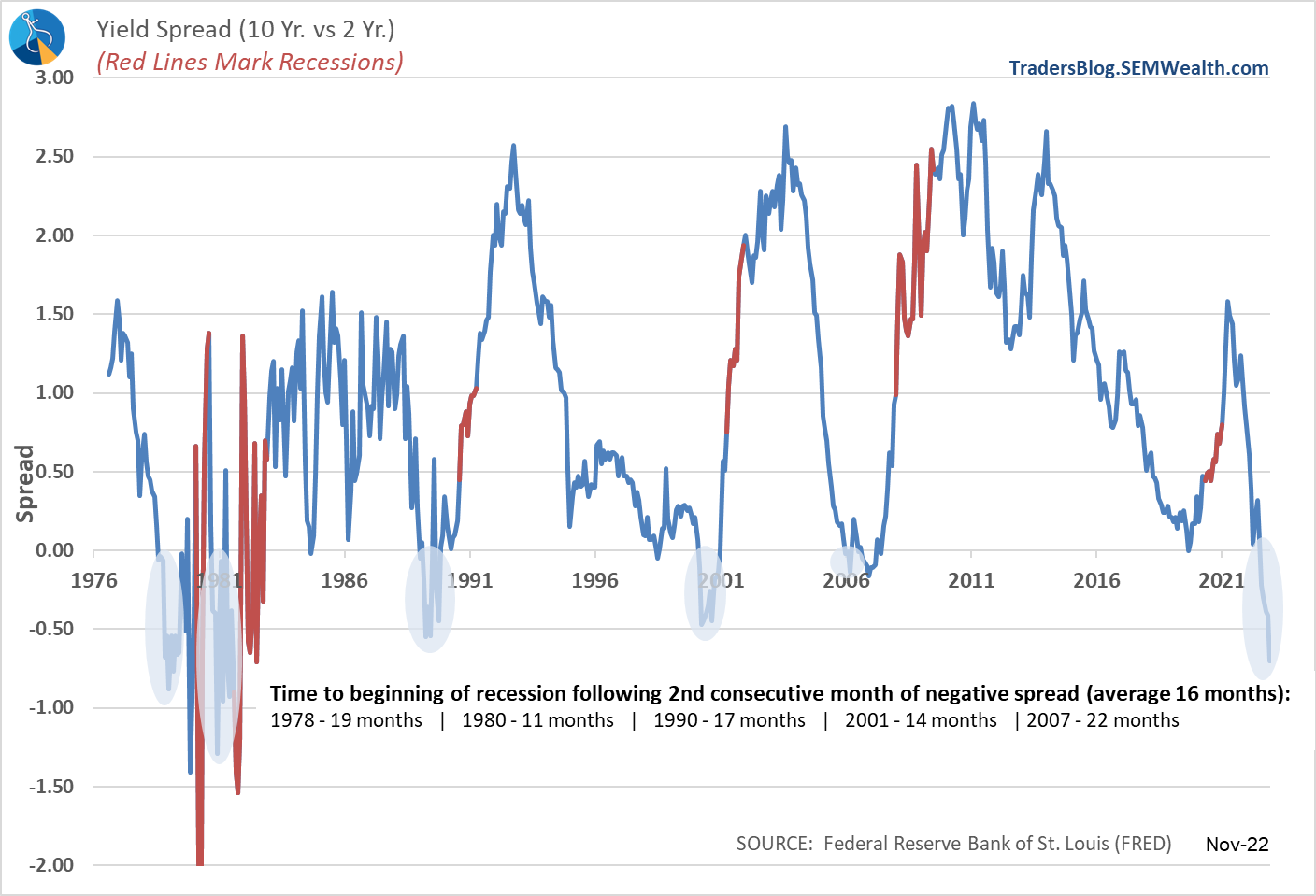

The yield curve has also been a reliable leading indicator. The spread between short-term rates and long-term rates has not been this negative since the early 1980s.

