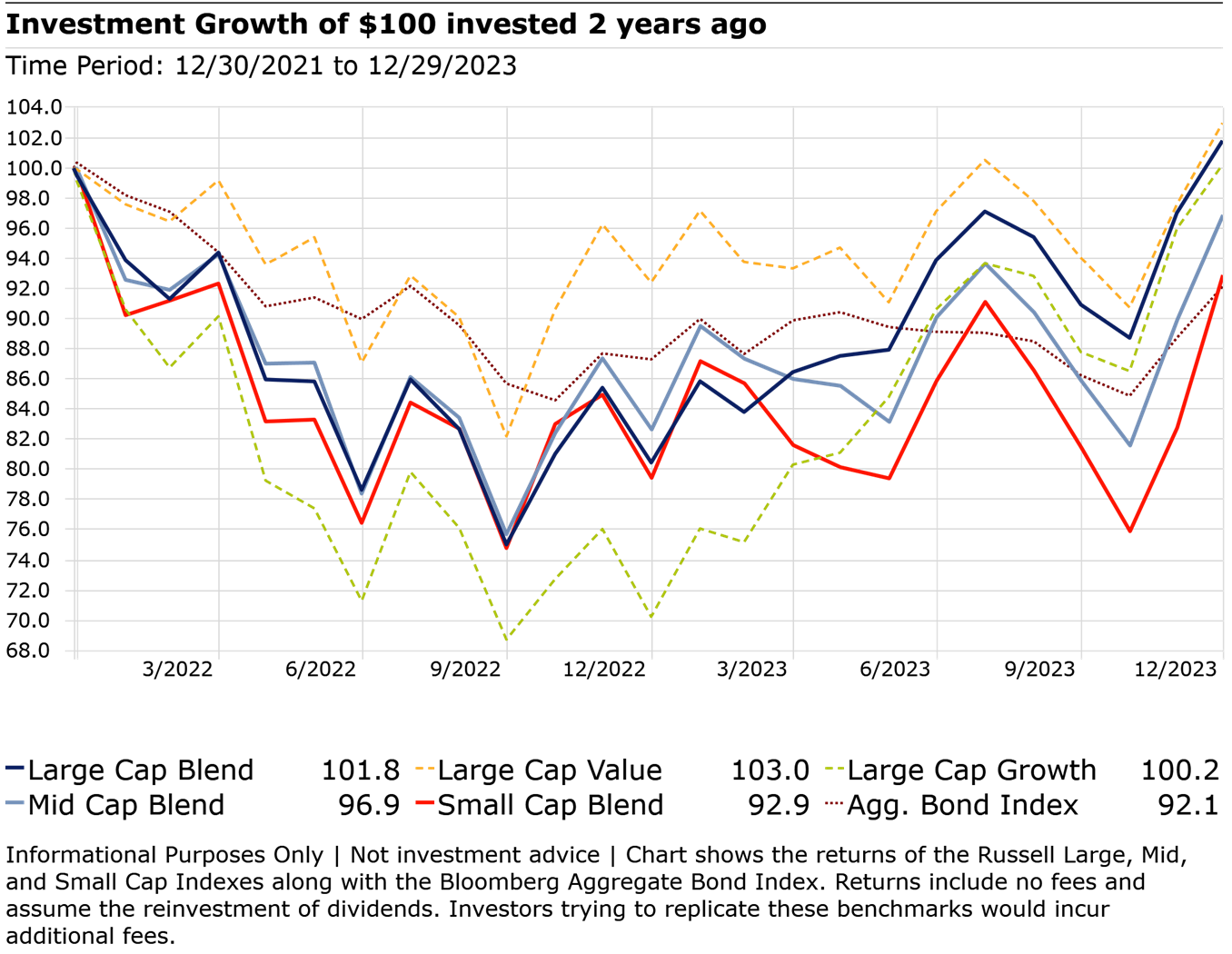

Stocks make a round trip

Each year many investors will take a look at their investment performance and reassess how and where they are invested. Often times they make the decision to sell their lowest performers to invest more in their best performers. This can be a big mistake. After being up over 25% in 2021, the stock market (as measured by the S&P 500 index) lost 20% in 2022. Stocks ended up the year up 26% in 2023 but we are simply back to where we were at the end of 2021.

This is a good way to understand the mathematics of losses. If you start with $100 and lose 20%, you then have $80. To get back to $100 you have to make $20 on your $80 so you have to earn 25% ($20 divided by $80).