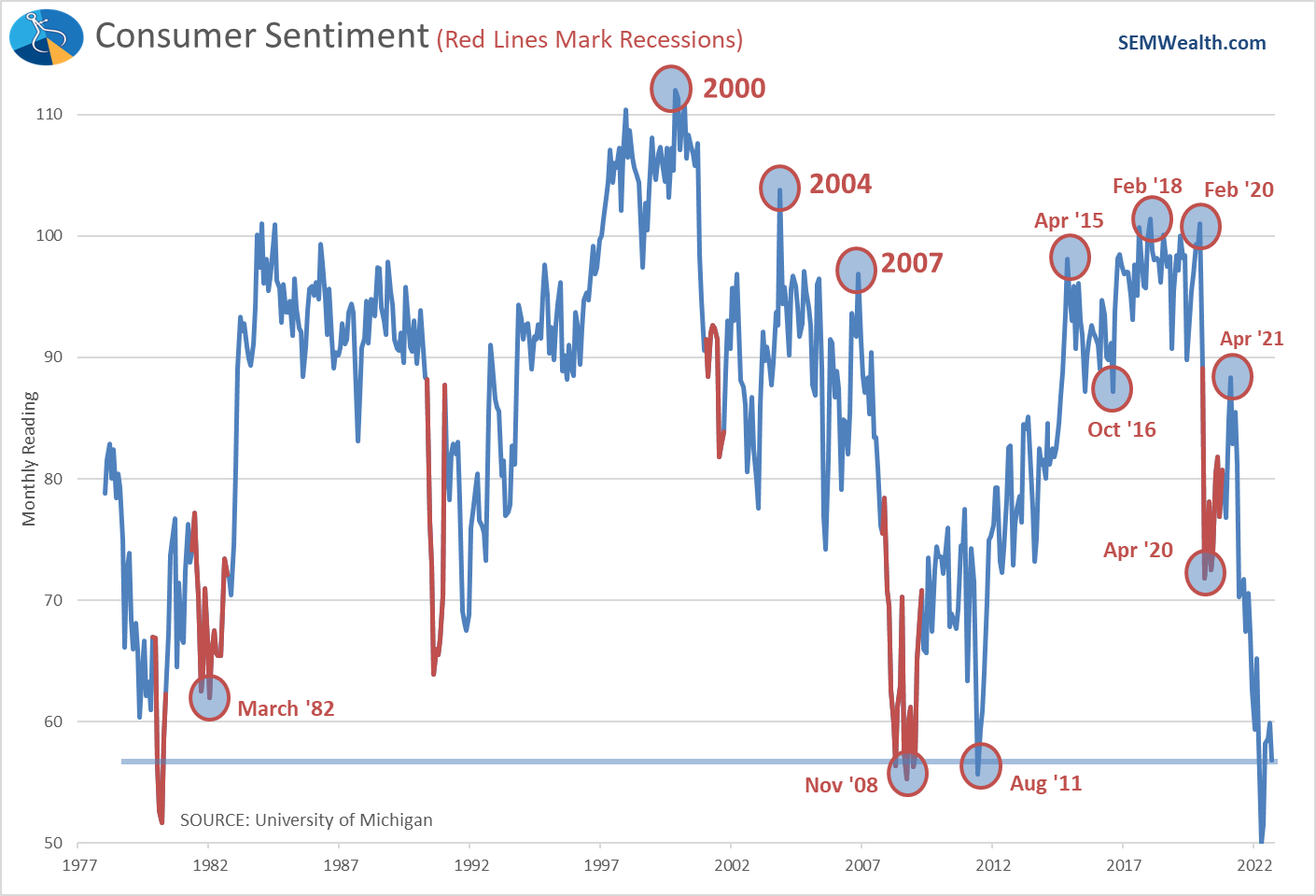

We've also seen Consumer Sentiment roll back over the past month. Consumer Spending has remained strong, but it's likely if sentiment remains weak we see it rolling over in the months ahead.

Another indicator which is technically still "neutral" in terms of economic growth contribution but rolling over is Building Permits. It's obvious the spike in permits was skewed by COVID and now with rates significantly higher the number of new houses should slow.

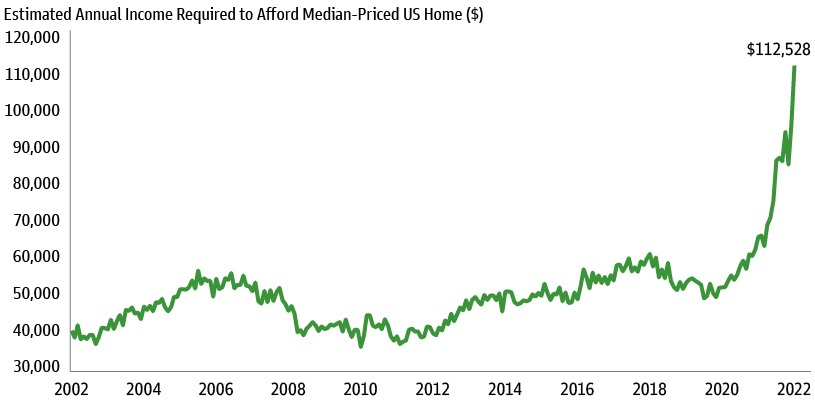

Speaking of housing, regardless of where you live, we've all seen how ridiculous housing prices moved since the start of the pandemic. Goldman Sachs sent this chart illustrating how difficult it is for the average American to afford a house. The median household income is just over $70K. Only 34% of American families make more than $100K per year. This will have longer-term ramifications for our economy.

Here's what our overall economic model looks like. If you look closely at the dashed line, you can see the sharp drop in the economy over the past month.