Looking at various asset class returns, mega-cap growth stocks may have led the stampede in 2023, but over the two year period “value” actually outperformed “growth”. Small cap stocks are still down over 5% and bonds are down over 8%. Looking at just the past year can hide the longer-term experience. We encourage all investors to take a much longer-term approach when evaluating their investments.

If you would like a personalized review of your portfolio, go to Risk.SEMWealth.com

What’s in store for 2024?

In 2023, the Federal Reserve all but declared victory in their battle against inflation. The consensus view is that inflation is on its way to the Fed’s 2% target level and the economy will avoid a recession. While we at SEM would certainly hope that is the case, we know the market often gets well ahead of itself. Nobody knows for sure what we will see develop in 2024, but we do know where the market is focusing going into the year.

Our biggest concern for 2024 comes from the euphoric rally we enjoyed the past few months of the year. Most economists, including the Federal Reserve believe 2024 economic growth will be half of what we saw in 2023, yet corporate earnings are supposed to grow significantly above the long-term average. It is rare to see that happen.

For more discussion around the table above check out this post:

Stay up-to-date with the Traders Blog

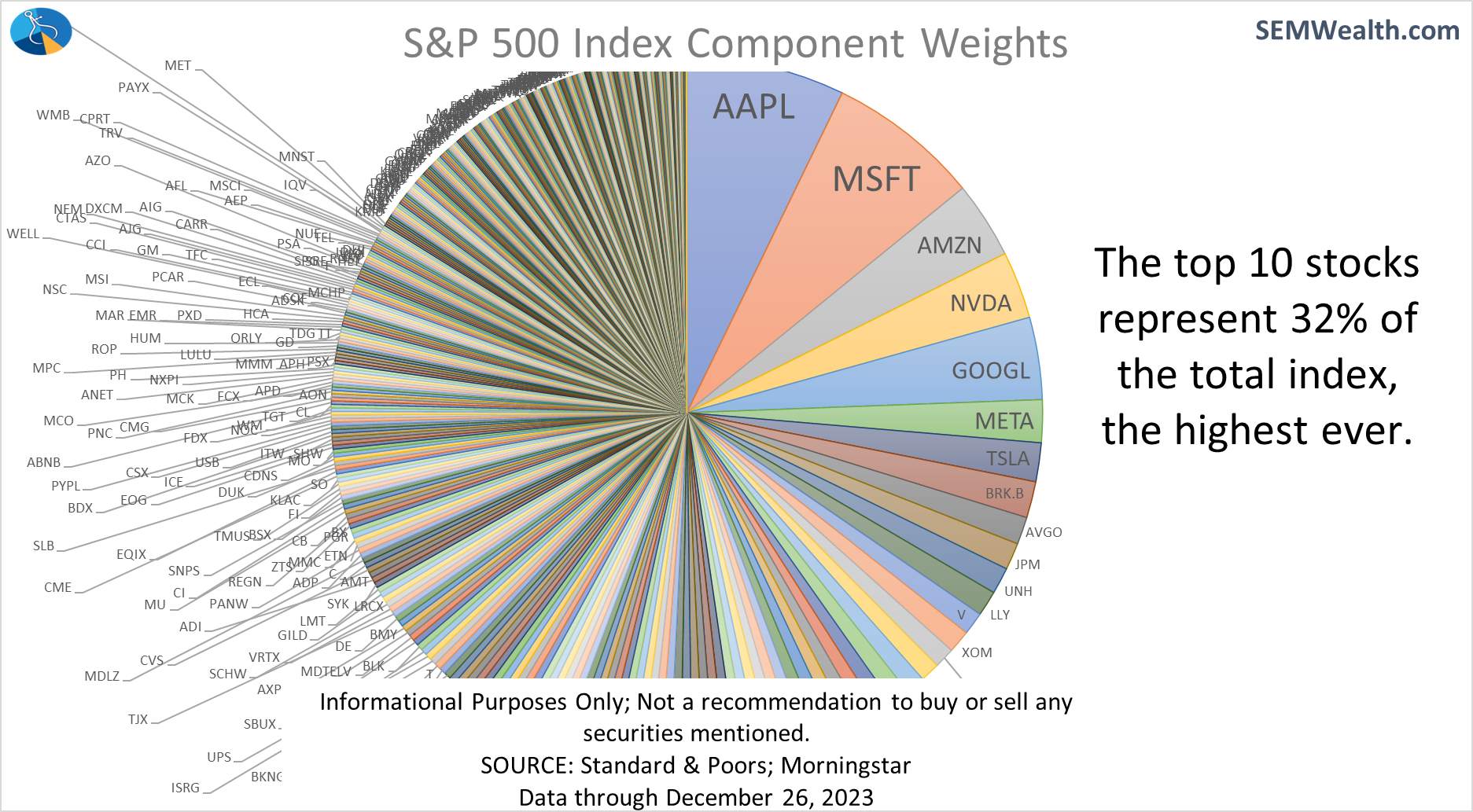

The focused technology index

What if we told you, we have 26% of your money invested in six technology stocks? As fiduciaries we would probably be fired. However, that is exactly what you are getting if you invest in the S&P 500 index. Many people believe the S&P 500 is a ‘diversified basket of stocks’, but there are times where the structure of the index puts way too much of your money in just a few stocks. The S&P is more concentrated than ever, exceeding even the months before the tech bubble. At SEM we take a much more diversified approach, which is why we do not believe the S&P 500 is a good benchmark to evaluate your investment portfolios. Our goal is to create a “smoother” ride over the long-term which means not putting too many ‘eggs’ in just a few stocks.

News & Notes:

2023 Year-End Tax Statements—what to watch for early 2024:

For taxable accounts, Axos Advisor Services will send your tax documents by February 15, 2024.

SEM strongly recommends you do not make your tax appointment until after February 15. Please wait until you receive Axos’s 2023 Consolidated 1099 prior to completing your taxes.

SEM will be posting additional information on the tax reports on our website: SEMWealth.com/tax-information

Online Bonus Content

Technology Topic: Why all these security things matter

We live in an online world where seemingly everything requires a username and password. Human nature leads us to find what in our mind is the easiest but still "secure" passwords. The problem is if you use the same username and password for all sites, it only takes one slip-up to have your digital life compromised. Last quarter in our technology topic we featured an article discussing password management. This time we want to include a blog from our Director of Technology talking about a real-life situation illustrating how all these security things can save our accounts from being compromised.

In case you missed last quarter's tech topic, you can read it here:

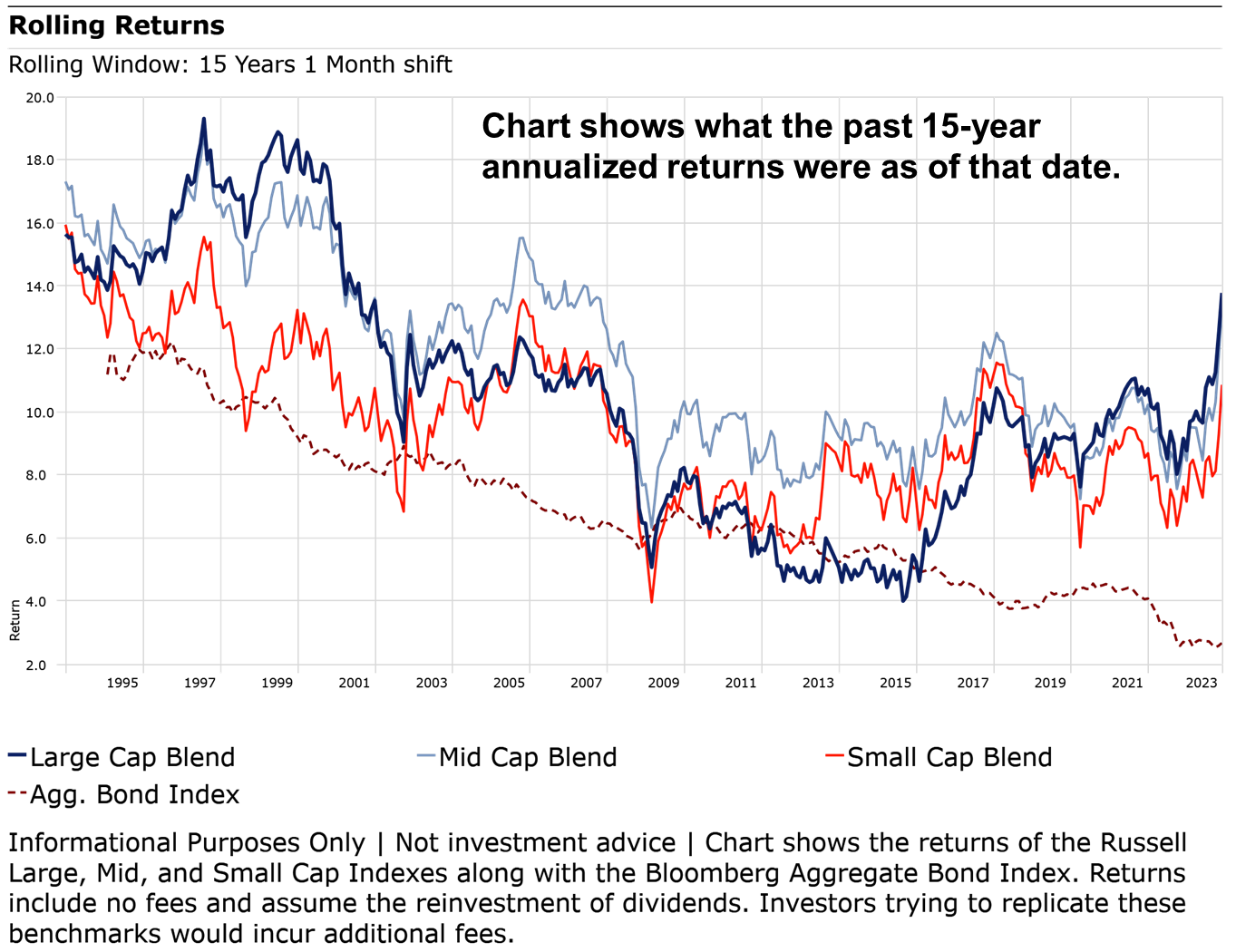

What 'long-term' return # should you use?

Above we talked about how over the past 2 years stocks have essentially made a "round-trip". The SEC requires investment managers to show "consistent" reporting periods to eliminate "cherry-picking" the best periods. Those periods – 1 year, 3 year, 5 year, 10 year, 15 year, and 20 year (if available) can sometimes give you misleading expectations. When the calendar rolled over to 2024, the 15 year period now starts at the beginning of 2009, meaning the "Global Financial Crisis" drop is not part of the evaluation.

Over the very long-term stocks have generally gained around 10%. However there have been periods of time where the 'long-term' (10 or even 15 year) returns have been much higher than that. There have also been times where they have been much lower than that. If you were using those 'long-term' numbers at that point in time you could have made a serious miscalculation in the best place to invest going FORWARD.

This chart shows the rolling 15-year returns for large, mid, & small cap stocks along with the Bond Market. You can look at any point in time to see what the posted 'long-term' return would have been. For example, when I (Jeff) began my career, the 'long-term' return for stocks was 15% and bonds were 12%!

Many people at the time (mid-1990s) were using 13-15% return assumptions for stocks and 8-10% for bonds as we rolled into the 21st century. Fast forward to 2015 and you see stocks returned around 4% annually and bonds about 4.5%.

The key question is what happens next? Unless it is truly a 'new era' and is 'different this time', most likely stocks and bonds will revert back to their 100-year 'mean', or 10% for stocks and 5% for bonds. How do they do that? That is the key question and something at SEM we will be monitoring closely.