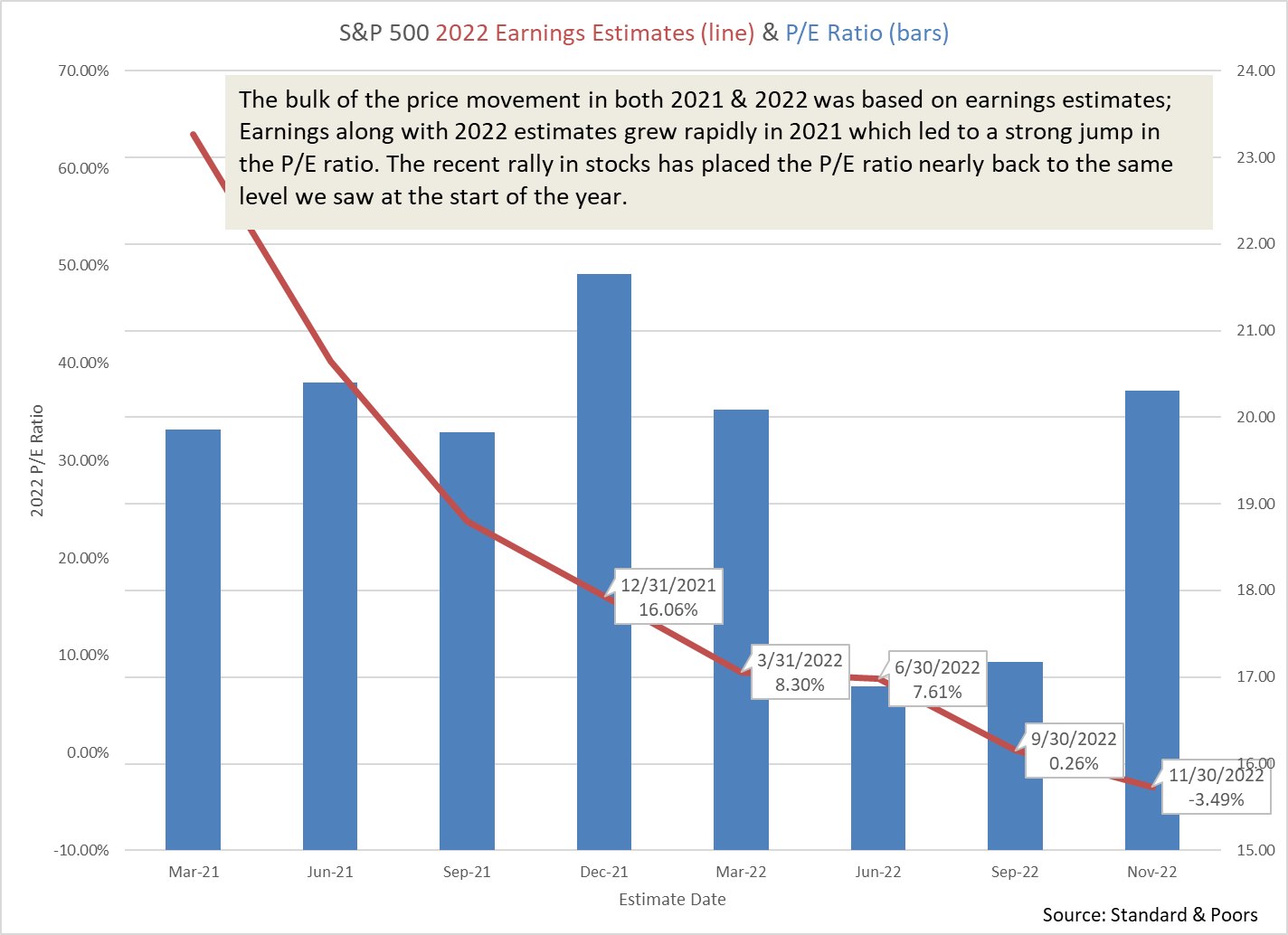

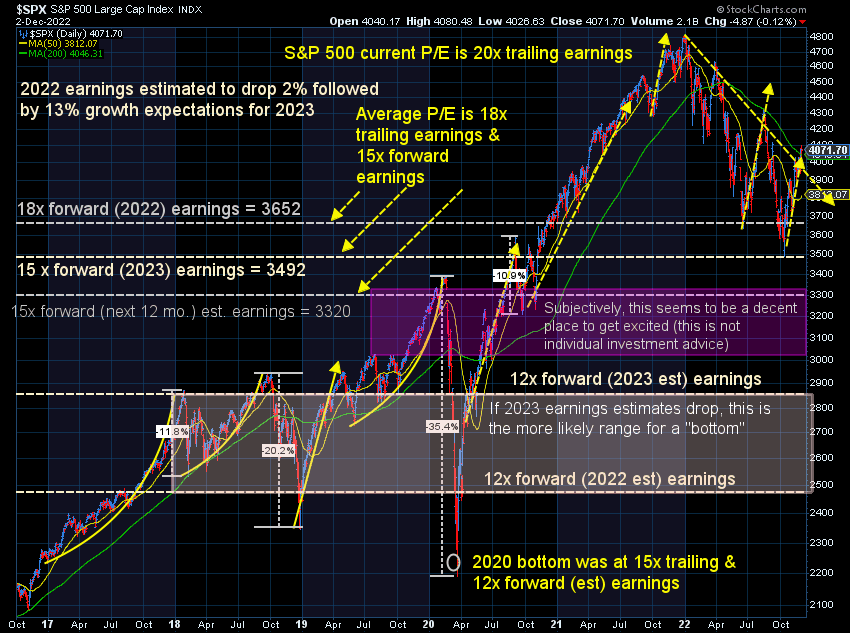

A slowing economy should mean lower stock prices as earnings will unlikely be able to keep up with current estimates. Right now, the market is priced for an INCREASE in corporate earnings. I'm not sure if that's a gamble I'd be willing to make.

Given our already "bearish" economic positioning (since April), there were no changes in our Dynamic models. Our "strategic" models allocated about half the cash we raised in February and March the last day of October, which remains where we are to start December. Our "tactical" bond models started stepping into high yield bonds a couple of weeks ago. Those positions remain in tact, but we've not received any additional buy signals since then.

Turning to the market charts.....

Stocks have had a nice run and technically still could move higher into the end of the year. It would make sense to see them first drop a bit to regroup given the magnitude of the move off the bottom.

The downtrend line was broken last week, and the market is just barely above the 200-day moving average. As mentioned above, the valuations are not attractive at all (unless you believe we're going to see strong growth in 2023).

Long-term bond yields have helped with the recent rally. Past stock rallies have seen similar declines in yields so it's important to not pre-maturely believe the worst is over for bonds. Subjectively, I believe if the economy is rolling over, we likely have seen the peak in TREASURY yields. It could be a different story for higher risk corporate bonds (and stocks) if that is the case.

Based on the data and our models, caution remains warranted. We're happy to see the market rally and will take any gains we can get to close out the year. That doesn't maintain our recommendation to be wary of any market rallies given the current economic outlook.