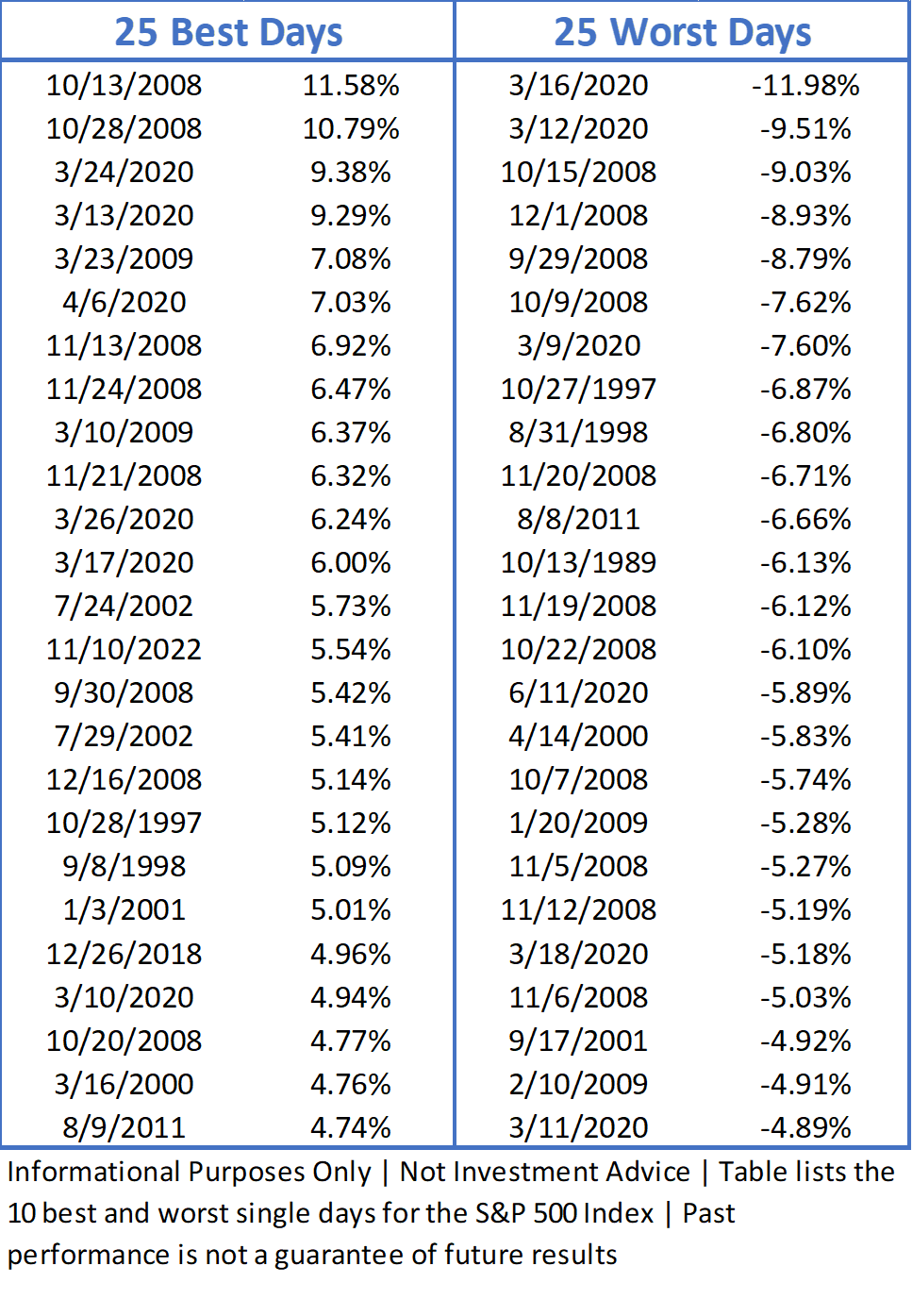

Missing the 10 Best Days.....

Most of you have probably heard the warning, "if you miss the 10 best days for the market your returns will suffer," (or something along those lines. While true, that statistic is misleading. We posted a blog discussing how nearly all of the BEST days occurred around the time of the WORST days (and almost always inside of a bear market or big market 'shock'.

The question we asked was, 'what if you missed the WORST days in the market?' The answer may surprise you. Check it out here:

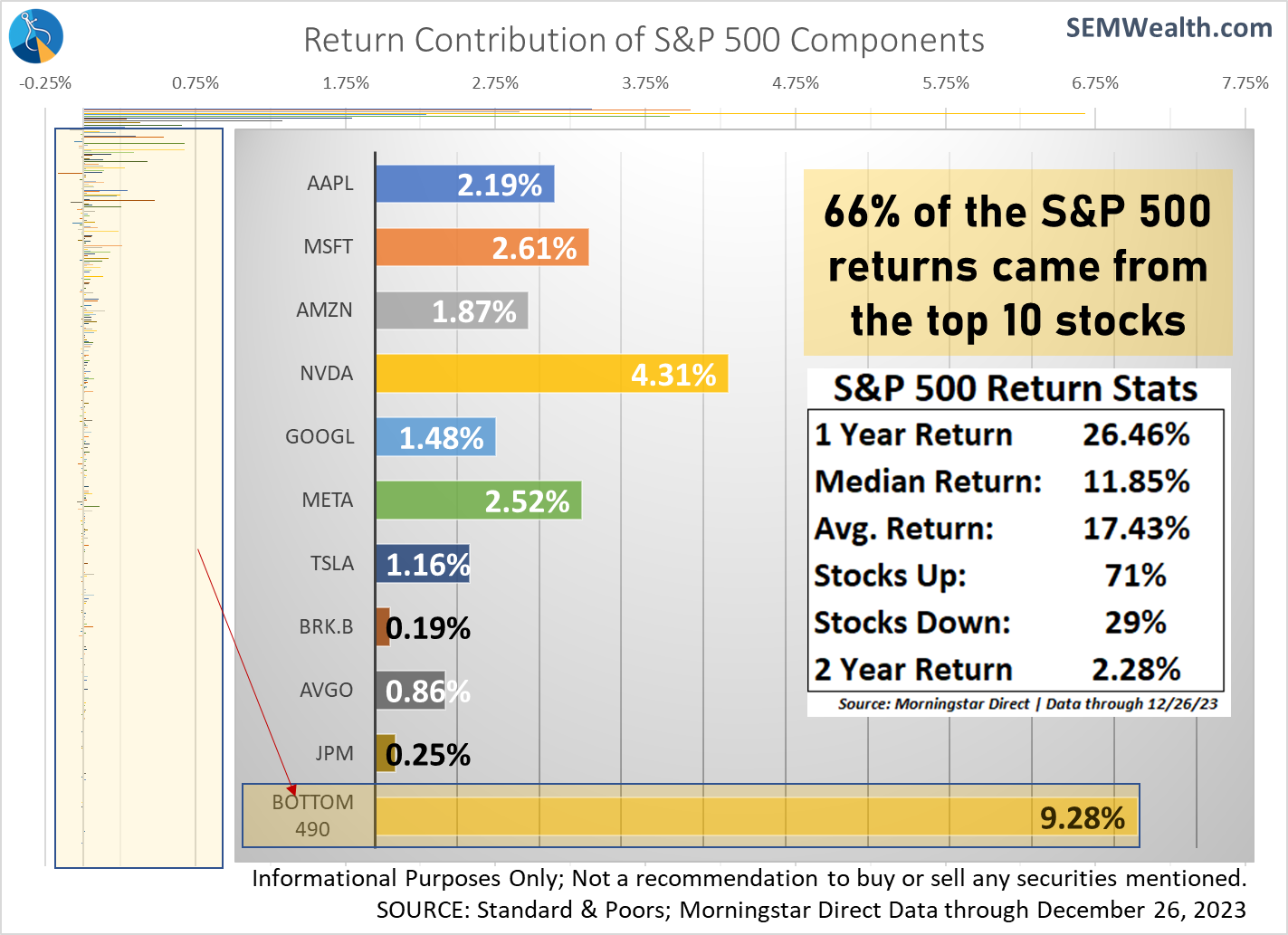

Just a handful of stocks

We mentioned above how the S&P 500 is the most concentrated ever (based on % of the index represented by the top 10 stocks. In 2023 any sort of diversification hurt performance if you are comparing that performance to the S&P 500. This chart shows how much each of the top 10 stocks contributed to the overall performance of the S&P 500. Note the only two non-technology companies in the top 10 (Berkshire Hathaway and JP Morgan) barely added anything to the returns.

Worst Crash of our Lifetime!

5 times in the last two weeks an advisor has forwarded me a question from a concerned client regarding this headline that has been circulating. It started on Fox Business (click here) and has since been circulating on various sites I consider 'click bait' (those who post sensational headlines to get you to click on it) such as Business Insider, Yahoo! Finance, TheStreet, and Market Watch.

I always consider the initial source of the article and then I go to CNBC, Reuters, or AP to see if they have anything about the same topic as I’ve found over the years they are the most ‘balanced’ politically. In this case, the fact they didn’t pick -up this 'news' was Strike 1 for me. [Side note, AllSides is also a great source to see which way the news source leans politically. Not saying one side is better or worse than the others, but it helps to know what the bias is in pushing the article to their readers.]

This reminds me of my Theme for 2024 – do not let your political opinions influence your investment decisions. Would this article appeared on Fox Business if the opposite party was in the White House? Probably not. Instead it would have been on MSNBC. Please, please, please keep in mind there primary focus – to scare you into not voting for the opposite party, which means creating an urge to DO SOMETHING with your investments. Do not fall for this! It doesn't always turn out how we think it might.

Strike 2 was when I saw who the “renowned economist" was…. Harry Dent. He is NOTROIOUSLY wrong about the economy. Here is an article from CBS talking about his track record.

Harry Dent and the chamber of poor returns - CBS News

Look, don't get me wrong. I've been quite outspoken about the 'everything bubble' and the long-term consequences we will pay when it comes crashing down. However, from a structural perspective, things are not as fragile as 2007, nor are things as ridiculous as we saw going into the year 2000, which means we are very unlikely to see the 'worst crash in our lifetimes'. This doesn't mean we won't see some big declines in stocks as we pay for all the "stimulus" since 2020.

My response when I receive this kind of slanted stuff:

The nice part about SEM is we don’t have to make these types of predictions. Right now the SEM economic model is already ‘bearish’ so it agrees that the economy is weaker than the markets. However, right now the longer-term trend is up so we are participating nicely in the market rally. When the trend reverses the systems are designed to take money off the table and wait for a better environment. No system is perfect, but the key is we don’t have to make calls on how and when things turn down. We know the market moves in cycles and use that to our advantage.

One thing I add – if you don't have SEM managing all of your investments, this would be a great time to do schedule a portfolio review so we can have SEM monitoring your entire portfolio for no matter what 2024 brings.

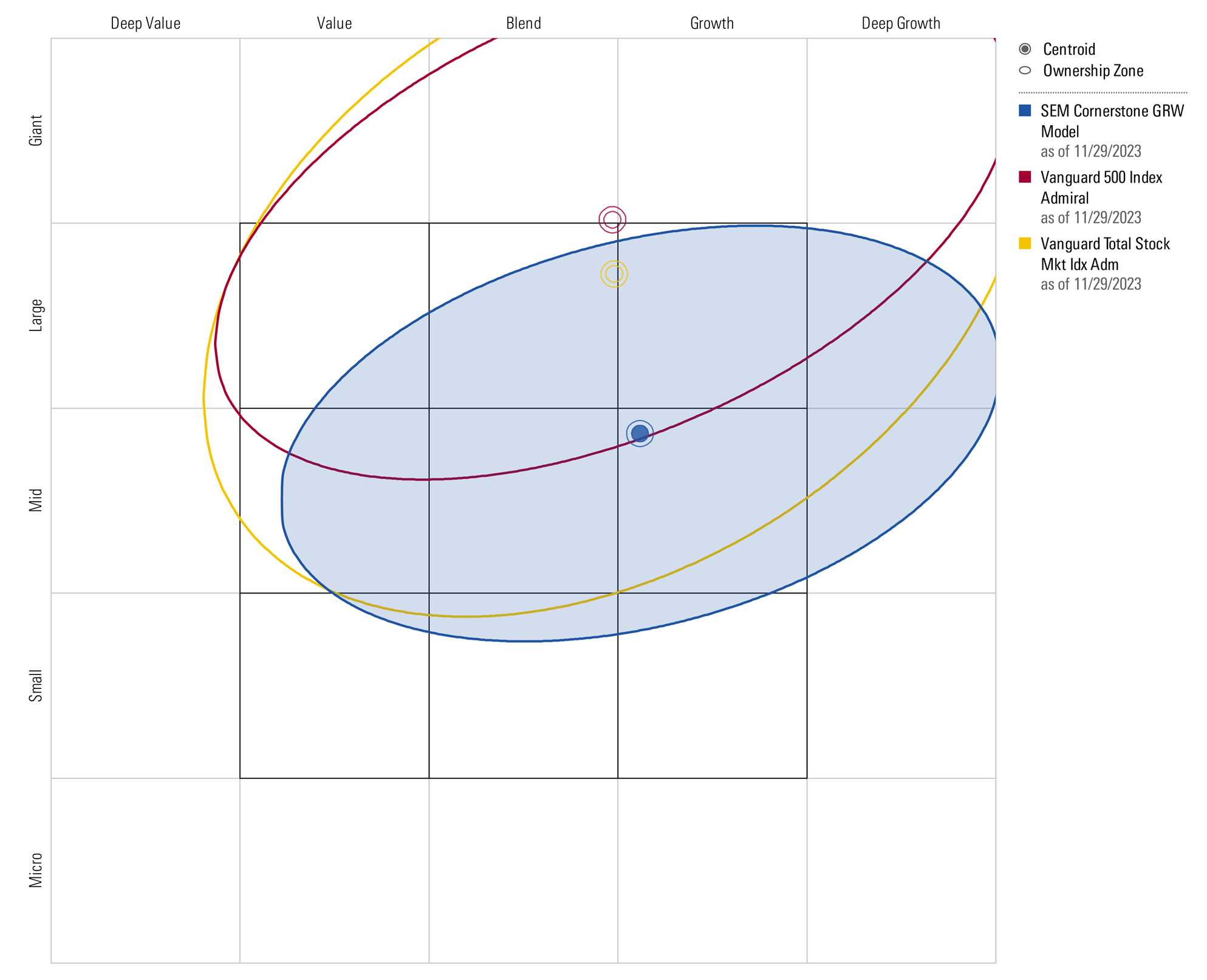

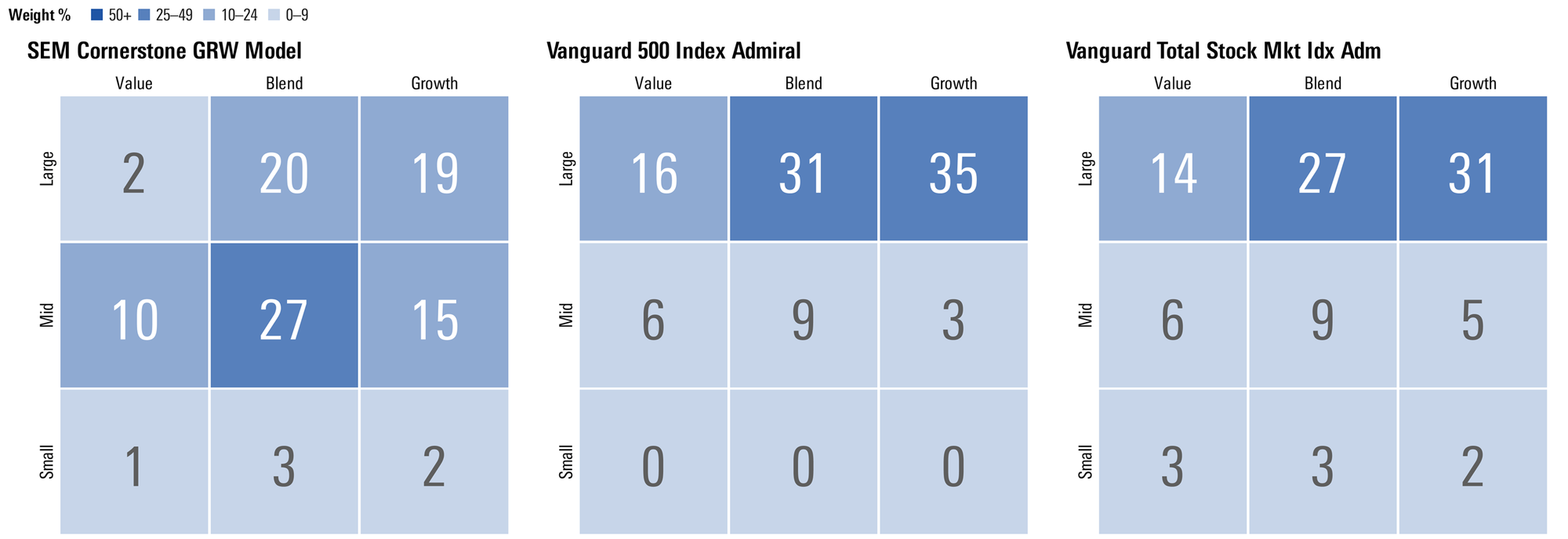

Understanding the Cornerstone Portfolios

Earlier this year we did a short update discussing the difference in the 'mandate' of our Cornerstone Portfolios and our AmeriGuard portfolios. [Click here to watch] In short, the investment guidelines of the portfolio eliminates a great deal of the 'mega-cap' growth companies that are currently dominating the stock market. When that happens, Cornerstone Portfolios will underperform.

The Morningstar 'style box' really tells the story in terms of asset allocation.

Comparing Cornerstone to the "broad" market, you can see how much more diversified a Cornerstone portfolio is.

Over the long-term, history tells us those assets that get too far 'above average' revert back to their mean by underperforming. Those assets that are too far 'below average' revert back to their mean by outperforming. As we said earlier with respect to the ability for mega-cap growth stocks to continue dominating, unless it is a 'new era' or 'different' this time, we should expect a 'mean-reversion' in the coming years, which bodes very well for portfolios invested outside of the mega-cap growth space.

Download/Print version of the Newsletter

What is ENCORE?

ENCORE is a Quarterly Newsletter provided by SEM Wealth Management. ENCORE stands for: Engineered, Non-Correlated, Optimized & Risk Efficient. By utilizing these elements in our management style, SEM’s goal is to provide risk management and capital appreciation for our clients. Each issue of ENCORE will provide insight into investments and how we managed money.

The information provided is for informational purposes only and should not be considered investment advice. Information gathered from third party sources are believed to be reliable, but whose accuracy we do not guarantee. Past performance is no guarantee of future results. Please see the individual Model Factsheets for more information. There is potential for loss as well as gain in security investments of any type, including those managed by SEM. SEM’s firm brochure (ADV part 2) is available upon request and must be delivered prior to entering into an advisory agreement.